Joe Raedle

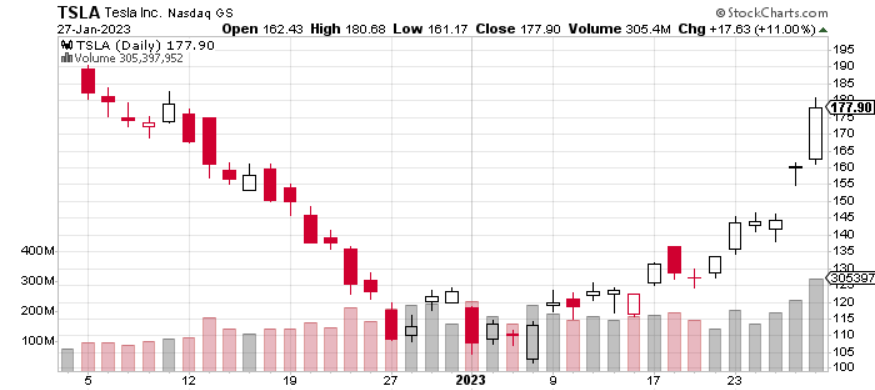

Tesla, Inc. (NASDAQ:TSLA) delivered on its Christmas gift to investors with a 63% gain following the holiday, as midday Friday trading saw Tesla in short-squeeze fashion, capping off a sixth straight gain on over 230% its average volume to bring weekly gains over 32%.

A gain of more than 32% following a relatively lackluster Q4 earnings report with some challenges presented for FY23 forces a deeper look at the underlying numbers — can Tesla reclaim summer 2022’s $300 level during FY23 with new models on the books, or will the $200 range be a target with Tesla having to flesh out margins early in the year after offering large discounts?

No Stranger To Short Squeeze Style Swings

Tesla’s latest 63% swing to date after Christmas is not necessarily unusual, as the company has seen multiple other short-squeeze style swings since 2020.

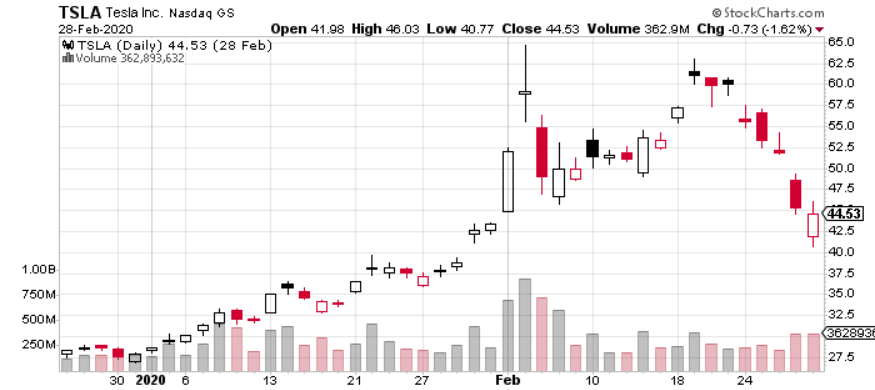

From after Christmas 2019 to February 4, 2020, Tesla gained 125%, with a 53% gain during the last two days of that period.

StockCharts

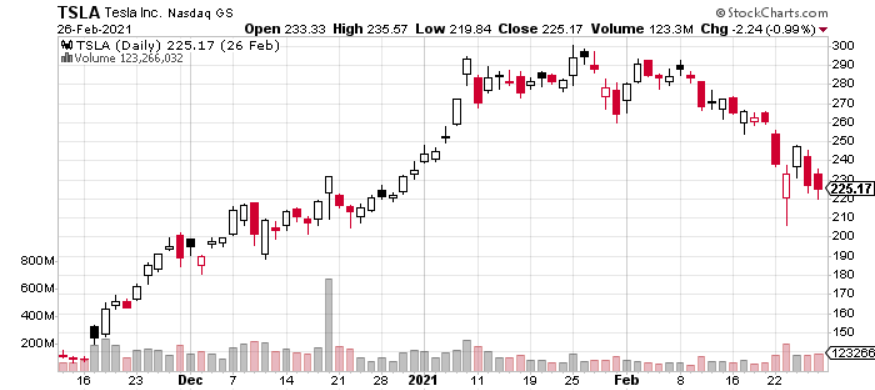

From December 23, 2020 to January 8, 2021, Tesla gained for 11 consecutive sessions, adding 38.1% over the period to cap off another 120% move in under two months.

StockCharts

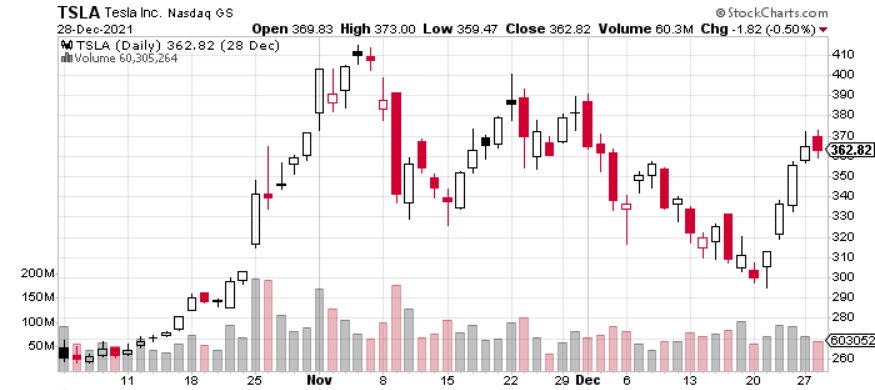

From October 8, 2021 to November 4, 2021, Tesla rose 56.5%, gaining in 16 out of 19 sessions, to reach its all-time high at $414.50 (split-adjusted).

StockCharts

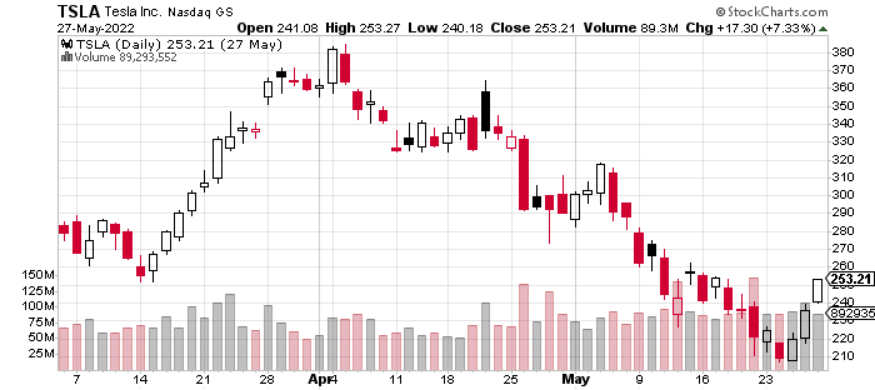

In March 2022, Tesla gained 43.5%, rising 10 of 11 sessions, with multiple large consecutive daily gains, before falling steadily lower for the next two months.

StockCharts

Now to Tesla’s recent rally — two strong days post-earnings have taken shares back to early December levels, moving from extremely oversold territory to overbought territory in just one month.

StockCharts

The question here: is this sustainable? Each of the prior short-squeeze style moves highlighted above were followed by substantial declines — each in excess of 25%, with April/May’s decline reaching nearly 45%. Moving forward, is Tesla’s Q4 report strong enough to generate substantial upside through 2023, or are shares set for a similar 25% drop first?

Digging Into Q4

The main headline figure from Q4’s release was a 59% surge in net income to a record $3.69 billion, but a handful of other numbers suggest there could be little to drive shares back to $300 this year.

31% Production Growth

One of the major takeaways from Q4’s report was Tesla’s forecast for just ~31% growth in production to 1.8 million vehicles during FY23; Musk did say that it is possible that Tesla “could build 2 million vehicles this year,” with demand existing to support that level of production.

At 2 million vehicles, Tesla’s production growth would be about 46% y/y, much closer to the level needed to support a “50% average annual growth in vehicle deliveries” over “a multi-year horizon” moving forward; however, Tesla is looking at the multi-year horizon beginning in 2020.

Tesla

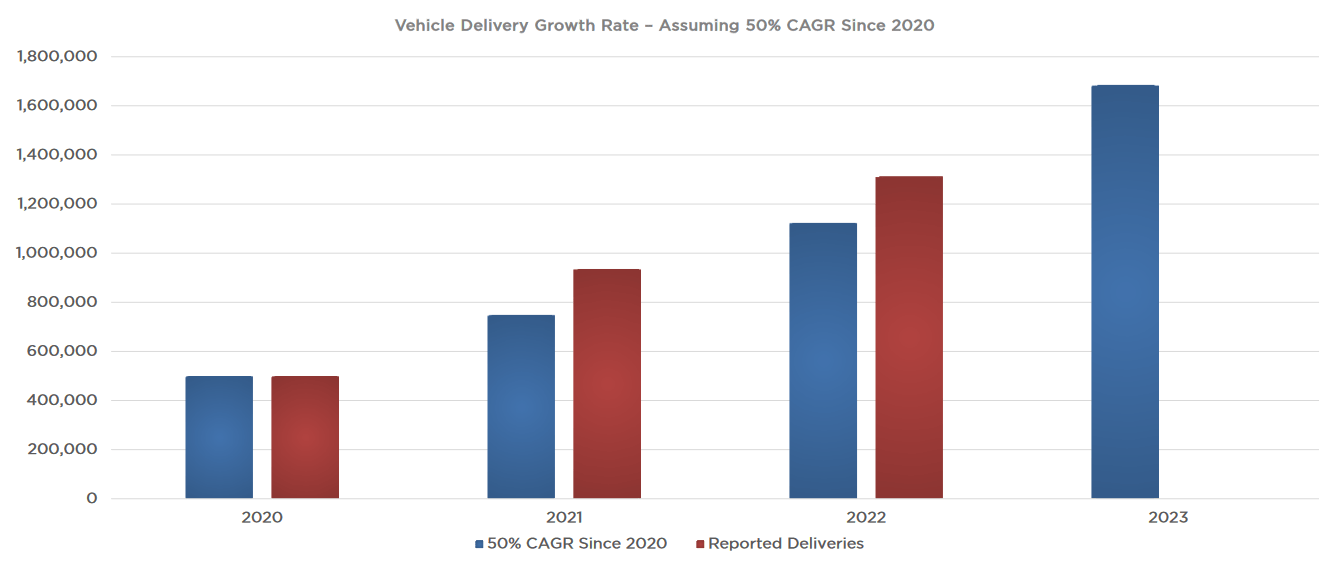

What would a 50% average annual growth rate through FY25 look like?

With about 1.31 million deliveries in FY22, a 50% average growth rate through FY25 would equate to deliveries ending the period at about 4.42 million. Modeling from FY20 through FY25, accounting for what Tesla considers its multi-year horizon, projects delivery volumes of nearly 3.8 million deliveries, about 10% below the forward-looking forecast.

24% Delivery Growth

In what is probably one of the most overlooked numbers gleaned from Q4’s report, Tesla is estimated to record only 24% y/y growth in deliveries for FY23, assuming that production tops out at 1.8 million units. With installed capacity in place to top over 1.9 million units of production, deliveries could reach closer to 31% growth should demand remain strong through the year, following Tesla’s major price cuts earlier in the month.

Modeling off of FY23’s initial production estimate of 1.8 million projects deliveries to be around 1.7 million, or that ~24% y/y growth rate. This correlates with Tesla’s internal estimate for about 1.69 million vehicles to hit that 50% CAGR from FY20’s 499.5k delivery volume. However, 24% y/y would be Tesla’s lowest ever growth rate for deliveries.

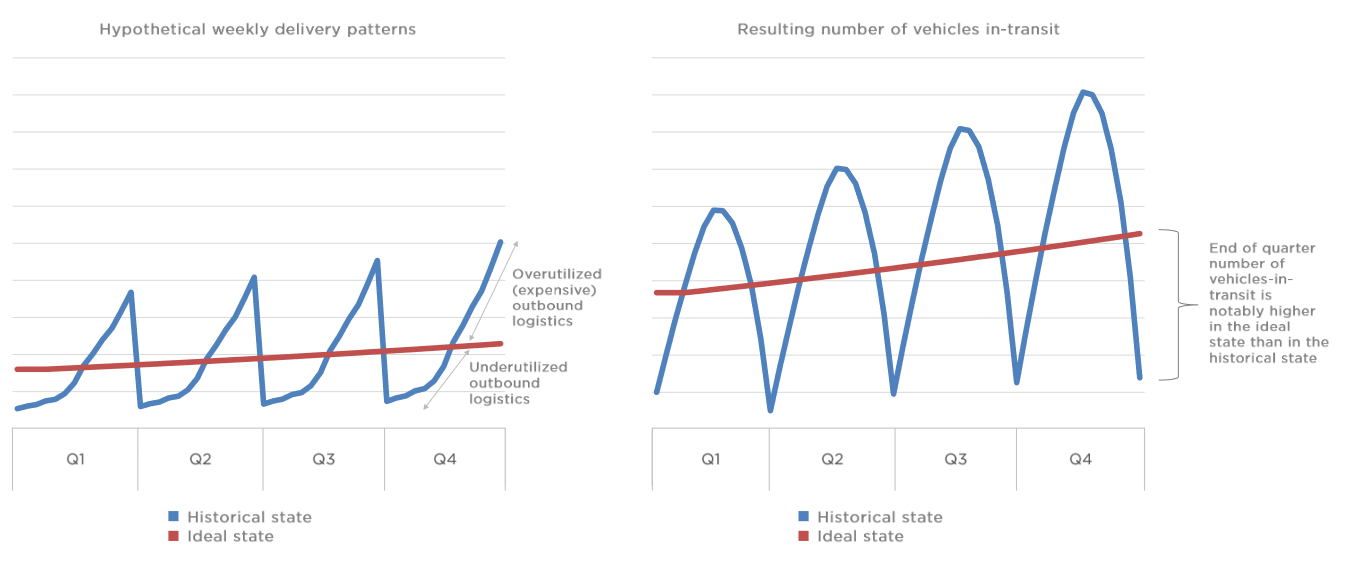

Supporting this view, or rather what is driving this view for 1.7 million deliveries on 1.8 million units production is an increasing amount of vehicles in transit and overextended outbound logistics.

Tesla

Increasingly overextended outbound logistics [left] not only increases logistics costs, impacting margins, but also leads to a higher number of vehicles in transit each quarter [right]. As seen above, Tesla witnessed a steady increase in the amount of vehicles in transit each quarter in FY22, as the company gradually overextended its outbound logistics.

With initial estimates for transportation capacity to expand and push freight rates lower through FY23, the logistics sphere should clear for Tesla — but vehicles in transit and overextended logistics will not clear immediately, if at all.

While the price cuts had initially sparked concerns over demand, Musk noted that “vehicle orders were roughly double production in January.” Although this certainly should ease concerns over the price cuts, having such a large order volume relative to production could extend fulfillment times, leading to continuation of the high vehicles in transit narrative that impacted deliveries in the back half of FY22. For 1H FY22, Tesla delivered just over 100% of production, while for 2H FY22, as vehicles in transit surged, Tesla delivered 93.4% of its production volume.

For FY23, this decline in Tesla’s delivery-production ratio is expected to persist, with Tesla projected to kick off Q1 delivering about 92% of its production, before an easing transportation market brings that back over 96% by Q4, for about 94.5% of annual production being delivered.

FY23 Projections And Beyond

From a revenue standpoint, the price cuts are not a positive especially when combined with the prospect for Tesla’s lowest ever growth in deliveries.

With Tesla Semi in pilot production and Cybertruck expected to start mass production at the end of the year, revenues and positive impacts to ASPs are expected to be minimal, at best.

Price cuts from about 6% to 20% for Tesla’s models are expected to have a negative impact on ASPs, which hovered at about $54.5k for FY22. Assuming ASPs decline about 9% to 11% for FY23 with no further price cuts or major increases, ASP would end FY23 at about $48,500 to $49,600.

From a revenue standpoint, 24% growth in deliveries to 1.7 million vehicles and a ~10% decline in ASPs is a worst-case scenario for growth — this projects FY23 automotive revenues at $83.47 billion, or 16.8% y/y growth. With about $12 billion to $14 billion in services and energy storage revenues, total revenues for Tesla for FY23 are estimated at $96.47 billion, or 18.4% y/y.

That 18.4% y/y revenue growth, following FY22’s 51% growth rate, looks abysmal. Combined with some persistent margin weakness, due to price cuts and rising component prices, among other factors, Tesla could struggle to find EPS growth, with current analyst estimates pegged at -3% growth. Musk sees software revenues from FSD aiding margins, but with that revenue being recognized on a deferred, rather than immediate, basis, margins may not be able to reclaim 29% this year.

Competition In Focus

The focus for 2023 through 2025 turns to competition — Tesla sits at second for global market share for the first nine months of 2022 with 13%, behind BYD’s (OTCPK:BYDDY) 16%.

Forecasts for EV growth in FY23 differ — BloombergNEF “is forecasting about 13.6 million deliveries, up from more than 10 million in 2022,” or around 35% growth. DigiTimes sees EV sales volumes potentially reaching 14 million units.

LMC Automotive is expecting fully electric vehicle sales to reach 11 million vehicles in FY23, up from 7.8 million in FY22, or about 41% growth.

Tesla’s projected 1.8 million production volume and subsequent 1.7 million delivery estimate arises as a major concern here — Tesla is expected to record slower growth than the market in FY23. We previously highlighted that “the challenge lies not within one manufacturer overtaking Tesla’s crown, but rather a handful of manufacturers all pushing EV volumes higher, and the group squeezing Tesla’s share.” For FY23, this is an increasingly likely scenario should Tesla not find meaningful upside above 1.7 million to 1.8 million deliveries. At such a level, Tesla’s market share is projected to dip about 12.5%.

Outlook

Tesla’s short-squeeze style move has quickly taken shares off lows in early January, back to early December levels following a mediocre, mixed Q4 earnings report. While Tesla did post 59% growth in net income to end the year, commentary about production volumes along with recent major price cuts do not bode well for FY23.

With an initial target of 1.8 million vehicles produced this year, deliveries could grow just 24% in FY23 with logistics and increased vehicles in transit expected to persist through the first half of the year. With decreasing ASPs, revenues for the year are projected to grow just 18.4% to $96.47 billion, a far cry from FY22’s 51% revenue growth. Margin weakness is also expected to keep EPS growth minimal, or negative. Given Tesla’s quick rise to overbought levels after such a rapid move in shares, entering the short-squeeze move should be approached with caution, as the underlying numbers do not look to support a reclamation of $300 in FY23.

Be the first to comment