Win McNamee

The Fed is trying to send a message to the market. Whether it has been received is yet to be seen. However, that issue will likely be cleared up by Friday, January 6, at 8:30 AM ET, when the December jobs report is released.

The December FOMC minutes may have been the cleanest and most straightforward set of minutes to read in more recent times. The message was unmistakable, as noted:

“…monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.”

When it comes to the Fed, this message seems pretty straightforward and something I have written about now for well over a year. The Fed wants financial conditions to be restrictive to slow the economy, and as the Fed goes on to say:

“Broad financial conditions were projected to be somewhat less restrictive than previously assumed, as the effects of a higher path for equity values and a lower path for the dollar more than offset a higher medium-term trajectory for interest rates.”

So when equity prices rise, the dollar falls, and financial conditions ease, the Fed’s job can be more challenging in the long term. It was a topic I discussed back in October on Fox Business Channel’s Making Money With Charles Payne.

So when the Fed talks about the need for financial conditions to tighten, it seems pretty straightforward; they are indirectly saying they need rates to rise, credit spreads to widen, the dollar to strengthen, and stock valuation to fall.

Not only that, but the Fed is very well aware that they need to deliver a more hawkish message than what the market is pricing in to avoid an undesired reaction, which is why:

Several participants commented that the medians of participants’ assessments for the appropriate path of the federal funds rate in the Summary of Economic Projections, which tracked notably above market-based measures of policy rate expectations, underscored the Committee’s strong commitment to returning inflation to its 2 percent goal.

Knowing the Fed Funds Futures were pricing at a peak rate of 5% on December 12, and to keep the market from viewing the FOMC dot-plot as a dovish message, the intention was to place the median plots above the 5% mark, to avoid the further easing of financial conditions.

Additionally, while the market has been pricing in rate cuts in 2023, it was noted in the minutes:

No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023.

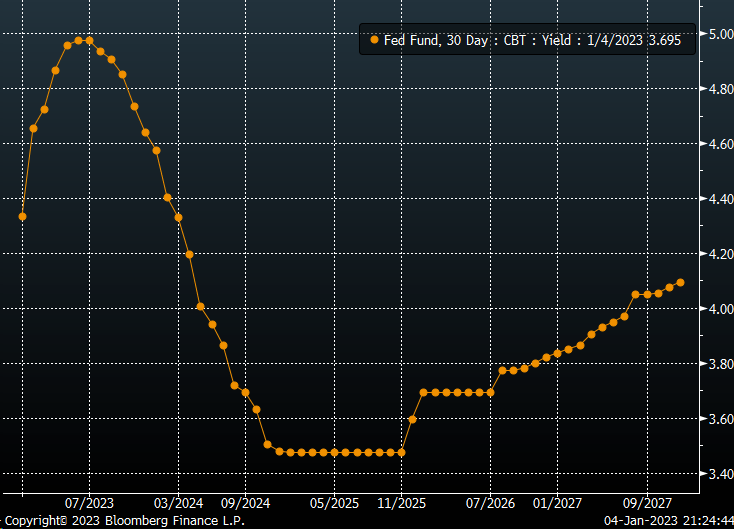

That is definitely not what the market is pricing in, even as of the release of the FOMC minutes on January 4. Currently, Fed Funds Futures show a peak rate of 4.97% in June and rates falling to 4.64% by December 2023. That would be nearly 50 bps below what the Fed is projecting on its Summary of Economic Projections.

Bloomberg

The irony of the situation is that the more the market fights the Fed on the matter, the less likely the Fed is to see financial conditions tighten as much as needed. It becomes more likely that the Fed will not only have to raise rates as they say but potentially even higher.

Focus Shifting to Wages

It makes this week’s jobs report all the more critical. The Fed appears to be moving the goalpost, shifting its attention now to the prices of core services, excluding shelter, which represents the most significant component of core PCE because:

this component of inflation has tended to be closely linked to nominal wage growth and therefore would likely remain persistently elevated if the labor market remained very tight.

