Vince Bucci/Getty Images Entertainment

Investment thesis: Not long ago, Tesla, Inc.’s (NASDAQ:TSLA) market cap was comparable in size to that of the next largest ten automakers combined. It was a valuation level that made very little logical sense from a fundamentals perspective. It suggested that expectations were for Tesla to eventually capture anywhere between a quarter and half of the global automaker industry’s revenues and profits.

It was never likely for Tesla to become that successful, therefore, some of the stock price highs we have seen just about a year ago were never going to be sustainable. A combination of factors, including some non-fundamental issues, such as a negative campaign against the Tesla brand triggered by Elon Musk’s Twitter takeover and his policy changes, helped to bring Tesla stock down to fundamentally reasonable levels. For the first time in arguably many years, TSLA may make sense for more conservative investors who are looking for a mature, well-established investment opportunity that makes sense as a long-term buy & hold.

An increasingly profitable, maturing growth stock

Given the poor performance of Tesla’s stock price in 2022, one would think that Tesla is a company on the verge of a cataclysmic negative event, one that could potentially endanger its very existence. In reality, nothing of the sort happened. It was just a fallback to reality, and when we take a look at reality, it is not all that bad.

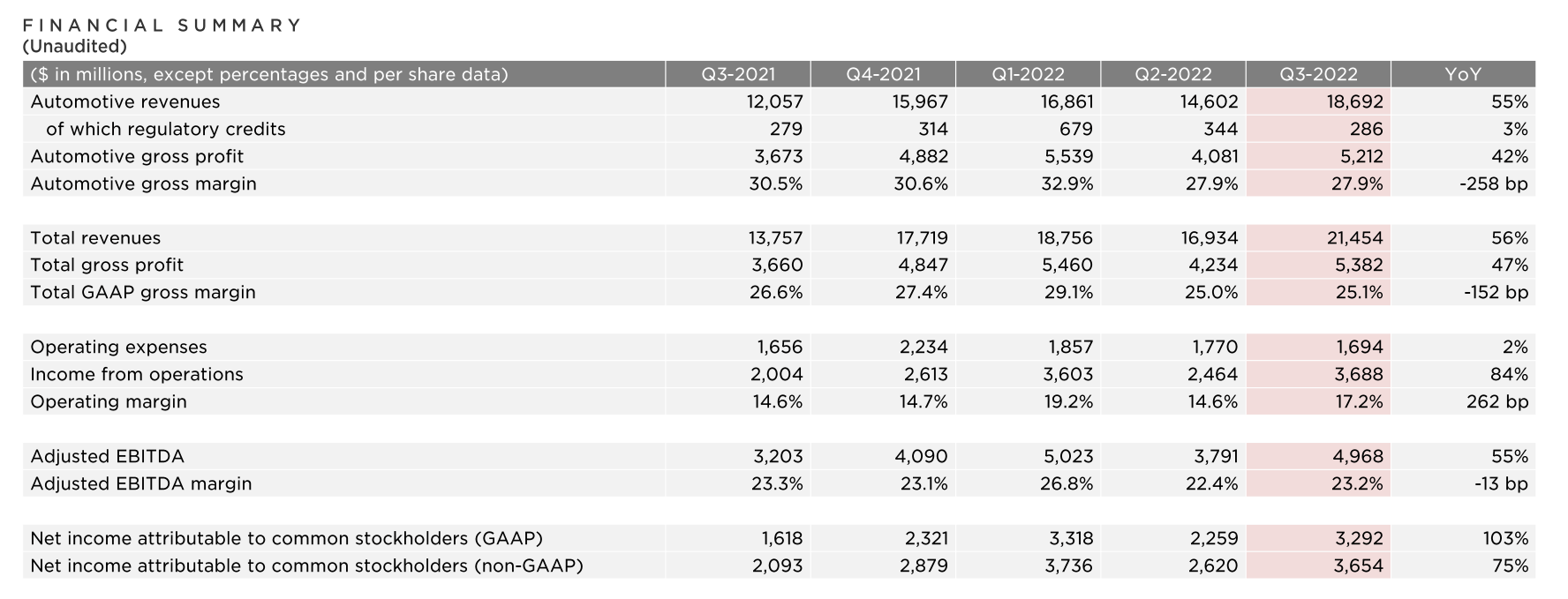

Tesla

As we can see, total revenues rose 56% y-o-y, which is quite impressive and, by most definitions, it still makes this a high-growth stock. I have no doubt that this pace of growth will slow going forward, but I don’t think that we are anywhere near the point where growth will stall. Net income doubled, meaning that profitability improved. The profit margin of $3.3 billion on revenues of $21.5 billion is a solid 15.3%. It should be noted that the latest news in regards to Tesla slashing prices suggests that the profit margin is set to shrink. We should not forget, however, to account for continued operating efficiency factors that can at least in part compensate for the lower sale price of its cars.

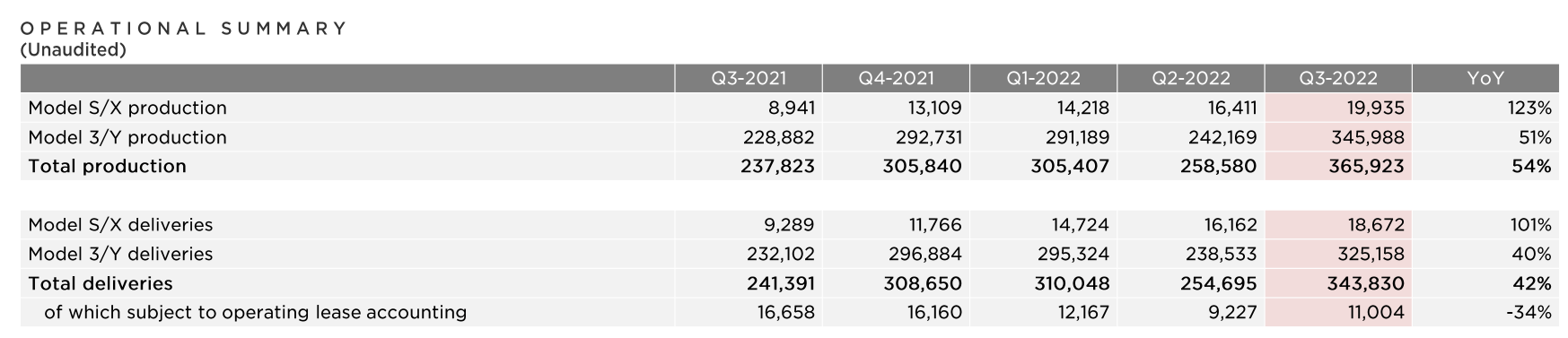

In terms of unit deliveries, I expect a significant slowdown going forward, but as of now, Q3 came in strong, with growth seen in most major markets.

Tesla

With a 42% increase in Tesla unit deliveries, it seems that demand is still going strong, which, as I will explain, can be prolonged by Tesla gaining in new markets that are currently marginal to its sales.

It should be noted that Tesla’s total debt, current & long-term, stands at $2.414 billion. For the same quarter in 2021, it was $6.7 billion, as reported in its Q-10 filings. The fact that debt is on the decline, even as the company continues to grow and it is proving to be profitable, suggests that even though Tesla will see much slower unit sales and revenue growth going forward, profit margins are likely to follow a path of further improvement, not factoring in the net effect of the sale price declines we are seeing, which should continue to help it to catch up to that P/E ratio that still has it trading far above its peers by this expense ratio measure.

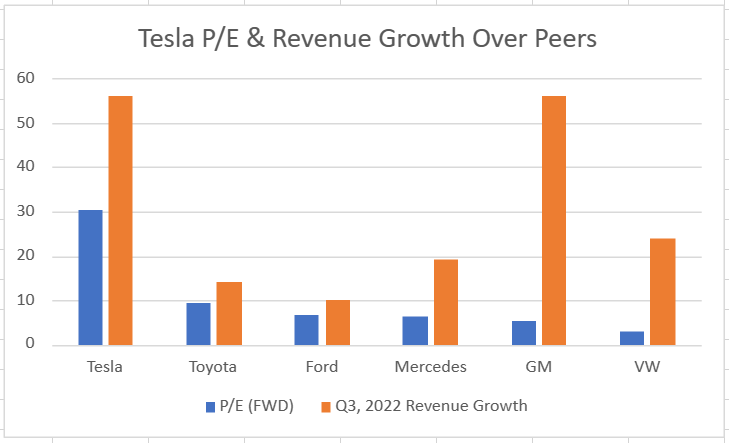

Data sourced from Seeking Alpha & company reports

As we can see, aside from General Motors (GM) and Volkswagen (OTCPK:VWAGY), Tesla is seeing far more robust revenue growth y-o-y compared with its peers. The matching of revenue growth by GM and the apparently robust performance of Volkswagen in this regard are anomalies, mostly having to do with continued post-COVID crisis readjustments towards normal market trends, rather than a real long-term trend. The more accurate picture in this regard is Tesla versus its other peers, namely Toyota (TM), Ford (F), and Mercedes (OTCPK:MBGYY).

There are, of course, other factors that play a role in P/E ratios when doing an industry peer comparison. The overall financial situation, such as debt levels, is an important factor, as well as profit margins, asset values, and so on. In the case of certain legacy car makers, especially European-based companies, we are arguably also looking at stranded assets, as EU law currently obliges car makers to switch to 100% non-ICE car sales in the EU by 2035. We could in fact be looking at companies such as Volkswagen facing decommissioning costs, a write-down of ICE-related patents, and so on. Dividends are another important factor that can play a role. For instance, Ford’s dividend will pay the equivalent of one’s basis within about 3 decades in dividends, if one does not include compounding effects. Tesla currently does not offer a dividend.

While many other factors can be considered, one of the main measures is whether a company can grow into its market cap and the speed at which it can do so. Looking at revenue growth, Tesla’s P/E ratio is currently about three times higher than Toyota’s and it is also growing about four times faster in terms of revenues. I expect revenue growth to decelerate significantly in the coming years for Tesla, but I think the same can be said about Toyota. Incidentally, Tesla’s market cap is now twice the size of Toyota’s, whereas just a year ago, it was about twice the size of the market caps of all of the companies I included in the comparison chart combined.

Tesla’s growth opportunities around the world & challenges ahead

Just a few years ago, the electric vehicle (“EV”) market in the Western world was Tesla’s to dominate. A fundamental flaw in the approach of most of the established automakers, namely the quest to provide the market with EVs that average people can afford, led them to focus on producing city EVs, with very little appeal for consumers who were looking to more or less match the utility derived from an ICE-powered vehicle. The inevitable result was a poor showing by most of them, even as Tesla captured more and more of the luxury car sales segment, which is where an EV can be priced at a level that allows EV producers the ability to provide the kind of range convenience that consumers have come to expect from an automobile.

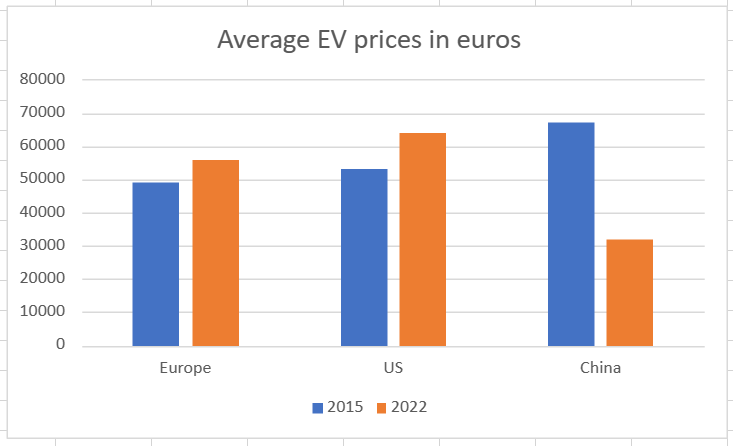

Other carmakers have been gradually learning, and as a result, the average price of an EV sold in Europe right now is 14% higher than it was in 2015, while in the U.S. prices rose by 43% for the same period.

Data sourced from: Fleet Europe

What the data on EV prices tells us is that Tesla has far more competition now in its quest to dominate the Western world’s luxury car segment. It is arguably going to become an impediment to further sales growth in these markets at some point, perhaps in the not-very-distant future.

In China, completely different market dynamics are taking shape. Evidently, Chinese consumers do not value range nearly as much, nor do they feel the need to splurge on the comfort that one might desire to have on a longer-range road trip. For this reason, a precipitous decline in average EV prices took place in that market, even as EV prices in the West rose. This presents Tesla with the challenge of providing a more affordable EV option in China, which is partly met by producing in China, where apparently the average cost to produce an EV may be as much as $10,000/unit lower on average, based on some recent estimates. Tesla’s Model 3 starting price was accordingly about $13,000/unit lower in China than it is in the US, before the latest price reductions announced by Tesla. I expect that Tesla still has some significant room to capture market share in the Chinese auto market, albeit while facing some very stiff competition from local EV makers.

We should not forget that while North America, Europe, & China are indeed by far the most important auto markets and EV markets as well, there are also plenty of other emerging markets where Tesla has plenty of room to make inroads going forward. India, for instance, has a fast-growing economy that is giving rise to a fast-growing strata of relatively wealthy professional elites and business owners, in other words, the prime consumer demographic for Tesla. The number of millionaires is set to double between 2022-2026. For now, Tesla avoided entering the Indian market, but it probably will within a few years, and that is a significant untapped market. Same can be said about South America, the ME region, as well as a number of Asian markets that are yet to be tapped. It may be the case that Tesla sales are reaching a point of stagnation in Europe & North America, but there are plenty of opportunities to continue growing in much of the rest of the world.

Investment implications

The continued volatility of Tesla stock, its lack of a dividend, as well as a number of other factors still make this a less than enticing investment opportunity for more conservative fundamental investors. I have absolutely no doubt that Tesla stock will at times get ahead of its fundamentals again on repeated occasions, and it may also overshoot the fundamentals on the way down. What I expect to see more and more is for Tesla’s stock price to intersect that point where one can argue that the fundamentals are reasonable more and more often. At its current price/share, TSLA is now trading in line with reasonable fundamentals when considering most factors, as I see it. Therefore, I decided to add Tesla stock to my portfolio. If it will rise in the future, getting far ahead of those fundamentals, I will probably take some profit, if it drops well below the fundamentals, then I will add.

The selloff in Tesla stock in the past year did bring it to its fundamentally reasonable levels, and as the company continues to mature, I expect that its valuation will increasingly be married to those fundamentals. Therefore, Tesla, Inc.’s stock price performance should from now on become increasingly less volatile, and more predictable.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment