bymuratdeniz/iStock via Getty Images

TG Therapeutics (NASDAQ:TGTX) CEO Mike Weiss made a good impression at the J.P. Morgan Healthcare Conference this week. The company started the presentation day with an initially poorly received in-licensing announcement of an allogeneic CAR T cell therapy from Precision BioSciences (DTIL). This was not the update investors and traders were waiting for, however. Weiss made us wait for the actual presentation, where he shared Briumvi’s net sales for the fourth quarter and revenue guidance for 2024 that was slightly ahead of the Street consensus at the mid-point.

Importantly, Weiss revealed plans for the start of human trials for the subcutaneous version of Briumvi, which is the important next step to improve the product’s convenience and competitive profile versus Ocrevus and Kesimpta.

Azer-cel deal with Precision BioSciences

CAR T cell therapy is becoming increasingly important in oncology, but it recently started finding its way to autoimmune indications with some companies pivoting from oncology to immunology. The theory is that CAR T cell therapy treatment could reset the immune system and significantly improve the lives of patients suffering from certain autoimmune diseases. There are early, but promising, results with this approach.

Treatment with anti-CD19 autologous CAR T cells resulted in remission of all five systemic lupus erythematosus (“SLE”) patients, as reported in Nature in November 2022.

Last month at ASH, additional data were presented with 12 SLE patients receiving CD19/BCMA CAR-T cells with the SLEDAI-2K score decreasing in all patients, from a mean of 18.3 to 1.5, and all patients met the LLDAS criteria and were able to discontinue SLE-related medications, including glucocorticoids.

TG in-licensed azer-cel from Precision BioSciences for the treatment of autoimmune diseases and indications outside of cancer. The upfront payment is $7.5 million, consisting of cash and 2.9 million shares of Precision common stock at $0.77 per share, and Precision will receive $2.5 million within 12 months as an equity investment and another $7.5 million in cash and common stock upon the achievement of certain milestones. Precision is eligible to receive up to $288 million in additional milestone payments and high-single-digit to low-double-digit royalties on net sales.

This is a very low financial risk and high reward in-licensing for TG. The clinical risk is very high as there is very little data on CAR T cells in autoimmune diseases and no data on azer-cel. The field is getting increasingly crowded with many companies switching their programs from oncology to autoimmune diseases, and it also remains to be seen whether an allogeneic (off-the-shelf) approach TG has in-licensed can be equal to or better than the autologous approach where cells are taken from a patient, processed outside of the body, and reintroduced.

Briumvi exceeded expectations in Q4 with some inventory benefit, 2024 revenue guidance is slightly better than consensus at the mid-point

TG expects to report $40 million in Briumvi net sales for the fourth quarter. This was better than the $33-37 million guidance range, the $38.6 million consensus, and my $37-39 million range. I noted in the earnings preview article to our Investing Group subscribers that it is possible we see some inventory benefit in the quarter, and that did happen – CEO Weiss said there was an inventory benefit of a few million as wholesalers increased days on hand at the end of December. This suggests actual demand was around the high end of the company’s guidance range or slightly above it, which is still a pretty good result after $25.1 million in the previous quarter.

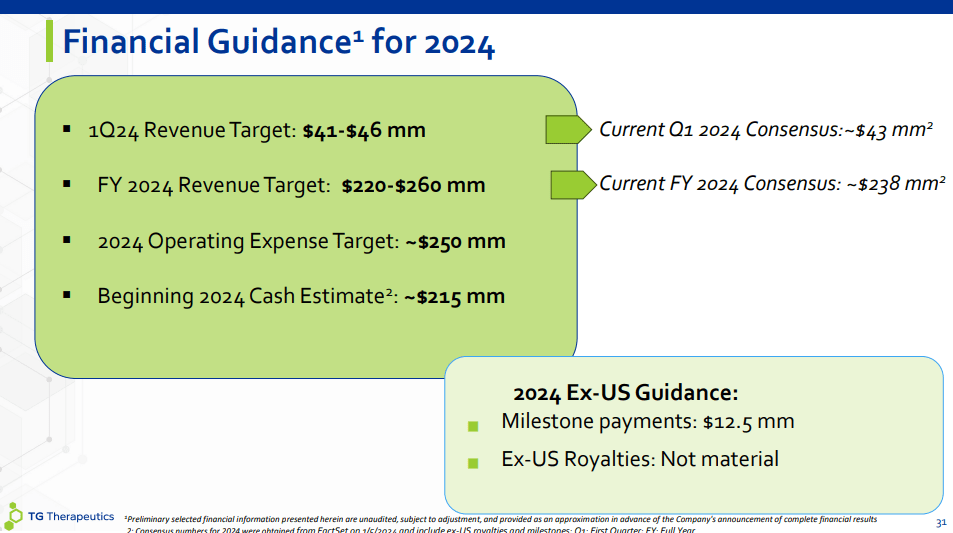

For the first quarter, the guidance range is $41-46 million and is largely in line with the Street consensus of $43.4 million. Q1 is the seasonally weakest quarter of the year for most pharmaceutical products, and Briumvi is no exception – insurance resets at the start of the year, expected higher co-pay assistance leading to higher discounts and lower net price, and the inventory benefit from Q4 turns into a headwind of a few million as wholesalers are likely to reduce days on hand.

All this suggests underlying growth should be good and that Briumvi will generate much stronger sequential growth in the second quarter.

For the full year, TG provided a relatively wide revenue guidance range of $220-260 million, the mid-point being slightly ahead of the $238 million consensus. This was not unexpected, and I thought the company would not significantly deviate from the consensus and management likely left some room for outperformance.

TG Therapeutics investor presentation

Patient start forms improved sequentially, from 900 in Q3 to 1,000 in Q4. As a reminder, this number only includes patients going through TG’s hub and there are between 10% and 20% of additional patients being prescribed Briumvi outside of the hub.

There are several tailwinds for Briumvi in 2024:

- More patients returning for the third infusion. The six-month window between the second and third infusion meant we only saw patients starting to return for the third infusion in greater numbers in the fourth quarter.

- Physicians becoming more experienced with Briumvi and its efficacy and safety profile. Many slow adopters prescribe Briumvi to one or a few patients to see how they are doing before expanding their use. And given the six-month window between infusions, this takes more time than for frequently administered drugs.

- Improved coverage, the permanent J-code, and the increasing number of institutions putting Briumvi on their formularies.

- The company expects to focus more on patient awareness with direct-to-consumer advertising. This should lead to more patients coming to physicians’ offices to ask for Briumvi.

I expect 2024 to be a strong year for Briumvi, with net sales coming at the high end of the company’s $220-260 million guidance range and possibly above it, and the company exiting the year with an annualized net sales run rate of more than $350 million and potentially close to $400 million.

With an expected expense base of around $250 million in 2024, this suggests significant operating leverage with the company reaching positive cash flow and becoming profitable before the end of the year.

Partner Neuraxpharm will soon launch Briumvi in Europe, which will trigger a $12.5 million milestone payment. However, Weiss said royalties this year will not be material, as it will take time for Neuraxpharm to secure access and reimbursement on a country-by-country basis.

TG is actively working on improved convenience of Briumvi, looking into indication expansion

TG is conducting a trial to show the feasibility of patients switching from Ocrevus and taking a one-year infusion instead of the initial four-hour one. The preliminary data were reported recently and show good tolerability with no issues. This bodes well for demand that will come from patients that want to switch from Ocrevus and Kesimpta.

TG Therapeutics ECTRIMS presentation, November 2023

The more important part is the development of the subcutaneous version of Briumvi. The company now expects to start a human bioequivalence clinical trial in mid-2024. Having a subcutaneous version should help TG compete with Ocrevus, as it will soon have a subcutaneous version on the market and against Kesimpta which is only used as a subcutaneous injection. It could also address the bear thesis of Briumvi being the only CD20 product that does not have a subcutaneous version.

Last, but not least, the company is planning indication expansion for Briumvi into other autoimmune diseases, although I am not sure where TG wants to take Briumvi, as neither Roche (OTCQX:RHHBY) nor Novartis (NVS) are actively developing Ocrevus and Kesimpta outside of multiple sclerosis.

Conclusion

TG Therapeutics reported strong Q4 net sales of Briumvi and provided Q1 2024 and full-year 2024 revenue guidance that did not disappoint. This puts the company in a strong position to increase shareholder value and become cash flow positive and profitable before the end of the year, and significantly profitable in 2025 and beyond. The active work on improved convenience of Briumvi could also add to the long-term upside, as could azer-cel in other autoimmune diseases, although azer-cel has much to prove. Fortunately, the financial commitments are modest, and while the clinical risk is high, the financial risk is low and with high potential reward if this candidate generates positive clinical data.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment