Lemon_tm

After covering the Alpha Architect U.S. Quantitative Momentum ETF (QMOM) in my previous article about momentum, I’m now looking toward the other end of the spectrum in this piece to examine the iShares Edge MSCI USA Momentum Factor ETF (BATS:MTUM).

In the conclusion of the above-mentioned article, I wrote the following:

…with QMOM you get a more sophisticated but also more risky implementation of momentum. If you don’t want to bear the risk that this differentiated process underperforms, you can also get a more diversified type of momentum from the MTUM ETF or other alternatives.

So I think this article is a logical follow-up to that piece.

Momentum – Idea and Evidence

Previously, I gave a quite detailed overview about the idea and evidence behind momentum, and why it probably will continue to work in the future. For the sake of brevity, I will not repeat this section here and instead refer interested readers to my prior article. That said, I will give you a brief summary of the most important points below.

The basic idea behind cross-sectional price momentum is very simple and goes back to academic research in the early 1990s: Stocks with high returns over the last 12 months (winners) tend to outperform stocks with poor returns (losers). Yes, it really is that simple.

The most basic (and academic) form of momentum is a market-cap-weighted portfolio of “winner” stocks in a given universe – for example, the top 33% of U.S. stocks with respect to 12-month returns. You can also advance that to an absolute return/market neutral strategy and simultaneously short the opposite end of the distribution (for example, the 33% of stocks with the lowest 12 month returns). Such a long-short portfolio gives you the well-known momentum-factor (more information about that can be found on Kenneth French’s website).

Although it appears to be rather simple, momentum historically “worked” across most international stock markets, other asset classes, and over different time periods (see here for an overview). In addition to the empirical evidence, there are also plenty of plausible theories for the excess returns of momentum.

Based on this empirical and logical evidence, I strongly believe that momentum deserves a spot in a diversified (equity) portfolio. Let’s now see if the MTUM ETF is a suitable way to implement it.

Implementing Momentum Via MTUM

The MTUM ETF tracks the MSCI USA Momentum SR Variant Index, which is basically the MSCI USA Momentum Index with some stretched rebalancing. To see how this index works, I downloaded the latest MSCI Momentum Indexes Methodology from August 2021. Section 2.2 explains that the index is based on two momentum signals: the price return over the last six and 12 months, in each case without the latest month (so the 12-month momentum signal is the return 13 months ago until one month ago). In my opinion, these are reasonable signals because they are transparent and identical to the academic definitions of momentum. In addition to that, the six-month price return also allows one to rank stocks without sufficient history (like IPOs), which makes the index more practical.

In the next step, MSCI scales this momentum score by the volatility of the respective stock and thereby punishes stocks with high volatility. I don’t know the specific reasons for this adjustment, but I could imagine that MSCI wants to have a rather smooth path of momentum and employs state-of-the-art risk management.

In the last step, they adjust the momentum signals for outliers and convert them into a multiplier. The weight of each stock in the momentum index is then given by the product of a stock’s weight in the MSCI parent index (here, the MSCI USA) and its momentum multiplier. The result is a portfolio that overweights (underweights) stocks with high (low) momentum relative to the U.S. market index.

