primeimages

Summary

I am recommending a hold rating for Dollar General Corp. (NYSE:DG), as I think the near-term performance is going to be weak given the deflationary pressure, higher mix of larger stores, and step-up in shrinking headwinds. That said, the positive turnaround in traffic is certainly positive, and I will continue to monitor the traffic trend.

Business model

DG has a simple and easy-to-understand business. It operates discount retail stores that seek to offer a wide range of product offerings, such as food, fashion, and daily necessities. In terms of revenue contribution, consumables account for about 80% of revenue, seasonal products for 11%, home products for 6%, and apparel for 3%. DG mainly serves the US population, with 19,488 stores across the nation as of 3Q23.

Financials/Valuation

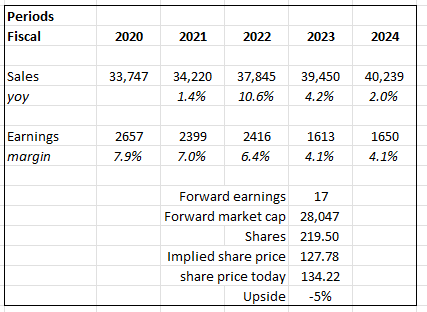

DG has been in the business for a very long time, and across the years, it has managed to scale its business to a massive revenue size of nearly $40 billion as of TTM 3Q23. Over the past 10 years, DG has shown nothing but positive topline growth. The business also has a strong balance sheet, as net debt to EBITDA (excluding operating leases) is generally under 2x. Most importantly, DG has generated positive free cash flow every single year over the past decade. As for the recent quarter’s performance, DG reported ~$9.7 billion in revenue, representing 2.4% growth. However, SSS decreased 1.3%, driven by a decline in ticket size, partially offset by an increase in traffic. By category, SSS declines were seen across all categories: home, seasonal, and apparel, except consumables. Gross margin came in at 29%, with the 147bps y/y decline primarily due to higher shrink, lower markups, and increased markdowns. Because of the fixed-cost nature of DG, the decline in gross margin had an asymmetrical impact on EBIT margin. In the quarter, the EBIT margin declined by 330bps to 4.5%. At the bottom line, 3Q EPS saw $1.26, beating the consensus estimate, but is a big drop from 3Q22’s $2.33 EPS.

Based on author’s own math

Based on my view of the business, DG is going to see a slowdown in growth in FY24, and margin is unlikely to improve given that incremental shrink headwinds are going to negate the positive impacts of SKU optimization. My model FY23 estimates follow management’s guidance, and I expect growth to further moderate in FY24. As for earnings, I expect FY24 margins to come in at the same guided margin as FY23, 4.1%. In terms of my valuation expectation, I believe DG will continue to track at a discount to peers like Five Below, Dollarama, and Dollar Tree, who are trading at 19 to 29x forward earnings. DG deserves to trade at a discount because of its weak growth outlook for both the top and bottom lines. Take, for example, Dollar Tree (DLTR), which is trading at 19x forward PE, which is expected by consensus to grow at mid-single digits for the next 2 years and earnings to grow even faster (30% in year 1 and 17% in year 2). This contrasts deeply with DG, for which I expect both revenue and net income to grow in the low single digits.

Comments

DG has finally shown some signs of turnaround-traffic has turned positive-but I think there is still a lot to be done before it can convince investors that the business has turned for the better. As I noted above, DG reported a 3Q SSS decline of 1.3%, driven by a decline in average ticket size. The silver lining here is that DG reported an increase in customer traffic. This is important as DG has reported three consecutive quarters of traffic decline, and more importantly, there was sequential improvement across traffic each month of the quarter. On the positive end, this tells me that DG product offerings and price points are back to resonate with customers and that this might be the start of a DG turnaround. However, on the negative end, this also tells me that there is a sequential decline in ticket size. In addition, management has stated that it is still seeing strong pressure on spending from its core low-income customers and that it anticipates this trend to persist into 2024, especially in the discretionary spending categories. I would also point out that DG is going to lose the benefit of inflation that it has enjoyed over the past year as deflation is kicking in, which will further impact ticket sales. This deflationary headwind is also being cited by bigger players.

In the US, we may be managing through a period of deflation in the months to come. And while that would put more unit pressure on us, we welcome it because it’s better for our customers. Walmart 3Q24 earnings call

And while we’re happy to see inflation rates moderating this year, if you compare industry pricing in key categories back to 2020, food at home pricing for families has increased 25% overall, and in some areas up to 30%. Target 3Q23 earnings call

DG did not provide formal FY24 guidance; they guided to a store opening target for next year at 800, implying 4% growth. At a glance, this is not good news for investors to hear, as it represents a slowdown from the 990 stores opened in FY23. Even if we take a step back, DG has historically opened about 900 to 1050 stores each year over the past 5 years. Management’s strategic viewpoint is that they are going to focus on rural communities and larger formats (90%) that have greater productivity per square foot. While I acknowledge this seems to be a good strategy, my pushback is that it is going to take a longer duration to hit mature utilization rates (i.e., traffic coming into the store), and bigger units have more opening and occupancy costs that will surface immediately, weighing on near-term profit metrics.

Other aspects of the business are also not stacking up well against DG in the near term. Moreover, shrink headwinds continue to step up, accelerating in 3Q from the 1H23 run-rate of 100 bps. In my opinion, the pressure on gross margin has not ended yet due to three reasons:

- DG continues to execute on the previously identified $95 million worth of markdowns in 2H;

- DG’s inventory optimization initiative is still in the works.

- Management noted promotional activity has picked up across the industry in recent weeks, which I expect DG to follow through on in order to stay price competitive.

That said, inventory levels have certainly improved, which bodes well for longer-term growth. Management noted inventory reductions of 15% and 19% on a per-store basis. The positive implication from here is that DG is progressing well in optimizing its inventory and is likely to be in a better position when the cycle turns (i.e., when the macro backdrop turns positive).

All in all, I do give credit for the positive inflection in traffic, but there are just too many variables in business that will impact how it will perform in FY24. I expect DG to continue seeing near-term headwinds from deflation (ticket size will likely compress), a higher mix of larger store units, and an increase in shrink.

Risk & conclusion

As I am recommending a hold rating, the upside risk is that DG continues to see stronger-than-expected traffic growth that is outpacing the deflationary pressure. In addition, the duration for new, larger stores to ramp up might be shorter than I expected. All of these could drive faster sales growth, surprising consensus, and my estimates.

Overall, my recommendation for DG is a hold. Despite positive signs of traffic turnaround, I am expecting the business to see near-term weakness due to deflationary pressures, increased larger store presence, and growing shrink headwinds. Specifically, the strategic shift towards larger-format stores, while might yield long-term benefits, is likely to put additional pressure on near-term profitability as it takes a longer duration to reach mature utilization, and it also comes with higher opening and operating costs.

Be the first to comment