courtneyk

I first wrote about The Trade Desk (NASDAQ:TTD) in the height of the initial Covid pandemic. I described it as a generational opportunity, despite its valuation. My thought was that cord-cutting has been a theme for years now, but the pandemic was effectively pulled forward trends that already existed in connected TV or CTV, digital advertising, and overall usage for many of the tech companies.

Seeking Alpha

Well, TTD shot up like a rocket, but has come back to Earth quite a bit since then. It’s still beating the market, and my long-term thesis is intact for the company. However, it really is the wild west out there right now in the digital advertising landscape.

Company Presentation

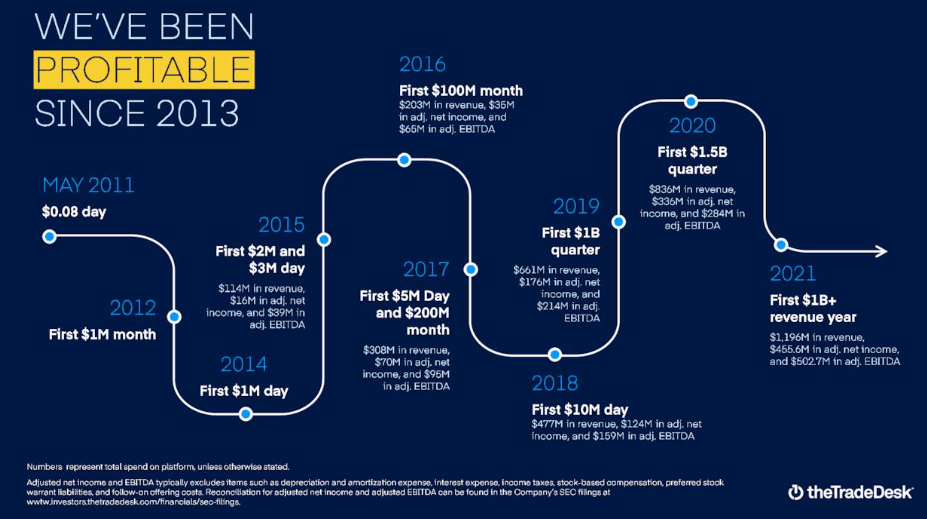

Looking at the numbers, it’s obvious why you should be interested in TTD. This is a relatively young high-growth company, operating in a fragmented space, and doing so profitably with an eye towards strong stewardship of shareholder capital. Despite the blistering revenue growth rates, the company has maintained profitability, hasn’t taken on any long-term debt to speak of, and hasn’t increased its share count meaningfully in years. I added emphasis to that because it’s so uncommon. The company is funding its own growth with cash, and as a shareholder, you aren’t being diluted to death as time goes on. There may be other good examples, but I haven’t found a ton.

Looking below, the key metrics are all pointed in the right direction. The company is growing faster than the overall advertising market. The CEO discussed on the earnings call that WPP’s Group M predicted worldwide advertising would increase 8.4% in 2022, and TTD grew three times that. The opportunity is immense. Streaming platforms are increasingly shifting to ad-supported tiers in an attempt to drive meaningful profitability. The landscape is shifting, and companies like Disney (NYSE:DIS) are having difficulties justifying the cash-burn on content and subscriber growth-at-all-costs. With the balance sheet showing dark red on Disney+, expect to see ads across your streaming platforms unless you’re willing to pay up in the future.

Company Presentation

Where does that leave TTD? In a great spot. The company is set to benefit from this shift, but the future remains uncertain. In just the past few years, massive seismic shocks have rolled through the digital advertising space. Google is set to discontinue third-party cookies in 2024, Apple has made great strides with Safari and increasing user privacy, as well. The landscape has shifted, and advertisers have to change with it. The way I’ve thought about it is this – it’s unlikely that online usage will result in no available user data for targeted advertising. However, the old framework raised several valid concerns about the way it was gathered, whether the user knew, etc. As we move forward, and the market develops, there are other options that can maintain user privacy while still allowing targeting by advertisers based at the very least on demographics.

