dzika_mrowka

The upcoming February 14 Consumer Price Index (CPI) report is poised to deliver a significant blow to the equity market. The market has been on a meteoric rise since the start of 2023, fueled by dreams of falling inflation and the possibility of interest rate cuts from the Federal Reserve. However, if the report reveals the expected change in trend from the previous couple of months of disinflation, it could shatter market hopes and cause a significant market reversal. The report could mark a turning point in the equity market’s expectations for inflation and interest rates, with far-reaching implications.

Analysts predict that the headline CPI will increase by 0.5% month-over-month and by 6.2% year-over-year. Meanwhile, core CPI is expected to rise by 0.4% month-over-month and 5.7% year-over-year.

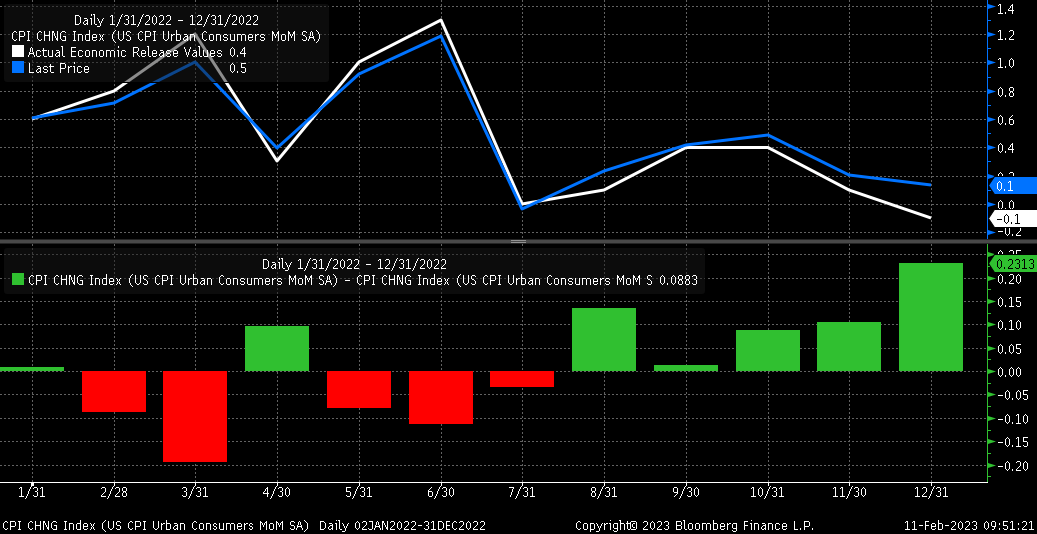

The year-over-year headline CPI is forecast to decline from 6.5% year-over-year in December, while core CPI drops from 5.7%. However, the headline CPI is anticipated to jump month over month from the recently revised increase of 0.1% in December, while core CPI is expected to be flat at 0.4%.

