Smederevac

Happy New Year, everybody. I wish all of you a happy and healthy 2023 for you and your loved ones. One of the things that defines this time of year is the “new year’s resolution”, and during one of the social events over the holidays, someone suggested that I make a resolution to dial down the bragging a little bit. I told her I prefer “call my mother more”, because at least that resolution offers up more opportunity for bragging. Anyway, I’m starting my first article of 2023 in this manner not only to express to you how broken my soul is, but to tee up an opportunity to brag. Today I want to write about The Greenbrier Companies, Inc. (NYSE:GBX).

It’s been about two months since I took most of my chips off the table in this investment, revealed in an article sporting the very original title “Taking Most of My Greenbrier Chips Off the Table.” The shares are down just over 11% since then, against a gain of about .6% for the S&P 500. Distracted by this pesky voice in my head droning on some nonsense about “hubris” and “pride goeth before the fall” etc., I want to review this name again to see if it makes sense to buy at current levels. After all, a stock trading at $33.50 is a much less risky investment than the same stock priced at $37.70. I’ll make that determination by reviewing some of the macro factors driving this industry, and thus this stock. Of course I’m also going to write about the valuation. Finally, I’m going to write about put options as a way to simultaneously enhance returns while fairly massively reducing risk.

I’ve heard from various sources over the years that my writing can be “a little much.” Because I couldn’t live with myself if I wasn’t trying to make your reading experience as pleasant as possible, I offer a thesis statement at the beginning of each of my articles. This gives you more than you get from simple bullet points, while exposing you to as little “Doyle mojo” as possible. I like Greenbrier shares at current levels, so I’ll be adding a few shares. In terms of specifics, I previously sold 800 of the 1,000 shares I owned, and will be buying back 300 at the earliest opportunity. Additionally, I’ll be selling 5 of the deep out of the money puts I write about below. The shares have fallen sufficiently in price to put reasonable strike prices within reach, and I want to take advantage of that. I like the visibility in the backlog, the fact that the backlog is growing reasonably well, and at a higher average price per unit. Thus ends the thesis statement portion of the article. If you read on from here, that’s on you.

Revenue Visibility

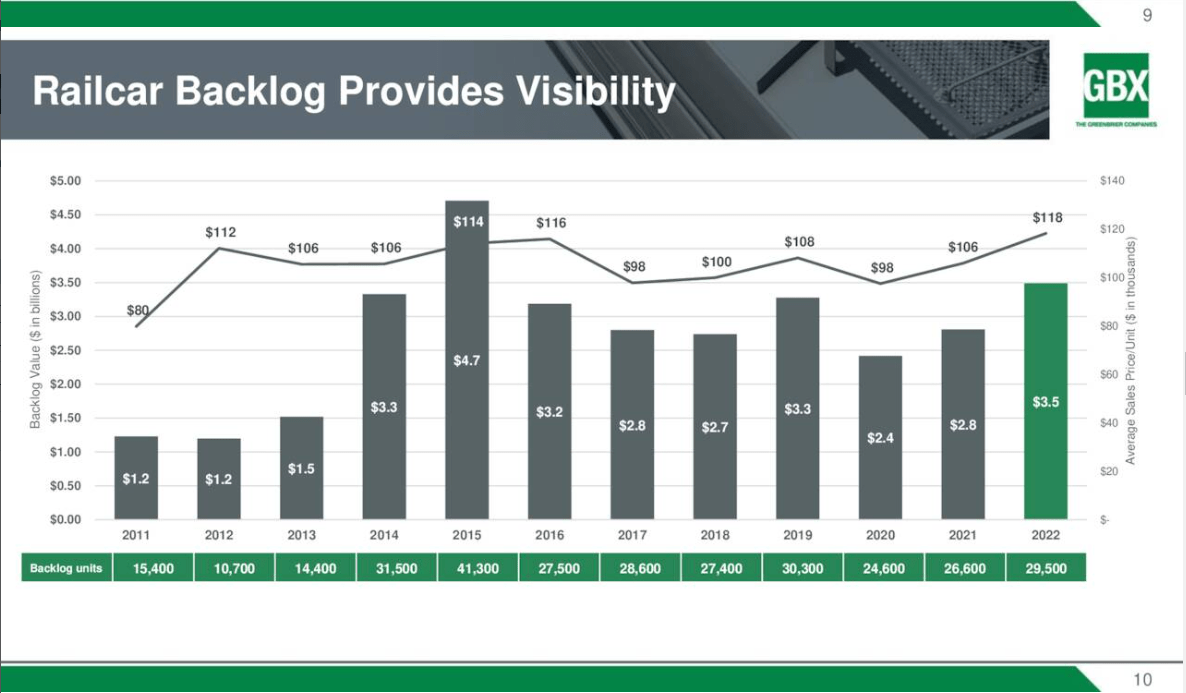

One of the things I’ve always liked about Greenbrier is the fact that future revenue is fairly predictable. This is because of the fairly robust backlog in orders. Additionally, we see that the size of the backlog has picked up nicely, and the average price per car is at a multi-year high per the following:

