XiXinXing

It’s not what you don’t know that kills you, it’s what you know for sure that ain’t so.

Written by Sam Kovacs

Introduction

It is one of those things which is just taken for granted. The recession is coming, and there is nothing to do but brace and prepare for impact.

Everyone is now getting cautious and loading up on low volatility stocks (a full 2 years after we suggested doing so), casting more cyclical or discretionary stocks aside.

As if a recession was certain.

The newspapers always hungry for clicks will tell you as much:

My favorite news outlet is the Economist. I don’t subscribe, I’m just there for the headlines. Whenever they write a headline on a topic with a strong view, I become interested in the contrarian case.

They are wrong so often, they have become an indicator in their own right.

They recently wrote: “Why a global recession is inevitable in 2023”.

But they’re not alone:

2023 = Recession is the consensus on Wall Street.

- According to Forbes, 60% Of Natixis Managers Say Recession Is Inevitable.

- Bloomberg says that the “Forecast for US Recession Within Year Hits 100%”.

- The Wall Street Journal writes that “Economists Think They Can See Recession Coming-for a Change”.

Now while they all seem certain, I am not.

Let’s first take a look at why there might not be a recession, and why Wall Street might be biased to think there will be.

Finally I’ll give you 2 undervalued dividend buys using the insights from our analysis.

What would cause a recession?

First let’s agree on what a recession is.

A recession is a period of economic downturn characterized by a decline in GDP, high unemployment, and low business activity.

Recessions are typically defined as two consecutive quarters of negative economic growth.

In other words, if GDP declines in one quarter and then declines again in the following quarter, the economy is considered to be in a recession.

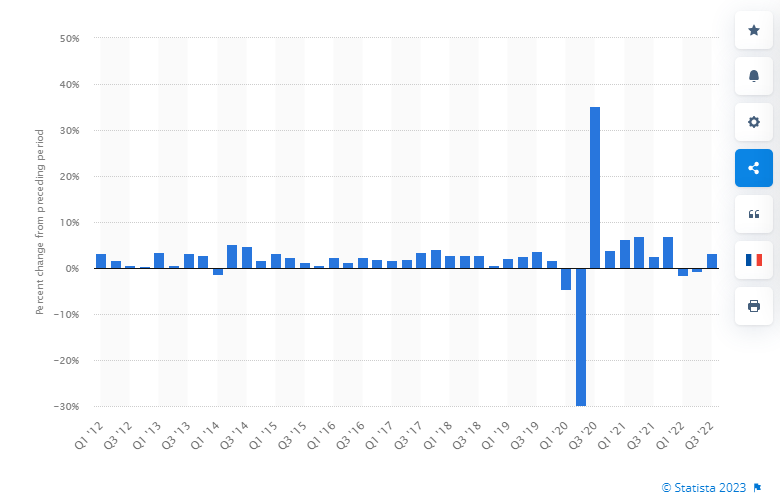

Note that based on this definition, the economy was in a recession in Q1 and Q2 of this year.

US GDP Growth Quarterly (Statista)

Everyone agrees that it was a “technical” recession, which was caused by influences in spending and cashflows from government subsidies during the pandemic which fudges the numbers.

But that is exactly the point. The GDP is a technical metric that is used to measure the size and strength of a country’s economy.

The GDP is calculated with use of four major components:

-

Personal consumption expenditures: This is the largest component of GDP, accounting for about 70% of total GDP. It includes spending by households on goods and services such as cars, food, clothing, healthcare, and education.

-

Gross private domestic investment: This component of GDP accounts for about 15% of total GDP. It includes spending on new capital goods (such as factories and equipment) and changes in the value of inventory held by businesses.

-

Government spending: This component of GDP accounts for about 20% of total GDP. It includes spending by all levels of government on goods and services, including national defense, education, and healthcare.

-

Net exports: This component of GDP accounts for the difference between the value of goods and services exported by the country and the value of goods and services imported into the country. Net exports accounted for about -3% of GDP in 2021.

When it comes to the US economy, components 2-4 are a sideshow.

US consumers are the backbone of the economy in a way which simply isn’t true in Europe or in Asia.

The health of the consumer is the single most important driver of the US economy.

So it’s crucial we understand consumers as a group.

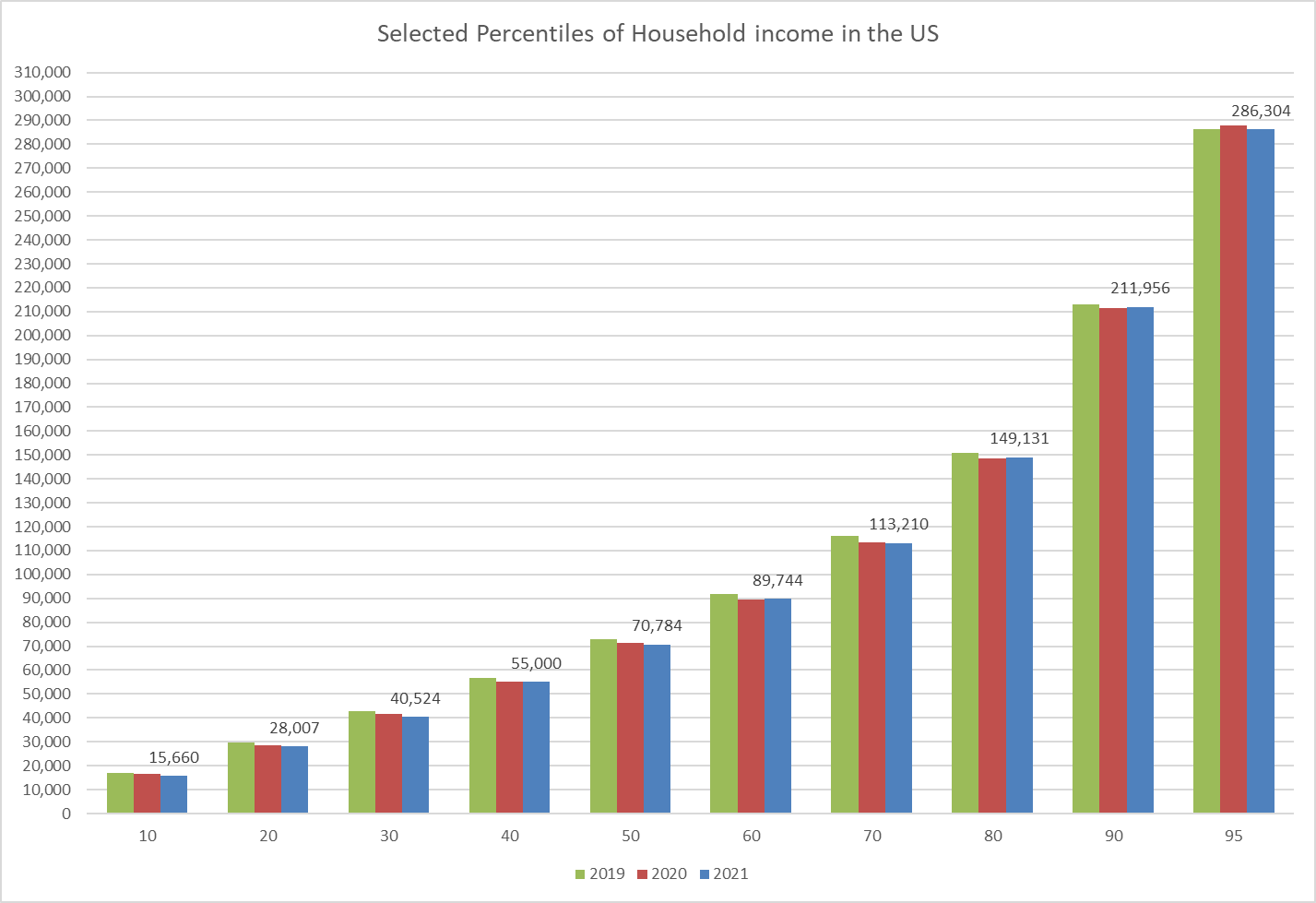

Let’s focus a little on the distribution of income among US Households.

On the face of it, everything seems okay.

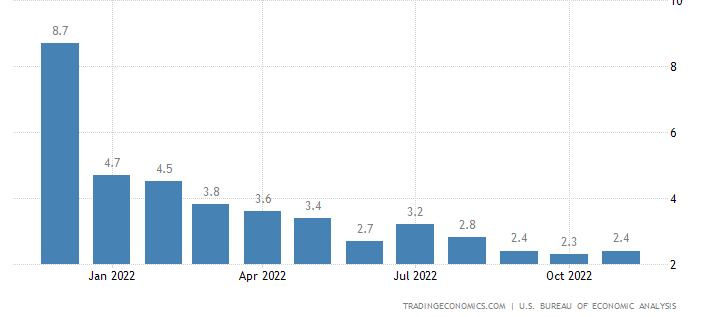

The savings rate, while still very low, is positive, which indicates that as a whole, US consumers are still living within their means.

US Household savings rate (tradingeconomics)

Of course, this likely means that certain Americans are probably being squeezed while others are still healthy.

In 2022, 19.5% of Americans paid a bill late because they didn’t have enough money to cover the bill.

When you look at the distributions of income within the US population, it becomes clear that a $70,784 median household income is casting shade on the 20% of poorest households which bring home $28K per year.

Census

These lower earning households are usually single income households which earn less individual income than the median.

These households are fragile, and always have been. They don’t drive the economy.

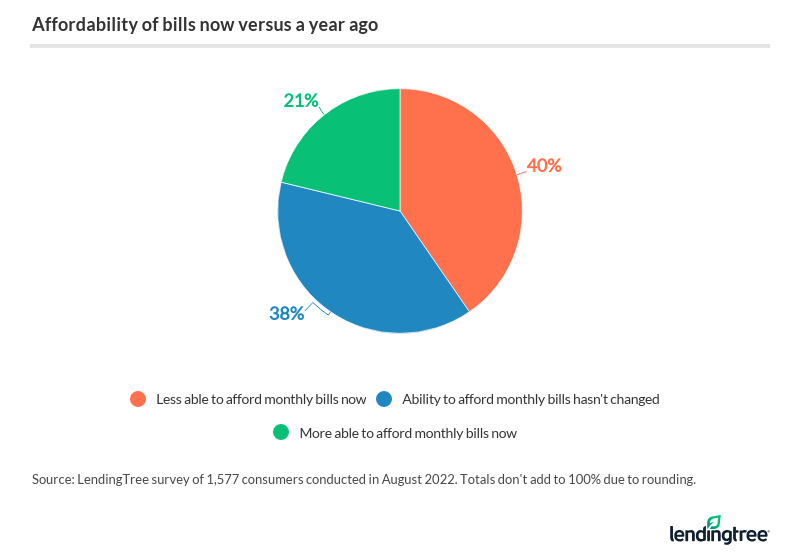

It is likely the lowest 40% of income earners who are finding it less able to afford monthly bills.

LendingTree

So over 70 million households are still just as able or more able to afford bills.

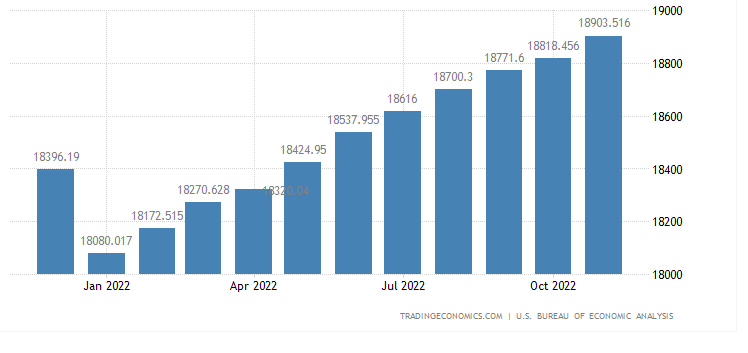

And despite all the “scary talk”, disposable personal income rose 5% from January last year, mostly keeping in line with inflation.

TradingEconomics

For there to be real prospects of a recession, the 60% most wealthy American households would need to feel a strain that they don’t currently feel.

Recent earnings and sales data from certain consumer oriented brands validate this hypothesis.

Costco (COST) saw sales increase 7%, and nearly ALL of that was driven by an increase in the size of the average transaction. Customers are able to pay more, so they do.

I went through the ramifications of this in a note to our members.

Conagra (CAG) continued to see strong consumer spending as prices were increased over the course of the year.

Target (TGT) has seen revenue continue to hold up, although spending has shifted away from discretionary categories, and more towards staples.

What the numbers suggest, is that while relatively there is somewhat of a tightening in the health of the US consumer, with those at the margins feeling the pain more than others, overall, the US spending machine is still alive.

It isn’t even extremely leveraged.

Job growth and income growth have enabled many Americans to keep up with inflation. Americans have in the past sustained long bouts of sub 5% saving rates, while the economy continued to grow!

There is a reason to be optimistic about the US economy.

The numbers are suggesting that things are still holding up.

Why does Wall Street believe it’s inevitable?

Because Wall Street often gets it wrong.

I mean, that’s if Wall Street even believe.

Take Ally Financial (ALLY) for instance.

Ally gets a lot of revenue from auto loans. For the next few quarters, rapid increases in benchmark rates will pressure margins as deposits initially reprice faster than earning assets of the company.

This is being used to quantify the risk of Ally’s business model. But some on Wall Street are interpreting this as a sign of weakness in Ally’s lending portfolio. But that’s not the case, net charge-offs remain below pre-pandemic levels.

So Piper Sandler upgrades it, BofA downgrades it, but nobody agrees.

But when it comes to inflation, they all seem to agree.

Below are snippets of Wall Street’s opinions for 2023:

- Barclays (BCS): We expect advanced economies to slip into recession,

- Bank of America (BAC): The US, euro area and UK are all expected to see recessions next year

- Fidelity: A recession is likely in the US and near certain in Europe and the UK.

- JP Morgan (JPM): Our core scenario sees developed economies falling into a mild recession in 2023.

- Wells Fargo (WFC): We expect a U.S. recession in the first half of 2023,

But it seems to me, that once again, the men in the suits and ties, in their business districts in London and New York, have failed to look beyond their office’s glass window.

Only a massive slowdown in jobs could crush the health of the US consumer.

When looking at the evolution of jobs in 2022, only the sales & office jobs saw a modest decline of 2.5%

| 2021 | 2022 | var | |

| Total, 16 years and over | 155,732 | 158,872 | 2.0% |

| °Management, professional, and related occupations | 66,366 | 69,297 | 4.4% |

| °Service occupations | 24,821 | 25,334 | 2.1% |

| °Sales and office occupations | 30,949 | 30,185 | -2.5% |

| °Natural resources, construction, and maintenance occupations | 13,774 | 14,295 | 3.8% |

| °Production, transportation, and material moving occupations | 19,821 | 19,760 | -0.3% |

Source: bls.gov

But Wall Street has focused instead on the high profile downsizing amongst tech firms and investment banks as value that there is a recession which is going to gain a lot of ground on unemployment.

Goldman Sachs (GS) is cutting 3,200 employees, Meta (META) fired 11,0000, Twitter cut half of its workforce, firing 3,70, Twitter cut half of its workforce, firing 3,700 employees in the process.

But these waves of layoffs are high profile, but not significant in the grand scheme of things.

The weakness in these industries, and in office and sales jobs country wide, tells of a “white collar recession”.

This white collar recession will hit Americans in the wealthier half of households. These households have pent-up savings, and usually have better job mobility within their industries.

This won’t gut the entire workforce, nor will it be an impediment to continued consumption.

While US consumption isn’t boiling hot, it is still at a level which keeps the economy afloat. Rate hikes might have put the brakes on, but I don’t see it grinding to a halt.

Picking stocks if a “soft landing” does happen.

A stock landing succeeded in the 1990s, and it could still succeed in 2023.

Similar set-ups were in place. Supply sourced inflation is going to phase out gradually in 2023, most likely in Q2 once China’s current Covid wave will run its course and the country will be back on the world stage.

This could help infinitely in taming inflation, and is still quite possible.

Stocks that are deeply undervalued, have quality operations, and cyclical upside are to be favored here.

Building a list of these is not easy, as it excludes a lot of names, nonetheless here are a few which pass the test.

Lowe’s (LOW)

There is a reason Lowes is on my list of 5 contrarian high growth dividend stocks for 2023.

There has been an intellectual shortcut taken to get to the consensus: higher rates, tougher housing market, bad for The Home Depot (HD) and LOW.

But as I pointed out in the aforementioned article, this logic is flawed.

As Lowe’s highlighted during its investor day presentation, the home improvement industry can perform well even when the home building market slows.

This was demonstrated empirically in the 1990s. The reason for this is that the demand for home improvement is influenced by different factors than those that drive demand for new home construction.

New home building is closely tied to interest rates and affordability. However, both of these factors are currently less favorable.

Whereas home improvement is influenced by the appreciation of home prices, the age of the housing stock, and disposable personal income.

Lowe’s points out that home prices in the US have risen significantly in recent years, and that the top 40% of income earners still have over $1 trillion in excess savings. Additionally, homeowner equity is at a record high, while the average age of houses in the US is 41 years. Given these trends, it is not surprising that Lowe’s is performing well and beating expectations.

The company’s business is split between DIY/retail sales, which account for 75% of its revenue, and professional clients, which account for the remaining 25%. This diversification works well in the current environment, as home improvement is primarily driven by consumer demand, while home building is driven by professionals.

So LOW is not on anyone’s radar despite a macro setup which is perfect for high quality performance from the company’s business.

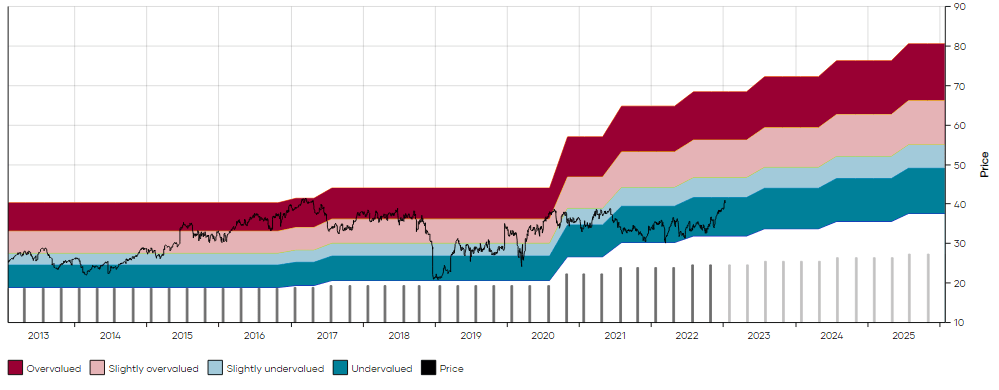

LOW currently yields 2.1%, an unusually high yield for the company, but one it has had many times in the past.

LOW MAD Chart (Dividend Freedom Tribe)

Never in the past decade has buying LOW when it yielded more than 2% been a bad idea. In comparison the 10 year median yield is 1.65%.

The value exists because LOW keeps growing to keep the odds on our side.

LOW is performing in the shadows, but an awareness of its continued success which could happen at the same time as a soft landing, could provide the upside catalyst needed to bring LOW back to historical yields.

Conagra Brands (CAG)

Conagra, a leading packaged food company, recently held its earnings call, where it reported strong financial results for the quarter.

The company’s top line saw an increase, with solid share performance across its portfolio, particularly in its frozen and snacks segments.

While the supply chain is not yet fully normalized, the company sees a long runway of opportunity ahead.

The company reported organic net sales of $3.3 billion, an 8.6% increase from the prior year period. The growth was primarily driven by an improvement in price/mix, which was partially offset by a decrease in volume.

Margin expansion was seen across all segments of the company. The strong performance resulted in an adjusted EPS of $0.81, a 26.6% increase from the prior year.

Retail sales for the company were also strong, with a 10% increase on a 1-year basis and a 26% increase on a 3-year basis.

Conagra was able to maintain its market share while taking inflation-justified pricing actions.

Compared to its peer group, which included Campbell (CPB), General Mills (GIS), Kellogg (K), Kraft Heinz (KHC), and J. M. Smucker (SJM), Conagra ranked second in dollar sales growth and first in unit sales performance.

A key point to consider is that last year, management had been reactive with pricing efforts to compensate for inflation, which lag before showing in financials. The benefits of this strategy have started to show in the past quarter and are what have led to the impressive increase in revenue, margins, and earnings.

We recommended Conagra to members of the Dividend Freedom Tribe in November 2021.

At the time, the stock had been dropping, shedding 25% of its value from $40 to $30.

The reason for the drop in price was due to higher than expected inflation which has pressured margins at the company level. But I highlighted that pricing actions were being rolled out and had only just started to hit the market.

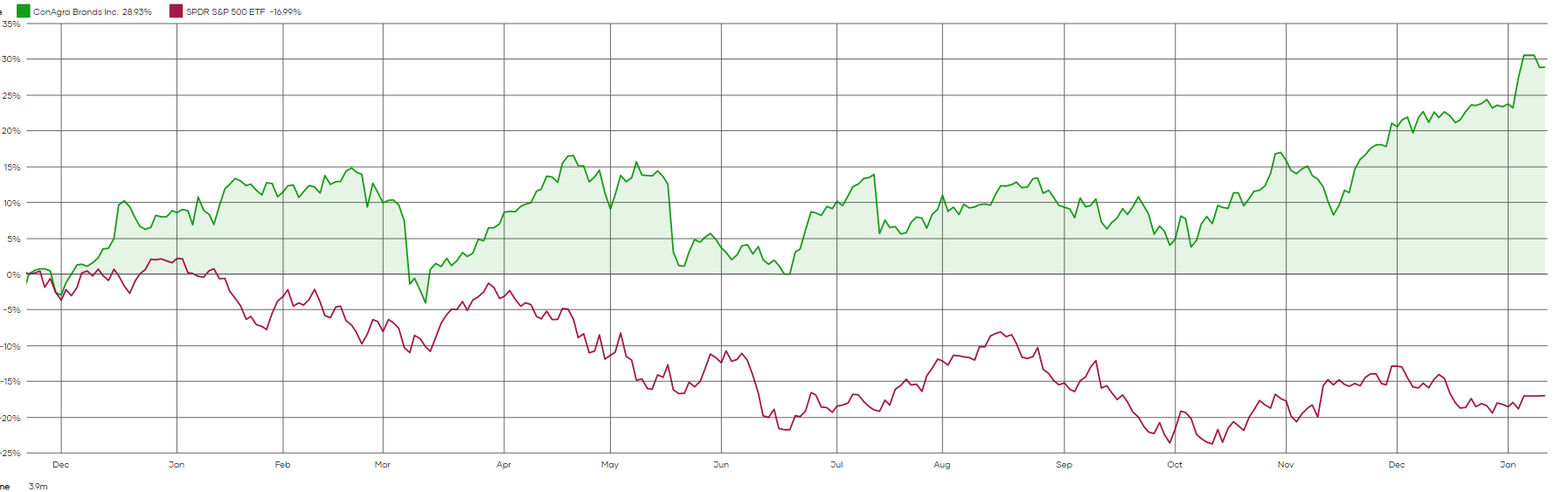

Since then the stock has returned 29% while the S&P 500 lost 17% of its value.

CAG vs SPY (Dividend Freedom Tribe)

Yet, the stock is still just getting going.

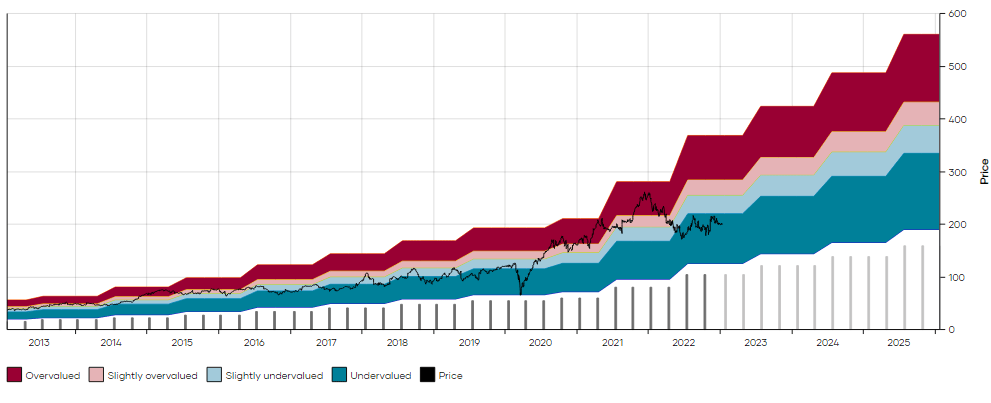

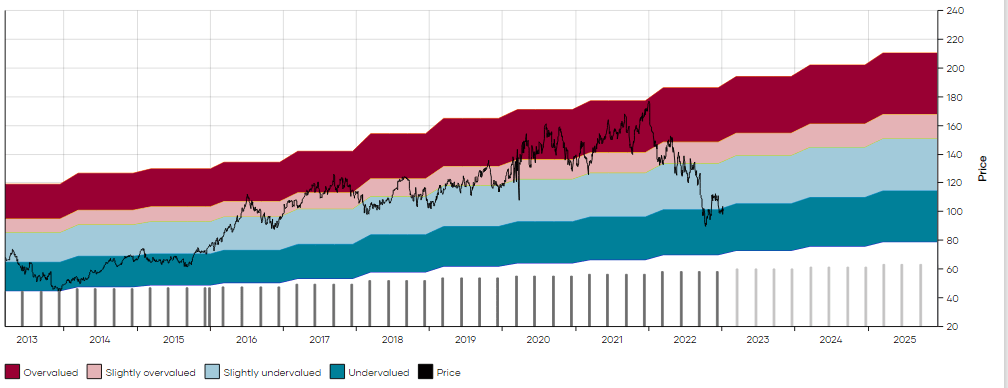

CAG MAD Chart (Dividend Freedom Tribe)

You see, it currently yields 3.25%, but if this last bout of momentum has legs, CAG could go up another 20% to 30%. The key for this will be to break out of $41, which would be a new all-time high, at a very fair valuation.

Here we could possibly be seeing a momentum & value play happen at the same time which could be a perfect pick for a conservative set of investors seeking to profit from future bullishness.

$40 is the price we recommend buying at or under, which means that it is still not too late to get in.

Digital Realty (DLR)

In November, while Digital Realty’s price was still slumping, I made the case for the stock as an investment to the Dividend Freedom Tribe.

I explained that Digital Realty had long been a company of interest due to its well management, industry tailwinds, and history of increasing dividends. However, its high valuation kept it from being considered for our investment portfolios.

Despite a decade of 5% per annum dividend growth, the company’s yield during this period of overvaluation was between 2.7% and 3.25%.

To make the company a worthwhile investment, either the future dividend growth rate would need to increase to 9-10%, or the price would need to decrease so that the dividend yield would be above 4%.

This year, the latter happened as DLR’s stock price dropped deep double digits from its late December highs.

DLR currently pays out about 72% of its FFO, leaving room for them to maintain their 5% dividend increase rate.

We warned that because the stock was dropping it still had quite a bit of downside.

That is no longer true, as the stock has dropped more, and entered bargain territory.

At $100, DLR yields 4.9%, which nearly guarantees attractive returns going forward.

DLR MAD Chart (Dividend Freedom Tribe)

Digital Realty has been rotating from a capital gains driven crowd to an income driven crowd. Picking up now means being ready to profit when everything stabilizes.

DLR is a strong buy, and likely won’t be impacted much by cost inflation.

Conclusion

The glass can be half full or half empty, maybe slightly more full or more empty.

We’re looking for glasses that are 55% full, but which have been interpreted as 45% full and therefore discarded as half empty glasses.

This is on the fringe, where consensus logic can fail and create opportunity.

Buying these sort of stocks gives us a great business, with a great valuation, and a great stream of income, something which just cannot be ignored.

Be the first to comment