The advanced economies of the world continue to reel from the coronavirus. Markets across the space that began their descent in late February have fallen sharply in March as the coronavirus has taken hold beyond the reaches of Asia where its first victims now lay dead and buried. The impact on markets across the board has been just short of stunning. Multiple trading time-outs have triggered on US exchanges. All US exchanges now wallow in bear territory, bringing to an end the 121-month bull market that stretched back to March 2009. In the US Treasury market, yields have fallen to record lows as retail and institutional capital worldwide continues to pour into dollar-based, safe harbor assets. Oil prices on the New York Mercantile Exchange are at lows last seen in February 2002. The current plunge in oil prices worldwide is both a function of falling demand from the pandemic as well as the continuing rift over production quotas being waged by Saudi Arabia and erstwhile ally, Russia. Last week’s new 30-year debt issues from Exxon Mobil (XOM) and JPMorgan Chase (JPM) saw spreads with comparable Treasuries soar to 220 basis points and 357 b/p while Occidental (OXY) 10-year notes hit a spread of 762 b/p, according to MarketAccess data. Heightened spreads mean that many bonds are just not trading as market liquidity slowly evaporates, creating severe dislocations and price volatility across a wide swath of the market. Meanwhile, the dollar continues to strengthen in global forex markets as funding shortages have accentuated the race for dollars, further placing the US and global growth at risk. Forex bid-offer spreads for major currencies continue to rise from not only global funding shortages, but from the sheer number of absent traders working from home, reducing the availability of people to transact trades. The dollar approaches an 18-year high. The debate on the economic impact of the pandemic on supply chain disruptions in manufacturing has moved on to the wholesale closures of non-essential businesses, self-isolation and the makings of one of the largest contractions in consumer spending on record. To date, seven global banks have published forecasts outlining a global recession already in progress. Recent consumer confidence data published by the European Commission sketched out a five-year low, making Friday’s survey by the University of Michigan of US consumers during the month of March all the more anticipated. The number of first-time US workers applying for unemployment benefits increased to 281,000 through the week ending March 14 – the highest level since the week ending September 2, 2017. A significant increase is expected for the week ending March 21. Meanwhile, business activity hit record lows in the US, Europe and China during the month of February, with even darker statistics of March yet to come.

On Monday, 90 minutes before markets opened, the Federal Reserve dusted off its bazooka, aimed and fired. The central bank lopped off a full 150 basis points off the Federal Funds rate earlier in the month, bringing the benchmark to zero. The effective Federal Funds rate is now 0.15 basis points through the 20th of March. It is now buying commercial paper for the first time since 2008, shoring up market liquidity in its role as lender of last resort. Short-term Treasury bills and mortgage-backed securities purchases in unlimited amounts likely going far beyond the initial $700 billion in Treasury and $200 billion in mortgage-backed securities announced earlier in the month. Instead, the Fed promised to buy what it takes to make markets functional, a role that could easily extend the Fed’s authority far beyond its 2008 playbook. A new facility was unveiled, aiming to support large private sector employers by offering up bridge financing for durations of up to four years to investment grade companies – a particularly delicate sector of the market where about 55% of investment grade companies sport BBB credit ratings while further credit downgrades of revenue-starved companies loom ominously on the horizon. Participating businesses would be allowed to defer principal and interest for up to six years and would not be allowed to use Fed funds to buy back shares or pay dividends to shareholders. In a throwback to the 2008 financial crisis era, the Fed revived the Term Asset-Backed Securities Loan (TALF) facility that gives the Fed the ability to buy securities backed by student loans, car and credit card loans while opening the door to lending directly to small businesses through the Small Business Administration. A disaster loan program is already up and running through the SBA that Congress authorized $7 billion in funding. Disaster loans are direct issues of the government rather than made by banks in conjunction with existing SBA small business lending programs.

The Fed’s newest lending facilities essentially bypass the traditional role of banks and Wall Street dealers which have increasingly been pushed aside by algorithmic market makers that have increased trading efficiencies and lowered costs, but have much smaller balance sheets than the banks of old. Market liquidity has suffered across large swaths of the market. The Fed has flooded markets with cheap loans to little notable effect. The question moving forward as the Fed awaits a fiscal infusion from ongoing Congressional negotiations is just how quickly the Fed’s programs can restore investor confidence and reverse the continuing market slide while preventing any lasting damage to the greater economy at large.