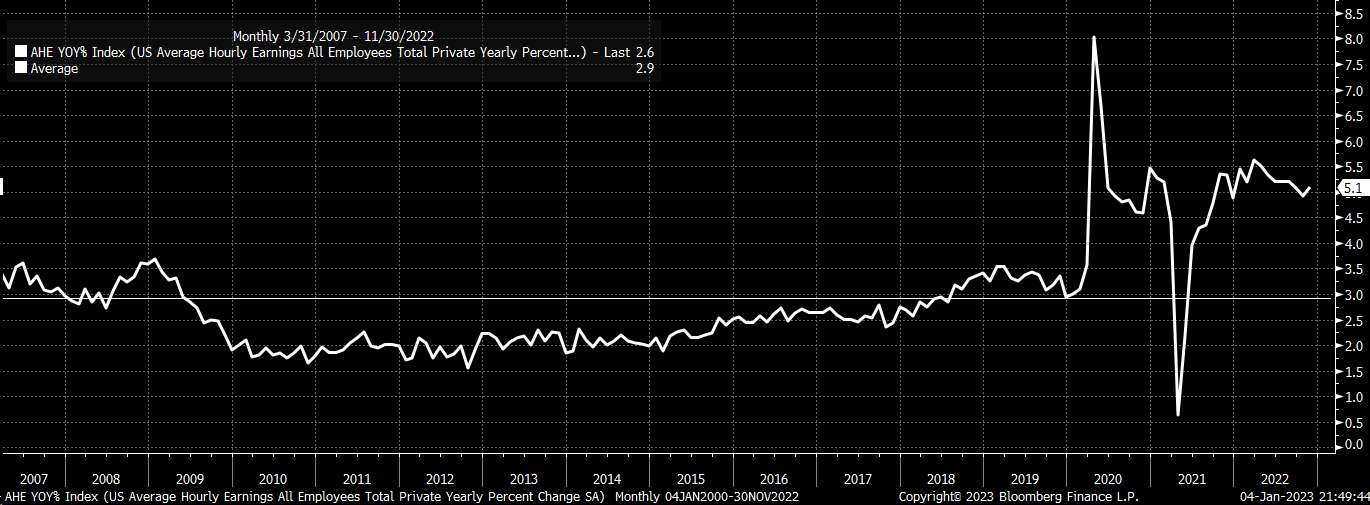

Therefore the December jobs report will pull into focus average hourly earnings, which are forecast to rise by 0.4% m/m and 5.0% y/y versus 0.6% and 5.1%, respectively, in November. And as noted by the FOMC minutes:

Nominal wage growth continued to be elevated and remained above the pace judged to be consistent with the FOMC’s 2 percent inflation objective.

The current pace of nominal wage growth is nearly 2.2% percentage points higher than the historical average of 2.9% since 2007. So we could imagine that if the Fed is now focusing on wage growth because of its impacts on core PCE ex-shelter, it makes one wonder why the market is concentrating on headline CPI.

Bloomberg

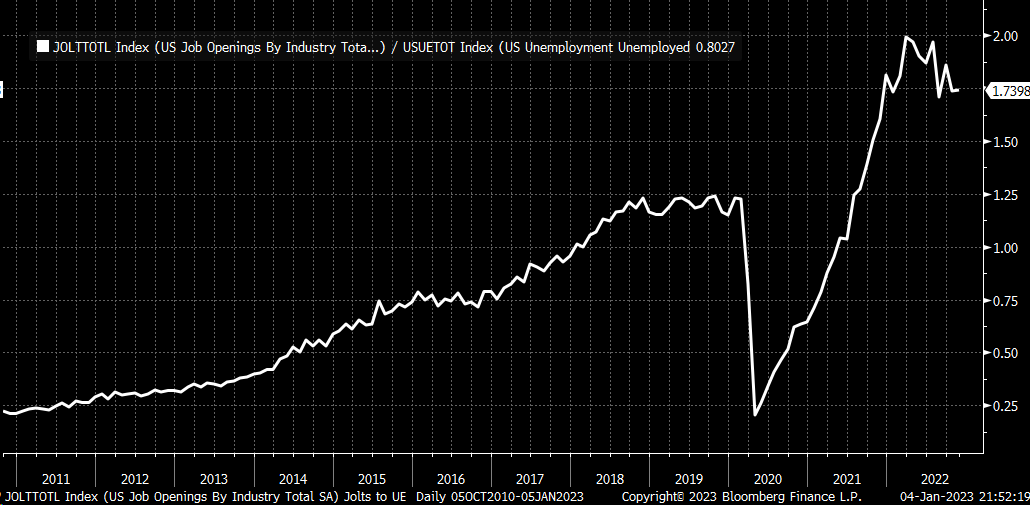

However, should wage growth remain elevated, which seems likely given that there remain 1.7 open jobs for every unemployed person, it may suggest the Fed even has to do more.

Bloomberg

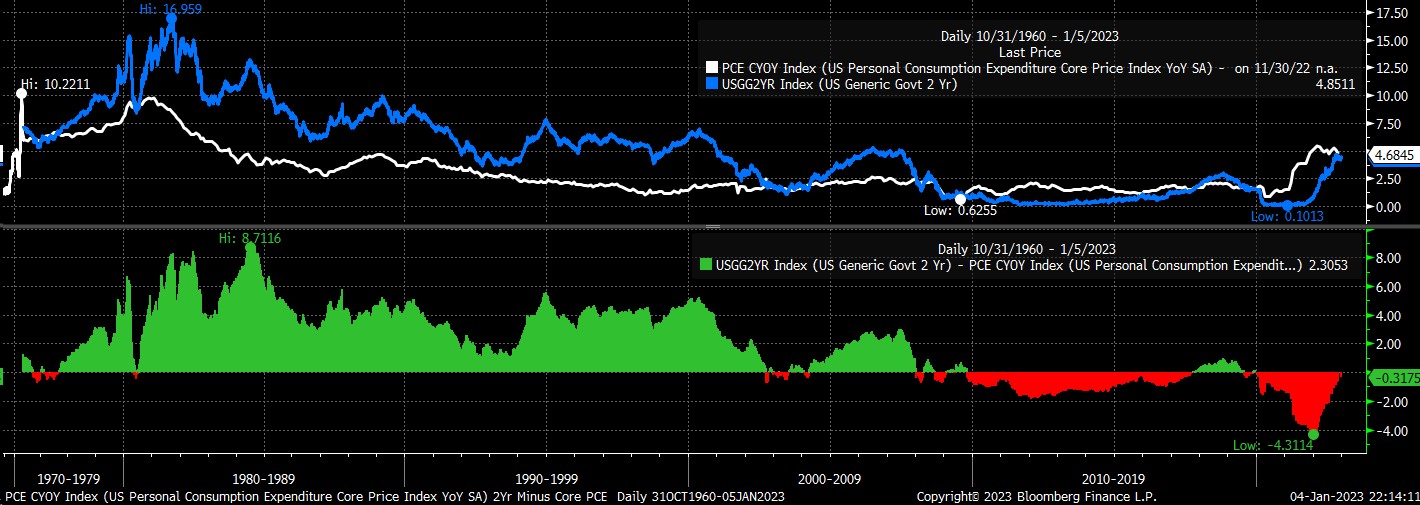

Because as history suggests, it takes getting the 2-year rate above the core PCE rate by about 1%. And if the core PCE stays elevated or is slow to come down, then it probably means that rates in 2023 are not only going above 5% but well above 5%.

Bloomberg

So, if the market is playing games with the Fed, then the market’s first true test of the Fed’s resolve comes this Friday at 8:30 AM ET. We will see who blinks first.

Be the first to comment