tortoon

Written by Sam Kovacs.

Introduction

In August, I presented the case for secular tailwinds to propel the semiconductor industry forward in the coming decade.

You can read the whole article, but the short version is:

The semiconductor industry is expected to be worth $1 trillion by 2030, according to McKinsey, thanks to its growth at a rate of 6-8% per year.

The industry has a history of cyclicality, due to factors such as inventory buildup and fluctuations in worldwide economic growth.

In the past, this has led to periods of strong growth followed by downturns, but the industry has consistently recovered and experienced growth over the long term.

The pandemic has had a significant impact on the industry, with both increased demand and decreased supply due to supply chain constraints and stay-at-home trends.

Despite this, the industry is expected to continue growing in the coming years, with the potential for strong returns for investors.

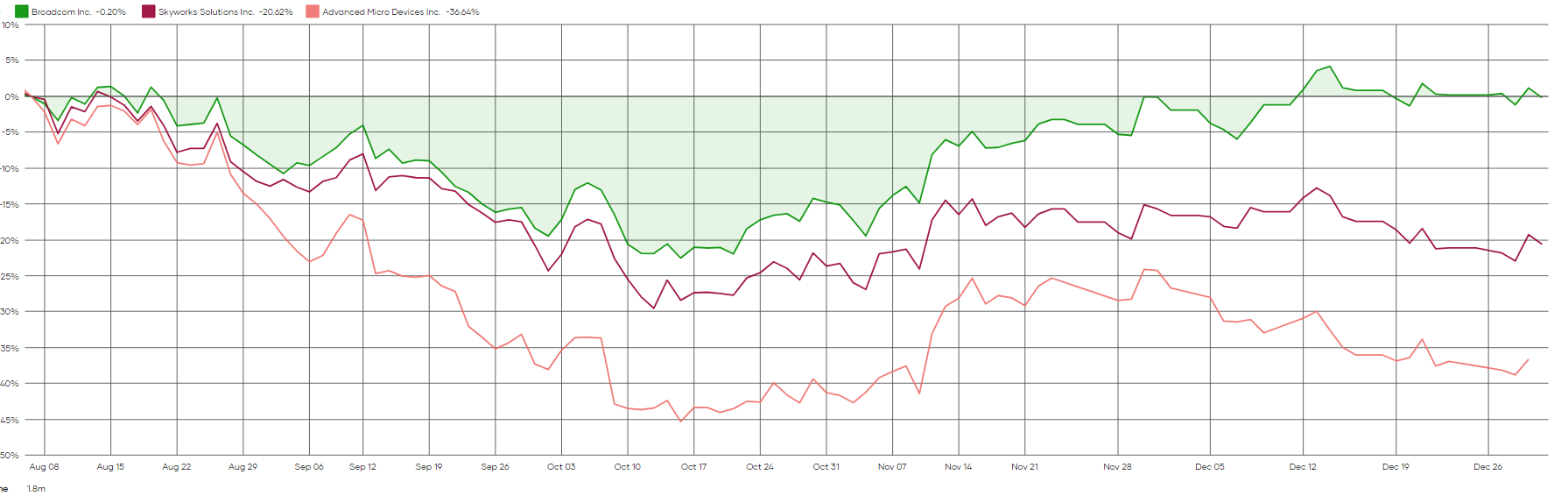

In the article, I made 3 suggestions: Buy Broadcom Inc. (AVGO), Buy Skyworks Solutions, Inc. (SWKS), Sell Advanced Micro Devices (AMD).

AVGO,SWKS,AMD (Dividend Freedom Tribe)

Since then, AMD is down 36%, SWKS is down 20%, and AVGO is flat.

For reference, over the same period, the S&P 500 Index (SP500) was down 8%.

Clearly, being invested in AVGO was a better proposition that the other two picks.

The losses on SWKS in the Dividend Freedom Tribe’s model portfolios was mitigated, as we had a reduced position relative to our AVGO exposure.

Broadcom: A phenomenally undervalued pick

Word on the street is that the rally Semiconductor stocks witnessed between October and December was premature because of likely “continued fundamental deterioration”. Deutsche Bank analyst Ross Seymore said that fundamentals for the semiconductor industry “largely held in better than expected,” as revenues for companies were up 14% in 2022

Following the feds 14th of December rate hike, Broadcom stayed flat, while Qualcomm (QCOM), Intel (INTC), AMD, and Nvidia (NVDA) all fell.

Why is Broadcom holding up better?

In August, I made the case that Broadcom was “the recession-proof pick” because it is exposed to industries with secular demand tailwinds, making it less cyclical than consumer facing AMD or INTC.

We projected 12% dividend growth, and this is exactly what Broadcom delivered.

When they reported earnings, it became clear that the company was doing extremely well and even projecting continued semiconductor revenue growth of 20%+ next year.

- Broadcom’s consolidated revenue for fiscal year 2022 was $33.2 billion, a 21% increase year-on-year

- Operating profit for the year grew 28% year-on-year, and free cash flow per share increased 25% year-on-year

- For the fourth quarter, consolidated net revenue was a record $8.9 billion, up 21% year-on-year, with semiconductor solutions revenue increasing 26% year-on-year to $7.1 billion and infrastructure software revenue growing 4% year-on-year to $1.8 billion

- In the fourth quarter, the semiconductor business performed well in hyperscale, service providers, and enterprise, and wireless grew sequentially as the company ramped up a new platform and a North American customer

- In the first quarter, the company expects strong growth in networking, storage connectivity, and broadband, with semiconductor revenue growth expected to sustain at around 20% year-on-year

- In the fourth quarter, infrastructure software revenue of $1.8 billion grew 4% year-on-year, and the company expects this growth to continue in the first quarter

- Electric cars need much more chips than cars with combustion engines.

- Factories will need many more chips as they automate.

- Cloud computing will also require a significant number of chips.

- Of course, the consumer segment is also set to grow. IoT and all those trends will lead to more chips in the household than we ever imagined.

- Having multiple dominating verticals will lead to less cyclicality and secular growth for the next decade or two.

It is, therefore, clear that the market is off the mark because of worries about a short term cyclical downturn in the sector.

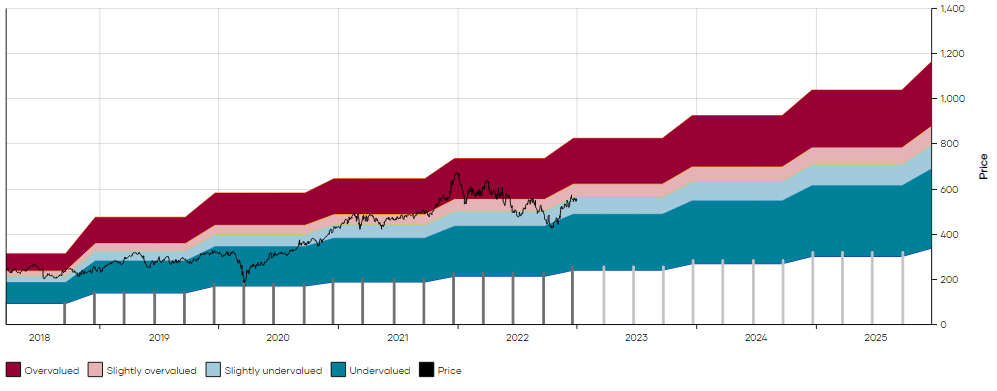

At the current price of $550, AVGO yields 3.34%, just above its 5 year median yield of 3.2%.

As you can see on the MAD Chart below (click here for more on MAD Charts), this makes AVGO more or less fairly valued at the current price.

AVGO 5y MAD Chart (Dividend Freedom Tribe)

But AVGO has in my opinion, always been held back in terms of valuation, which make it particularly interesting to a dividend investor.

My outlook remains for 12% dividend growth from AVGO in upcoming years. This should be achievable through continued growth in many of its verticals, all while maintaining free cash-flow payout ratios sub 50%.

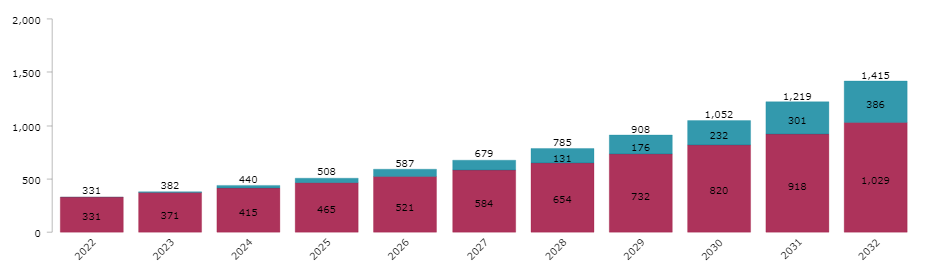

If you invest $10K today in AVGO, assuming dividend reinvestment and a constant 12% CAGR, then 10 years from now, you’ll receive annual income of $1,415. This equates to an annual yield of 14.15% on your original investment, which shows amazing potential.

AVGO Income simulation (Dividend Freedom Tribe)

We’ve been buying AVGO since 2020, and it remains an amazing opportunity, as the market hasn’t fully realized the stock’s long term potential.

Down the line, growth will align with capital appreciation. AVGO’s price should trend towards $800 over the next 3 years, with possible swings higher and lower on the way there.

I remain bullish and overweight AVGO going into 2023.

Intel: National Security depends on its success.

Government intervention can offer amazing opportunities for certain companies.

Intel has found itself in a brilliant position to become the premier chip foundry in the US, as the country has a strategic need to become self-sufficient when it comes to producing semiconductors.

The vast majority of high complexity chips are currently built in Taiwan, mostly by the Taiwan Semiconductor Manufacturing Company (TSM).

With Xi’s determination to bring Taiwan back into the Chinese fold as part of his legacy, the supply chain of semiconductors is one over-zealous decision away from being entirely compromised.

The CHIPS for America Act, also known as the Creating Helpful Incentives to Produce Semiconductors (CHIPS) for America Act, is a piece of legislation that aims to increase domestic production of semiconductors and other microelectronics in the United States.

It includes provisions such as $52.7 billion in subsidies over the next five years to boost U.S. chip production and a 25% investment tax credit for chip plants worth an estimated $24 billion over the next decade.

Currently, the U.S. produces only about 10% of the world’s supply of semiconductors, while East Asia accounts for 75% of global production.

The legislation aims to rebuild America’s capabilities in chip production and address shortages of semiconductor chips, which have caused supply chain disruptions for automakers and producers of appliances and other devices.

Intel is expected to be a major beneficiary of the CHIPS Act, with estimates of $10 billion to $15 billion worth of U.S. government subsidies over the next five years.

The company is receiving over a quarter of the subsidies to build its chip fabs.

A theme which has legs for the next decade is de-globalization. It has become obvious to all that we are gravitating to a multipolar world, and failing to price geopolitical risk in business endeavors is no longer an option.

Self-sufficiency is going to be an extremely important topic going forward. The U.S. is self-sufficient when it comes to its food supply and energy supply. But when it comes to its infrastructure, especially digital infrastructure, it is still overly dependent on other countries.

This is going to have to change, as semiconductors are an essential part of the economy.

The case for Intel becoming America’s premier foundry is quite compelling at this point.

Especially given that the market has all but given up on INTC at this point.

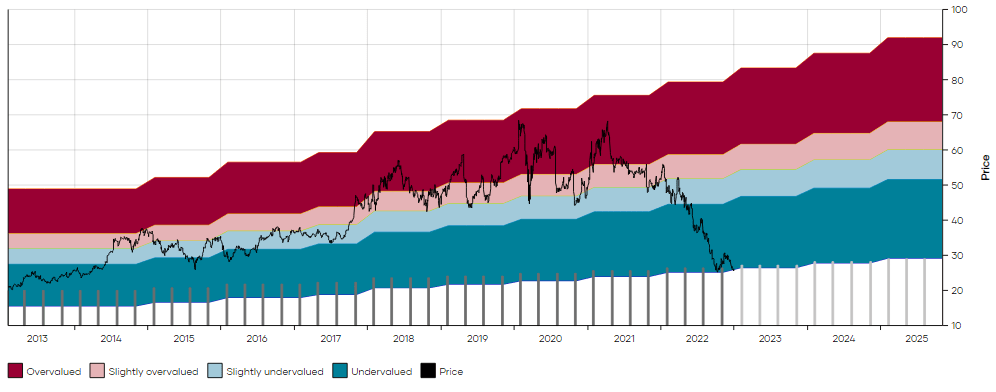

The stock now yields 5.6%.

INTC MAD Chart (Dividend Freedom Tribe)

With this current yield, investors shouldn’t expect any dividend growth for upcoming years, as management has hinted that there is no case for increasing the dividend but that they do not intend on cutting it either.

They view it as important to provide investors with a yield while the company is undergoing a transition and might not provide the best capital returns.

This is very sensible, and frankly if INTC stayed at this yield, they could keep their dividend flat for the next 10 years, and you’d still get amazing income.

If you invest $10K today and reinvest dividends, assuming a 5.6% yield and flat dividends, then in year 10 you’ll receive $1,075 of annual income, or 10% of your original investment. Pretty good!

INTC Income Simulation (Dividend Freedom Tribe)

What’s more is that it is very likely that within 3 years or so, we’ll start to see some results come through and the dividend be raised again.

A great deep value play, while the market is extremely concentrated on the reducing consumer demand and lost market share to AMD.

Everyone will look back in a few years and think that it was obvious that INTC would bounce back.

Get in now, and get paid to wait.

Conclusion

The semiconductor sector is set to grow. It’s a lot easier for stocks to do well in industries that have long-term tail winds. Especially when you can get them at bargain prices, and watch your dividends compound as you wait for the market to notice.

Be the first to comment