Douglas Rissing

Last week’s market ride was driven by two major press releases on Wednesday and Friday. The first was the Federal Reserve’s decision to raise its benchmark interest rate by 25 basis points to 4.5 to 4.75 percent. While the move was expected by the markets, the press release along with Jay Powell’s comments during the press conference had markets pricing future rate cuts with equities rallying and medium range Treasury rates plunging.

Then, the January employment report was released on Friday, showing over 500,000 jobs were created last month. The market reacted by reversing Wednesday’s course. At the end of the day Friday, one fact remained clear, market participants were at odds with the Federal Reserve’s pathway, a dichotomy that could have volatile consequences for the equity markets.

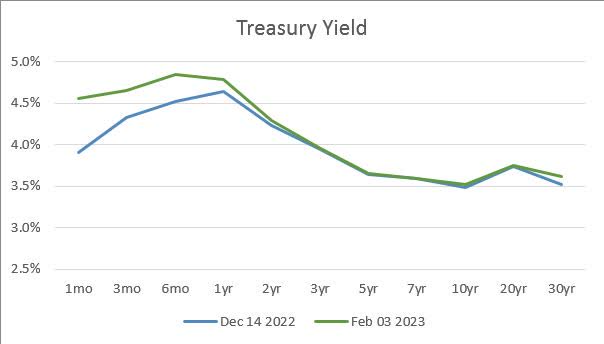

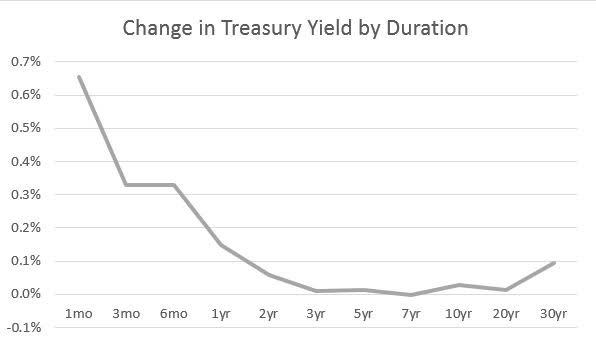

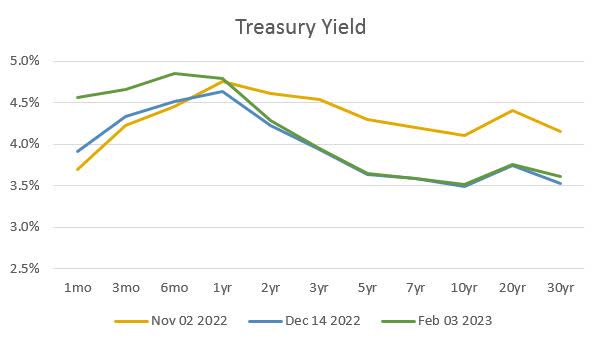

While interest rates moved all over the place between Wednesday and Friday, they remain fairly settled compared to the last Fed meeting in December. Treasury maturities of three to twenty years are trading at near identical yields compared to the previous Fed meeting. Short term rates are trading to account for the incremental interest rate increases in the Fed funds rate. The inversion is steepest between the 6 month and the 10-year Treasury, currently standing at an unprecedented 133 basis points. Treasuries maturing longer than one year remain at yields below where they were after the November Fed meeting.

Federal Reserve FRED Database Federal Reserve FRED Database Federal Reserve FRED Database

An inverted yield curve has consequences for the economy. The biggest consequence is the availability of credit. Financial firms like to borrow short and lend long, thus using duration as a form of arbitrage to offset financial risk. With an inverted yield curve, the cost of acquiring funds is much higher and must be passed on to consumers. The jump in mortgage rates is a good example of this practice, and companies that invest in and/or originate mortgages can expect compression to continue in their interest earnings less borrowing costs (also known as net interest margin).

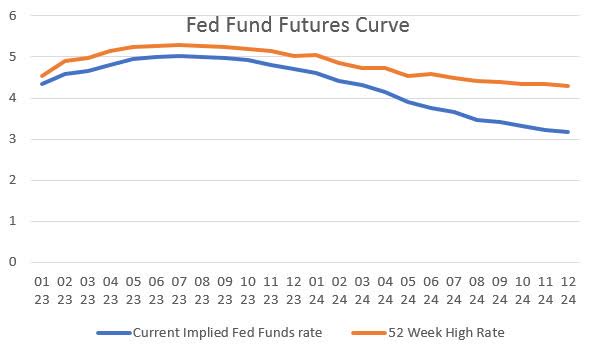

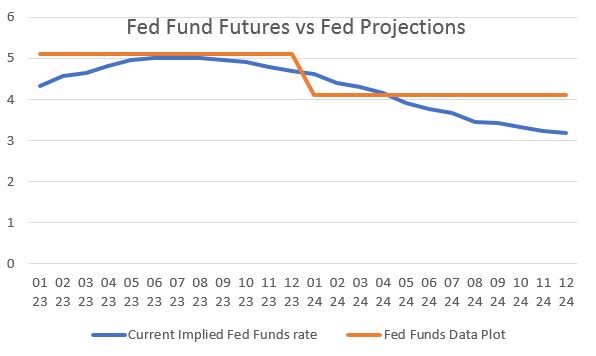

In terms of looking ahead, the Fed fund futures do a good job of expressing the market’s forecast for future Fed rate action. While the terminal rate, or highest interest rate of the cycle, appears to have moved from May to July of this year, the Fed funds rate projections are more than 100 basis points lower than what they were projected at their 52 week high after the November Fed meeting.

Barchart Barchart

Where the disconnect seems to be most prevalent is in late 2024, where Fed fund futures are pricing approximately 100 basis points lower than the Fed’s most recent projections. December 2024 Fed fund futures did sell off by 25 basis points on Friday, but the trend dating back to the November Fed meeting shows a constant price increase, implying a lower Fed funds rate.

Fed Data Plot & Barchart Barchart

The further apart the Fed and market go, the more volatile equity and debt markets will react to economic news suggesting a certain direction for the economy. For now, I am siding with the Fed’s determination to stamp out inflation and continuing to build cash. With excess liquidity, I am investing in 3 to 6-month Treasury bonds so I know my cash is generating a return while trying to feel out a direction for the market.

The Federal Reserve’s meeting on March 22nd will be interesting as the committee will update its economic projections last made in December.

Be the first to comment