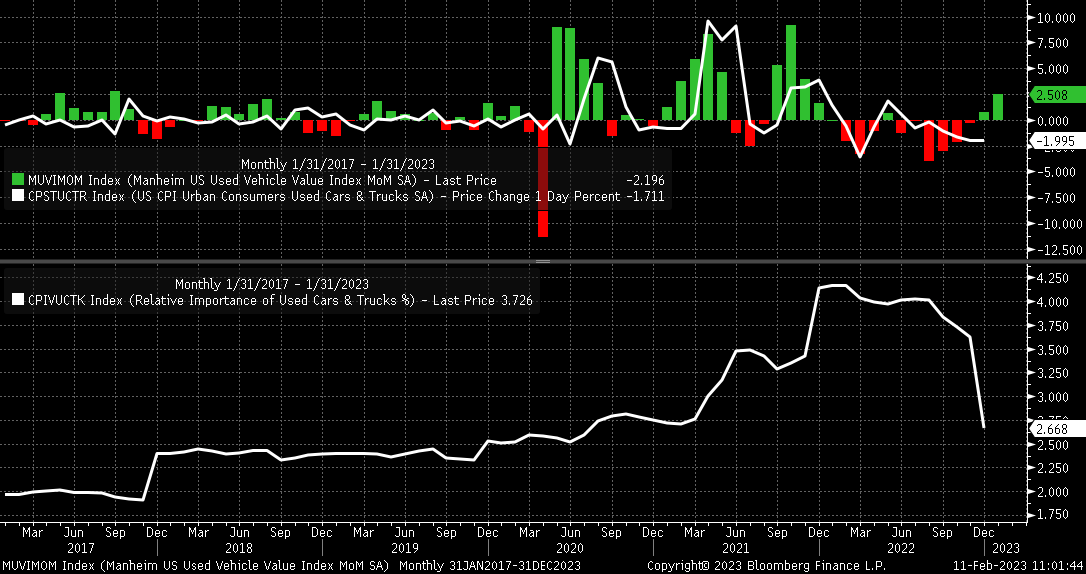

The recent revision of the CPI has also reweighted the various components, leading to changes in their relative importance. For example, energy, which had provided a meaningful deflation impulse in the second half of 2022, will see its weight drop to 6.92% from 7.86%. Meanwhile, the importance of shelter has risen significantly to 34.41% from 32.92%, while used cars and trucks have dropped to 2.66% from 3.62%.

These changes in weighting could result in the CPI running hotter to start the year. For example, the inflation impulse from the owner’s equivalent rent is likely to continue to drive prices higher for some time, while the impact of declining used car prices will be less pronounced.

The revised data suggests that inflation was weaker in last year’s first half compared to the year’s second half. The disinflationary impulse that the equity market was focused on was not as strong as initially thought and was nearly non-existent.

Bloomberg

Higher Prices and Changing Importance

Additionally, January saw significant gains in some factors declining in the year’s second half, such as used autos and gasoline. The Manheim used auto index rose by 2.5% in January, which could indicate that the actual CPI used vehicle index will also rise in the coming months. The Manheim used auto value typically leads the actual CPI used vehicle index by 1 to 2 months. However, the positive impact of these gains is likely to be limited due to their lower weighting in the revised CPI.

Bloomberg

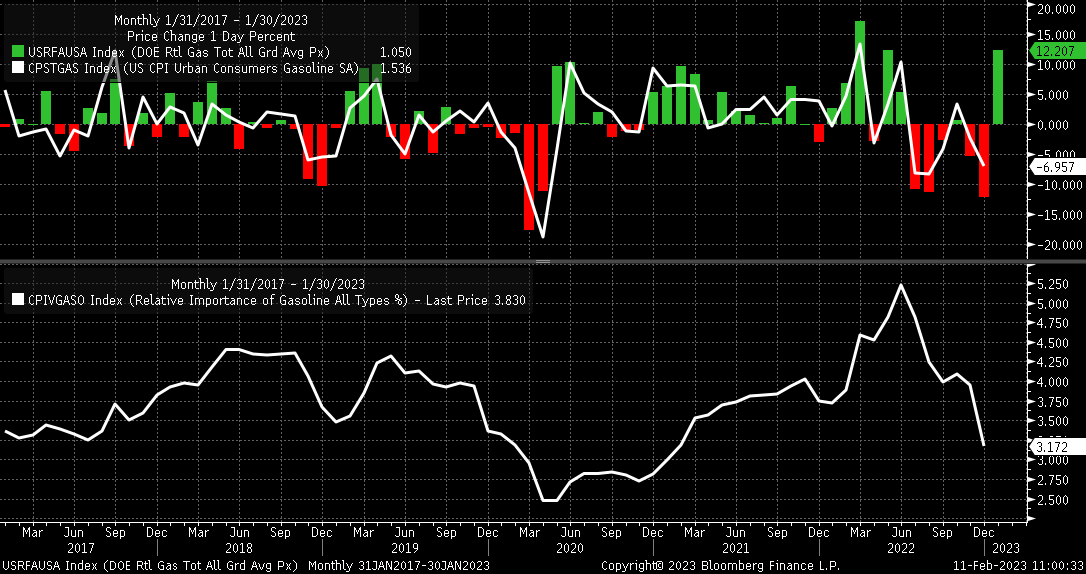

Meanwhile, the rise in gasoline prices should also provide a positive boost to CPI in January, despite the weighing of gasoline falling to 3.17% from 3.95%.

Bloomberg

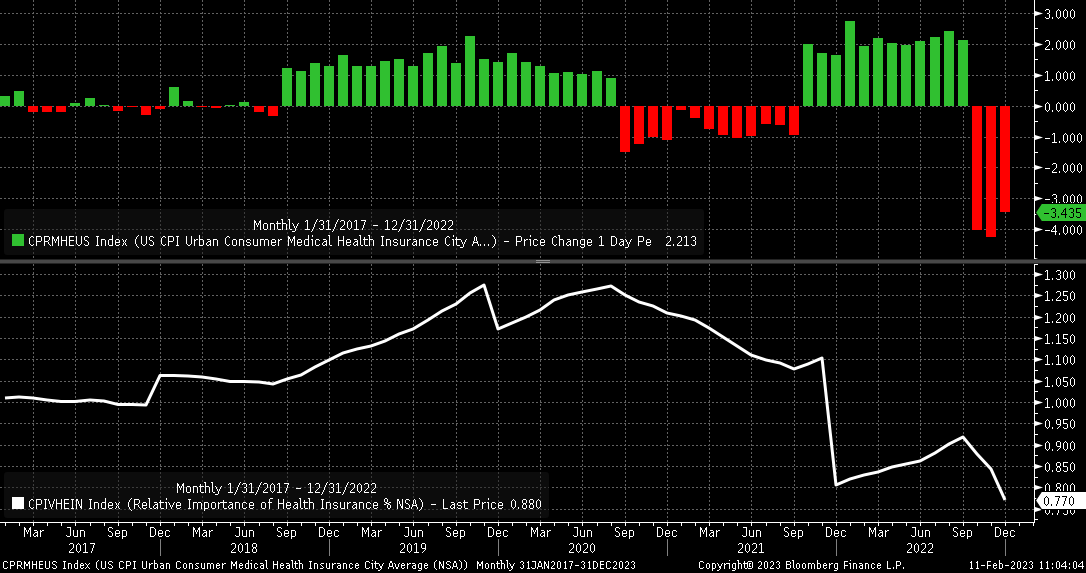

Additionally, health insurance, which has been a disinflationary force on CPI since the October reset, had its weight lowered, which means that the disinflationary force is likely to be smaller in the January report. For example, in the October report, health insurance had a weight of 0.92% and fell by 4%, negatively impacting prices by 0.037%. The same impact with the new weighting of 0.77% would mean it would have only declined by 0.031%.

