Devrimb/iStock via Getty Images

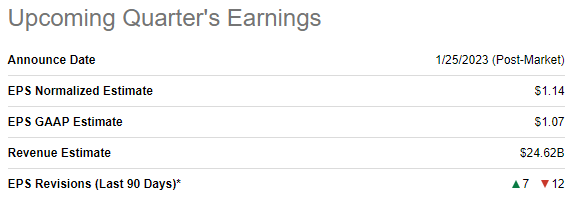

Seeking Alpha’s Consensus Estimates

Seeking Alpha provides average revenue and EPS estimates from more than 30 Tesla (NASDAQ:TSLA) analysts each quarter, which appear on its “Tesla Earnings” page. There are no public averages of the individual components, nor are detailed models of individual analysts easy to obtain. Many are in fact proprietary. I attempt to “flesh out” what consensus supporting details might look like.

Below is the data on Seeking Alpha’s website to which I am reconciling my detailed estimates:

Seeking Alpha

The first figure I focus on is the consensus revenue estimate of $24.62 billion reported above. Later, I try to justify the associated fully diluted GAAP EPS figure of $1.07, also reported above. (Seeking Alpha defines its GAAP earnings estimate as the fully diluted GAAP figure. A certain other financial website which provides EPS figures does not specify whether it uses GAAP or non-GAAP, primary or fully diluted, so it is great that Seeking Alpha does so.)

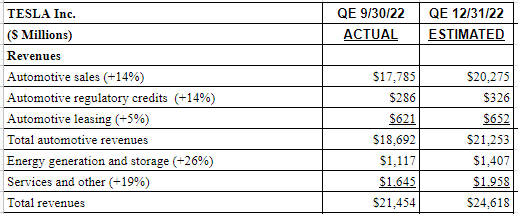

“Fleshing-Out” $24.62 Billion of Revenue

Below is my line-by-line breakdown of the consensus total estimated revenue figure of $24.62 billion for Q4. For each category of revenue, I made an estimate based upon what I believe are reasonable percentage increases from the corresponding Q3 actual figure as reported on p. 5 of Tesla’s September 30, 2022 10-Q.

Tesla (Q3) and Author (Q4)

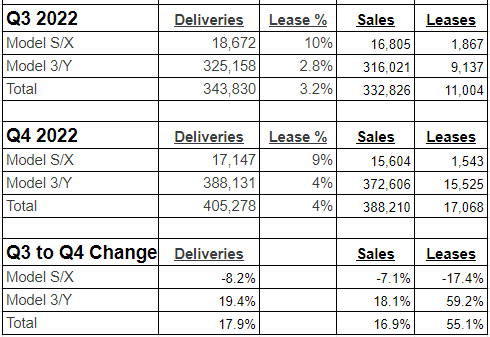

Sales vs. Lease Estimates:

Obviously the most important figure for estimating revenue is the automotive sales number, which is also the category we know the most about due to the recent production and delivery (“P&D”) report. Utilizing the two most recent reports, I created the following table:

Tesla and the Author

Although the Q4 figures are exactly the ones Tesla reported in the Q4 P&D report, I made some minor adjustments to the Q3 P&D Report figures. Tesla only provides the percentage of leased cars (not the specific number) in the delivery figure, rounded to the nearest percent, in those reports.

When the Q3 shareholder letter was later issued, it reported a total of 11,004 leased vehicles, which means the total lease percentage was more accurately about 3.2%, but the letter does not provide a breakdown of S/X vs. 3/Y. I kept the original S/X total in the above chart, and made the entire adjustment to the 3/Y total. In actuality, the S/X leases could have been any amount between 1,713 and 1,960 (9.5%-10.5%) with a similar unit range possible of the 3/Y leases.

My Logic for the above Line-by-Line Estimates

- Automotive Sales-Unit sales increased 16.9% in Q4. However, higher priced S/X sales actually decreased. We also know that there were price cuts, mainly in China. As a result, I am estimating a 14% increase in revenue, which may be a bit optimistic.

- Automotive Leasing-New leases have increased about 55% last quarter, but this does not translate to a 55% increase in lease revenue. Under normal lease accounting, revenue for a lease is typically taken ratably over the period of the lease. Further complicating matters is the fact that there are always old leases running off, and even the new leases would only be in effect for part of the quarter. Finally, Tesla discloses that some leases are sales-type leases, which I believe means that in certain cases the entire lease revenue (or at least the leases present value) is recognized up-front. In any case, quarterly lease revenue has fluctuated between $558 million and $688 million in the past year with no clearly discernible pattern. My estimate is that there was a 5% increase last quarter.

- Automotive Regulatory Credits-This is an impossible figure to accurately predict; I simply increased the figure by the same percentage I used for automotive sales revenue.

- Services and Other– Revenue increases have been surprisingly strong during the past year, ranging from 12% to 20% per quarter, although it was only a 12% increase in Q3. I would have expected the increase in this category to more closely track the size of Tesla total “installed base” (cumulative sales). I am estimating a generous 19% increase.

- Energy Generation and Storage-I have estimated a 26% quarterly revenue increase for this category partly because this is the area where investors are expecting rapid growth. To a certain extent, it is also a “plug” in my attempt to justify the analysts’ average estimate of $24.62 billion of revenue.

Although I have simply tried to justify the consensus revenue estimate, I feel that I may have been a bit optimistic in some of my assumptions. As a result, if I had to take the over/under on $24.62 billion, I would take the “under”. it is also interesting that the reported consensus estimate on SA has decreased by $160 million over the past few days, likely as a delayed reaction to the delivery disappointment.

“Fleshing Out” Q4 Expenses and Net Income

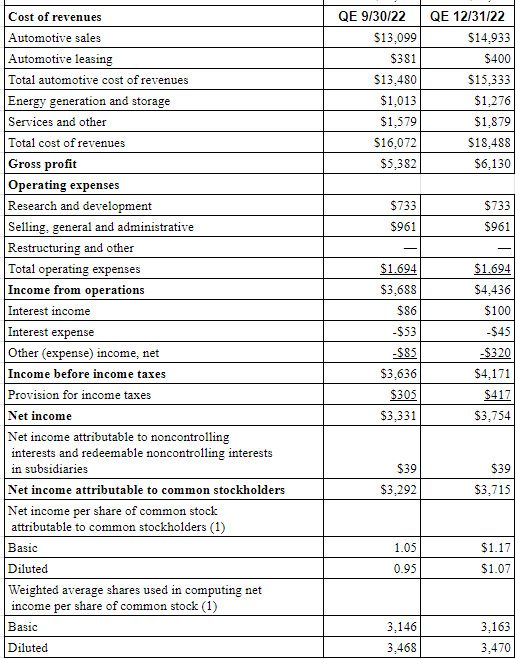

I have provided below the remainder of my estimated income statement for Tesla’s Q4:

Tesla (Q3) and Author (Q4 Estimates)

The consensus analyst estimate does not provide a net income figure, just a diluted EPS. I therefore put together this table by working first from the “bottom up” and then from the “top down.”

The diluted share count only increased by 3 million in Q3, so I increased the share count a further 2 million to get to the 3.47 billion diluted share figure. I then multiplied this by $1.07 to arrive at the implied net income of $3.713 billion. I then worked from the top to reconcile to this net figure. (My table, due to rounding, shows $3.715 billion.)

Cost Assumptions

I made a set of straightforward (some might say simplistic…) assumptions regarding individual cost figures. For all business lines I used the same gross margins as had been the actual case in Q3. I also utilized the same operating expense figure as the actual Q3 amount. My logic for the major line items is as follows:

- Automotive Gross Margin- On the one hand, increased volumes should have aided margins. On the other hand, price cuts during the quarter could have negatively impacted them. As a result, I am assuming margins have remained about the same.

- Energy Generation and Storage- If in fact this segment’s revenue increases as much as I have penciled in above, margins on Tesla’s energy storage products should have increased. On the other hand, energy generation is quite seasonal, with both revenue and margins being much lower in the winter months.

- Operating Expenses- I have kept these expenses the same. Despite the company growing, Tesla management has been making statements about trying to control expenses.

- Interest-Although minor amounts, I have increased interest income a bit and decreased interest expense. I expect that Tesla’s cash balance will increase and its debt to decrease.

- Income Tax-I am utilizing 10% of pre-tax income as Tesla’s tax rate; it has generally been a bit less than that.

Finally, in order to get near the net income figure of $3.713 billion, I used the Other (Expense)/Income line as a “plug,” which required that amount to be a net expense of $320 million compared to a net expense of $85 million in the prior quarter. In fact, in many quarters this line has shown a minor amount of net income.

As a result, if anyone does not agree with my specific allocation of revenue and expense items, this is a convenient line to set to zero, and utilize the $320 million somewhere else. For example, Regulatory Credit Revenue, an extremely hard to predict item, is $326 million, so by making that zero, the totals would almost perfectly balance. If a reader thinks that keeping the automotive gross margin the same despite price cuts in Q4 is unreasonable, then the automotive sales cost of revenues line item could be increased by $320 million. (This would cause the gross margin, prior to regulatory credits, to decrease from 24.2% to 22.8%.)

Of course, a reader could also decide that any set of assumptions and estimates that result in $3.7 billion of net income are too conservative, and so there would likely be an earnings beat announced on Wednesday. I have attempted to make this model as logical and transparent as possible, allowing readers to make a few of the own adjustments more to their liking.

A Couple of Wildcards

Income Taxes:

Income tax is an extremely complex and widely misunderstood topic but potentially a hugely material one. Tesla only reports certain details regarding its income tax situation once per year.

There are two tables in “Note 14- Income Tax” on Tesla’s 2021 10-K (p. 86) which I provide below. I will explain a bit about each table and some “takeaways” from them. Once the 2022 10-K is released (likely within a week of the earnings report) I encourage TSLA investors to compare the 2022 tables to the ones presented here.

The first table indicates that ALL of Tesla’s pretax GAAP income was generated overseas (most, if not all, in China) and that it actually experienced a $130 million pre-tax loss in the U.S. (As a result, Tesla did not accrue any U.S. federal income tax expense for 2021.) It is this table that is referred to by posters who state that Tesla loses money in the U.S.

Tesla 12/31/21 10-K

These figures are not necessarily 100% in alignment with the underlying economics; companies have a certain amount of discretion as to how to allocate income and generally will attempt to do so in the most financially advantageous way. One factor is tax rates; the U.S. federal corporate tax rate is 21%, while Tesla receives a concessionary 15% rate in China until the end of 2023, as opposed to its statutory rate of 25%.

Items such as transfer pricing, allocations of overheads etc., can impact the relative numbers. However, I believe it is fair to say that, at a minimum, the vast majority of Tesla’s pre-tax income was generated in China in 2021. It will be interesting to see what the 2022 figures look like. In fact, 2024 should be even more interesting, when China’s 25% rate goes into effect for Tesla.

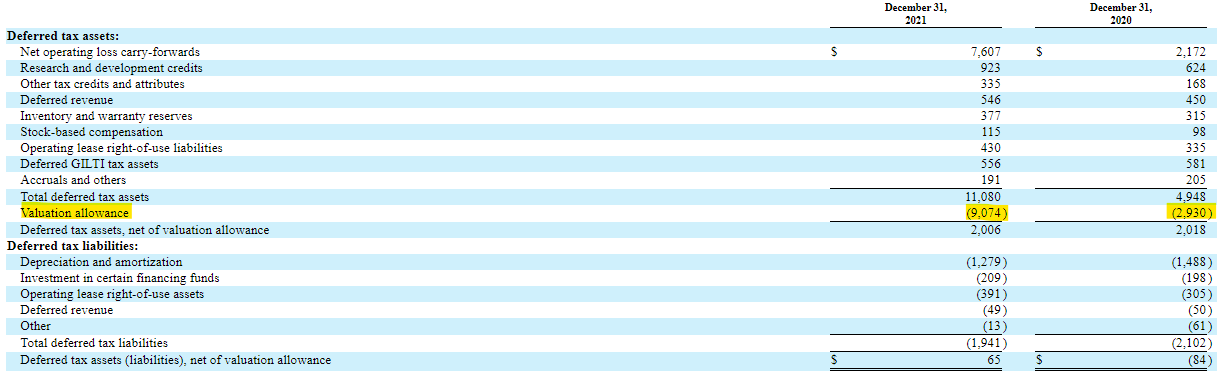

I have highlighted the one figure in the footnote’s “Deferred Tax Assets” table that I believe investors should focus on, the “Valuation Allowance”:

Tesla 12/31/21 10-K

Tesla has established a huge $9+ billion “Valuation Allowance” against its $11 billion of “Total Deferred Tax Assets” which is explained in the note below the table:

As of December 31, 2021, we recorded a valuation allowance of $9.07 billion for the portion of the deferred tax asset that we do not expect to be realized. The valuation allowance on our net deferred taxes increased by $6.14 billion, $974 million, and $150 million during the years ended December 31, 2021, 2020 and 2019, respectively. The changes in valuation allowance are primarily due to additional U.S. deferred tax assets and liabilities incurred in the respective year. ….. We continue to monitor the realizability of the U.S. deferred tax assets taking into account multiple factors. In completing this assessment, we considered both objective and subjective factors. These factors included, but were not limited to, a history of losses in prior years, excess tax benefits related to stock-based compensation, future reversal of existing temporary differences and tax planning strategies. After evaluating all available evidence, we intend to continue maintaining a full valuation allowance on our U.S. deferred tax assets until there is sufficient evidence to support the reversal of all or some portion of these allowances. Given the improvement in our operating results and depending on the amount of stock-based compensation tax deductions available in the future, we may release the valuation allowance associated with the U.S. deferred tax assets in the next few years. Release of all, or a portion, of the valuation allowance would result in the recognition of certain deferred tax assets and a decrease to income tax expense for the period the release is recorded.

The bolded portions in the above note are my additions to identify the most significant bits. In particular, the final section states that release of the valuation allowance would result in a decrease in income tax expense for the period; this might be the understatement of the year. If the entire valuation allowance of $9.1 billion were to be released all at once, it would result in a negative tax expense of $9 billion dollars and a similar increase in net income for the quarter!

It is also important to understand how this deferred tax asset comes about. There are many differences between GAAP accounting and income tax calculations regarding income and expenses. One example is accelerated depreciation of equipment as permitted by the IRS. As a result, depreciation expense may be higher on the tax return than the GAAP statements, possibly even resulting in a GAAP profit but a taxable loss for a company, and therefore no income tax due.

One difference, which in the case of Tesla is a huge one, is the treatment of stock option exercises. Even though the actual exercise of options does not impact GAAP statements (instead the theoretical expense for them would have previously been recorded), the IRS allows an expense entry for the difference between the market value of the stock and the option exercise price on its income tax return.

Of course, in 2021, Musk exercised much of his vested 2012 stock option grant. CNBC estimated he had a potential $28 billion gain based upon the market price at time of grant, which is taxable at the time the options are exercised even if the stock is not sold. Tesla was able to record this same amount as an expense on its tax return. Having a $28 billion taxable deduction means that, at the Federal corporate rate of 21%, this will save Tesla almost $6 billion in taxes if it is ever able to utilize it. Although the gross deferred tax asset increased by about $6 billion, company management decided to increase the allowance by a similar amount due to the associated uncertainty of being able to utilize it, resulting in almost no change in the net deferred tax asset at about $2 billion.

The logic behind the IRS rule is that if Tesla had paid Musk $28 billion in cash compensation, it would have been a deductible expense, so giving him $28 billion in stock should be treated no differently. However, due to this provision, some large profitable corporations with generous executive compensation plans have had to pay little or no income tax, and it has become a political issue. My understanding is that the laws were changed for options granted after 2017. As a result, Musk’s 2018 options will not receive such generous treatment.

One additional issue Tesla investors should be aware of is the “Inflation Reduction Act” passed last summer about which Tesla stated the following in its September 30, 2022 10-Q (p. 16):

On August 16, 2022, the Inflation Reduction Act of 2022 (“IRA”) was enacted into law and is effective for taxable years beginning after December 31, 2022. The IRA includes multiple incentives to promote clean energy, electric vehicles, battery and energy storage manufacture or purchase, in addition to a new corporate alternative minimum tax of 15% on adjusted financial statement income of corporations with profits greater than $1 billion. These measures may materially affect our consolidated financial statements, and we will continue to evaluate the applicability and effect of the IRA as more guidance is issued.

Although final implementation rules have not yet been determined, the new AMT could have a significant impact on how/where Tesla reports income and what its reported tax rate going forward becomes. In addition, if Tesla takes a one- time gain by reversing the allowance on its deferred tax asset, it would likely need to begin reporting a higher tax rate in its GAAP statements. However, I believe it would not need to actually write checks to the IRS until the allowance is exhausted, subject to how it is impacted by the new AMT rules.

A Partial Write-down of Tesla’s Solar Lease Portfolio:

Tesla has a solar lease portfolio with a net carrying value in excess of $5.5 billion (most of which was acquired from Solar City.) The company has been amortizing the portfolio based upon the assumption that most of its customers will renew their leases after the initial term, typically 15 to 20 years, ends.

I suspect this is an unrealistic assumption and that many customers will not renew. Some of the earlier leases had initial terms of only 10 years, and were originated by Solar City over 10 years ago. As a result, Tesla must be beginning to obtain some actual data on renewal rates. If they are considerably lower than anticipated, Tesla may need to take a partial write-down plus increase future years’ amortization amounts. I would not be surprised if a write-down in the range of $500 million or more might eventually be necessary.

Summary/Conclusion

Although it is never an undynamic time with Tesla, it seems to be particularly dynamic one now, with new factories coming up to speed, significant price cuts being announced in various of its markets, and a number of “wildcards.” This may make the soon-to-be announced year-end financial results, and associated commentary, particularly enlightening.

In addition to my financial model, I focused on two “wildcards” in this article which do not seem to have garnered much attention. Even if neither one has a material impact on the financial results about to be reported, they are likely to have an impact in upcoming quarters.

Be the first to comment