undefined undefined/iStock via Getty Images

Investment thesis: There are signs of increasing financial stress while the Fed is hiking rates. This is not the time to invest in small caps.

Due to the rise of data showing that active management performs poorly over the long term, investors now use ETFs as the backbone of most portfolios. These funds allow investors to target broad sectors of the market, like the IWM which tracks the Russell 2000.

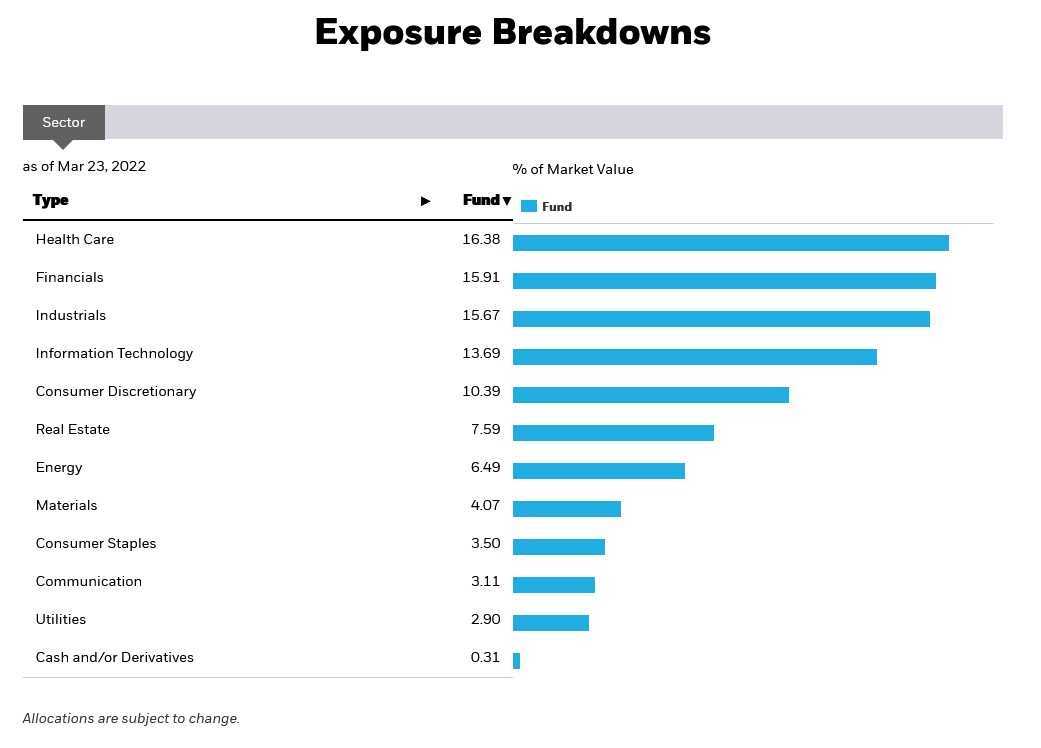

The IWM is issued by iShares. Here are the sector percentage holdings:

IWM sector percentages (iShares)

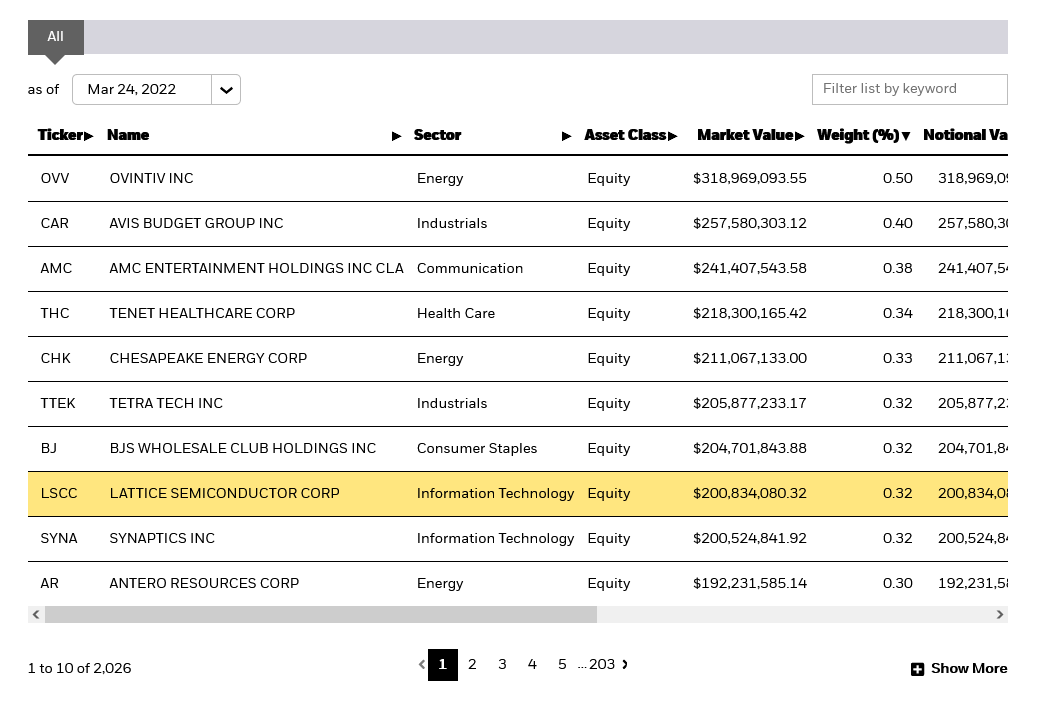

And here are the 10 largest holdings:

IWM 10 largest holdings (iShares)

For additional information, please click here.

The Russell 2000/IWM is comprised of smaller, growth-oriented companies which need swift economic growth. Unfortunately, the economy is starting to face headwinds.

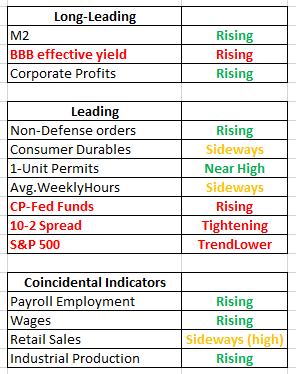

Let’s start that discussion with this table:

Long-leading, leading, and coincidental indicators (Author’s calculations)

The above uses the long-leading, leading, and coincidental economic indicator methodology developed by Arthur Burns and Geoffrey Moore. Note that financial indicators are starting to show increased stress and pressure.

Let’s look at the charts in more detail.

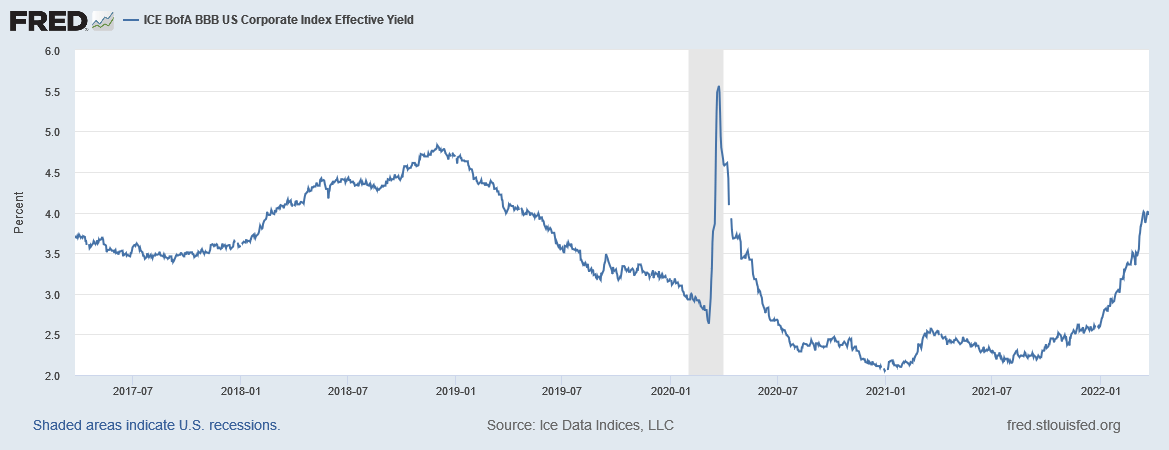

BBB effective yields (FRED)

BBB yields are at the key line separating junk and investment grade. They start to sell off when investors believe that credit risk is rising. Yields have increased sharply in the last six months.

