MesquitaFMS

Company overview

The Gap (NYSE:GPS) is an apparel retail company. The company sells apparel, personal care products and accessories for men, women, and children. Their brands include Old Navy, Gap, Banana Republic, and Athleta brands.

The company’s distribution channel includes stores, franchise stores, websites, third-party arrangements, and catalogs. As of Q3-22, the company had 2,743 company-operated stores and 637 franchise stores.

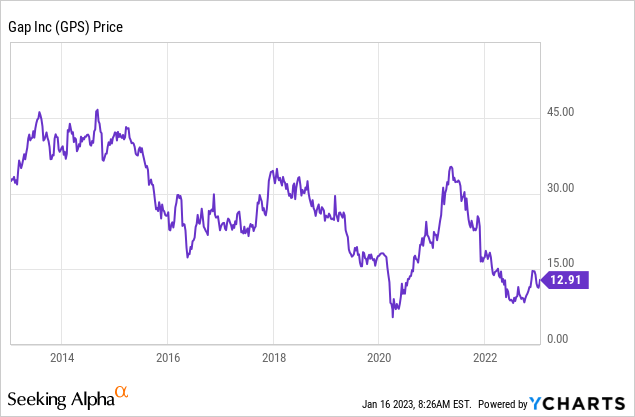

The Gap has found itself struggling in recent years, seemingly being passed by and falling out of fashion. The business has attempted to target a younger generation, who generally dictate fashion trends and are the fast-growing income demographic. Growth has completely slowed across all of their brands and new entrants have taken market share. Revenue between 2002 and the LTM period has remained within $13.8BN and $16.8BN, illustrating the degree of stagnation. We also see this stagnation in their share price below which has persistently declined, except for an impressive reversal in 2020 into 2021.

With the Yeezy deal over (analysis below), now is a good time to assess the quality of the business going forward. We will consider macro-economic factors, as they are a major driver of retail sales, as well as key themes within the retail industry. Finally, we will look at The Gap’s financials and compare it to its peers, in order to assess if it is undervalued.

Yeezy x Gap

Gap has taken several steps to combat this, with the most recent strategy being a partnership with Kayne West’s Yeezy. This was announced in Jun20, with products launched from 2021 onwards. Culturally, The Gap took an unprecedented step up when Kanye brokered a partnership with Balenciaga (OTCPK:PPRUF) (OTCPK:PPRUY), to launch the Yeezy Gap Engineered by Balenciaga line in 2022. This is one of the first times a high fashion brand produced clothing in partnership with a traditional fashion brand. In typical Kanye fashion, the relationship quickly soured (Likely on Kanye’s end) and was officially ended in late 2022.

The question is what has The Gap taken from this short two-year deal. The Balenciaga deal added incredible credibility to The Gap as a modern brand and was invaluable for marketing to the younger generation. For a luxury brand to partner with them shows belief in their quality and brand image. From a financial perspective, Wells Fargo estimated that the Yeezy line would add c.$1BN in incremental revenue, which is 7.2% of FY21’s revenue. Investors were clearly a fan of this as the stock soared when it was initially announced and slumped when the deal was called off. It is difficult to assess the long-term value of this, our view would be that it has shone a light on the business, and it is now management’s responsibility to take advantage. Revenue grew 20.8% in FY22, the largest single annual gain since before 2002, but subsequently declined.

CEO situation

The Gap have been without a permanent CEO since their leader departed in the summer of 2022. Bob Martin the executive chairman is serving as interim president and CEO.

It has been over half a year without the position being filled, contributing to their inability to execute their strategy. The Yeezy deal provided a once-in-a-lifetime opportunity to make valuable inroads into their strategy of shifting customer base but without leadership dictating pace, this seems to have fallen flat. Retail analyst Jessica Ramirez stated, “Gap seems to just constantly miss what the consumer is looking for.” Our view is that the business does not understand what the modern-day consumer requires.

Our belief is that an experienced CEO in retail is required, with a track record of brand modernization of digital marketing. Ideally, multiple hires would be brought in, including marketing and corporate development individuals. As an example, struggling Footlocker (FL) have recruited the former CEO of Ulta Beauty, who grew their online sales fantastically over 10 years. Complementing this, they recruited several other experience individuals, with a view to reinvigorating the brands image.

Old Navy

Old Navy is a discount brand owned by The Gap and was seen as the saviour of the company, with plans drawn up to IPO the brand. Unfortunately, demand slowed and actually declined in FY19. Management attributed this to poor inventory management, but we have not seen a bullish bounce back.

Sales by brand (Annual Accounts 21)

FY21 was an outlier period, driven by pent up demand following lockdown. Looking at Old Navy’s share of total sales, it looks to have stagnated at around 54%, with Banana Republic now growing.

Banana Republic has grown in consecutive years as the brand was able to transition from a workwear-focused brand in the age of working from home. This has come from offering comfortable and smart-casual clothing. This is an example of understanding changing market trends alongside what the target audience wants and responding in kind. This approach needs to be replicated across the other brands.

Economic consideration

Growth wise, things began to slow in 2022. The post-lockdown pent up demand had dried up and conditions were not conducive to discretionary spending, with this continuing to be the case.

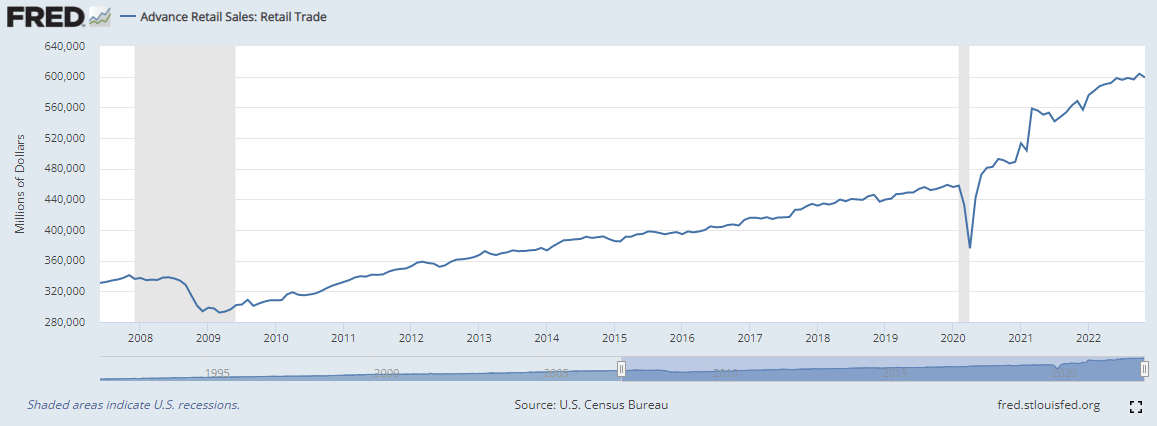

Inflation has risen sharply, with energy costs and wage inflation (initially) at the forefront. In response to this, governments have raised interest rates, with the intention to cool demand further. The US has seen several months of inflation falling, suggesting this is working but there is still more time required. The biggest issue for consumers is that they are being pressured on both fronts, their borrowing costs and spending costs have increased. This has led to a cost-of-living crisis for many households and a reduction in discretionary spending. Retail sales look to have flatlined in since H2 2022.

Retail sales (FRED)

Our view is that demand-side contraction will continue during much of 2023, as interest rates remain elevated. It is still uncertain if a recession will be triggered but regardless, discretionary spending will continue to be reined in. For a retail business, this is very bad news for The Gap.

In the case of retail, we have seen issues on the supply-side also. Wages have increased substantially, predominantly in late 2021 and early 2022. We have seen supply chain issues continue, with lockdowns in China, and the Russian invasion of Ukraine. This has contributed to increased costs and greater disruption, causing a squeeze to margins for many businesses. The Gap has responded by cutting corporate jobs and closing stores, but this has yet to have the impact required.

The only real opportunity we see is for Old Navy. With less discretionary income, consumers will focus their retail spending on budget / discount options, which Old Navy focus on. How much of the downside this can negate is yet to be seen but is unlikely to be significant.

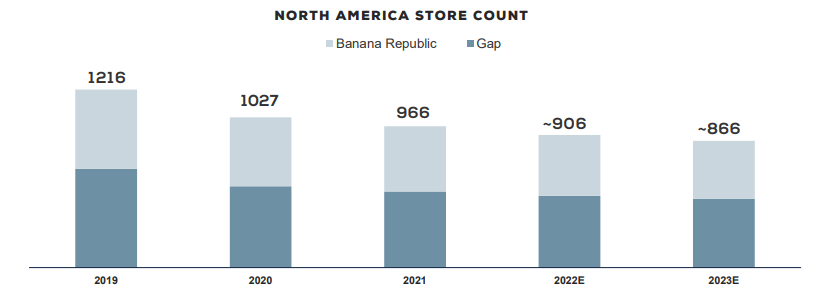

Store closures:

As mentioned above, The Gap is conducting a process of reducing store fronts, as they seek to cut costs and low profit locations. The intention is to cut locations by 29% between 2019 and 2023.

Store closures – GAP (Q3 Investor pack)

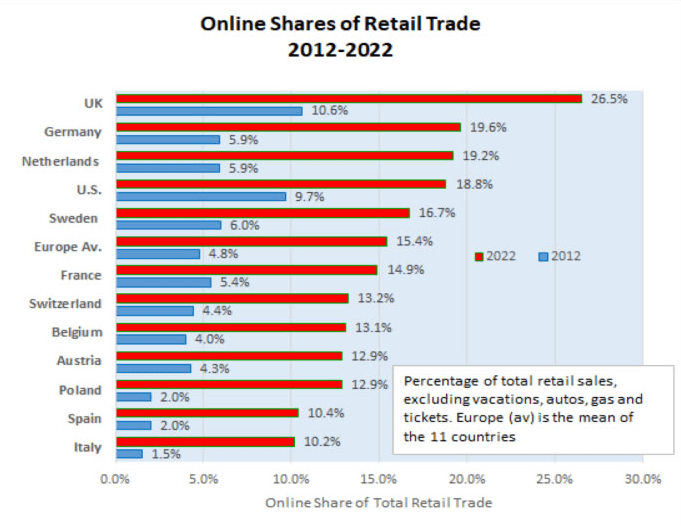

This is not a bad strategy, as online sales have grown faster than brick-and-mortar for several years consecutively. As the graph below shows, the online retail market in the US now accounts for 18.8% of the total market. This would allow The Gap to reduce its fixed costs, thus increasing margins, while allocating a portion of costs to driving online traffic.

Online retail sales (Retail research)

There are two problems with this. Firstly, trends are showing resilience in brick-and-mortar. For the first time ever, B-A-M outgrew online sales in 2021, with consumers saying they valued the instore experience.

Secondly, The Gap has shown weak online penetration. Prior to COVID-19, online sales were a mere 25% of total, increasing to 45% given the lack of optionality. However, following the end of lockdown, consumers look to have moved back to going instore. It is yet to be seen if this trend will continue or normalize at 61%/39% but we would like to see this move closer to 55%/45% as The Gap continues its closures.

Store v. online sales (Annual accounts 21)

This said, we think COVID-19 has benefited the business here. 61/39% is a fine ratio given this company is historically known for storefronts. Had COVID-19 not occurred, it’s very unlikely that the business would have transitioned so quickly.

Financials

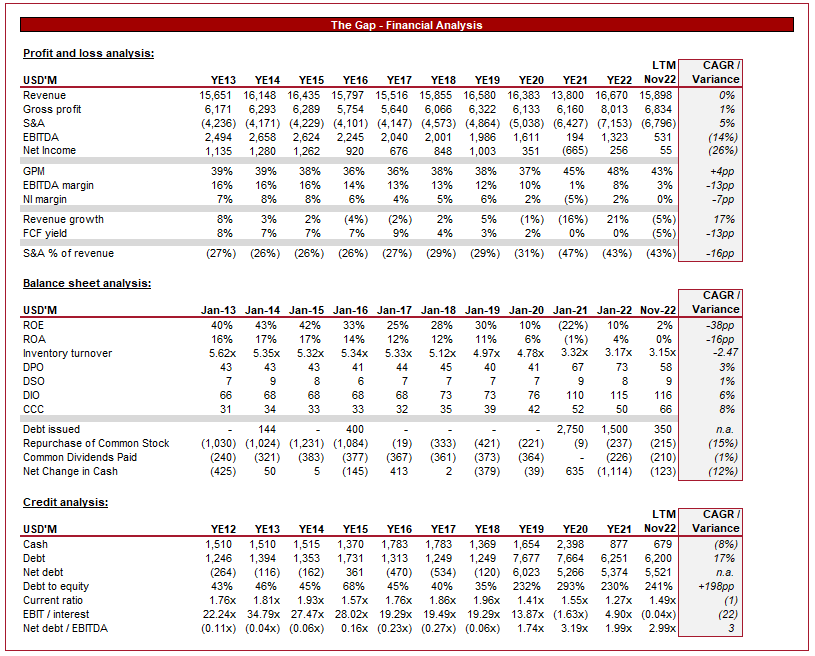

GPS – Financials (TIKR Terminal)

Revenue growth has been non-existent, fluctuating between $15.5BN and £16.7BN (excl. COVID) for 10 years. The reason for this is a decline in the Gap brand, while Banana Republic and Old Navy have grown. The real problem is that BR and ON are nothing special as standalone brands and so the business is left without a flagship.

GPM has improved in recent years due to success in passing on inflationary costs, and also demand driven price hikes. This has begun to shift in the other direction, with costs continuing to increase but a lack of demand leading to discounts. This GPM deterioration trickles down to EBITDA and NI. The Gap may have cut employees, but this will not compensate for freight, energy and other costs which have risen substantially.

When considering operational efficiency, we observe inventory turnover decreasing. Alongside an almost doubling in their cash conversion cycle, the business is struggling to move inventory. The problem with this is that they are more likely to discount stock, which leads to tighter margins.

We also observe strange cash management, with several years of negative cash movements, while still choosing to pay dividends / buying back shares. This is all while further debt is raised by the business. This does not look good to us, as it is clear the business is expending more than is sustainable and raising debt to balance their cash needs.

From a credit perspective, we have seen debt grow at a CAGR of 17%, with debt to equity reaching 241%. The company’s debt interest coverage has also declined, meaning cash may need to be expended to fund 2023’s payment. We do not see evidence to suggest solvency issues, but funding may need to be raised in late 2023.

Peer group analysis

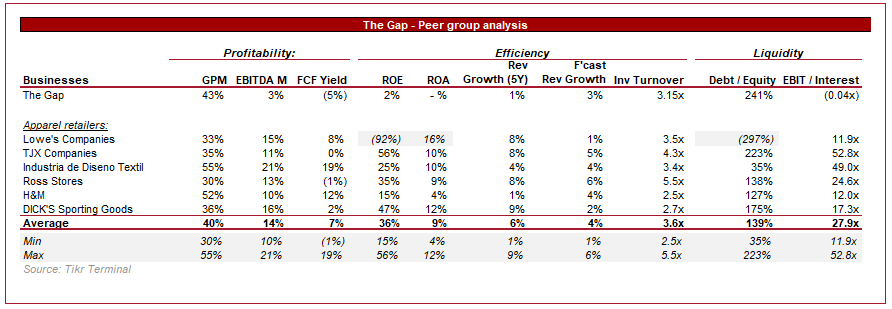

Peer group analysis (TIKR Terminal)

The Gap is completely outclassed relative to its peers. They are significantly less profitable, even if we compare their margins several years ago. Efficiency is poor and growth is noticeably below average.

We expect The Gap to trade at a comfortable discount to its peers for these reasons, there are basically no redeeming qualities.

Valuation

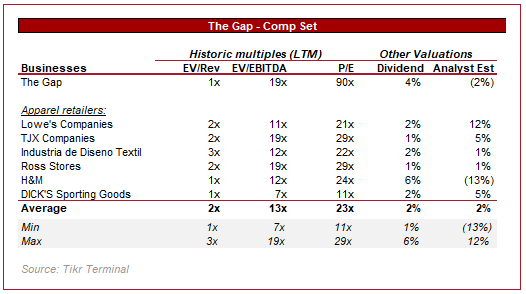

Peer group valuation (Tikr Terminal)

Due to the sharp contraction in margins, we have not seen a re-rating of the valuation fully. The Gap’s EBITDA multiple has shot up to 19x from c.7x, as EBITDA has more than halved. The business is likely overvalued and may see further bearish sentiment if demand continues to fall.

Conclusion

The Gap is a culturally important business which has innovated and made its impact on the fashion industry. At some point in the last 20 years however, it lost sight of the customer, and has never really recovered. Our view is that The Gap is a case study on ineffective management, with many problems derived from a lack of quality decision making.

Now we are left with a low-quality business, which among the worst in the retail large cap space. For some reason, Management is choosing to pay dividends and buyback shares as it struggles to post consistent profits, suggesting the lack of long-term thinking.

Finally, the one opportunity to bring The Gap back came and went without so much as a squeak, as The Gap’s revenue falls in the LTM period.

We do not think this stock will go to zero or decline substantially but apply a “strong sell” rating because we believe there is no vision for any kind of improvement.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment