Spencer Platt

The Upcoming Recession

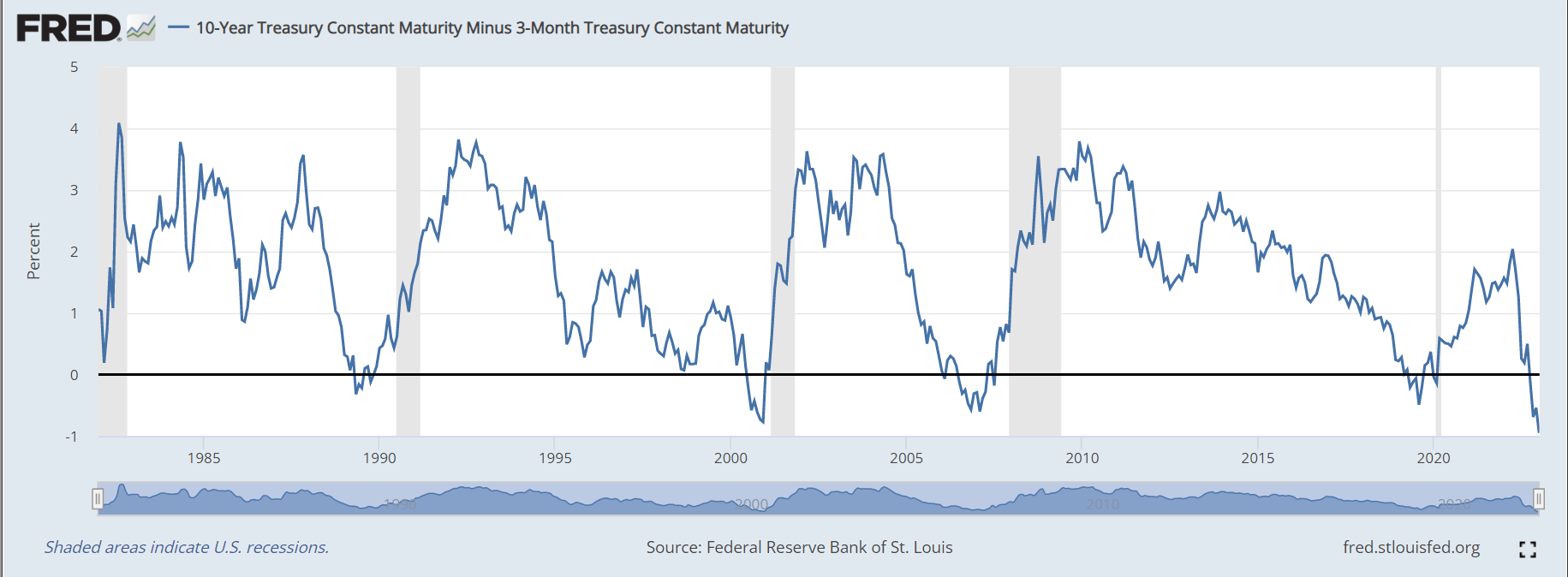

The recession is coming. Historically the inversion of the spread between the 10Y Treasury Bond and the 3M Treasury Bill has been a reliable recession indicator as the 10T-3M spreads inverted before each past recession. In fact, the NY Fed specifically uses the 10Y-3M spread to estimate the recession probability.

Currently, the 10Y-3M spread is nearly 1% inverted, based on the chart below, which is the record inversion. This translates into a virtually guaranteed recession.

FRED

The NY Fed FAQ section explains in detail all relevant information regarding the yield curve spread as a leading indicator.

What’s causing the likely recession?

This will be the Fed-induced recession. After misreading the post-pandemic inflation as transitory, the Fed rushed to increase the interest rates in 2022, which pushed the short-term interest rates well above the long-term interest rates and inverted the yield curve.

The Fed Chair Powell stated in his speech at the Brookings Institute on Nov. 30 that the most worrisome part of inflation is the service inflation, which is caused by the rising wages, which is turn is based on the historical imbalance in the labor market.

