Xiaolu Chu

Tesla’s (NASDAQ:TSLA) share price has continued to suffer. The company is struggling to maintain its market share as new offerings come to the market and it is no longer the largest EV company globally. As we’ll see throughout this article, we expect the company will decline into “another” car company, substantially decreasing its multiples and valuation.

Elon Musk’s Divided Attention

Elon Musk is a polarizing figure; however, it’s easy to argue that Tesla wouldn’t be where it is without him.

However, there’s no denying that his attention is currently divided. The rumor is that Elon Musk is now living on the 10th floor of the Twitter headquarters effectively, with his kid at work, looking to salvage what was undeniably a misplaced $44 billion bet. As Elon Musk himself has told employees, bankruptcy isn’t out of the question.

We expect in the intermediate term Twitter will utilize the majority of Elon Musk’s efforts. On top of that are the greater risks of dozens of Tesla employees being pulled to Twitter, and Tesla’s financing. Those are risks worth paying close attention to as Twitter struggles. While everyone knows those struggles, the company is continuing to sell billions in stock to fund Twitter.

Tesla Market Share Decline

At the same time, there is a larger risk of Tesla’s market share decline as competition increases in the markets.

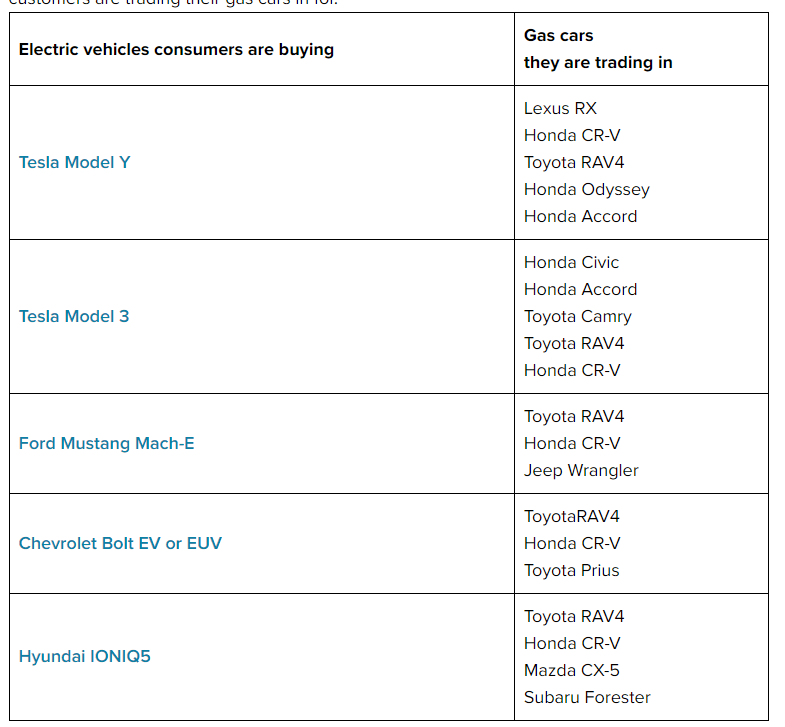

New data from S&P Global Mobility highlighted how Tesla’s share of newly registered EVs was 65% in 3Q 2022, down from 71% in the prior year and 79% in 2020. The forecast is for the company’s share to decline to less than 20% by 2025. As the number of new models out there increases, it’s clearly evident that consumers are moving away from Tesla’s offerings.

A substantial part of the case is that Tesla isn’t cost-competitive with the company’s cheapest offerings at barely before $50,000. In a world where EVs make up 5% of the market, Tesla is declining its market share in an incredibly small market. While U.S. EV demand will grow over the long term, for the above reasons, we expect Tesla won’t maintain its dominant market position.

We expect this market share decline to continue rapidly.

New Competition

We expect that the company’s new competition will continue to increase rapidly, hurting its potential, especially in markets like China.

Cars

One of the largest sources of new EV purchasers is the classic massive legacy car makers, especially those in South Korea and Japan like Toyota (TM, OTCPK:TOYOF) and Honda (HMC, OTCPK:HNDAF), have been slow to shift to EVs, driving away customers. We expect that to change. Despite these companies being slow to the game, they have lofty targets to change their goals.

Honda has announced plans earlier this year to spend $40 billion on electrification, with 40% North America 2030 EV sales and 100% EV sales in 2040. The company is also aiming for 0% emissions and 0% fatal crashes globally by 2050, both lofty goals that we think the company should be able to achieve.

Toyota has announced the largest goal of any car manufacturer at $70 billion, with the goal of 35% of sales happening from EVs by 2030 across 30 vehicles. The specifics are less important, but the takeaway here is that Tesla did great to begin with because it was the only game in town. But the short-term market share declines and long-term automaker targets show changes.

Second to the Semi, Autopilot Next

An example of Tesla falling behind isn’t just in the low-cost market where it’s a true competitor.

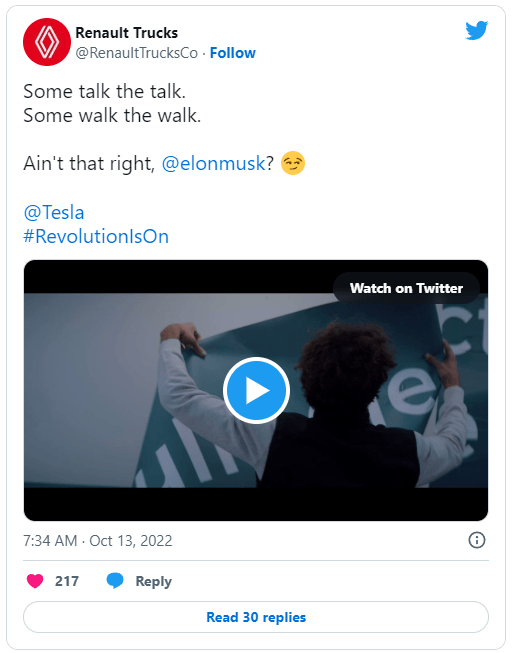

Renault Trucks

Renault (OTCPK:RNSDF, OTCPK:RNLSY) recently mocked Tesla after sending its EVs to the market to Coca-Cola ahead of Tesla’s promised trucks to Pepsi. Tesla has announced a plan to produce 200 semis in 2022 and up to 50,000 vehicles in 2024. The company’s semi did recently accomplish an impressive 500-mile drive with an 81-thousand-pound load.

The EV truck market is very different though. The company’s customers are much more willing to buy a new vehicle to save, and the producers need to produce a single high-quality model. In Europe especially, where trucking routes are much shorter, the market is expected to grow rapidly. Volvo (OTCPK:VOLAF, OTCPK:VLVLY, OTCPK:VOLVF) has also recently started production of its heavy-duty truck.

While the Tesla Semi is finally hitting its point of delivering to customers, EV battery pack shortages are still substantial, and we expect that to define the markets for the next few years.

This is similar to autopilot where, despite originally promising a full EV years ago, Tesla has continued to flounder. Multiple companies are leading Tesla in self-driving technology. What bulls once touted as a massive source of revenue, self-driving packages for existing cars, has now become a source of lawsuits after the company’s claims.

Delays for the company’s semi and autopilot, where it loses significant first-to-market advantage for both, we expect to put major pressure on the company.

Our View

There’s no denying that Tesla has changed the market. Our view against the company as an investment doesn’t change our view over the company itself or its cars.

However, in markets where the company is looking to enter, such as Tesla Semi and autopilot, not only does the company not have a first mover advantage, but as discussed above, the company is already facing lawsuits from prior claims. There’s no denying the Tesla Semi is a game-changing vehicle but ramp up will be slow and competition increasing.

Unfortunately, the volatility around Tesla’s stock makes it a tough short. Even Jan. 2024 PUTs at current market price have a cost of ~20%, making it an expensive short. Shorting it on the open market is an incredibly risky proposition, one worth paying close attention to, and one that we would recommend being cautious about doing.

We recommend investors aggressively sell out of the stock, at minimum, if they have a position.

Thesis Risk

The largest risk to our thesis is that Tesla has a history of execution and there are still new markets. At 200k per semi, the company’s 2024 semi targets alone could become $10 billion in revenue at reasonable margins given the potential for cost savings to the company’s customers. It could happen to solve self-driving.

Or investors could just drive the company up in another bull market, like they have over the past few years. For no reason at all. All of that will mean investors are worse off than they could have been.

Conclusion

Tesla has lost the semi race, although it’s not far behind, delivering to Pepsi just a few days after Renault’s delivery to Coca-Cola with a better semi truck. Unfortunately in autopilot, another rumored area of growth, the company doesn’t seem to be performing well either, with lawsuits now having the potential to cost the company substantially.

A substantial number of Tesla’s customers have been moving away from classic companies like Toyota and Honda that don’t offer EVs yet. That’s expected to change in the upcoming years and new models are already reflected in Tesla’s declining market share. We expect that change to substantially hurt Tesla’s ability for future returns.

Be the first to comment