Kameleon007

Investment Thesis

Increased skin health awareness has benefited The Beauty Health Company (NASDAQ:SKIN) over the last couple of years. Looking forward, I believe the company should continue to deliver strong revenue growth, benefiting from healthy demand for its Hydrafacial treatment globally and expansion of its footprint to new locations, retail stores, and medical spas worldwide. Margins should benefit from normalized investment levels beginning from 2023 and higher volume generation. SKIN is an attractive multi-year growth story and given its good growth outlook, I have a buy rating on the stock.

Revenue Outlook

The Beauty Health Company is experiencing healthy demand for its Hydrafacial delivery systems due to increasing consumer awareness and prioritization of skin health globally. The company quickly recovered from the 2020 COVID-related sales decline and surpassed pre-pandemic levels in FY21.

The growth momentum continued in 2022 as well. The company benefitted from its omnichannel presence and increasing brand awareness due to its digital and influencer marketing. The company sold ~6500 delivery system units in the first three quarters of 2022, which was greater than the full-year unit sold in 2021. In the third quarter, sales benefited from increasing global consumer demand at medical spas, sales momentum for Syndeo (a new delivery system launched in March 2022), and retail expansion. The healthy demand was partially offset by FX headwinds.

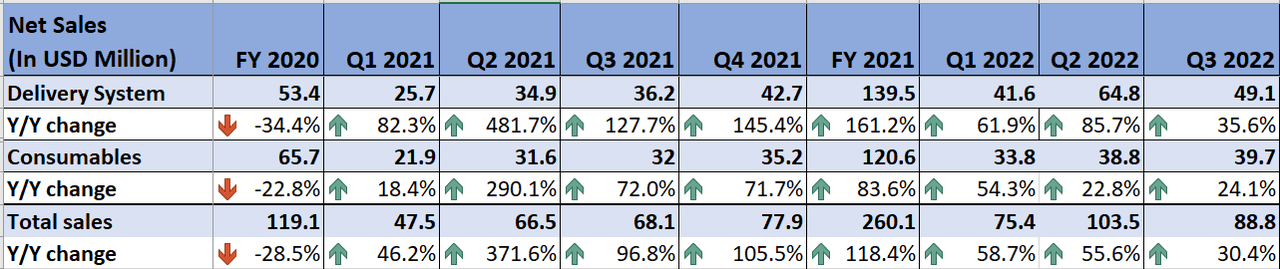

SKIN’s Historical Revenue from Delivery System versus Consumables (Company Data, GS Analytics Research)

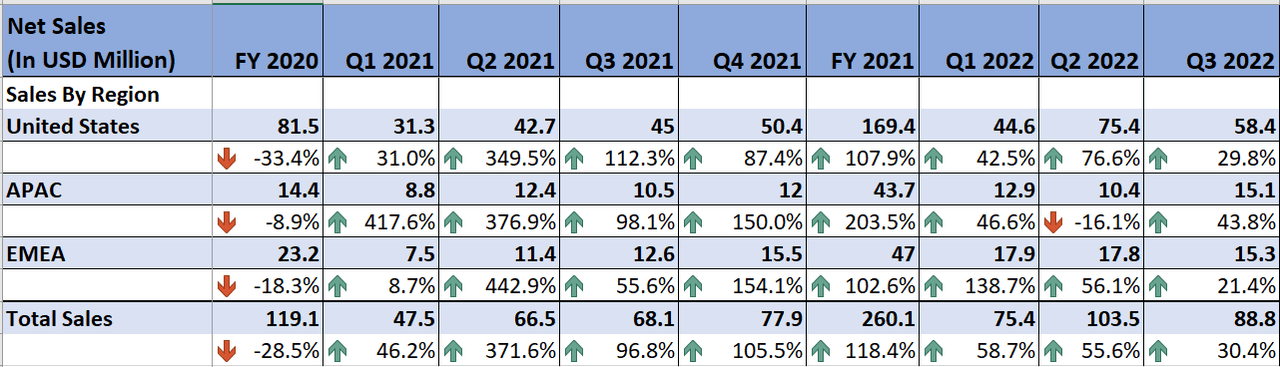

SKIN’s Historical Revenue by Region (Company Data, GS Analytics Research)

Looking forward, I believe the company should continue to benefit from healthy demand and an increasing footprint globally. In the third quarter of 2022, SKIN entered its first One Hotel location in Kauai, Hawaii along with expanding to iconic hotels like the Mandarin Oriental in Hong Kong, and The Addition in Miami Beach. The company also launched Hydrafacial in Sephora’s ‘first store of the future’ in Singapore. It also launched in Douglas’ luxury flagship in Dusseldorf, a beauty and lifestyle hub in Germany. In addition, SKIN expanded to new locations with its existing retail partners such as John Lewis throughout the U.K. and Gallery Lafayette in France. This footprint expansion across the globe should help the company add new consumers and deliver sales growth.

Furthermore, the company’s estheticians and skin healthcare providers are its biggest asset, helping in spreading consumer awareness and providing a good Hydrafacial experience. Skincare specialist jobs are among the fastest-growing occupations in the U.S. and are projected to grow 17% from 2021 to 2031. This job growth mirrors accelerating consumer skincare demand.

The prioritization of skin health and wellness has increased over the past few years, and society has broadened the definition of beauty beyond one size or one-skin type. Consumers are embracing their own unique visions of beauty and they seek products that provide health and self-confidence. Hydrafacial has more than 20 skin health boosters (consumable products) to choose from for every Hydrafacial treatment, customizable for all skin types, and personalized skin care solutions. SKIN stands with a Net Promoter Score (NPS) of 44, reflecting good consumer loyalty and satisfaction with the brand. Moreover, increasing men’s attraction to cosmetic procedures and products is also a tailwind for the company’s sales growth. Further, in this increased video call era, and hybrid working model, people focus more on their facial appearance, which should continue to drive demand in the coming years.

Now some readers might also be worried about the weakening economy and consumer spending environment. It might come as a surprise to them but the wellness, beauty, and skincare categories are much more resilient in periods of economic slowdowns as people prioritize spending on small luxuries that make them feel good. The use of beauty products as tracked by the ‘Lipstick Index’ increased during the dot-com bust of the early 2000s as well as the great housing recession. So, despite an inflationary environment and price increases by the company, I expect demand to remain strong. This healthy demand should be further supported by the Chinese economy reopening as the company expands its footprint in the APAC region. Hence, I am optimistic about the company’s revenue growth outlook.

Margin Outlook

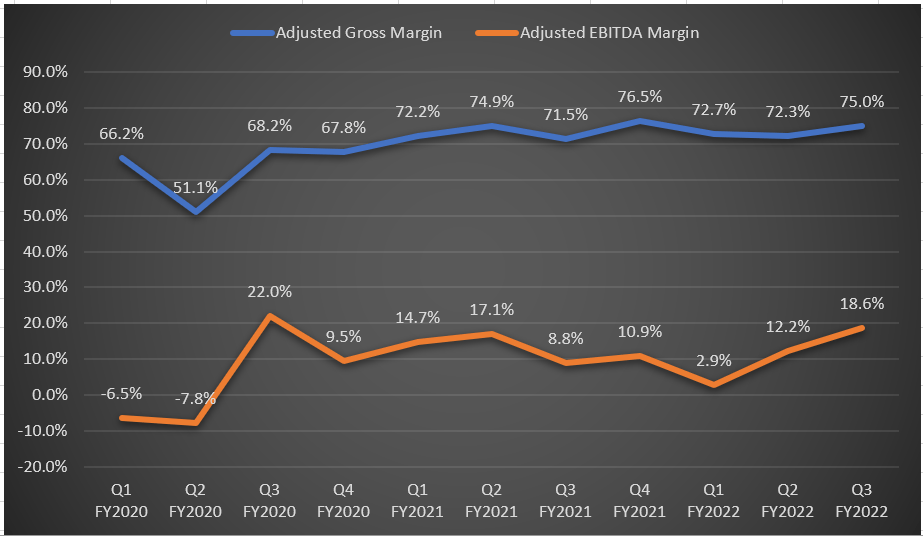

Since its IPO in September 2021, SKIN’s adjusted gross margin is benefiting from fixed cost leverage and the increased selling price of the delivery system. Adjusted EBITDA margin, on the other hand, has been more volatile in the past two years due to the company’s heavy investments in the initial phases as a public company. The company is expanding its experience centers (where the company provides training and education to estheticians related to Hydrafacial), building global office infrastructure, optimizing distribution networks through local manufacturing, implementing ERP, and has increased marketing investments to create brand awareness.

However, over the last couple of quarters, the adjusted EBITDA margin has been improving as the company has started benefiting from these investments along with fixed cost leverage associated with higher volume and better price realization on both delivery systems and consumables. In the third quarter of 2022, the company’s adjusted gross and EBITDA margins increased by 350 bps and 980 bps respectively due to these tailwinds, partially offset by supply chain issues, inflationary pressure, and FX rates.

SKIN’s Historical Adjusted Gross and Adjusted EBITDA margin Generation (Company Data, GS Analytics Research)

Looking forward, after the last couple of years of elevated investments to build scalable infrastructure, management intends to shift its focus toward margin expansion over the next few years and is targeting an adjusted EBITDA margin in the 25%-30% range by 2025. In addition to normalized investments, the company’s margin should benefit from network optimization, higher volume growth, and easing supply chain headwinds.

While upfront costs from Syndeo’s international launch are a slight headwind in the first half of FY23, I am optimistic about the full-year 2023 margin prospects and believe the company should see margin improvement in FY23 and beyond.

Valuation and Conclusion

SKIN is currently trading at a forward P/E of 45.33x FY23 consensus EPS estimate of $0.26. The company has an interesting razor/razor blade model, where it benefits from recurring revenue from selling consumables for its installed base of Hydrafacial equipment. I believe the company is still in the initial phase of its multiyear growth story. While the company’s P/E on FY23 consensus EPS estimates may look pricey, the P/E multiple of 25.94x on the FY24 consensus EPS estimate of 0.45 and 16.03x on the FY25 consensus EPS estimate of 0.73 looks much more reasonable. Given SKIN’s revenue and margin growth prospects driven by healthy demand, increasing footprint, volume leverage, and normalized investment levels, I believe it is a good long-term buy.

Be the first to comment