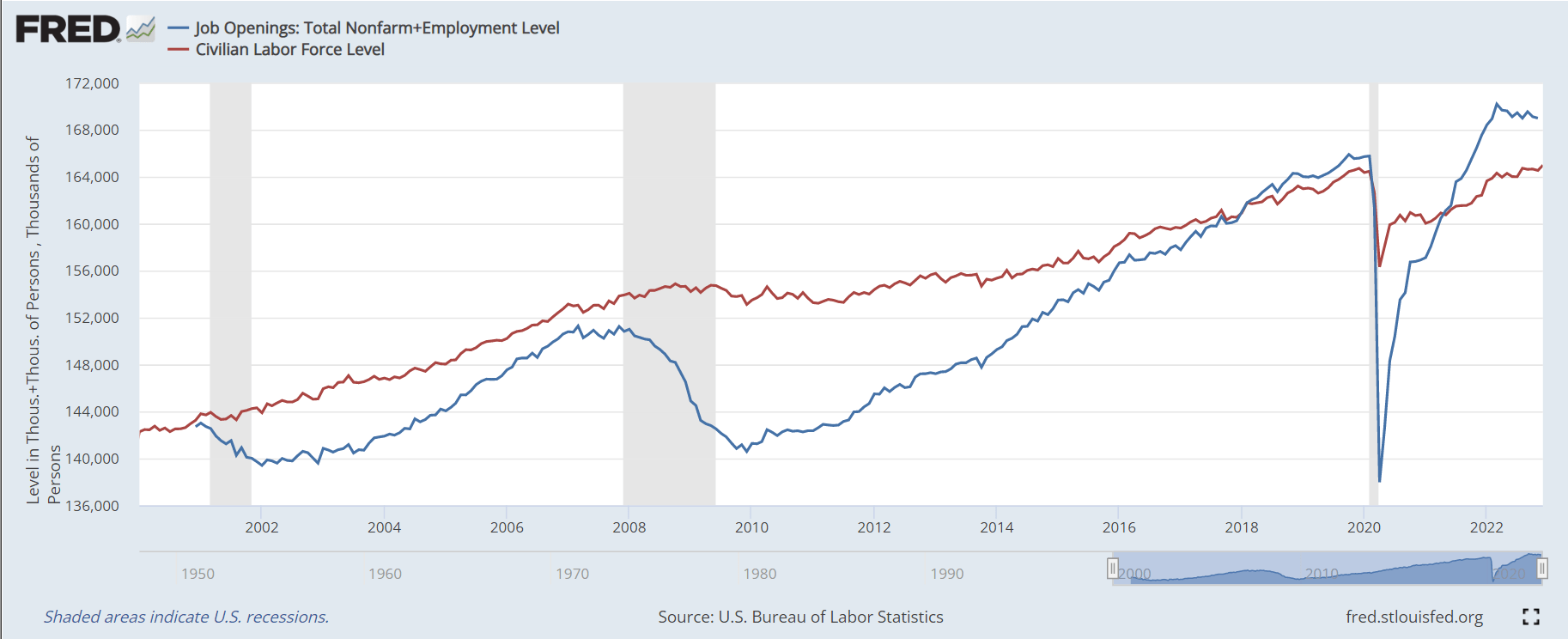

Specifically, the Fed Powell mentions the jobs-worker gap as the key variable behind the service inflation. Here’s the chart. I added the total Job Openings Nonfarm and the Employment level variables and plotted against the Labor Force (to replicate the chart Powell used).

FRED

The chart above shows clearly the civilian US labor force is currently at around 165 million. However, there are abound 159 million people employed with additional 10 million job openings which rounds up to nearly 170 million in total, around 5 million jobs in excess on the labor force.

This situation is clearly unsustainable as it will likely cause elevated wage growth as the demand for labor greatly exceeds the supply for labor. Thus, the Fed made is clear that the objective is to increase the unemployment rate from current 3.5% to 4.4%.

Note, even with this objective only 1-1.5 million jobs would be lost. Thus, the expectations are that the slowing demand for labor would be reflected mostly via the decrease in jobs openings, since the total demand for labor needs to drop by more than 5 million jobs.

But this is a questionable assumption, given that about 4 million of jobs openings are in health and education, which are unlikely to be affected by a recession. Thus, the unemployment rate is likely to have to rise toward the 5% level to solve the imbalance in the labor market – and that’s the recession.

The December payroll report

Thus, the countdown to a recession starts with every employment report. The December 2022 employment report shows that the unemployment rate actually decreased to 3.5% from 3.6%. Further, 233K new jobs were created.

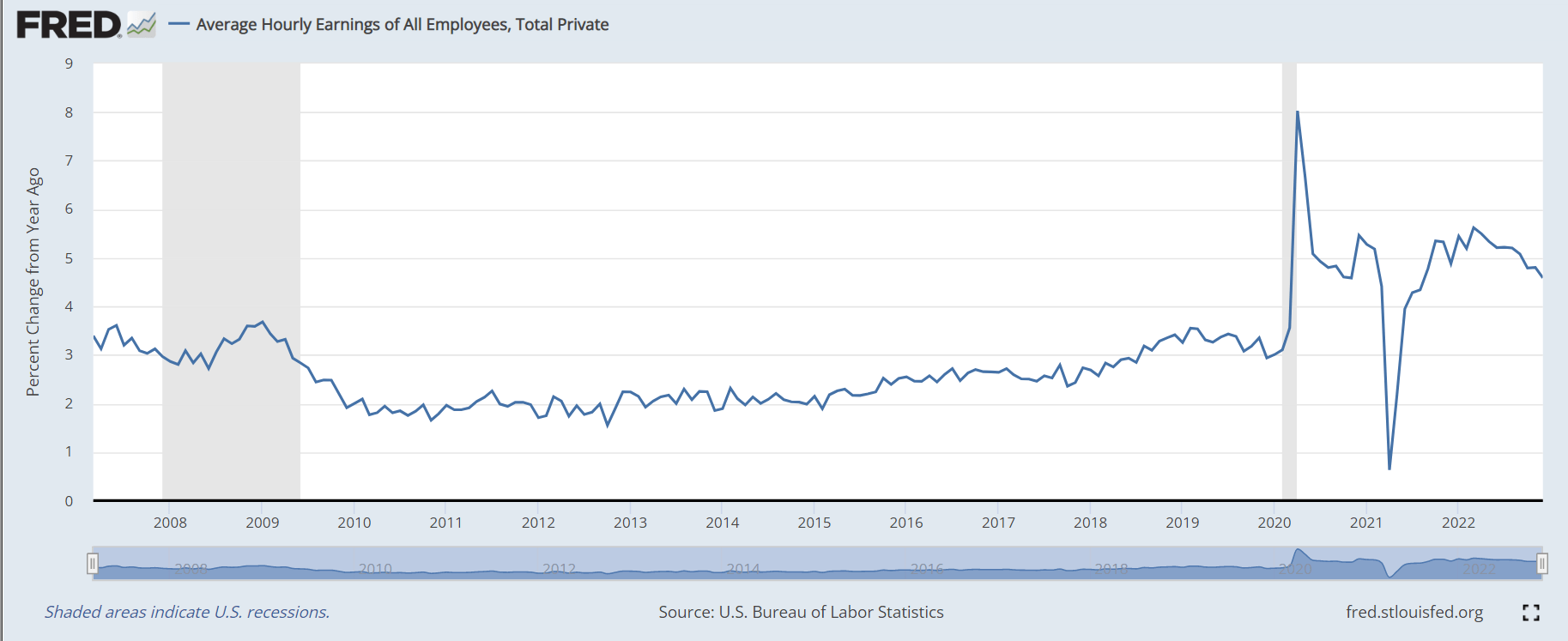

Obviously, the labor market is still strong, and the numbers are going against the Fed’s objectives. On the positive side, the wage growth has slowed to 4.6%. But historically this is still very high. Here’s the chart of average hourly wage growth, we are still well above the 2-3% target.

FRED

The expectations that the wage growth will slow down without solving the jobs-worker gap is irrational.

However, if the labor participation rate sharply increases, the labor market imbalance could be solved by increasing the labor supply. The December labor report shows that the labor participation rate increased slightly to 62.3% from 62.2%.

The supple-side solution to the labor market is unlikely due to 1) demographics (many retired prematurely during covid and are unlikely to return), and 2), immigration restrictions, which are unlikely to be changed anytime soon.

Thus, the Fed has no choice but to continue with its efforts to restore the job market imbalance – which means causing the recession.

The market implications

The S&P 500 (SPY) had a strong positive response to the December payroll report, up almost 3% on the day, focusing on the slower wage growth as the signal that the labor market imbalance is unlikely to cause the wage-price spiral. The move in the stock market is supported by the sharp fall in interest rates and a weaker US dollar, all suggesting a more dovish Fed.

Specifically, the market now views that the Fed will hike to 4.95% by July 2023, and then cut by 25bpt by November 2023, and continue cutting down to 3.17% by December 2024.

These expectations are very different from what the Fed signaled it will do. The Fed clearly stated that it plans to increase interest rates to 5.1% and hold at this level for the entire 2023 – with the clear goal to solve that labor market imbalance with the increase in the unemployment rate to 4.4%.

Thus, in my opinion, the SPY reaction to the slowing wage growth is not fundamentally justified.

We’re still in a bear market, and the sharp daily rallies in response to any data point are to be expected in a bear market.

The countdown to a recession is in fact the countdown to the buyable market bottom. Once we get the increase in the unemployment rate and the obvious signs of a recession, the Fed’s objective will be reached, which will be the next opportunity to buy for a longer term.

Currently, the S&P 500 (SPY) is still overvalued at the PE ratio well above 20, facing the recession, with a significant downgrade in earnings and valuation contraction. Thus, my recommendation is still a Sell.

The premature Fed pivot seems to be the major bullish counter thesis. This is possibly based on the 2018/2019 experience, when the demand for labor slightly exceeded the supply of labor, and the Powell’s Fed attempted to sharply hike interest rates, but quickly pivoted and lowered the interest rates.

However, during that period, the jobs-worker gap was much smaller, the wage growth reached only 3.5% at the highest point, and most importantly, the former President Trump was heavily “lobbying” for the dovish monetary policy.

Don’t expect a premature Fed pivot at this time. Rather, let’s focus on the recession countdown, which still seems to be delayed based on the December payroll report.

Be the first to comment