JJ Gouin/iStock via Getty Images

Intro

We wrote about FutureFuel Corp. (NYSE:FF) (Chemicals & Bio-Based Fuel Outfit) back in late July when we stated that the company’s margins were beginning to come under pressure. Inflationary cycles really bring margins into the spotlight as increasing sales are often not enough to keep margins from eroding due to rising costs. As we stated in that July article, the gross margin had slipped below 9% and the modest gross profit figure of $1 million in the second quarter on sales of $117.8 million means FutureFuel’s trailing 12-month gross margin percentage now comes in at a lower 7.69%.

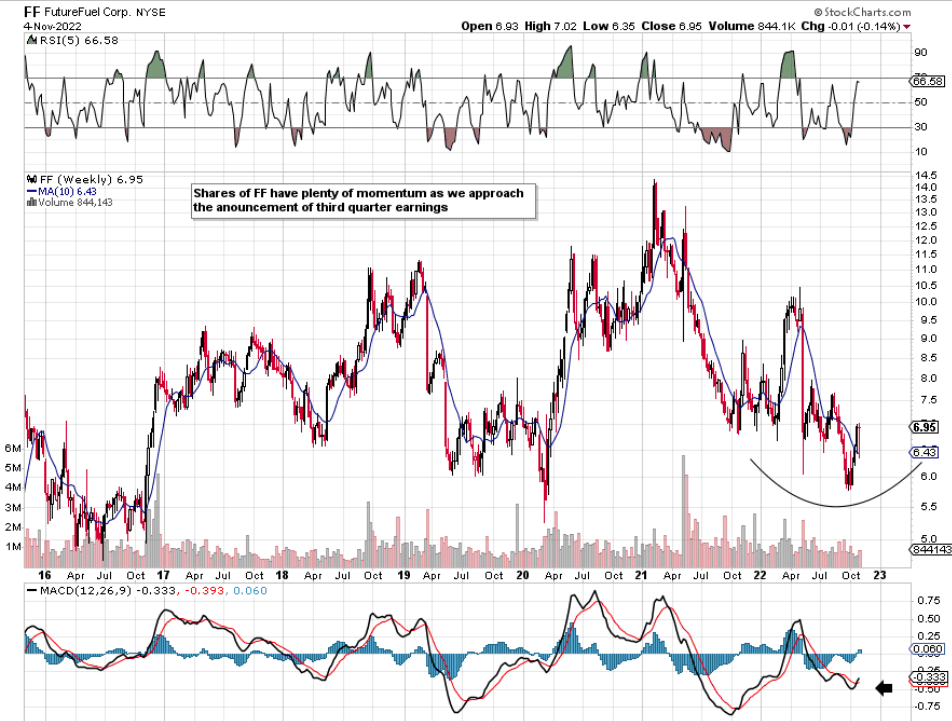

From a technical standpoint, we see below that shares managed to bounce off support just below the $6 level in late September and really rallied well in October. Given the stock’s recent momentum, the fact that the MACD is still in oversold territory, and the generous 3.45% dividend yield, investors may like this play from the long side as we approach the company’s third-quarter earnings print (November 9th). Although FutureFuel reported a net loss of $3.1 million in Q2 (due to the higher costs alluded to earlier), it did manage to report an adjusted EBITDA of +$18.7 million which is probably a more accurate way of determining profitability. Furthermore, the biodiesel segment is expected to bounce back in the latter part of the year plus the fundamentals remain bright in the Chemicals segment, especially in the pharmaceutical intermediates space.

Suffice it to say, more capital gains in the share price along with growth in the dividend would be exactly what the doctor ordered for the bulls at this stage. The special dividend of $2.50 per share last year will be fresh in the memory and demonstrated loyalty from management to shareholders, especially given how poorly the share price performed in fiscal 2021. However, getting a read on how strong the dividend actually is remains difficult due to the lack of forward-looking guidance in this play. Therefore, let’s go through FutureFuel’s associated dividend trends to see if more sustained growth is on the way in the payout.

FutureFuel Technical Chart (Stockcharts.com)

Payout Ratio

Despite the Q2 negative earnings print, we must remember that it is cash that pays earnings and not bottom-line profits. Management recently reiterated the quarterly dividend payout of $0.06 per share, stating that it expected to pay the dividend in Q3 as well as Q4. Despite the recent headwinds regarding earnings, FF still managed to generate $44.5 million in operating cash flow over the past four quarters. Since Capex investment only amounted to $2.9 million in this period, there was ample free cash flow to fund the $10.5 million of dividend payments over the past 12 months. FutureFuel’s free-cash-flow payout ratio now comes in at 25.2% which is below the company’s 30.6% average over the past five years.

Balance Sheet

Payout ratios though can be manipulated as cash flow can be generated through a myriad of ways (taking on debt, selling assets, working capital changes, etc.). At the end of Q2, FF reported almost $169 million of cash and short-term investments on its balance sheet. This means shares currently trade for less than two times their cash position which is a big calling card here. Why? Because even if cash flow or EBITDA figures disappoint in upcoming quarters by some margin, the company’s war chest of cash means the dividend, if not another special dividend, is easily affordable from a cash standpoint. In saying this, shareholder equity stooped to just over $262 million at the end of Q2 which is the lowest book value number we have seen in quite some time in FF. Declining book value is a problem when growth is not there to meet it. FutureFuel’s net profit for example over the past 12 months comes in at approximately +$16 million which again is a very low number compared to historical 12-month tallies.

Value

FutureFuel’s ability to generate cash flow and lack of interest-bearing debt (total debt to equity of 0.19%) means the company should be able to withstand any potential near-term headwinds in its divisions. As we can see below, FutureFuel’s valuation still looks compelling compared to yesteryear. Sales are cheap, the company is still profitable from an earnings standpoint over the past 4 quarters, and the company’s assets (despite declining in value) continue to trade below historic multiples.

| Metric | Trailing 12-Month Multiple | 5-Year Average Multiple |

| Price To Earnings (GAAP) | 18.96 | 18.04 |

| Price To Book | 1.16 | 1.44 |

| Price To Sales | 0.83 | 2.12 |

| Price To Cash Flow | 6.83 | 11.09 |

Conclusion

Although net profit can be volatile in companies such as FutureFuel, the company remains profitable and continues to generate meaningful cash flow. Management pointed to an upturn in the biodiesel segment in Q3 & Q4 which the market may be pricing in already. The dividend remains well covered buoyed by a sizable amount of cash on the balance sheet. Let’s see what Q3 numbers bring. We look forward to continued coverage.

Be the first to comment