Bloomberg

Pricing in Higher Inflation

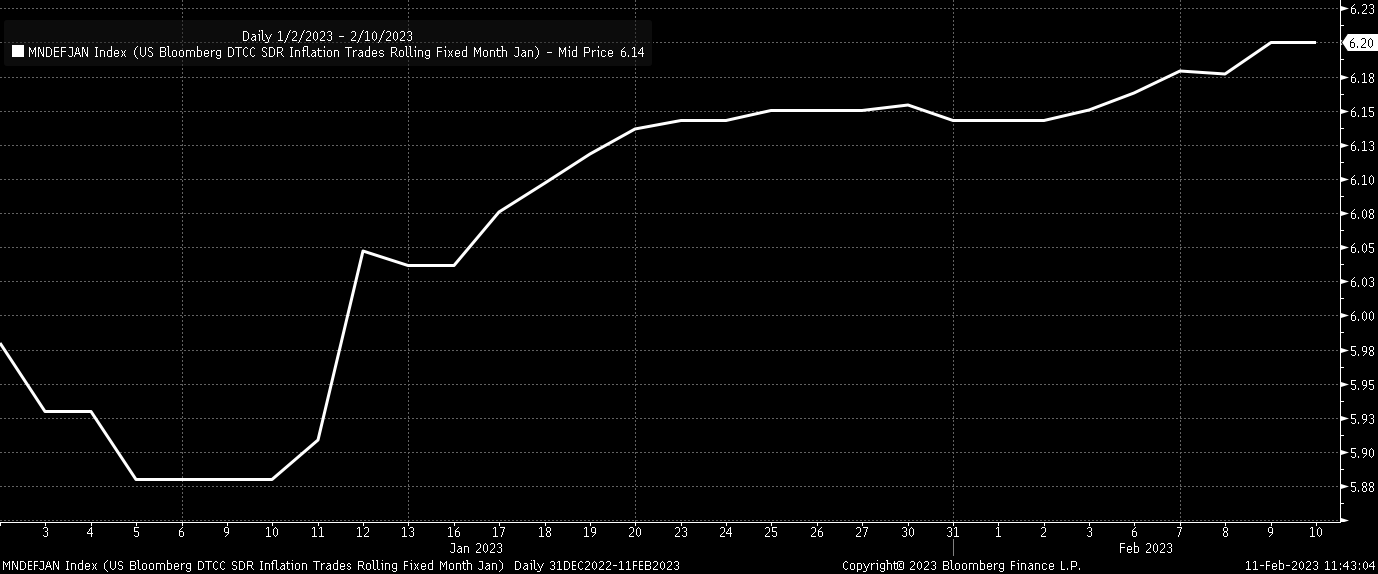

The January CPI report will be tricky to interpret due to weight changes and recent gains in some inflationary factors. If the trend of higher-than-expected CPI continues, it could pose a considerable risk. Trends in the inflation swap market have generally been on the rise, with the January year-over-year increase in swaps rising from a low of 5.88% on January 10 to 6.2% on February 9, which is in line with analyst consensus estimates for the January report.

Bloomberg

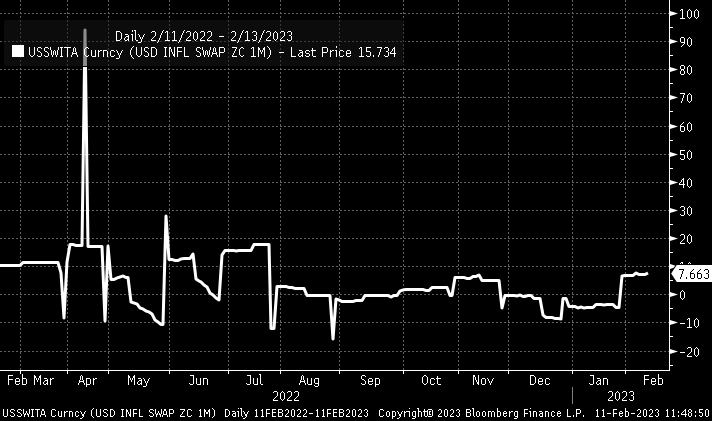

In addition, pricing in the 1-month zero coupon inflation swap market on Friday continued to show rising inflation expectations for January. Based on my current calculations, the pricing suggests that the market forecast the CPI to rise by 6.22% in January year-over-year, a continuation of the trend towards higher inflation reading, and may even indicate the market is thinking actual headline inflation could come in above consensus estimates.

Bloomberg

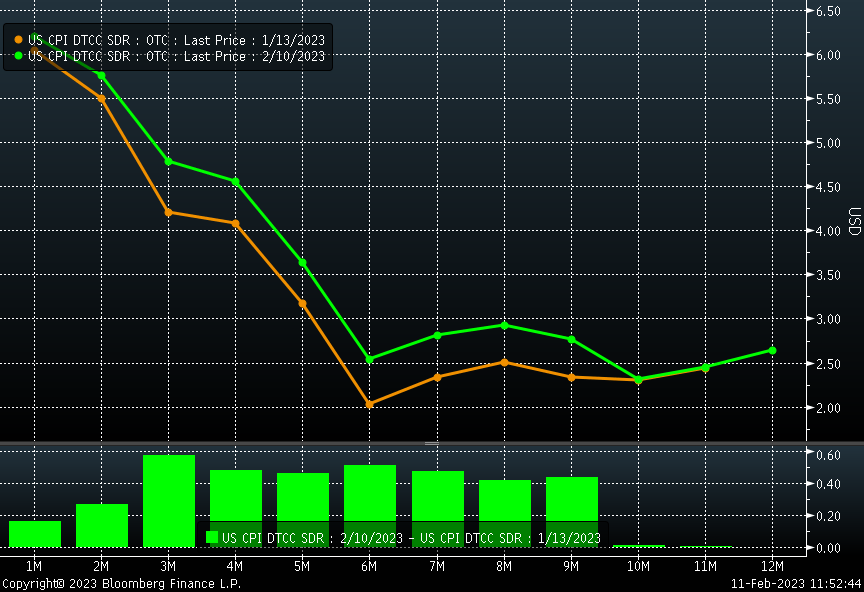

This trend is not limited to just January; it is also evident every month until June. Swaps for March have risen by almost 60 basis points over the past month, while the expected reading for June has shifted from a 2% increase to 2.55%. These shifts suggest that the market expects higher inflation in the coming months.

Bloomberg

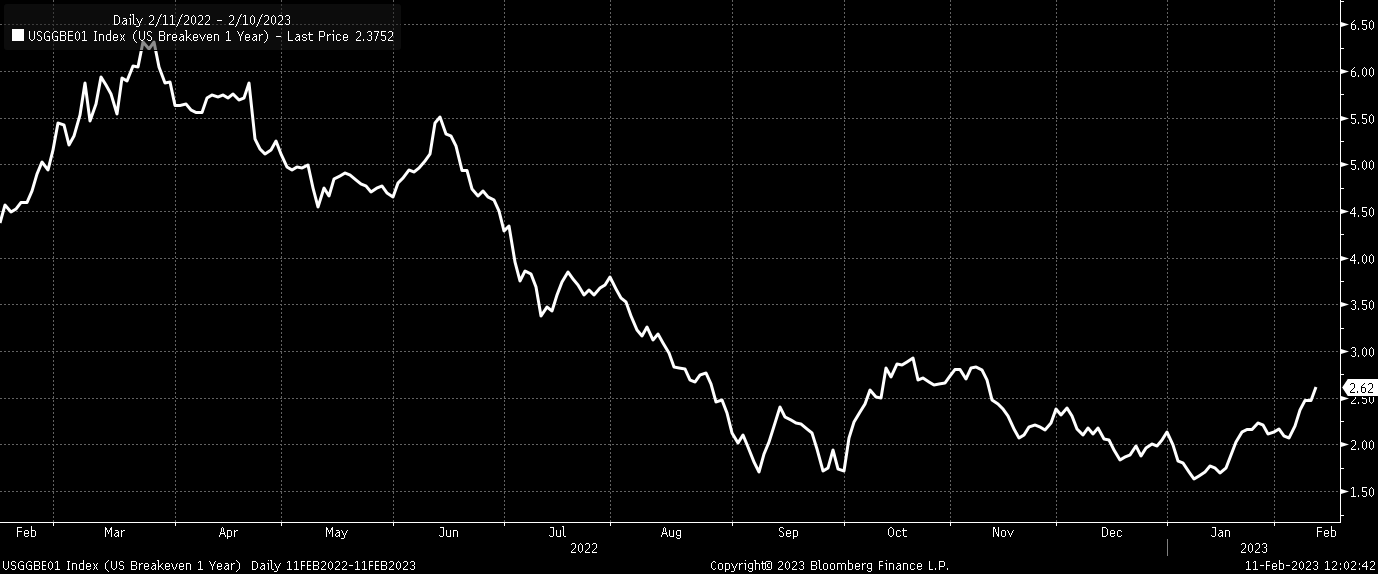

It is not only the inflation swaps pricing in higher inflation rates; the bond market also reflects this trend. The 1-year breakeven inflation rate, which measures the spread between nominal and real yields, has risen to 2.62%, well above the lows of 1.63% seen on January 9. This increase in the breakeven rate suggests that the bond market is also anticipating higher inflation shortly.

Bloomberg

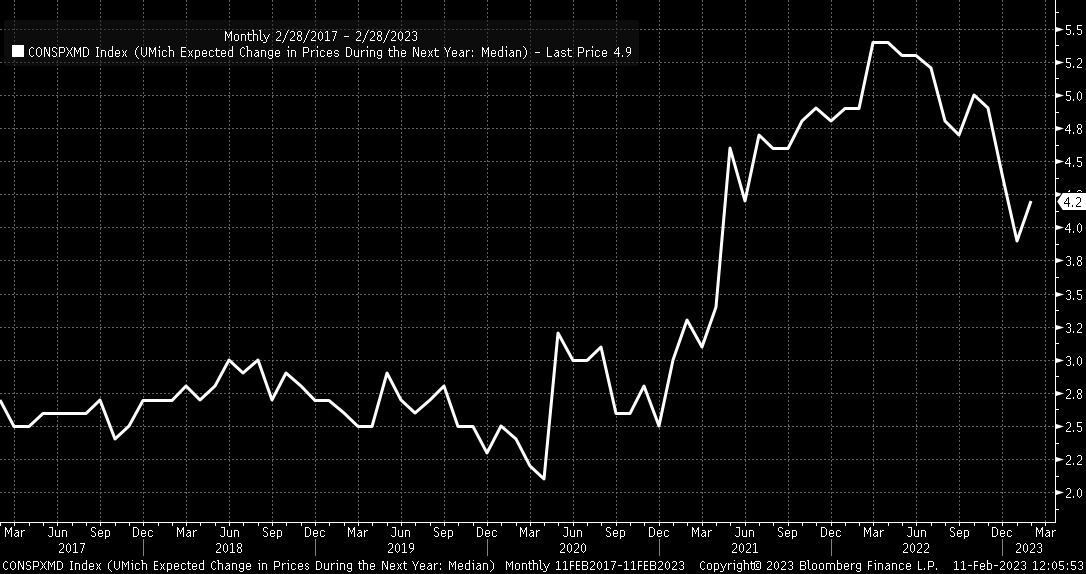

Additionally, the University of Michigan’s 1-year inflation expectation has risen to 4.2%, the first time it has increased in three months. Although it is still below its highs, it is consistent with the inflation swaps and the bond market trends. This suggests that inflation expectations are on the rise across multiple market indicators.