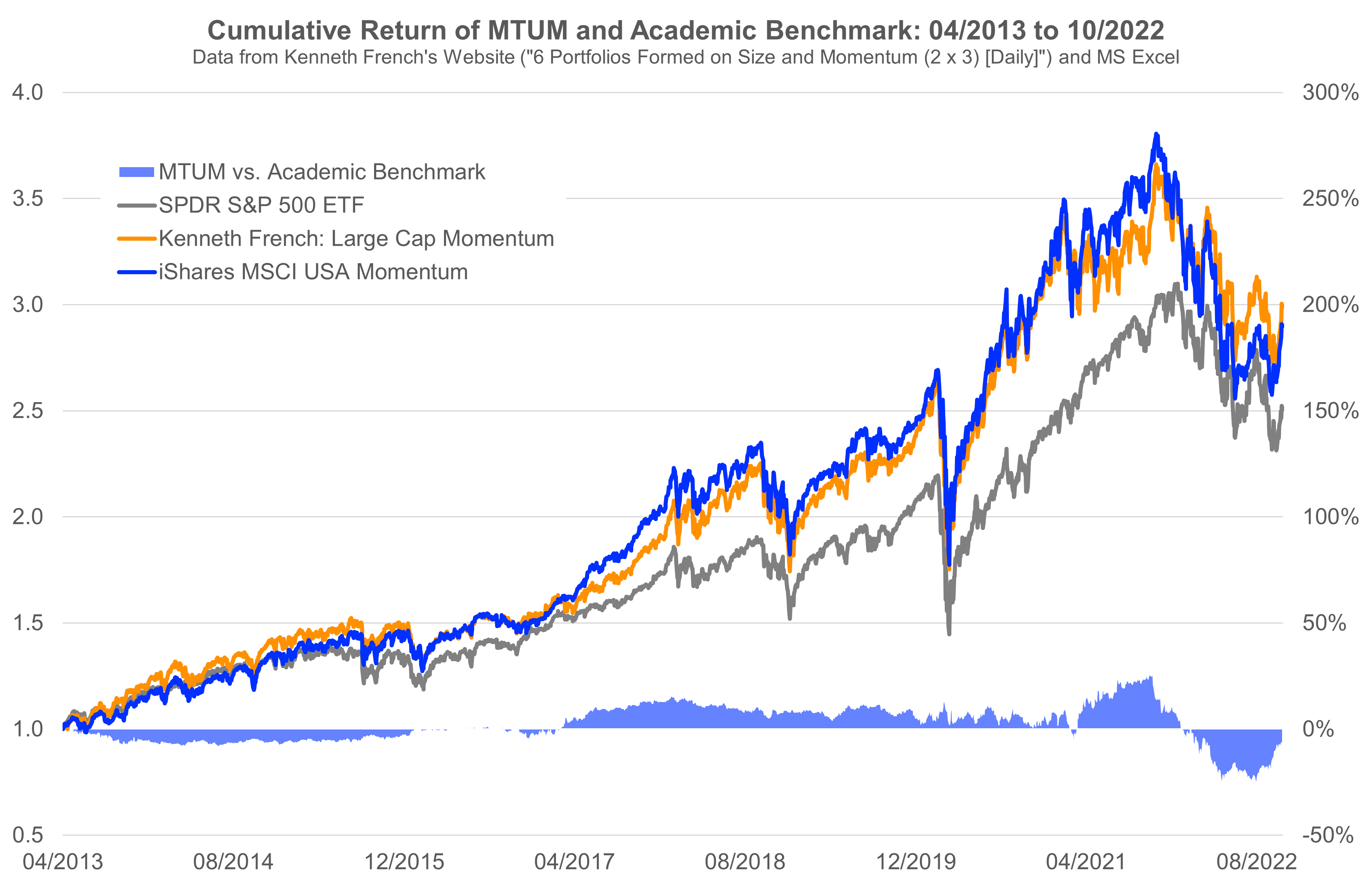

MTUM Vs. Academic Benchmark

To check if this methodology indeed delivered momentum exposure, I will start with a comparison of MTUM and the simple academic benchmark from Kenneth French’s website. Since the MTUM ETF is obviously a long-only strategy, I use the returns of the large-cap momentum portfolio as benchmark. To compare it with the overall U.S. market, I also plot the cumulative returns of the SPDR S&P 500 Trust ETF (SPY). The chart below summarizes the results.

Own illustration of data from Kenneth French’s website and ETF return. (Tuck School of Business and Microsoft Excel Stock API)

Both momentum strategies outperformed the S&P 500 ETF since April 2013, the inception date of the MTUM ETF. I think this isn’t too surprising, as the U.S. market was particularly dominated by a few very successful companies (FAANG or whatever acronym you want to use) with long-lasting positive trends during that time.

The second important observation is that the MTUM ETF performed in line with the academic momentum benchmark (sometimes slightly better, sometimes worse). I think this is a very good result because the ETF is designed to deliver the well-researched momentum premium, and, for that purpose, it shouldn’t deviate too much from the academic consensus.

In fact, in my opinion the MTUM ETF deserves even more credit as it achieves this performance with much slower rebalancing and after-transaction costs and management fees. To be honest, in the beginning I was somewhat skeptical of the ETF because it only rebalances every six months. For momentum, this is quite slow as most academic studies documented the factor with monthly rebalancing and pretty high turnover. The academic benchmark in the chart even assumes daily rebalancing, which is, of course, unrealistic – but at the same time, the “fastest” momentum exposure you can get. At least historically, however, the slower rebalancing also worked, and the ETF delivered the (long-only) momentum premium.

But, as always, past performance doesn’t guarantee future results. When there are sudden changes in markets and trends break down, as was the case in 2022, slower rebalancing is harmful for momentum strategies because they cannot adapt fast enough. For example, the MSCI momentum indices probably strongly overweighted technology at the beginning of the year and only shifted to outperforming energy and defensive stocks at the first semi-annual rebalancing date in May. I suspect that this is the main reason why the MTUM ETF underperformed the academic benchmark in 2022 (for more, check this thread on Twitter). I will come back to this problem of slow rebalancing below.

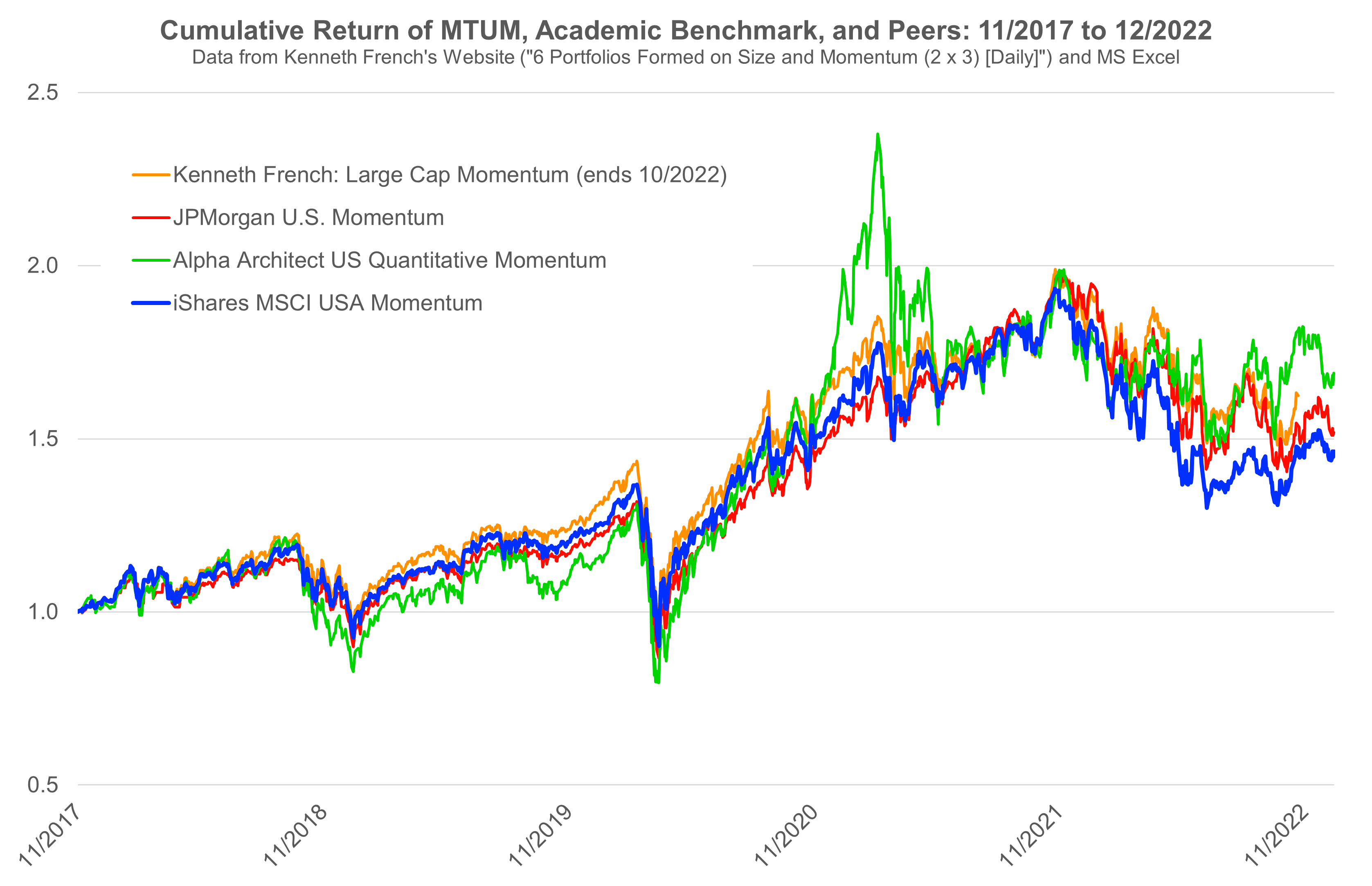

MTUM Vs. Momentum Peers

Apart from MSCI style indices and academic benchmarks, there are of course also active managers who offer momentum strategies. Many of them focus on the speed-issue and aim for faster rebalancing, while at the same time keeping transaction costs under control. AQR, for example, writes on the website of their momentum fund that they “employ optimization and other sophisticated techniques to keep transaction costs as low as possible.” Apart from that, momentum managers also try to improve the strategy even further (new signals, better risk management, etc.).

Own illustration of ETF returns and data from Kenneth French’s website (Tuck School of Business and Microsoft Excel Stock API)

The chart above shows the longest common history of the MTUM ETF, two active alternatives (the JPMorgan U.S. Momentum Factor ETF (JMOM) and QMOM), and Kenneth French’s academic benchmark from before. I will not go into detail on each fund’s methodology, but rather will focus on the big picture. Over this five-year period, the MTUM ETF was the worst of the strategies and also worse than the academic-benchmark. Except for the current year, however, the differences are quite small and probably not statistically significant.

As already mentioned above, I suspect that the recent outperformance of the momentum peers was driven by faster rebalancing. In 2022, the semiannual rebalancing of the MTUM ETF was just too slow to avoid losses at the beginning of the year. In fact, I also found an interesting analysis on Twitter that shows the MTUM ETF would have performed much better with monthly rebalancing.

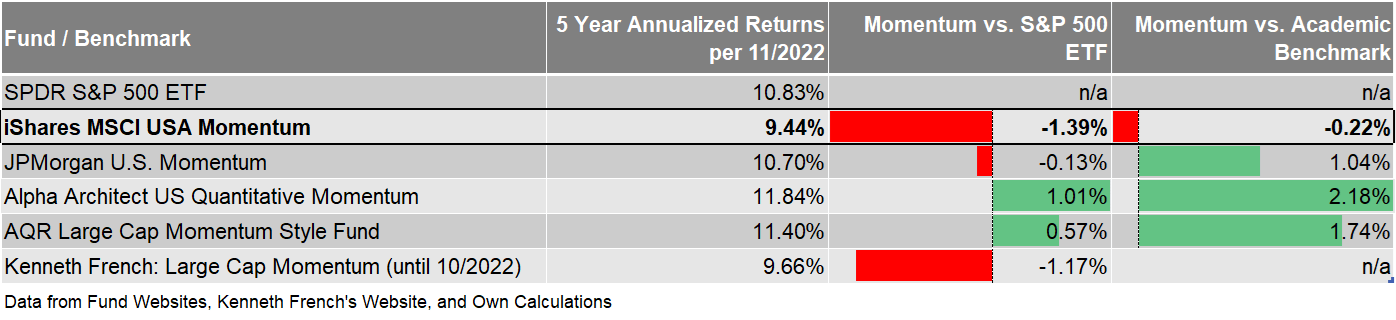

The following table again summarizes these results with annualized returns over the last five years per November 2022. Note that the table also includes the AQR Large Cap Momentum Style Fund, for which I unfortunately couldn’t obtain a time series in the previous graph.

Own illustration of data from fund websites and Kenneth French’s website (Tuck School of Business, Performance Disclosures on Fund Websites, Microsoft Excel Stock API)

As mentioned before, the MTUM ETF was the worst momentum strategy over this time period and underperformed both the S&P 500 and its momentum peers. The best momentum implementations were the Alpha Architect US Quantitative Momentum ETF (the reason I wrote my prior article) and the AQR Large Cap Momentum Style Fund. Both managers are well-known and respected for their research on momentum, so it’s nice to see that they practice what they preach.

Conclusion

As I’ve already mentioned, I strongly believe in momentum and think it should be part of a diversified portfolio. The strategy is very well-researched, there are plausible theories why it worked and should continue to do so, and, most importantly, there are efficient instruments to capture the premium.

As this article is primarily about the MTUM ETF, the next question is of course whether the ETF is actually a good way to implement momentum. Overall and for most people, I think it is. The underlying MSCI momentum index follows a transparent methodology and receives a lot of scrutiny from professional market participants (remember the Twitter threads). More importantly, the index was historically fairly close to the academic momentum benchmark of Kenneth French (although the years since 2013 were arguably quite special).

That said, the index is not perfect. The key problem, as we have seen in 2022, is the six-month rebalancing interval. Slower rebalancing is fine if you have markets with long-lasting trends (like the FAANG names during the 2010s), but it hampers performance when things suddenly reverse. In my opinion, it’s unfortunate that MSCI does not improve this aspect. I don’t know the details that might prevent them from doing so, but I believe it shouldn’t be too difficult to switch to quarterly rebalancing.

So what is the takeaway of this article, especially in combination with my previous thoughts on the QMOM ETF? Well, I think there is a tradeoff. On the one hand, the MTUM ETF gives you a simple and transparent momentum exposure that historically wasn’t too much off the academic benchmark. On the other hand, good momentum managers also demonstrated that they are capable of improving the strategy further. So the answer is an unsatisfying “it depends.” If you want to add some momentum to your portfolio and don’t want to compare the investment processes of asset managers, I think the MTUM ETF is fine. You might leave some of the premium on the table, but you will get momentum exposure.

Also note that since the MTUM ETF works with over- and underweights with respect to a market index, it takes less active risk than some of the other momentum funds (QMOM, for example, is a concentrated bet on the top 50 momentum stocks). Again, this is neither better or worse – it just depends on what you want. If you want momentum but don’t like to monitor asset managers and analyze investment processes, go with MTUM (but accept that the slower rebalancing is not optimal in years like 2022). However, if you enjoy reading about momentum implementations (given that you read all the way through this article, I suspect you do) and evaluating asset managers, you might find better momentum processes from dedicated active managers.

Be the first to comment