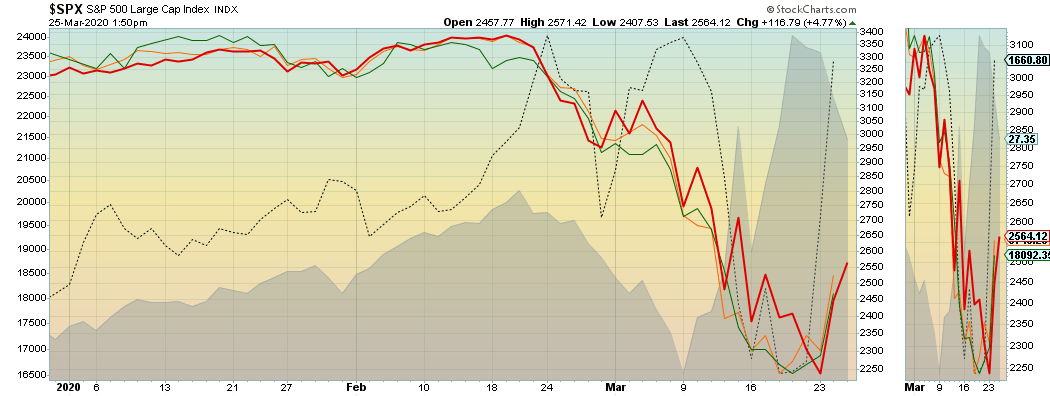

Figure 1: The S&P 500, German DAX, Japanese Nikkei and Gold against the US Dollar

{kind=link}

The major indices opened sharply higher on Tuesday (March 24) with stocks climbing most the day on news that a $2 trillion fiscal stimulus package was close to fruition. The S&P benchmark (red line, Figure 1 insert, above) soared 9.4% on the day, though still down 24% from its February high. Before Tuesday’s market swoon, the benchmark had fallen just short of 28% since its February 19 high, the fastest ever market plunge from a record high to a bear low, shedding a whopping 939 points in the matter of 24 trading days. The yield on the 10-year Treasury remained largely unmoved by the Fed’s actions, settling at 0.81% for the session and down a whopping 55% on the year. Japan’s Nikkei (green line) also responded positively with an 8.62% increase, though down 22% on the year. The German DAX (orange line) was up 10.98% at today’s market close but down almost 28% on the year. Gold (black dotted line) is down 2.46% from its late February high but is up just over 13% from its low the yellow metal was forced to sketch out as investors essentially cashed out of the market in the third week of March. Gold has risen almost 4% since the Fed’s market intervention on Monday, reassuming its more traditional safe-haven role. While a weak dollar and rising inflation are more traditionally associated with surging prices of gold, the race for greenbacks (grey area) through much of March demonstrated just how distorted markets had become. The Fed’s opening up of dollar swap lines with Brazil, South Korea, Singapore, Mexico, Australia and four other central banks produced the main driving force behind the late March surge in gold. On the other side of the Forex trade, the Mexican peso lost about 28% of its value against the dollar in March while the Brazilian real dropped about 13% against the dollar. The slide has added upward cost pressure on dollar debt servicing in both countries. The servicing of dollar-denominated debt in the emerging markets space continues to be a worry, with both the International Monetary and World Bank earmarking emergency funding facilities to mitigate the growing problem. Markets continue to struggle with a black swan economic shock of unknown proportions.

Access to credit and market liquidity, the efficacious deployment of a fiscal package and a verifiable slowdown of the infectious spread of the coronavirus worldwide is clearly the holy trinity of market stabilization moving forward.

On the first leg of this journey, the Fed’s market moves to date have forcibly targeted clear areas of liquidity deficiency, including investment grade corporate debt where BlackRock’s (NYSE:BLK) iShares 0-5 Years Investment Grade Corporate Bond ETF (SLQD) appears to be a recent beneficiary. Other important corners of the bond world running short on liquidity include mortgage-backed securities that funnel liquidity to the all-important housing market. The SPDR Portfolio Mortgage Backed Bond ETF (SPMB) troughed on the 12th of March due mostly to market dislocations rather than any change in underlying market fundamentals. The issue has since rallied almost 14% in the wake of the Fed’s MBS purchase announcement. Municipal debt is also beginning to see the light at the end of the tunnel. The Invesco Oppenheimer Rochester® Fund Municipals Fund (RMUNX) which cascaded deep into bear territory since peaking in the last days of February, nosed out a 1% gain at today’s market close (24 March). What is interesting about the Fed’s Monday intervention was that bond prices generally rallied at the same time that stock prices generally fell. In recent market selloffs, both stock and bond prices fell sharply and in unison, implying a strong, wholesale desire by retail and institutional investors to turn securities of whatever flavor into cash. Treasuries and gold, in defiance to their traditional safe harbor status of old, figured prominently in the selling deluge (see Figure 1, above). The Fed’s forceful market intervention has sparked small but encouraging signs of market normalcy. It goes without saying that monetary policy in its many forms cannot by itself tame the current pandemic crisis.

The fiscal stimulus leg of the trinity is a make-or-break proposition for the overall intervention package. To date, the leg remains sketchy as the various stimulus packages dance through the halls of Congress. According to news reports, the $2 trillion package has clearly helped with ongoing market sentiment, causing a selloff of Treasuries and a subtle weakening of the dollar (see Figure 1, above). The fiscal component will likely take on myriad forms. The final proposal is rumored to include a one-off $1,200 direct payment, which will include funds for the self-employed and part-time workers normally left out of direct payment plans of the past. “Helicopter” infusions will likely create a robust environment for new money investments in gold as dollars flood US mailboxes and businesses continue to scramble to replace lost revenue streams in the intermediate term. To that business end, an estimated $500 billion will become available for the Treasury to make loans, loan guarantees or investments in support of businesses. Attached to that money is a 5-member appointed Congressional panel and inspector general to oversee the distribution and deployment of the funds. Roughly $130 billion will be earmarked for hospitals and another $150 billion will go to state and local governments to offset increased safety net costs due to the pandemic.

The third leg of this journey is more problematic. The large-scale testing and quarantining in the environs of New York City, following the largely successful containment model of South Korea, has sent the numbers of those infected to levels that rival the country totals of France, Iran, Germany, Spain and even Italy where new case counts are running well over 1,000 per day. Pressure from business quarters has been very vocal for a more nuanced approach that would quarantine those infected with the virus from those unaffected with the latter being allowed to return to the workplace and to ward off further economic implosion. (Amazon (AMZN) confirmed two new cases of coronavirus in its Oklahoma and Michigan fulfillment centers but has so far resisted closing down the facilities.) The two approaches have publicly butted heads with each accusing the other of irresponsibility. Yet, given the crush for masks, gloves, ventilators, hospital beds, sanitizing wipes, testing kits, protective suits – not to mention trained staffing – it’s next to impossible to maintain even a semblance of a functioning economy without first containing the spread of the virus. Meanwhile, lingering trade sanctions and tariffs wreak havoc on already stretched global medical supply chains. The current health emergency clearly presents a defining moment for current economic decision makers. The business cycle has given way to a global public health and economic disaster. Unfortunately, global economic contraction is inevitable. The question moving forward is to limit the damage.

The coronavirus is the first pandemic declared in a century. And unlike the 1918-19 flu pandemic that claimed up to 50 million victims worldwide, the current pandemic takes place without the backdrop of world war. Covid-19 has created a one-off economic shock. The virus has a finite incubation period and as such is temporary in nature and will pass into history in due time. If its statistics are to be believed, China’s Hubei province reported no new cases of confirmed infections and no new cases of suspected infections. If China can avoid a second wave of viral outbreak in the fall, the country is poised to becoming the first large economy to largely recover from the Covid-19 pandemic. With the thought in mind, Oxford Economics of Hong Kong is projecting an 8% quarter-over-quarter bump in economic activity in the second quarter. Here in the US, Credit Suisse (NYSE:CS) projects the S&P 500 at 2700 by the end of the year, down almost 17% on the year but up 6.38% from its current level. Initial projections of 1st and 2nd quarter GDP growth in the US remain decidedly negative and are expected to fulfill the technical definition of a recession. The 3rd and 4th quarter growth estimates will likely see dramatic QOQ improvement as the lasting economic impact of the pandemic fades. Current paper losses should subside accordingly. Full market recovery will likely take the better part of a year. We shall see.

Disclosure: I am/we are long AMZN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment