davidrasmus

Introduction

I don’t write many macro articles on Seeking Alpha because most of the time I don’t find macro articles very actionable (or accurate), and therefore not very useful to readers. Because of that, I tend to integrate my macro view into my expectations for individual stocks. But this is the time of year when strategists put out their obligatory estimates and predictions for the new year, and I was invited by Seeking Alpha to share my views, so I decided, what the heck? I’ll give my 2023 outlook.

The most important thing I want to stress, though, before I get properly started, is that where the S&P 500 ends in 2023 is much less important for investors to estimate or predict than where the S&P 500 ultimately bottoms. If you have a rough idea of the bottom, you can then create a strategy that is anchored to that expectation. Where the market ultimately ends up on a specific date, like year-end, is much less important (and virtually impossible to predict), but I will include my thoughts on that as well since those were the guidelines for the article.

The second most important thing I want to stress is that I am mostly an individual stock picker. This means where “the market” as a whole goes isn’t all that important to me. There can be individual stocks and groups of stocks that do reasonably well even if there is an extended or deep bear market, just as there can be stocks that perform poorly in a bull market. Those groups of individual stocks and how they are valued are much more important to me than the market as a whole.

That said, my wife’s 401k has limited investment options (as do other saving vehicles like 529 plans), and I can’t buy individual stock in those accounts. So, there are situations where broad market expectations can be very important to how one manages these types of restricted investments. These are the types of accounts I’ll have in mind for this article, and I’ll share the approach I’m personally taking with them at the end of the article so that we do indeed have an actionable conclusion and not just rough guesses at what the market might do next year.

Interest Rates & Fiscal Stimulus

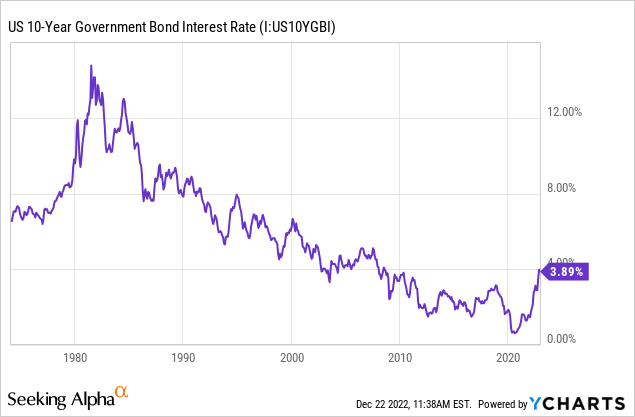

One of the most important things investors need to realize for 2023 is that the Federal Reserve is unlikely to come to the rescue of the stock market. Inflation is currently much higher than interest rates are. Part of that inflation will indeed be transitory as stimulus money runs out and the prices of goods come down, but part of it is caused by things like demographics, immigration (or lack thereof), and deglobalization. Those parts will likely be less transient, which means they won’t go away without a recession. This rate dynamic has not been experienced for more than 40 years in the US, and that period was a disaster for many parts of the US economy when the Federal Reserve back then raise interest rates and kept them high during a recession.

Unlike 40 years ago, when the Fed raised rates to ridiculously high levels, this time around, the Fed is simply normalizing rates back toward the historical average, though. So I think investors’ base interest rate expectation should be a 10-year Treasury yield of about 4%. The Fed might push it higher, but 4% to 5% makes sense to me as the old normal.

That would put us somewhere around where rates were in the early 2000s before the Great Financial Crisis. The key here is that we should not expect rates to come down to 2009-2021 levels unless there is a very bad recession, in which case the stock market will have crashed deeply from today’s levels.

With the Fed out of the way as a market savior, next, we need to turn to the federal government, which was the key provider of fiscal stimulus in 2020 and 2021, and to a lesser degree in 2022. 2022 saw the continuation of the federal student loan repayment pause. This prevented a massive drag on the economy from occurring in 2022 if people would have started paying their loans back. This issue is now likely to be decided by the US Supreme Court by the summer of 2023. I have no idea how the court will rule, but if they strike down the loan forgiveness it will probably put the US into a significant recession within one or two quarters. This is a serious downside risk to the market in the second half of the year.

During the mid-term elections, Republicans won back control of the House of Representatives. The Republicans have no political incentive to help the economy ahead of the next election in 2024, so they will likely be unwilling to issue any more stimulus. If the economy collapses or stagnates, that is good for them politically. This means that, unlike every crisis we’ve had since, well, I can remember, the central government should not be counted on to help. This increases market risk.

When I put all this together, what I see is interest rate conditions returning to near the long-term average. And the long-term average multiple of the S&P 500 is about a 15 P/E ratio, so that is what I will assume the market will gravitate towards over the course of this year. The current P/E ratio is about 19. If that 19 P/E reverts to a 15 P/E in one year’s time, it will produce about a -21% decline in the S&P 500 index if earnings stay the same.

To summarize:

- The Fed is likely to return to “normal” interest rate levels, where short-duration cash and bonds yield a little over core inflation, and longer-duration, yield a little more than that.

- Some inflation will indeed be transitory and come down. But, demographics, immigration, and deglobalization, will keep the base level higher than it has been for the past 20 years when these factors actually contributed to deflation.

- The Fed will only lower interest rates in the case of a bad recession and deflation. So, there will be no help for the stock market from the Fed after a -20% drawdown. It will take more like a -50% drawdown in the stock market for the Fed to act.

- The central government is split, and there are incentives for gridlock, which means little or no government stimulus for the next two years.

- The Supreme Court will rule on student loans. No matter what happens there, some loans will start to be paid back, but it could end up that all loans will need to be paid back, which will trigger a recession, or turn a mild recession into a worse one.

- The S&P 500 will likely move toward the long-run average 15 P/E ratio, rather than the inflated P/E ratios we’ve seen in recent years. That would produce a -21% decline in the market from here.

Now Let’s Talk About S&P 500 Earnings

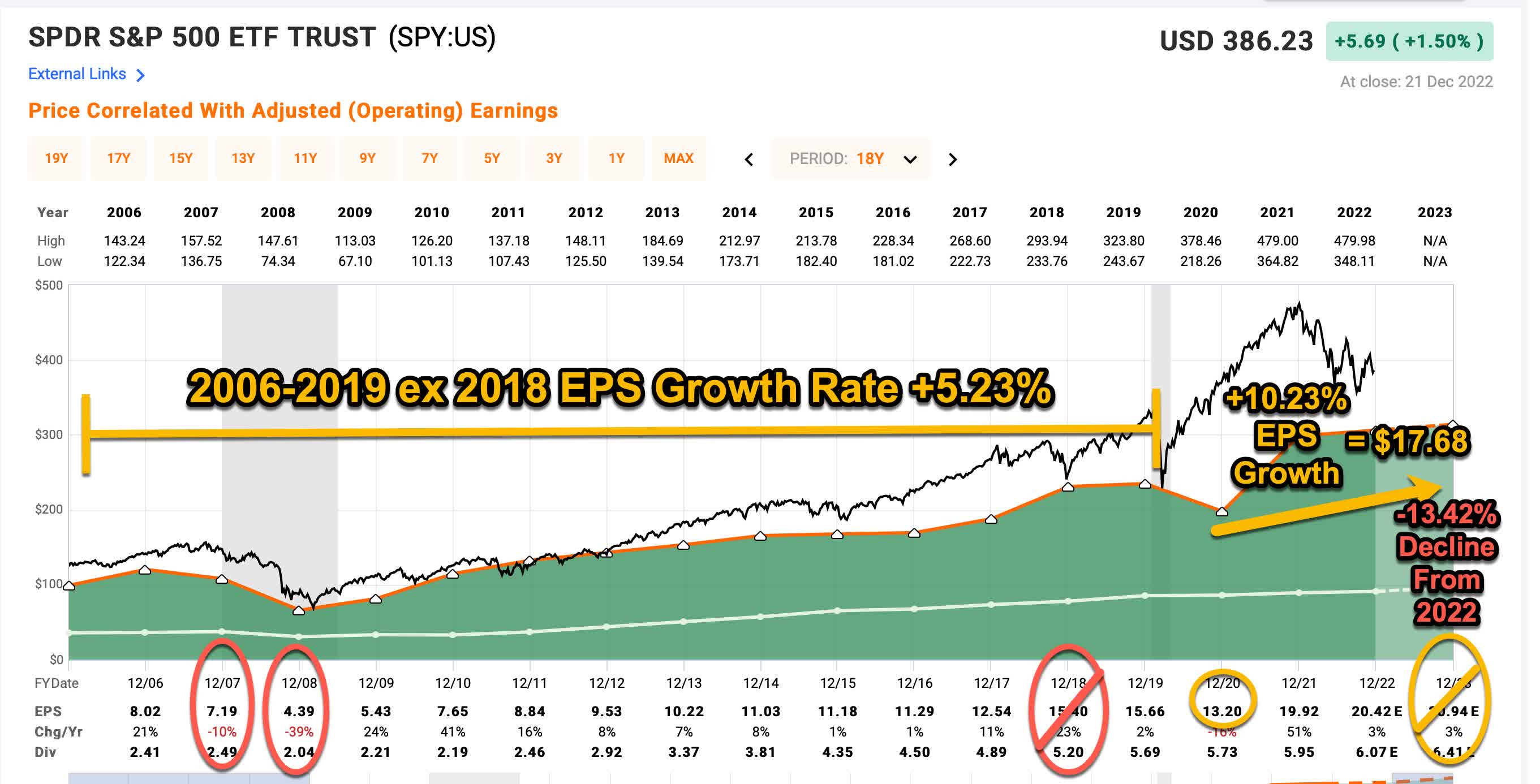

I will use the ETF (SPY) to estimate the likely EPS decline percentage, and then after I do that, I will apply that to the index itself.

FAST Graphs

Alright, the way I’m going to estimate earnings growth next year is a little complicated but it shouldn’t be too hard to follow along. Let’s start with the assumed earnings growth rate first. My basic method is to take the EPS growth rate from the previous cycle, which by my way of thinking starts in 2006, and use that growth rate as the baseline expectation for the future. There are four factors, however, that I make adjustments for. The first is negative EPS growth years. I calculate my EPS growth rate by taking the total earnings collected over a time period and converting that into a CAGR based on how many years we are measuring. So, I account for the down EPS years of 2008 and 2009 rather than just measuring, point to point, from 2006 to 2019. The second thing I adjust for are the corporate tax cuts in 2018. Those were one-time events that benefitted earnings growth a lot but are unlikely to happen again next year, so I simply omitted 2018 from the data set. Third, is the negative growth rate caused by the pandemic in 2020. That is unlikely to repeat as well, so I end the range of measurement at the end of 2019 (so I am measuring the EPS growth rate from 2006-2019 ex 2018). And the fourth issue is the earnings growth in the past two years, which was heavily influenced by stimulus money that has since gone away. (More on this in a moment.)

From a period of 2006-2019 ex 2018 I get an earnings growth CAGR of +5.23% for the SPY, so that is my baseline earnings growth expectation. In order to account for the stimulus money that is still floating around in the economy, but not assume we will get more stimulus money, for the years 2021, 2022, and 2023, I will assume the S&P 500 earnings will grow +5.23% as it would have on average without stimulus and also an additional 5% to account for above average inflation, for a total earnings growth rate for 2021-2023 of +10.23%, building off 2020’s SPY EPS of $13.20 per share. Put more simply, I assume that $13.20 worth of earnings grow at a +10.23% rate for three years, and that is probably where 2023 earnings should be without continued stimulus money, but taking into account the stimulus money already in the economy.

When I do the math on that I get $17.68 per share of earnings for SPY in 2023. This year, in 2022, SPY is expected to earn $20.42 per share, so I expect a -13.42% decline in earnings per share for 2023 for the S&P 500. As I noted earlier, I estimate a valuation of the S&P 500 at a P/E of around 15 by the end of the year, and 15 x $17.68 is $265.20 per share. SPY’s current price is $380.72, so it needs to fall a little over -30% from here to hit $265.20.

Conclusion

As I write this, the S&P 500 index is trading at 3,837. If it falls -30% from there it will fall to about 2,686. It’s difficult to know exactly how long the index might take to fall that low, but I’m leaning more and more toward it taking a longer time rather than a shorter time. Fed interest rate hikes will take some time to work their way into the economy and the biggest downside catalyst other than earnings disappointments will probably be the Supreme Court decision on student loans. If that doesn’t happen until summer, then most of the negative effects will occur later in the year economically. Also, I think it’s going to take some time for middle-class Americans to fully deplete their savings from stimulus money, for job cuts to occur, and for market psychology to turn negative. Additionally, the economy has often reacted more slowly to bad headwinds in the past compared to what I might have expected, so I think the economy might be a little more resilient and take longer to turn negative than I would naturally expect this time as well.

Putting all this together, my prediction for S&P 500 index is a -30% decline to 2,686 for 2023.

I promised to have something actionable in this article for investors. Recently, in my marketplace service, The Cyclical Investor’s Club, I developed a 401k strategy that only uses an S&P 500 index fund (like SPY) and cash (or cash equivalent), and the weightings between the two options are adjusted using a number of factors that I track like valuations, economic outlook, public policy, and some basic technicals. Going into the year, my allocation is 65% cash and 35% S&P 500 (though if the S&P 500 drops a little more in the next week, I might adjust to 60% cash and 40% S&P 500 before the new year). So, in the accounts where I can’t carefully select individual stocks, I’m about 2/3rds cash and 1/3 S&P 500. In the accounts where I can select individual stocks, I’m the inverse of that, with about 2/3rds individual stocks, and 1/3 cash.

You’ll notice that I’m not allocated 100% one way or the other, but that I’m tilted more defensively than normal (which is 100% stocks). This is to account for the likelihood that I could be wrong or something unexpected could happen. These allocations will be adjusted as the year goes on and more information comes in. I think the biggest risk to the general bear thesis of a -30% decline is probably that the Fed totally reverses course before the market drops very much. And, the biggest risk to the year-end estimate, is the market drops -30%, inflation comes down more rapidly than expected, earlier than expected, and the Fed massively shifts its policy before the end of year, causing a market rally. This scenario shouldn’t be a problem for investors, though, because I will probably have gotten most of my cash into the market by the time of the policy shift.

I hope this article lets everyone know how I’m thinking about the market in 2023 and positioning for it. It could be a very exciting, yet challenging, year for investors. Happy new year, everyone!

Editor’s Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today

Be the first to comment