Greenbrier Order Backlog (Greenbrier investor relations)

Some portion of this increased selling price is a function of inflation, but I think it’s also related to the fact that railcar demand remains robust. In my previous article, I whined about the fact that the dividend payout ratio had reached 77%, but I think the unmoving dividend is reasonably well covered at current levels. If you want a more in-depth review of my thoughts on the financial history here, I’d recommend perusing my earlier work on this name. Suffice to say, I think the dividend is reasonably secure, and that the financial performance in 2022 was generally quite good. I’d be very happy to buy back into this name at the right price.

The Stock

My regular readers know what time it is. It’s at this point in the article where I describe how I think a reasonably good company like this one can be a terrible investment at the wrong price. This is because the “company” and the “stock” are not the same thing. They’re not even close, actually. The company pays for a host of inputs, like skilled labour and rolled steel, adds value to those, and sells the results to the Class 1 railroads, for example. The stock, on the other hand, is a piece of virtual paper that gets traded around in a marketplace. The stock is impacted by a host of variables that have little to do with the business. For example, the stock might be impacted by the pronouncements of a fashionable analyst. The stock might move around based on the rising and falling demand for “stocks” as an asset class. Most bizarrely in my view, the stock may be impacted by the pronouncements of a Fed official, as if a 50 basis point move in the overnight rate matters all that much. Given that the business chugs along (forgive the pun) and the stock is much more volatile, there’s sometimes a disconnect between what’s going on with the company, and what’s going on with the stock.

In my experience, the only way to trade stocks profitably is to spot discrepancies between these two, and buy when the market is overly pessimistic, and sell when the market is overly optimistic. I really, really hate to brag about it, but this is how I’ve done well trading this stock over the years. Those who read my stuff know that I measure the pessimism embedded in price in a few ways, both simple and complex.

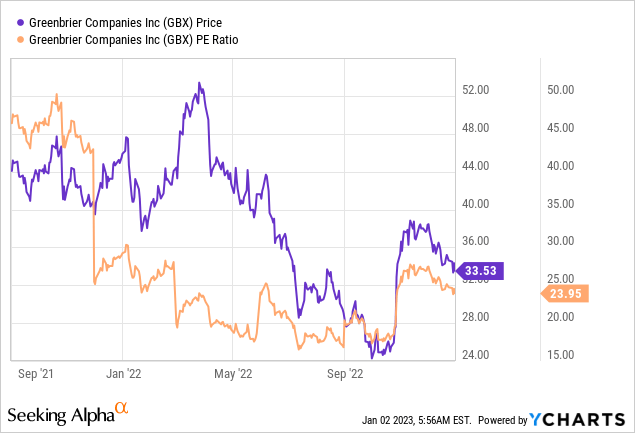

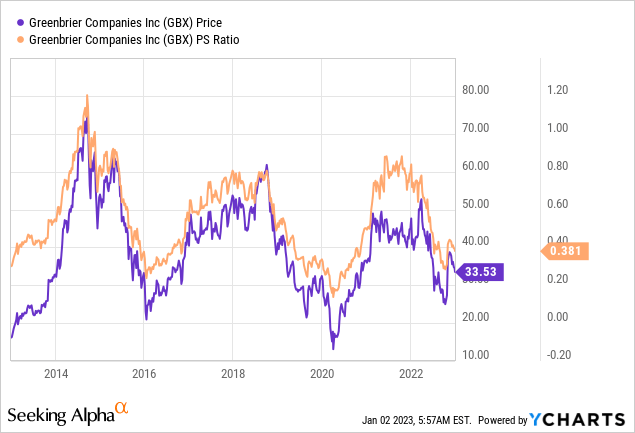

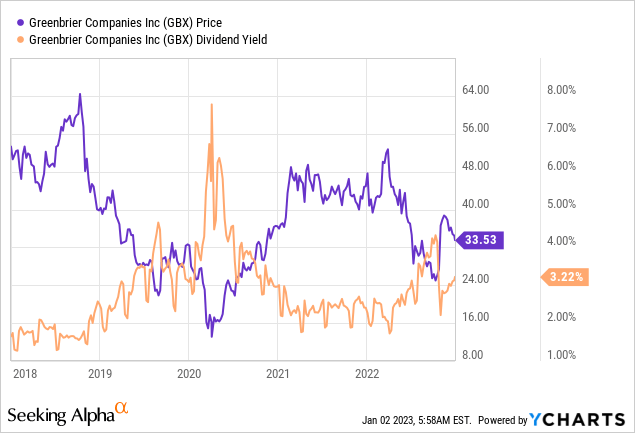

On the simple side, I like to look at the ratio of price to some measure of economic value like earnings, free cash, sales, and the like. I like to see a stock trading at a discount to both the overall market and its own history. Unsurprisingly, the shares are about 11% cheaper today than they were when I last reviewed the name. I also like the fact that the dividend yield is about 10.25% higher now than it was previously.

My regulars also know that in addition to looking at ratios, I want to try to understand what the crowd is currently “assuming” about the future of a given company. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit too thick, you might want to crack the spine on “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Applying this approach to Greenbrier at the moment suggests the market is assuming that this company will not grow from current levels, which I consider to be a wonderfully pessimistic view. Given the above, I’ll be buying a few hundred shares at the earliest opportunity.

Options As Alternative

Those who have read my stuff for months now know that I really like writing deep out of the money puts, because I consider these to be “win-win” trades. If the shares remain above the strike price, I pocket the premium and drive on. If the shares fall below the strike price, I am obliged to buy, but do so at a price that I deem acceptable. So, whatever happens, the outcome is a favourable one. Now that Greenbrier shares have fallen nicely in price, we’re once again in range of some decent strike prices in my view. In particular, I like the June Greenbrier put with a strike of $25, which is currently bid at $.65. This is an intriguing trade to me because the premium on this 25% out of the money put annualises out at a rate of about 5.25%. In my view, this is the definition of a “win-win” trade. If the shares fail to drop another 25% in price over the next six months, I’ll simply pocket the premium. If the shares drop in price and I’m “forced” to buy at a net price of $24.35, I’ll be into the stock at a PE of about 17, and a dividend yield of about 4.4%.

It’s that time again. Now that I’ve written about a “win-win” trade, it’s time for me to engage in my semi-sadistic tendency to spoil the mood by writing about risk. It’s all well and good for a stranger on the internet to write about “win-win” trades, but if you’re going to trade these, you need to be made aware of the fact that this investment, like all investments, comes with risk. I consider the risks associated with short puts to fall into two broad categories: the economic and the emotional.

Starting with the economic risks, I’d say that the short puts I advocate are a small subset of the total number of put options out there. I’m only ever willing to sell puts on companies I’d be willing to buy, and at prices I’d be willing to pay. So, I would never advocate that people simply sell puts based only on the size of the premia. In my view, that strategy would lead to disastrous results. So my first bit of advice is to only ever sell puts on companies you want to own at (strike) prices you’d be willing to pay. Take my word on this one, as it’s informed by painful history.

The two other risks associated with my short puts strategy are both emotional in nature. The first involves the emotional pain some people feel from missing out on upside. To use this trade as an example, let’s assume that Greenbrier stock price goes parabolic and shoots to $50 per share between now and the third Friday of June. Obviously, my puts will expire worthless, which is a great outcome in some ways. My upside will be limited, though, by the fact that I’ll only have 500 shares of Greenbrier. So, short put returns are capped by the premium received. This may be emotionally painful, but my attitude is that the benefits accrued from reducing risk far outweigh the potential harm of missing upside, so no harm, no foul.

Secondly, it can be emotionally painful when the shares crash below your strike price. So far, whenever this has happened to me, things have worked out well over the long term, because I insist on only ever writing puts at “screaming buy” strike prices. That said, it has been emotionally stressful in the short term on occasion. If you’re going to sell puts, please be aware of this phenomenon.

If you understand these risks, and can tolerate them, I would recommend that in addition to nibbling on shares at this level, you sell some deep out of the money puts. In spite of their risks, I think short puts offer the best risk-adjusted returns at this point.

Be the first to comment