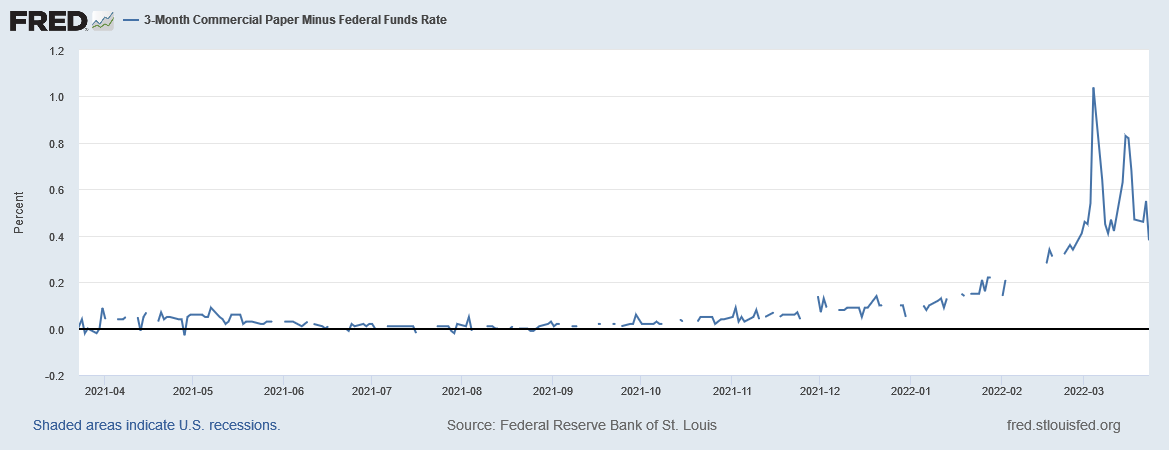

Corporate paper-treasury spread (FRED)

The short-term funding market is a little-known and seldom discussed area of the credit market that only has problems before recessions. The above chart shows that this market is starting to have liquidity issues.

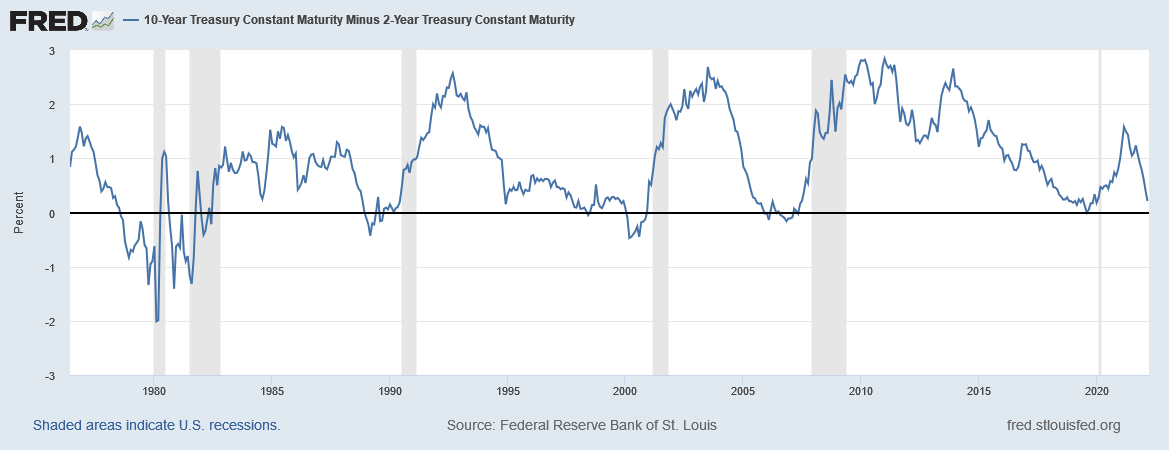

10-2 spread (FRED)

The 10-2 spread is a solid recession predictor. While the curve didn’t contract before the last recession, that was an economic special case. In all other times, a contracting yield curve occurs before a recession. The curve is almost there.

Add in the following factors:

- The war in Ukraine is once again crimping global supply chains.

- The war is also causing spikes in commodity prices, which is adding to inflationary pressure.

- The Russian oil embargo will likely lead to a recession. That’s the conclusion from the Dallas Fed in a recent research note:

- “If the bulk of Russian energy exports is off the market for the remainder of 2022, a global economic downturn seems unavoidable,” economists Lutz Kilian and Michael Plante wrote in an article posted by the Dallas Fed Tuesday. “This slowdown could be more protracted than that in 1991.”

- Not only is the Fed hiking rates, but several Fed Presidents are advocating for a 50 basis point hike.

- Powell: Federal Reserve Chair Jerome Powell said the central bank is prepared to raise interest rates by a half percentage-point at its next meeting if needed, deploying a more aggressive tone toward curbing inflation than he used just a few days earlier.

- Bullard: Asked how quickly the Fed should move, Bullard said “faster is better,” adding that “the 1994 tightening cycle or removal of accommodation cycle is probably the best analogy here.”

- Mester:

Fed President Mester on rate policy (Twitter)

Add up all these factors, and there’s plenty of reason to move away from small-caps and into larger companies.

Finally, here are the charts:

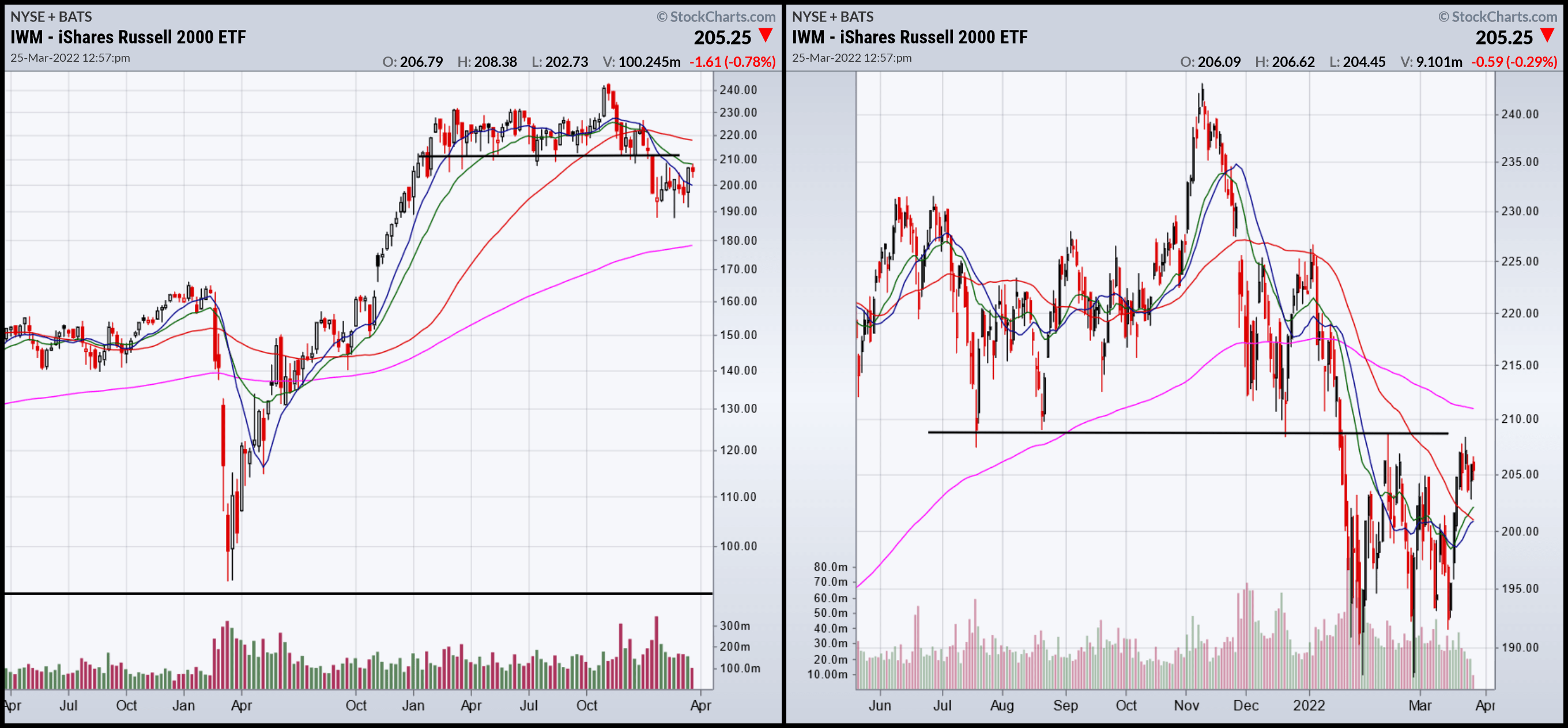

IWM weekly and daily (StockCharts)

The weekly chart (left) shows that prices spend the better part of last year consolidating sideways. The daily chart (right) shows that prices are below the 200-day EMA and are consolidating below key levels.

We’ve clearly moved away from a small-cap orientation to a large-cap focus. It’s time to look for greener pastures.

Be the first to comment