Company Presentation

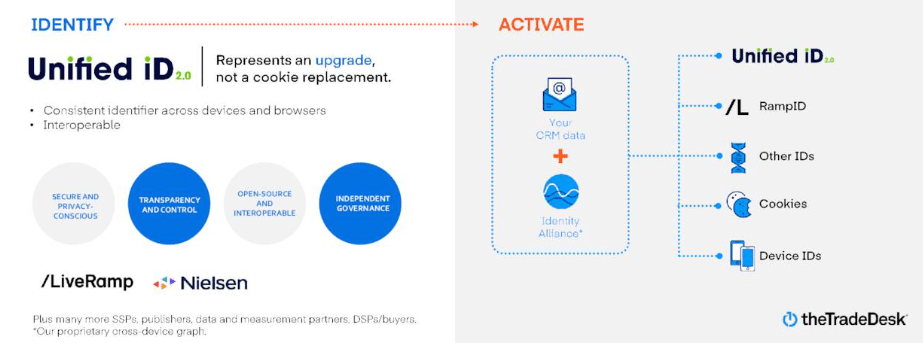

Enter UID 2.0, an initiative from TTD. It isn’t the only company attempting to fix this problem, and isn’t even the market leader based on a survey of the space by Advertiser Perceptions in 2021. At the time, LiveRamp’s offering had about 17% of the market share, Google (NYSE:GOOGL) sat at 13%, and TTD 12%. Like I said, it’s still the wild west. That being said, TTD doesn’t make money off of UID 2.0, and sees it as an initiative to improve the space overall. It links a user’s email or phone number data anonymously into an encrypted identifier that follows the user around the internet. This allows the identifier to maintain user privacy, while still effectively doing what cookies did in tracking the user’s interests. I’m sure there can be some great debates about privacy in the digital age, and the ethics of each company’s solutions, but ultimately I’m looking at TTD as an investment, and this appears to be a better solution than what exists now as the market matures.

It’s vital for TTD and other ad-tech companies to be able to measure ad spend. The value proposition for digital advertising is increased visibility for company’s ad dollars. With a targeted, programmatic ad campaign, the company’s CFO wants to be able to understand the money was well spent, and actually drove returns. I’ll add some perspective here from Jeff Green, the founder, on the most recent earnings call:

One of the key factors in our progress with UID2 has been our success with the world’s leading data aggregators such as AWS, Snowflake, Salesforce, Adobe and many, many others. Put simply, these companies house the first-party data of the world’s leading advertisers. With UID2, advertisers can transact on that data without it ever leaving home. Because of this progress, I predict that more than half of the data inventory flowing through our platform by early next year, will be UID2 tag.

With more and more of our publishers’ inventory also UID tagged, that means the value of advertiser first-party data increases exponentially on our platform, more than 10x next year compared to this year. With this progress, the strategic value of UID2 in helping advertisers drive relevance in a privacy-centric manner becomes undeniable. While most of our advertisers are already transacting on UID2 on our platform in some way, I expect they will fully embrace it next year, because we have done the hard work on the data and the inventory side, advertisers now have every incentive to fully unleash the first-party data in a way that will supercharge their campaigns. They will finally be able to realize the value of their first-party data to model and understand where their next generation and most loyal customers are and reach those customers with precision, and of course, do that more effectively than ever. This gives me tremendous confidence for 2023 and beyond.

Company Presentation

The company is also launching Galileo, a data solution which combines many of the offerings the company offers into a CRM solution to connect user ID’s and among other things allow for frequency capping. Have you ever watched a show on a streaming platform like Hulu and gotten the exact same advertisement over and over again? I haven’t seen it in a while (thanks, ad-free tier), but it was infuriating when it happened. This offering is supposed to fix that. When the ad spot is filled, it is able to link who it is actually being filled for, and whether they have seen that exact same advertisement already. Good for the user, and good for the publisher. It was a waste of money, otherwise.

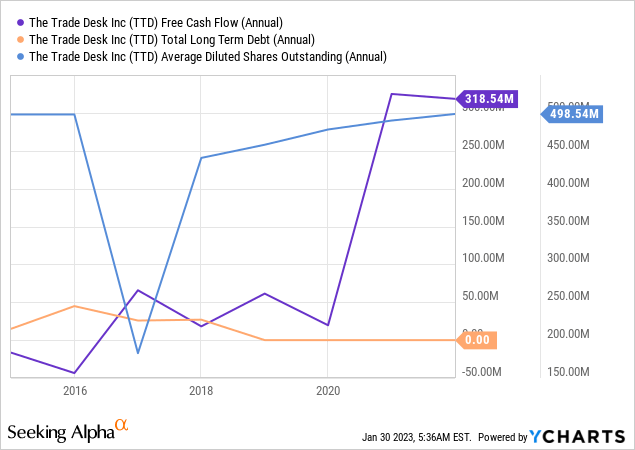

Looking at the most recent quarter, the company managed 31% revenue growth with 32% expense growth effectively in-line. The company drove 53% free cash flow growth over the trailing twelve months to $500M, and currently has $1.3B on-hand and no long-term debt. All-in-all, this is just further confirmation that the company continues to execute well on its initiatives. If you’re a shareholder and you don’t listen to the earnings calls, do yourself a favor. Jeff Green, founder and CEO, is passionate about this company, and is a terrific salesman, here’s an anecdote he shared on the most recent call:

You only have to look at a couple of comments made by the CFO of P&G during the most recent earnings call a couple of weeks ago. As you may know, Procter & Gamble is one of the world’s largest and most progressive advertisers. He said, and I quote, “it is difficult to describe media sufficiency in dollars, especially when we are actively shifting our spending from linear non-targeted TV into programmatic and into digital spend. That is a lot more targeted and a lot more precise in terms of delivering reach and quality of reach where we need it. We now have more than 50% of our media spend in digital. We are increasing our first-party data and our digital capabilities to increase precision of reach, not only in the U.S. or in Europe, but around the world and that is allowing us to drive significant productivity while increasing reach while increasing quality of reach and while more precisely targeting our consumers.”

One development since I last wrote on TTD is the lengthening of the company’s MSA’s with customers. As the company signs 2-3 year vice the traditional 1-year, it will provide some additional predictability while allowing the company to better tailor the offering over time. This could result in some level of moat.

As I mentioned before, this sector is the wild west. There is no clear winner yet, although Google is the dominant force in digital advertising overall. The path forward isn’t perfectly clear for TTD, and is beset with huge amounts of execution risk. However, while keeping a close eye on the company’s results, we could see something of a network effect unfold here. As UID 2.0 increases adoption, and TTD becomes more and more of a dominant player in advertising, it just becomes more likely to win future contracts on the demand-side. The company has tie-ups with Peacock, fubo, Paramount, and now Disney, and streaming is moving towards more and more ad-supported tiers. The future is bright for the company, but this isn’t a set-it and forget it type stock.

Although TTD is worldwide in reach (around 10% of revenues outside of US), and operates across effectively every industry, its revenues are tied to overall economic health. If companies cut ad spend, it will negatively impact the company. Keeping that in perspective, there aren’t all that many truly recession-proof companies, so this isn’t a specific risk to TTD.

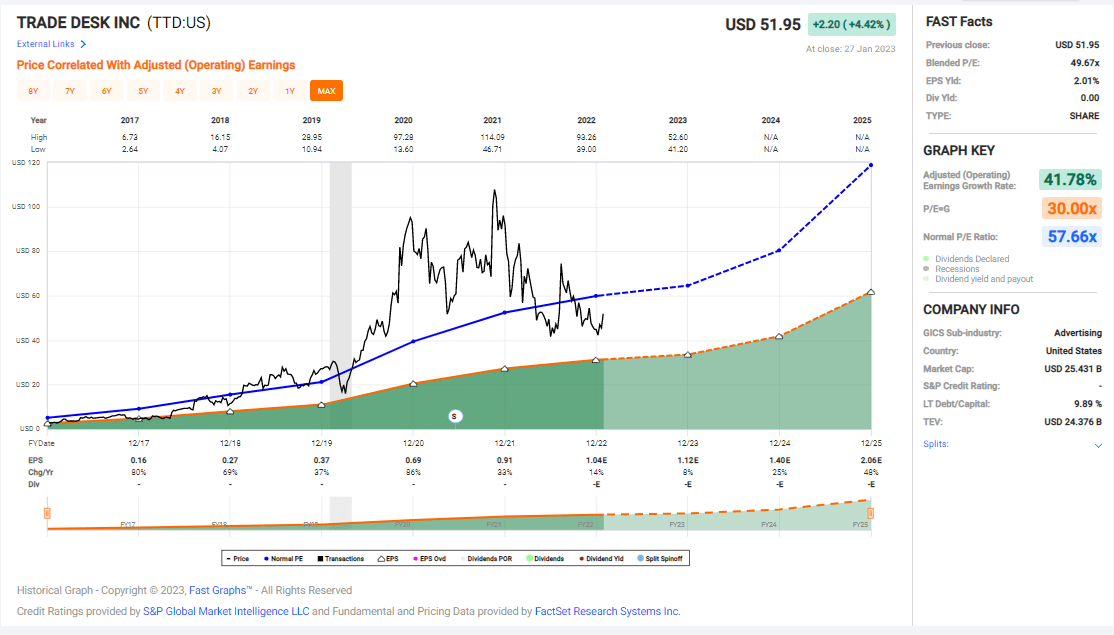

FAST Graphs

Looking at the company’s valuation, it’s no surprise that it’s expensive. It’s currently trading around a blended P/E ratio of 50X. However, earnings growth is solid, and looking into the future, this is the type of company that could easily grow its way into looking cheap from this entry point. Considering the growth since the last time I wrote about the company, I don’t see the valuation as a particular problem for an investment thesis.

FAST Graphs

I’m using this analyst projection, but I want to put in a disclaimer ahead of time. When you’re buying a growth company like this, valuation expansion and compression can happen at the drop of a hat. Don’t anchor yourself to these numbers at all. However, if the company were to maintain its current P/E, we are looking at 25% earnings growth and therefore annualized ROR into the next few years. Something as simple as material news dropping about Google’s DOJ investigation could send this stock screaming in either direction. As for me, I’m along for the ride. TTD is a buy.

Be the first to comment