Bloomberg

Betting on Higher Interest Rates

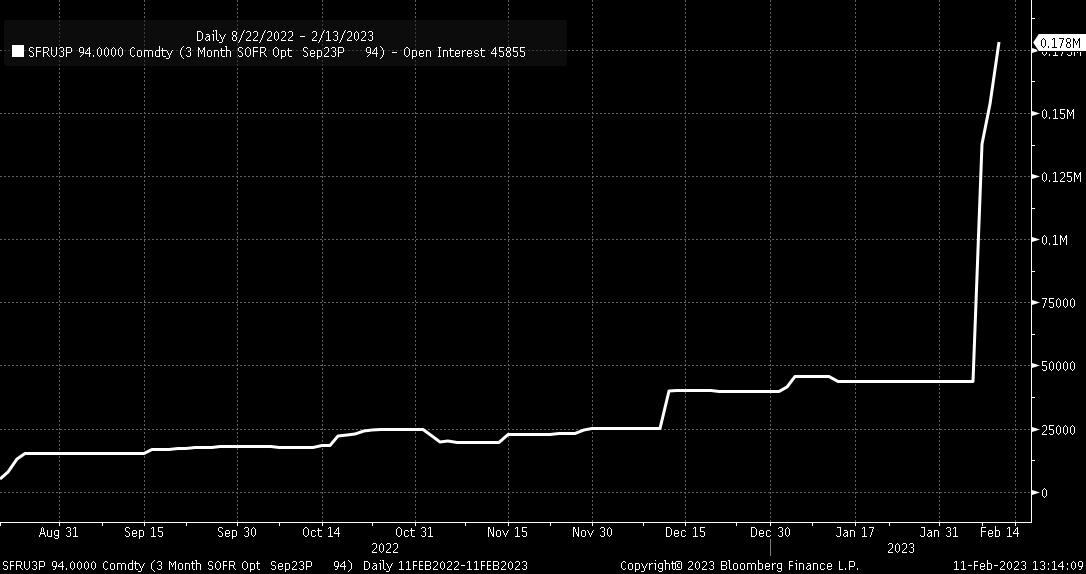

Additionally, there has recently been some betting in the SOFR futures options market that suggests traders see the Fed Funds rate hitting 6% by the September FOMC meeting. Open interest for the SOFRA September 94 strike price has jumped 178,000 contracts from 44,000 on February 6. This implies that the Fed Funds rate is 6% or higher by the expiration date.

Bloomberg

Complacency In Stocks

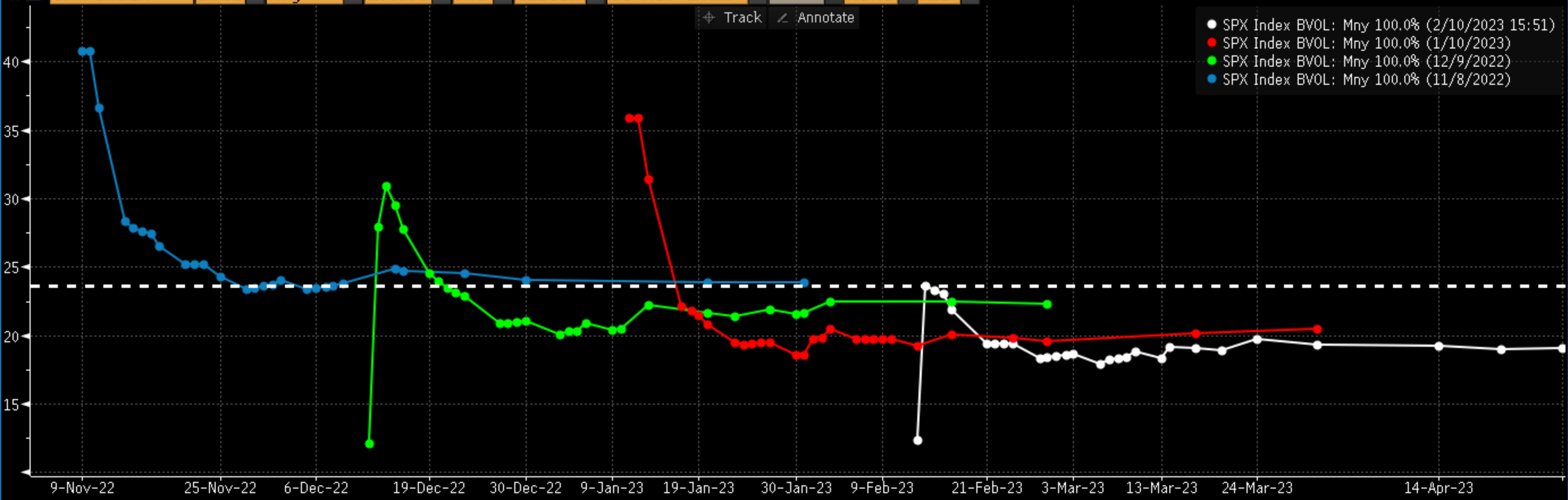

Despite all the warnings from various parts of the markets, the equity market continues to live in fantasy land. It does not appear to be greatly concerned about the upcoming CPI report. Implied volatility for the Tuesday report is just 23.6%, which is well below the readings of 35.8% two days before the January CPI report, 27.95% in December, and 40.7% in November. This suggests that the equity market may not be fully pricing in the potential impact of higher inflation on the economy and equity prices.

Bloomberg

It seems that despite the expected increase in inflation from analysts and the warnings from the inflation swaps, options, and bond market about a potential trend of higher-than-previously-expected inflation in the future, the equity market is still oblivious.

Therefore, it is possible that there is indeed a hotter-than-expected CPI report this week, which so many parts of the market appear to be anticipating. If CPI does come in hotter than expected, the equity market may find itself on the wrong side of the trend again, just as it has several times over the past 12 months.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment