MCCAIG/E+ via Getty Images

Originally published on May 31, 2022

By Seema Shah, Chief Global Strategist, Kara Ng, Global Economist

With the struggles from the Global Financial Crisis (GFC) still fresh in policymakers’ minds, the 2020 COVID-19 recession was fought proactively, with every tool available. After trillions of dollars in fiscal and monetary stimulus, protracted economic crisis was avoided. However, policy actions worked too well, supercharging aggregate demand before supply could fully heal and pushing inflation to fresh 40-year highs. The United States Federal Reserve (Fed) is now embarking on a mission to reassert price stability without ending the post-COVID expansion.

In the sport of professional diving, one of the most difficult feats is attempting to enter the water from ever-increasing heights without creating a splash. Similarly, the Fed’s task of bringing inflation down from current levels that are more than quadruple the 2% target, without triggering a wave of economic pain, will be extraordinarily difficult. As such, just two years into the post-COVID recovery, investors are already discussing the risk of recession.

The Fed attempts the “splash-less dive”

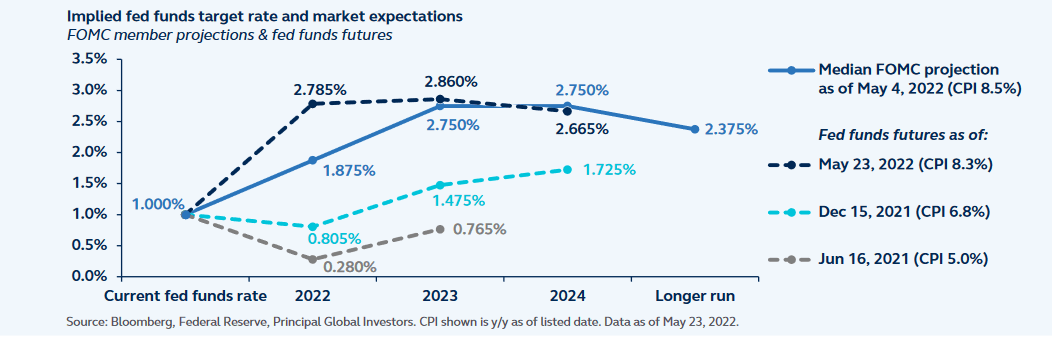

Anchored by the deflationary experiences of the last decade, the Fed waited until headline CPI inflation had hit 7.9% before it finally started tightening monetary policy. This delayed response has permitted inflation expectations to rise and wage growth pressures to increase. As a result, bringing inflation down will be very challenging and the Fed must move with haste. Markets currently expect the equivalent of around seven more 25 basis point (bp) rate increases over the remaining five meetings this year – that equates to two 50bp hikes and three 25bp hikes.

Additional tightening in 2023 would take policy rates toward 3% and solidly into restrictive territory. Going by these forecasts, a slowdown in economic growth appears a near-certainty. The key question is, on its route to bringing inflation back to the 2% target, will the Federal Reserve push growth all the way down into negative territory? While the Fed believes that it will be able to avoid recession, in 12 major tightening cycles since 1954, the Fed only managed a “soft landing” (avoided recession) on three occurrences: 1965, 1984, and 1994.

Implied Fed Funds Target Rate And Market Expectations

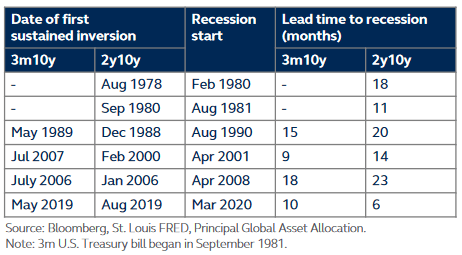

Yield curve inversion

Key market indicators don’t inspire much confidence in the Fed’s maneuverability. In recent months, the 2y10y U.S. Treasury yield curve1 flattened significantly, even inverting briefly in April, alerting investors to elevated risks in the economic outlook. While investors should be mindful of the yield curve inversion signals, there are some key nuances that should be considered:

- While every U.S. recession since the 1970s has been preceded by a yield inversion, not every inversion has led to a recession. For example, the yield curve gave false alarms in June 1998 and February 2006 when the 2y10y inverted only shallowly. Generally, deeper and sustained inversions are a more telling indicator than brief and shallow inversions.

- Over the past decade, high demand for perceived safer assets, including central bank holdings of U.S. Treasurys, has suppressed long-term yields. Given today’s lower starting point for the long end of the yield curve, it may be easier for the curve to invert, thus fading the recessionary signal. It seems that for an inversion to really “count” as a valid recession signal today, the magnitude of inversion must be sufficiently deep.

- The lead time between 2y10y curve inversion and recession tends to be long and variable, on average 12-18 months, but sometimes extending to four years. The recent flattening of the 2y10y curve indicates a rising risk of recession in late 2023, into early 2024.

- While the long lead time of the 2y10y curve can offer some guidance on the risk of recession in 12-24 months’ time, yield curve measures that start from the near term, such as the 3m10y spread, are typically more reliable predictors of recession during the next 12 months. Combined today, these different segments of the yield curve point to a low probability of recession during the next 12 months but higher risk in the following 12 months.

Date Of First Sustained Inversion; Recession Start Date; Lead Time To Recession

The Fed must act quickly

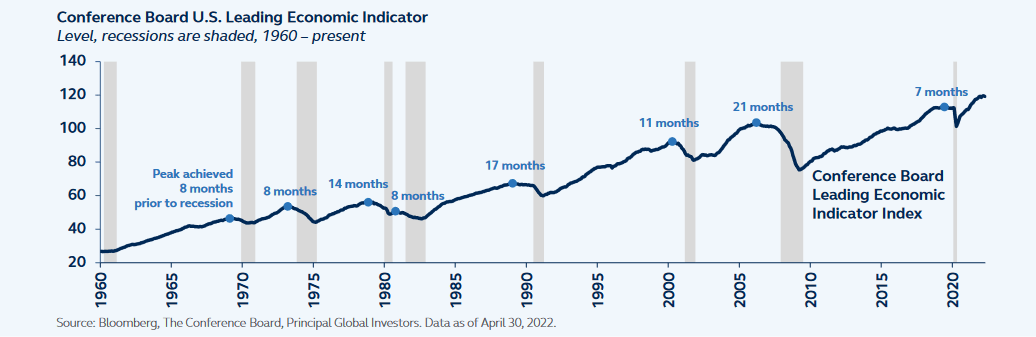

At this point, there is no space for Federal Reserve complacency. Monetary policy typically hits the real economy with a lag of around 6-24 months. Therefore, by the end of 2023, once higher policy rates have had a chance to flow through to the real economy, many economic indicators will likely be considerably more stressed, and risk of recession will have likely risen.

Still, for investors worrying that a recession is imminent in 2022, the Conference Board’s U.S. Leading Economic Indicator provides some reassurance. The Conference Board’s Index, which made a new high in March 2022, historically precedes a recession by a year – which suggests that the slowdown is unlikely until mid-2023 at the earliest.

Conference Board US Leading Economic Indicator

Current economic data also corroborate with the signals from the 3m10y spread and the Conference Board’s Indicator that risk of recession in 2022 is very low. Fast forward to late 2023, however, and economic data will likely tell a different story.

The U.S. consumer

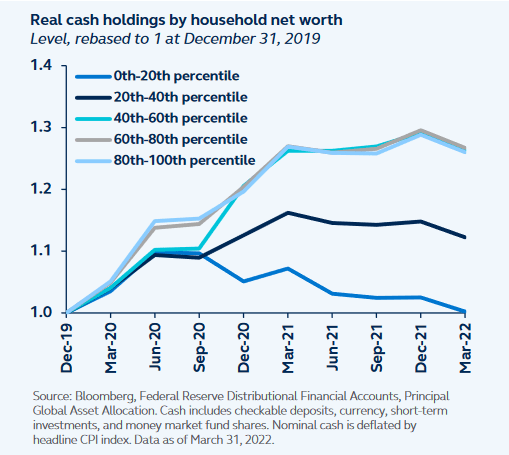

Current environment: Higher inflation has significantly squeezed household purchasing power, yet the impact on consumer spending has been tempered by households’ willingness to draw down excess savings.

However, healthy household balance sheets and residual excess savings can’t cushion pain from higher prices forever. After a pandemic-relief cash influx in 2020, time and inflation has eroded real cash holdings for the poorest cohort of U.S. households back to pre-COVID levels. The next quintile of poorest households will likely face the same fate within the next few quarters, further pressured by rising borrowing rates, suggesting that household spending will become increasingly strained over the coming quarters.

Real Cash Holdings By Household Net Worth

The labor market

Current environment: The labor market remains extremely strong, with the unemployment rate just a touch above the pre-pandemic low (3.6% today vs. 3.5% in February 2020) and nearly two job vacancies per unemployed worker.

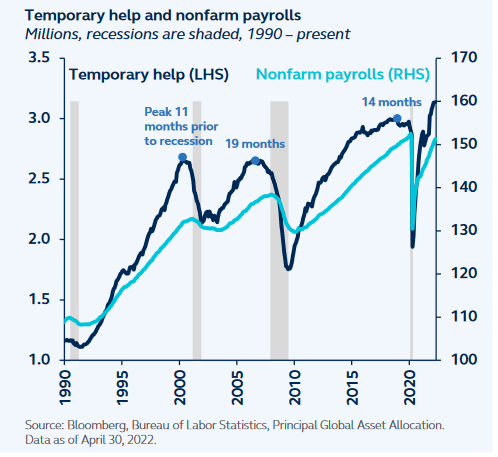

Temporary Help And Nonfarm Payrolls

While strength in the labor market remains key for keeping recession risks at bay, overheating can raise the risk of recession. Low unemployment, high job vacancies, and high wages are symptomatic of a tight labor market – good for the economy in the short term but potentially dangerous in the longer term. For example, as companies bid up wages to compete for scarce labor, they are then either passing on rising labor costs to consumers (contributing to price pressures and adding to the inflation headache) or are having those higher wages eat into corporate profit margins. Either way, an unsustainably hot labor market raises the risk of a recession at the 24-month horizon.

Are there any labor market indicators that can provide warning signals? For one, a slowdown in payrolls is often representative of a slowing broader economy. As wages rise and labor demand slows, firms typically first resort to cutting worker hours, cutting temporary help, or removing job postings. Today, while job postings are at all-time highs, worker hours have been falling throughout 2022, and growth in temporary help employment appears to be slowing – usually a precursor to a slowdown in payrolls.

The housing market

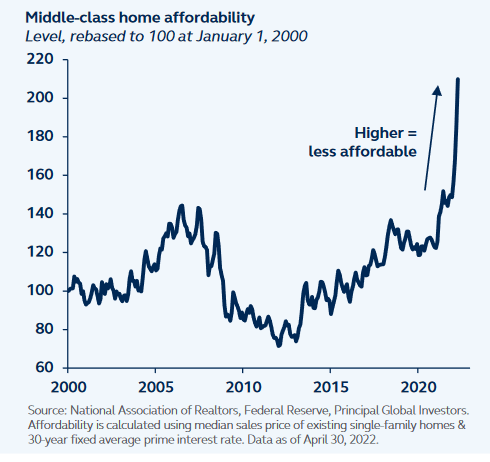

Current environment: House price growth is red-hot, hitting a record high in April, even as recession fears have grown.

As the Federal Reserve hikes rates, mortgage rates have risen sharply (to levels unseen since 2009) and should likely dampen housing demand and create a softer housing market over the next year. Already in 2022, mortgage applications, building permits, and housing starts have started to decline. A housing market crash of GFC levels is unlikely, as mortgage originations today are disproportionately made to high-quality prime borrowers, reducing the risk that higher interest rates will trigger a wave of defaults.

Middle Class Home Affordability

The signal from key economic and financial indicators is clear: While near-term recession risk is low, it becomes more elevated during the 12-24 month period. Some weakness is beginning to seep in, as households and companies start to struggle under the weight of inflation, and as the Fed rapidly moves the policy rate towards restrictive territory. A recession in early 2024 is increasingly likely.

Implications for investors

The temptation for investors to reduce exposure to risk assets as recession risks climb is real. Yet, with positive economic growth expected in 2022, earnings growth should also be positive, supporting equity returns. It’s only once the economic data begin rolling over and earnings growth meaningfully weakens, currently projected during 2023, that a more sustained loss in risk assets is likely.

However, given the asymmetric costs around precise recession timing, investors should avoid chasing potential gains and be more selective in their allocations. Exposure to stocks with strong balance sheets, stable earnings growth, and high margins can help navigate this increasingly challenging environment, while taking refuge in high-quality credit adds an element of defensive positioning. Real assets, such as infrastructure investments, can offer an opportunity for diversification, potentially provide attractive real yield and predictable cash flows, and can be a natural inflation hedge. As markets tread the road to recession, risk is not off the table, but return-seeking investors should be deliberate and disciplined to keep portfolios on a level footing.

*********

1 The 2y10y U.S. Treasury yield curve has inverted ahead of every U.S. recession since the 1950s, making it a strong predictor of future recession.

_______________

Risk considerations

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results. Fixed-income investments are subject to interest rate risk; as interest rates rise their value will decline. Asset allocation and diversification do not ensure a profit or protect against a loss. Investments in natural resource industries can be affected by disease, embargoes, international/political/economic developments, variations in the commodities markets/weather and other factors. Investing in derivatives entails specific risks regarding liquidity, leverage and credit that may reduce returns and/or increase volatility.

Important Information

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. The opinions and predictions expressed are subject to change without prior notice. The information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell, or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

This material may contain ‘forward-looking’ information that is not purely historical in nature and may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

© 2022 Principal Financial Services, Inc. Principal®, Principal Financial Group®, and Principal and the logomark design are registered trademarks of Principal Financial Services, Inc., a Principal Financial Group company, in the United States and are trademarks and services marks of Principal Financial Services, Inc., in various countries around the world. Principal Global Investors leads global asset management at Principal®. Principal Global Asset Allocation is an investment management team within Principal Global Investors.

MM12939 | 2217254

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment