PonyWang

Introduction

ASML Holding (NASDAQ:ASML) reported strong results Jan. 25, especially considering the current semiconductor industry landscape. The demand for the company’s tools remains strong but it’s normalizing. However, it does seem that the company will come out of this semiconductor downturn with its income statement largely unaffected thanks to its growing order backlog, just as we described in previous articles.

Without further ado, let’s get on with the numbers.

The numbers

The headline numbers

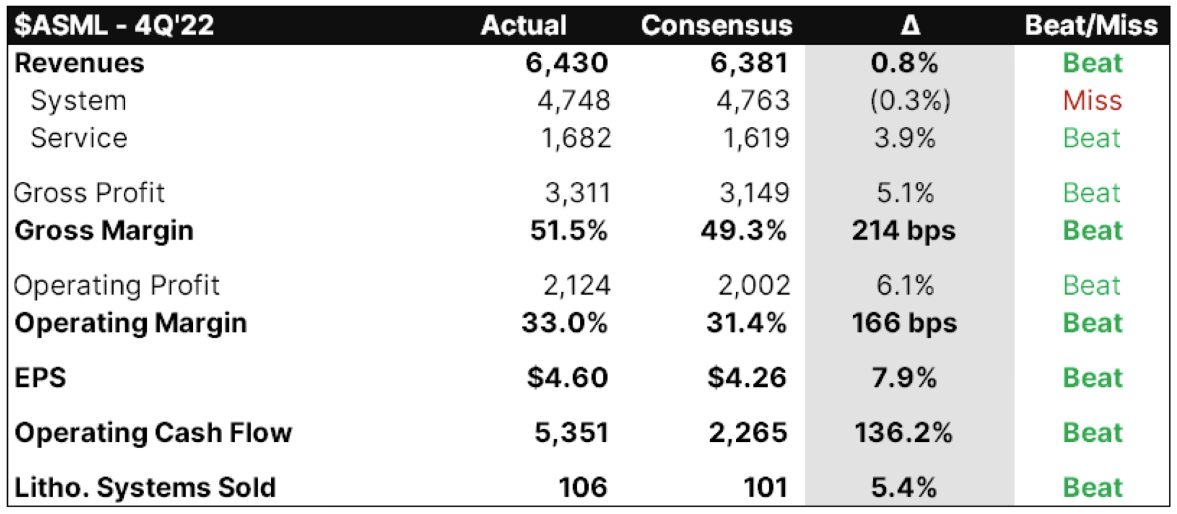

ASML managed to beat analysts’ top and bottom line expectations again by a substantial margin:

Consensus Gurus

We are typically skeptical of estimates (we think they are constructed more by management than analysts), but we honestly don’t blame analysts for getting them wrong for ASML. Making quarterly predictions for ASML must be one of the most challenging things in the investment profession. We say this because some of the company’s systems have a high selling price and delaying or anticipating the recognition of their revenue can change any given quarter quite a bit. For example, say that the revenue recognition of two EUV systems gets pushed out to the next quarter; this already defers around €300 million in revenue and it’s pretty challenging for analysts to grasp such timing.

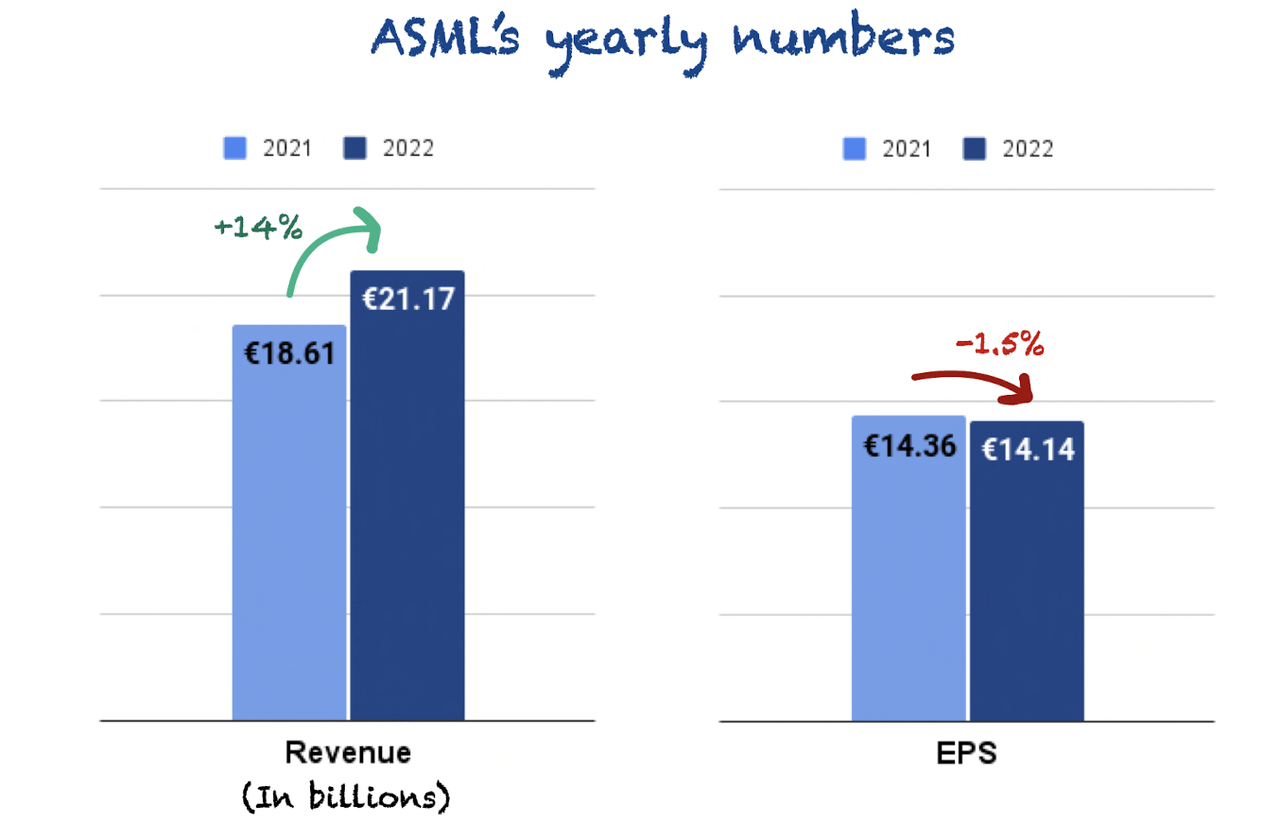

Anyhow, as quarterly numbers are difficult to estimate due to volatility, looking at the quarterly year-over-year growth rates can be misleading too because deferred revenue can make these growth rates vary substantially. The good thing is that we already have the yearly numbers, so we’ll focus on these for this article. ASML posted strong numbers in 2022:

Made by Best Anchor Stocks

Revenue grew 14% year over year, but several things negatively weighed on margins, making EPS decrease 1.5% year over year. It’s also worth noting that ASML deferred €2.8 billion in revenue to 2023 due to fast shipments. To strip out this effect, management calculates “normalized revenue,” which was €24 billion in 2022:

ASML’s Q4 and FY 2022 Earnings Presentation

Had the company recognized all the systems it shipped as revenue, sales would have grown by 29% year over year. This sounds great, but the reality is that sales, as reported, grew 14%, which is the number that we should really look at.

Breaking down net sales

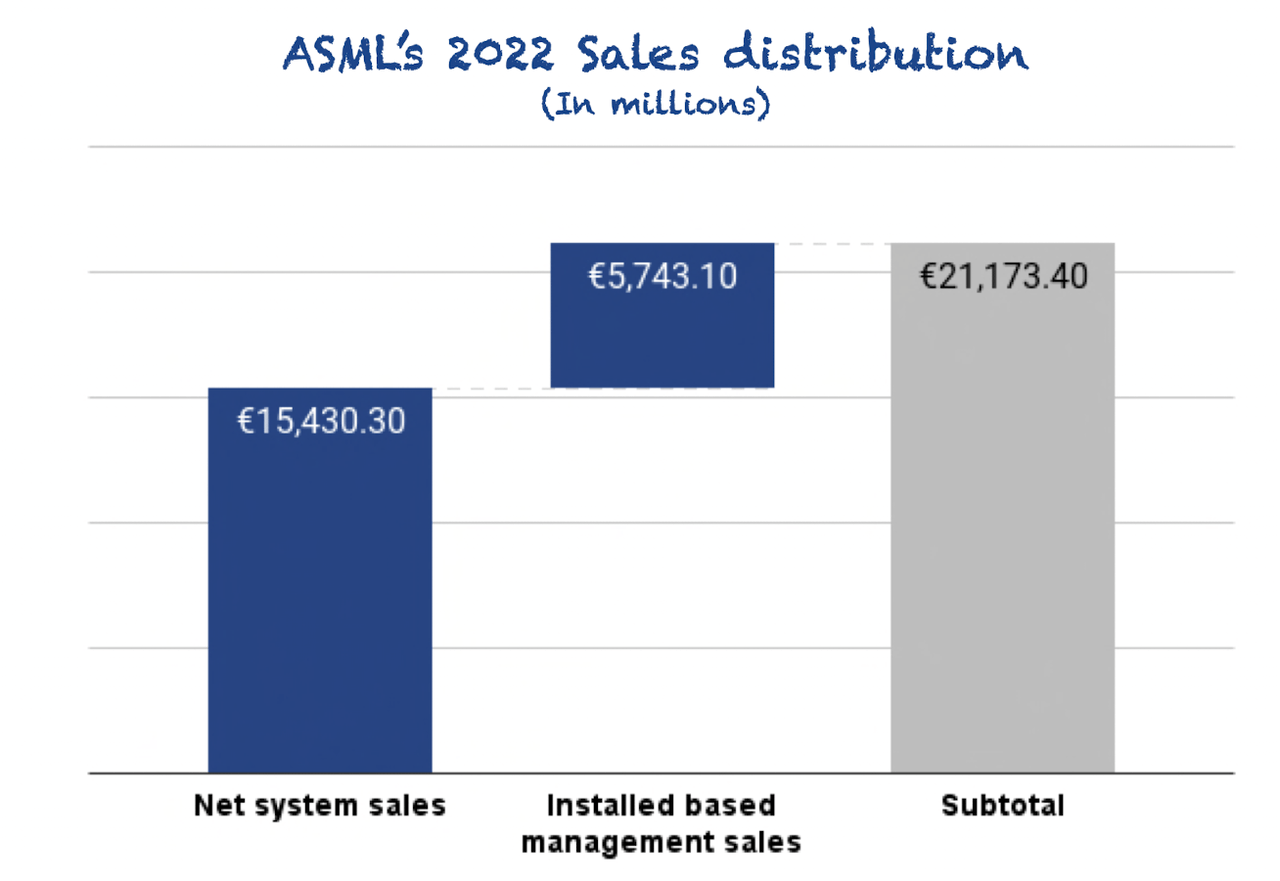

Revenue was distributed as follows across net system sales and installed base management sales:

Made by Best Anchor Stocks

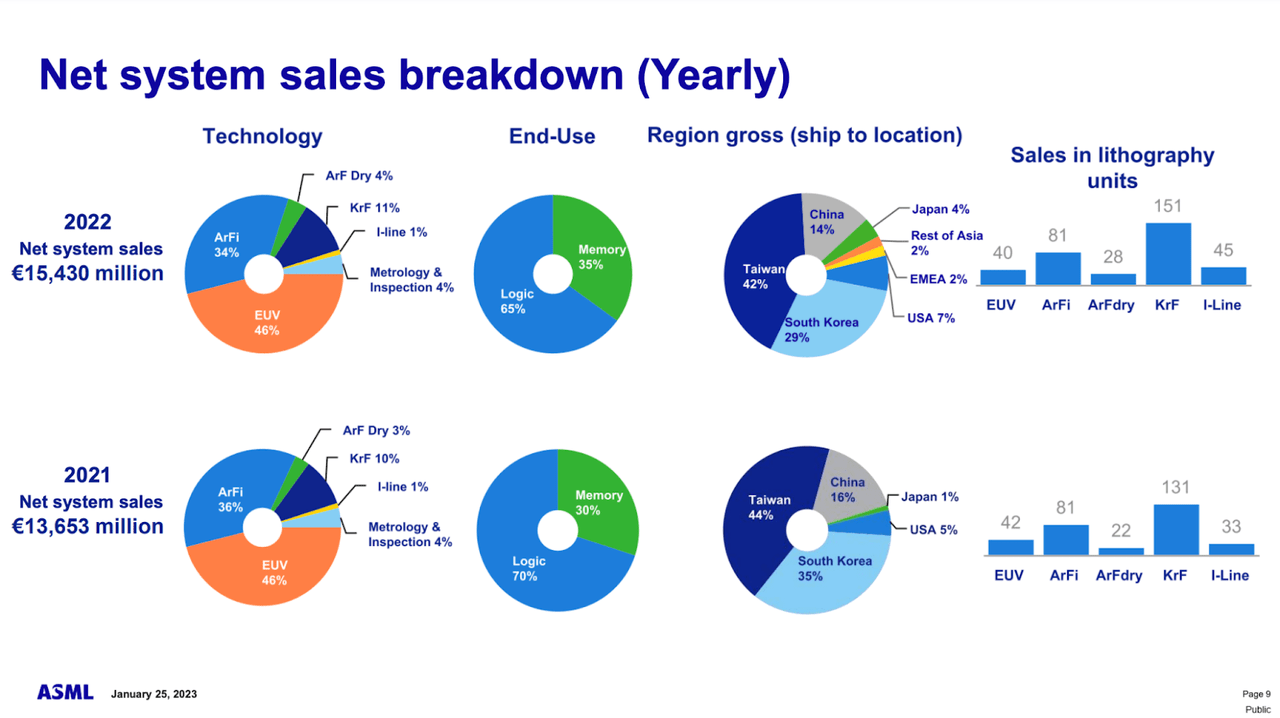

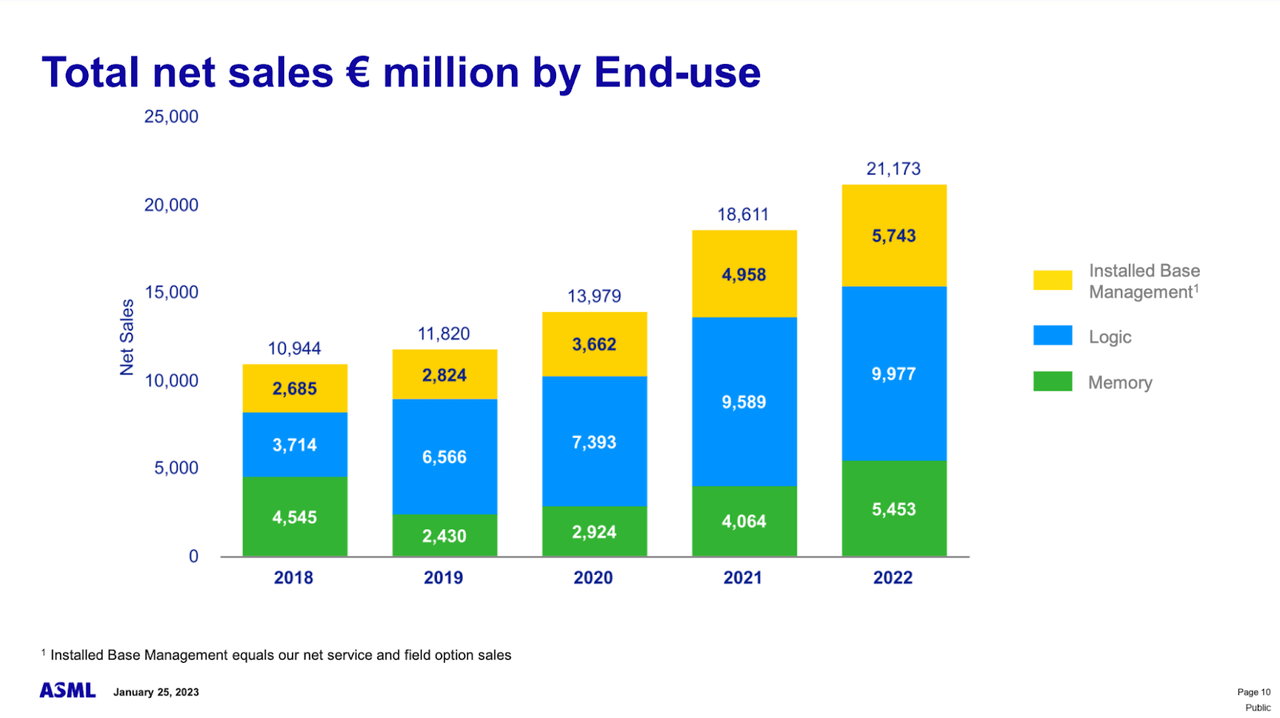

Net system sales grew 13% year over year and were distributed as follows across technology, end-use, and region:

ASML’s Q4 and FY 2022 Earnings Presentation

Note that net system sales should grow substantially in the coming years thanks to the capacity increase plans the company is undertaking and the continued rollout of EUV which carries a significantly larger ASP (Average Selling Price) than DUV and metrology and inspection systems.

We also found the following quote by Peter Wennink (ASML’s CEO) interesting:

Our metrology tools have a very strong attach rate to our DPV tools.

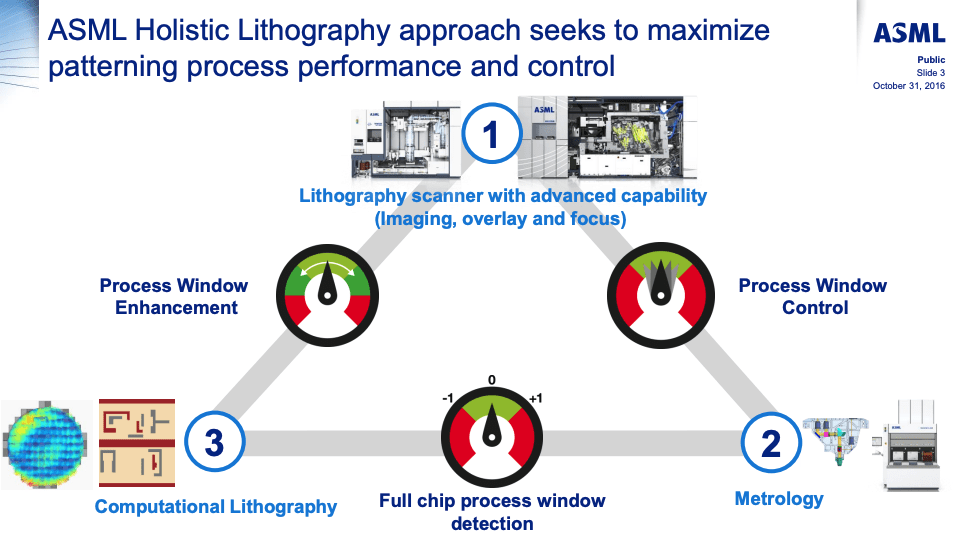

We have always believed ASML could enjoy an advantage in metrology and inspection systems over competitors such as KLA. The rationale is that ASML owns an essential part of the chip-making process (i.e., lithography), and it could use its large installed base to grow its metrology and inspection sales in pursuit of what management refers to as “holistic lithography”. The rationale is that it’s “easier” to get better yields if everything comes from the same company:

ASML 2016 presentation

Peter Wennink’s quote above, combined with the fact that metrology and inspection sales grew 28% in 2022 and are expected to grow at a similar rate in 2023, makes us think that we shouldn’t count ASML out of this market. KLA is a much larger company today than ASML’s metrology and inspection business (€660 million in sales) and it’s a very good company, however ASML seems to have opportunities to make inroads here.

Installed-based management sales grew 16% year over year, despite facing tough comps from last year:

ASML’s Q4 and FY 2022 Earnings Presentation

This segment’s sales are driven by a more extensive installed base and more complexity in the tools that ASML is rolling out, such as EUV.

It was a strong year on the revenue side for the company, but we should always try to look forward and assess the future demand for ASML’s tools.

The demand landscape: bookings and management’s comments

When we started researching ASML, the order book was crucial to our investment thesis. In our view, it was responsible for protecting and stabilizing the income statement, which should eventually help the stock remain stable and thus be worthy of being chosen as a Best Anchor Stock. We were right in assuming that the order book would protect the income statement. However, we misunderstood how the market would interpret the company’s fundamentals, as the stock has swung quite violently.

The thought process was that, if demand were to fall due to a semiconductor downturn (which eventually happens), ASML would be able to isolate its income statement by eating through its order book. Demand would fall, and cancellations or pushbacks would eventually come, but the order book was of such magnitude that we believed the semiconductor downcycle would be over before it was depleted.

Integral to this narrative was our belief in the resiliency of the order book, which was becoming increasingly tilted towards EUV (55% of the order book as of 2022 end). ASML’s customers are unlikely to defer their EUV investments because they fear losing technological leadership (nobody wants to be the next Intel). This quote by Intel’s CEO, Pat Gelsinger, during Intel’s Q4 earnings confirms this view:

We’re not going to diminish from the capital required for strategic leadership for the long term. So, strategic capital, largely unchanged.

Note that not even ASML’s worse performing customer is willing to defer such investments.

The thing is that ASML is currently supply constrained, so customers willing to defer a purchase are looking at 2024 or 2025 for shipment. One or two years doesn’t seem like a lot, but it’s a substantial amount of time in such a fast-changing industry. The bottom line is that these investments are strategic. For example, all 5 EUV customers have already placed orders for ASML’s high-NA EUV, expected in High Volume Manufacturing in 2025. Nobody wants to be left behind!

So, summarizing, the order book was large and safe (to an extent), paving the way to smooth fundamentals and strong protection against a semiconductor downturn.

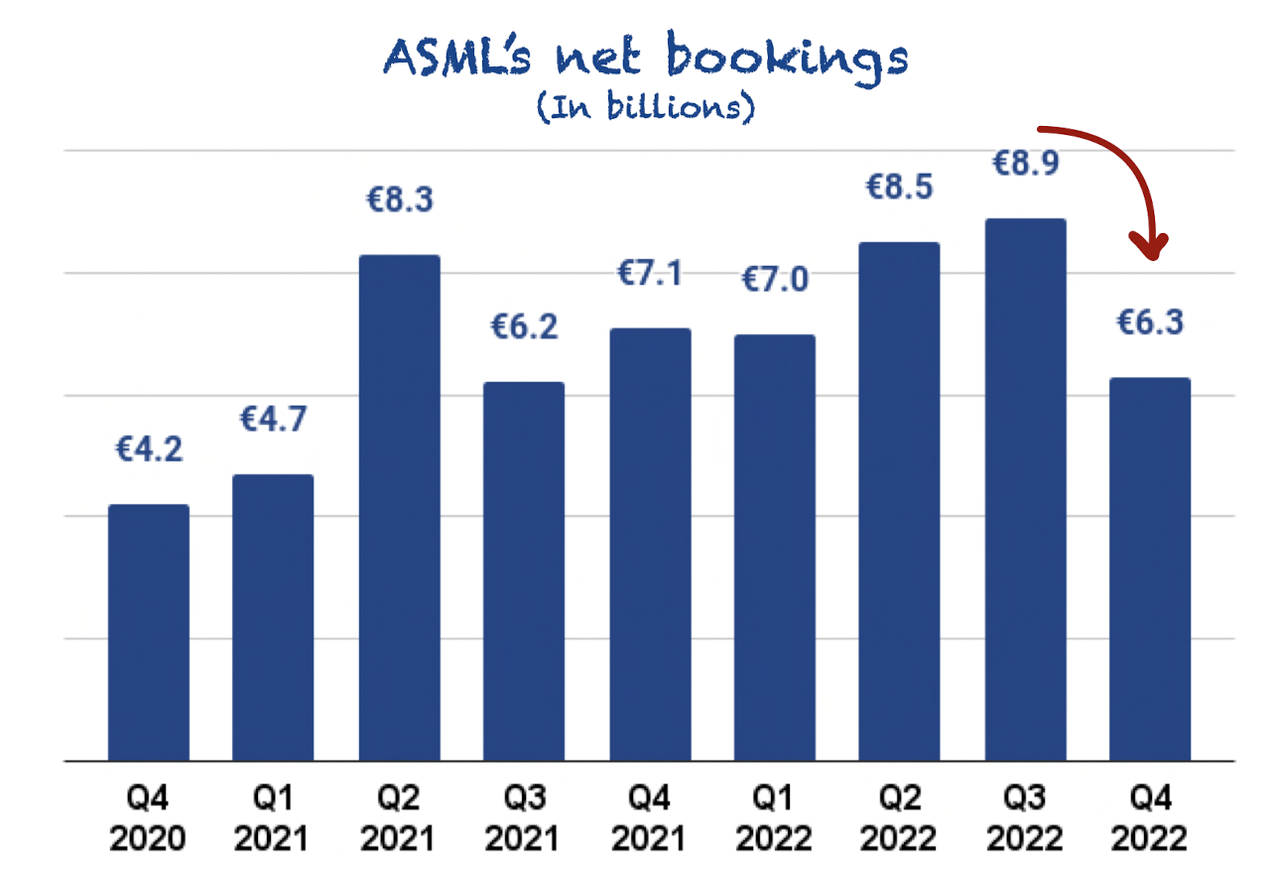

Now, what we didn’t have in our book (no pun intended) is that the order book would keep growing through the downcycle. ASML reported yet another quarter of net bookings at €6.3 billion:

Made by Best Anchor Stocks

Net bookings did come down compared to last quarter, but it was pretty naive to assume they would keep accelerating in a lower-demand environment. In fact, the normal scenario here would’ve been to see ASML eat through its order book as demand fell, not continue to see the order book increase!

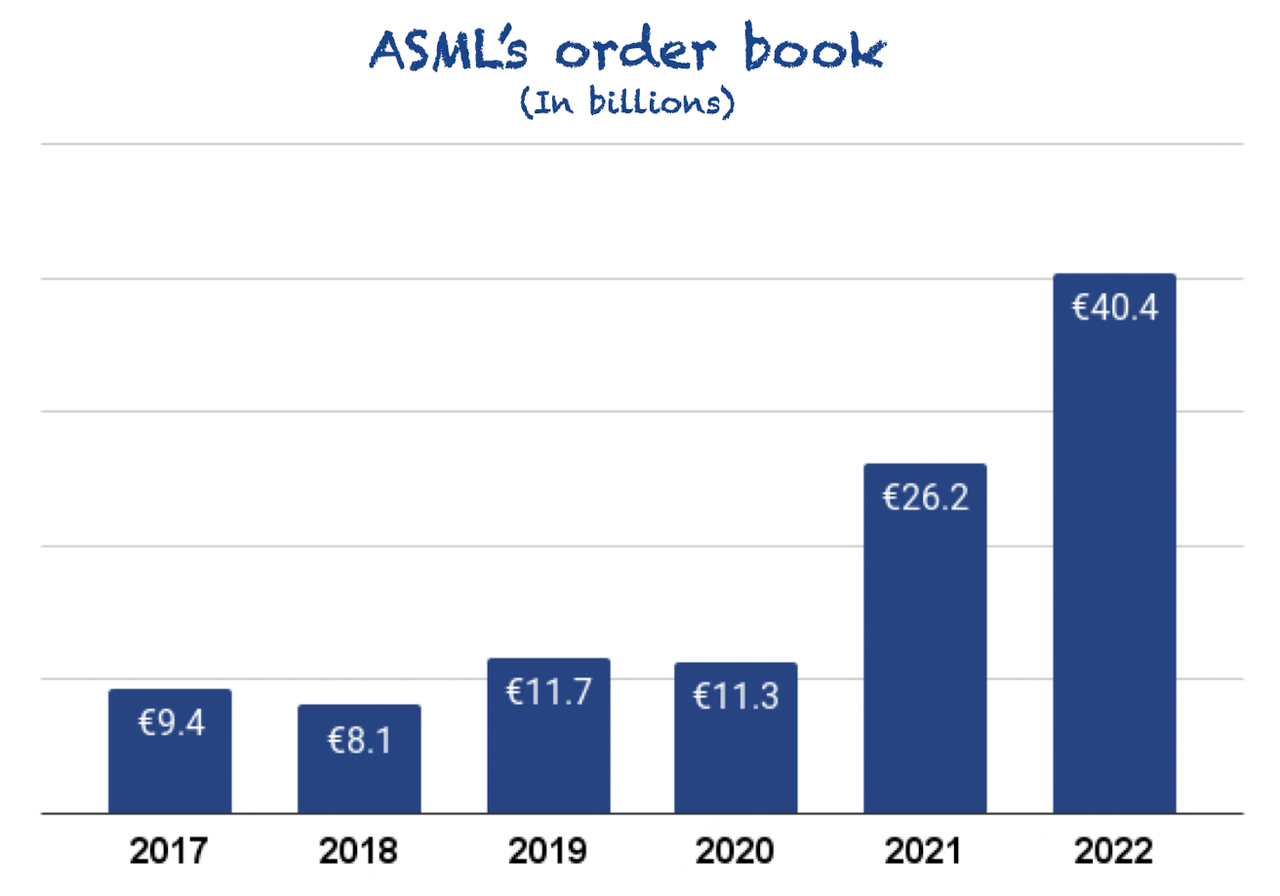

Increased net bookings during the quarter allowed the company to end the year with a record order book of €40.4 billion:

Made by Best Anchor Stocks

The interpretation of this number is straightforward: if ASML were to stop taking orders today, it would be able to recognize €40.4 billion in net system sales in the next couple of years. Note that no Installed Based Management sales are taken into account here, which would naturally grow due to a larger installed base. How many companies can say they are pretty confident they will recognize €40.4 billion in revenue in the coming two years without doing any more business? I’d say there are very few.

It’s also worth noting that bookings were restated upwards due to inflation. ASML’s management has been talking for a few quarters about sharing the inflationary pressures with customers. As a result, the company has slightly increased average selling prices, even on signed orders.

Of course, this ASP lift raises bookings. Investors who don’t consider this might be led to overstate the actual unit demand the company is seeing. It’s difficult to really measure the impact of these price hikes on the order book because we don’t really know how many orders it applies to. Still, we don’t think we have to believe the order book massively overstates demand, especially because price is another consideration in the demand equation. It’s also worth considering that now that the order book has already been restated, we should see true unit demand in the net booking numbers in upcoming quarters.

Peter Wennink, ASML’s CEO, did admit that demand has been dropping. Orders are now outpacing supply by double digits and not 50% as they were several quarters ago:

So now that has come down, but it’s still significantly double digit above our capacity. So — and like I said earlier in an answer to an earlier question, yes, of course, we also see the reflection of the demand curve because of the weakness in for instance, the consumer demand, Clearly, so some of that over demand has gone away, but it’s still there. And it was actually not 30%, it was more like 50%.

While demand is above supply capacity, we should continue to see the order book increase. However, if the opposite is true, we should start seeing ASML eat into it. If the semiconductor downcycle worsens, investors should be prepared for the second scenario. The market will probably dislike ASML eating into its order book, but it changes little of the long-term thesis in our opinion. Peter Wennink also referred to the expected resilience of the order book:

Most of our customers have made the assessment that the duration of a potential recession is significantly shorter than our average delivery lead time. On top of this, lithography investments are strategic in nature, which means that the demand for our systems remain strong.

So, all in all, despite lower sequential net bookings and management’s comments regarding lower demand, the buffer continues to be significant, and it looks highly likely that ASML will escape this semiconductor downturn without receiving any meaningful impact on its income statement. As for the long term, there’s nothing new to assume that ASML’s tools will not be in demand for many years to come. In fact, Peter Wennink claimed that customers are still very confident about where the long-term demand is going despite lowering the utilization of the tools over the short term to adjust to the demand environment:

You just lower the utilization of tools that short term, they’re very clear. It’s also very clear about their confidence in the long-term growth trajectory of the industry and have the need for significantly more semiconductors in all kinds of applications.

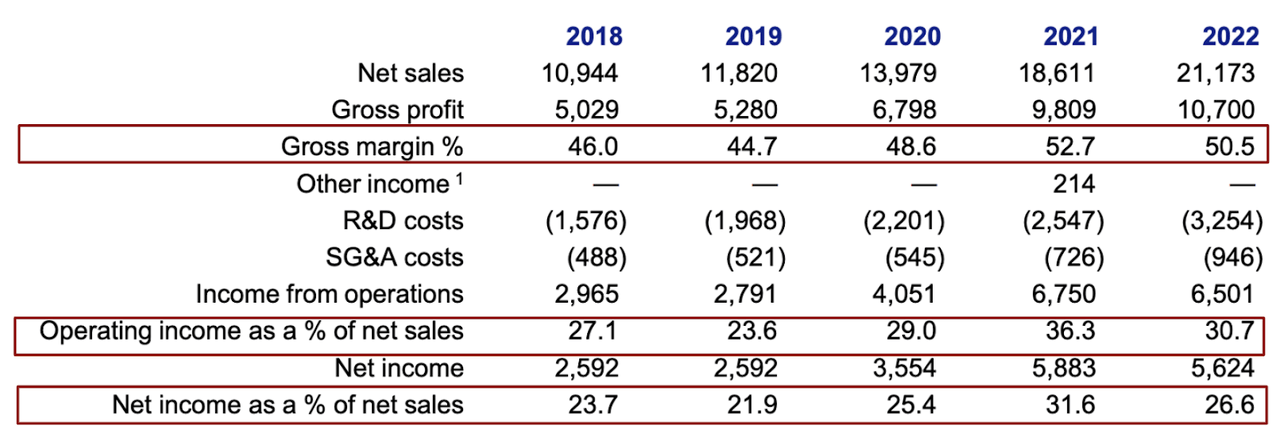

Breaking down profitability – Inflation and a return to a normal path

Margins for the year came significantly below 2021 numbers and there was margin contraction at basically every level:

ASML’s Q4 and FY 2022 Earnings Presentation

So, why did this happen? Well, our best guess is that 2021 was a year with somewhat inflated margins which set tough comps for 2022. There was also a substantially lower level of inflation in 2021 than in 2022.

From 2020 to 2021, the gross, operating, and net margins expanded by 410, 730, and 620 basis points, respectively. Several things caused this margin expansion, but surely the installed-based management sales surge played an important role because it typically carries a higher margin than system sales. The rationale behind the increase is that, in 2021, demand skyrocketed and ASML was supply-constrained, so customers turned to upgrades.

The margin contraction we saw this year just seems like a return to a more normal margin path as these tailwinds faded together with increased inflationary headwinds. Management did not share inflationary pressures in 2022 with customers, but that will change in 2023.

Besides sharing inflation, margins will enjoy several tailwinds to achieve management’s long-term guidance. This, in our opinion, is what matters, not how margins vary along the way.

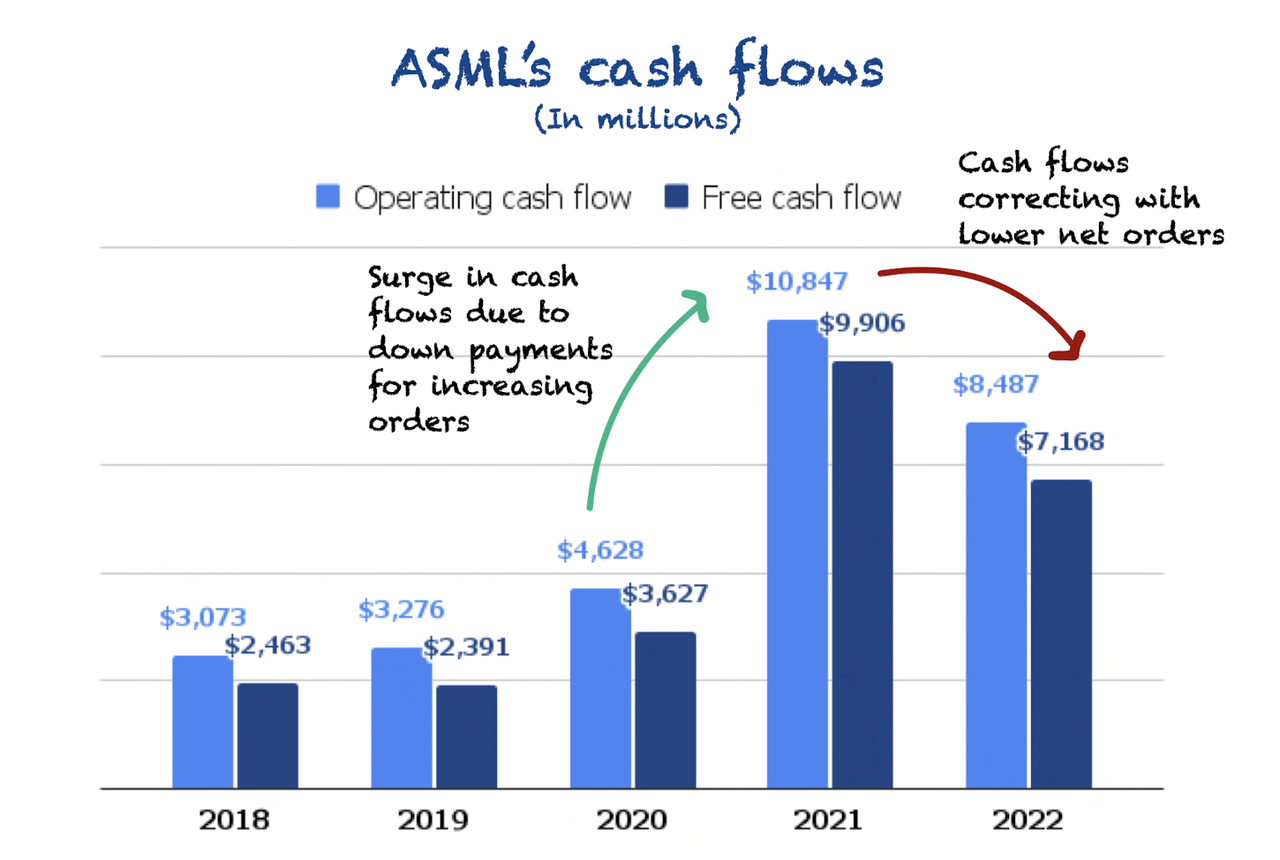

Some normalization in cash flows

Cash flows were substantial in 2022 but showed some normalization when compared to 2021:

Made by Best Anchor Stocks

The surge in cash flows in 2021 occurred due to customer down payments caused by a surge in orders. ASML has been supply-constrained for the last couple of years, so it has required customers to make payments (a portion of the tool’s price) before receiving the system. These payments have flown directly into the company’s cash flow and order book, but they will only be recognized as revenue (and therefore earnings) once the customer accepts the shipment in some future period. For this reason, cash flows are somewhat overstated and should normalize once order growth returns to a normal level.

This is also why investors should not look at ASML’s free cash flow yield to assess its valuation. We believe FCF will continue to correct in 2023 as orders fall. This said, the strong cash generation has strengthened ASML’s financial position. The company now has €7.3 billion in cash and short-term investments and €3.5 billion in debt.

The qualitative highlights

Will 2023 bring the end of fast shipments?

We have talked about fast shipments extensively in other articles. It’s the “method” ASML uses to ship systems to customers faster by doing all the necessary tests on the customer’s site rather than on ASML’s premises. The only “problem” with fast shipments is that ASML can’t recognize the revenue until the customer accepts (not receives) the shipment after testing it. Fast shipments have created a mismatch between what is recognized in revenue and what is actually shipped.

Some months ago, management announced talks with customers to close this “gap” by making them take ownership of the system once shipped, as the test phase was not adding much value (this should be especially true as systems mature and improve). Talks with customers are ongoing and management now believes 2023 could be the end of fast shipments:

Those conversations were now starting. Cannot tell you when that is done. In all likelihood, I would say, by mid this year, we should have clarity on whether customers are willing to do that or not.

Source: Roger Dassen, ASML’s CFO, during the Q4 earnings call

Note that it will not be an all-or-nothing scenario. What we mean is that some customers might accept the new way of operating while others might not. In the guidance section, we’ll talk about the implications of this change should it happen in 2023.

Not speculating around export bans to China

China was another hot topic during the earnings call, but management declined to comment much on it. There are rumors that the US might “push” the Netherlands to ban the exports of immersion DUV to China. While we do believe this will eventually happen, it’s all speculation at this point, and the uncertainty keeps management away from making predictions:

And it’s not that I want to talk about that. I don’t want to talk about China. I want to it’s no problem. What I cannot do is just tell you what the impact of the potential outcome is because I don’t know the outcome. That’s the only thing that — so I just don’t want to speculate. That’s the only thing.

Source: Peter Wennink, ASML’s CEO, during the Q4 earnings call

This is the correct take. We know people love to make predictions, but it’s better to wait for the facts in most cases.

In the worst-case scenario where ASML can’t export any system to China (note that this includes also dry DUV), that would wipe out 18% of the order book. It’s undoubtedly substantial but nothing that the existing buffer can’t absorb.

We should also consider geopolitics as a double-edged sword for ASML. Yes, sales to China might be hurt, but on the other hand, all the Chips Acts worldwide will probably make up for this and more due to increasing inefficiencies in the semiconductor supply chain.

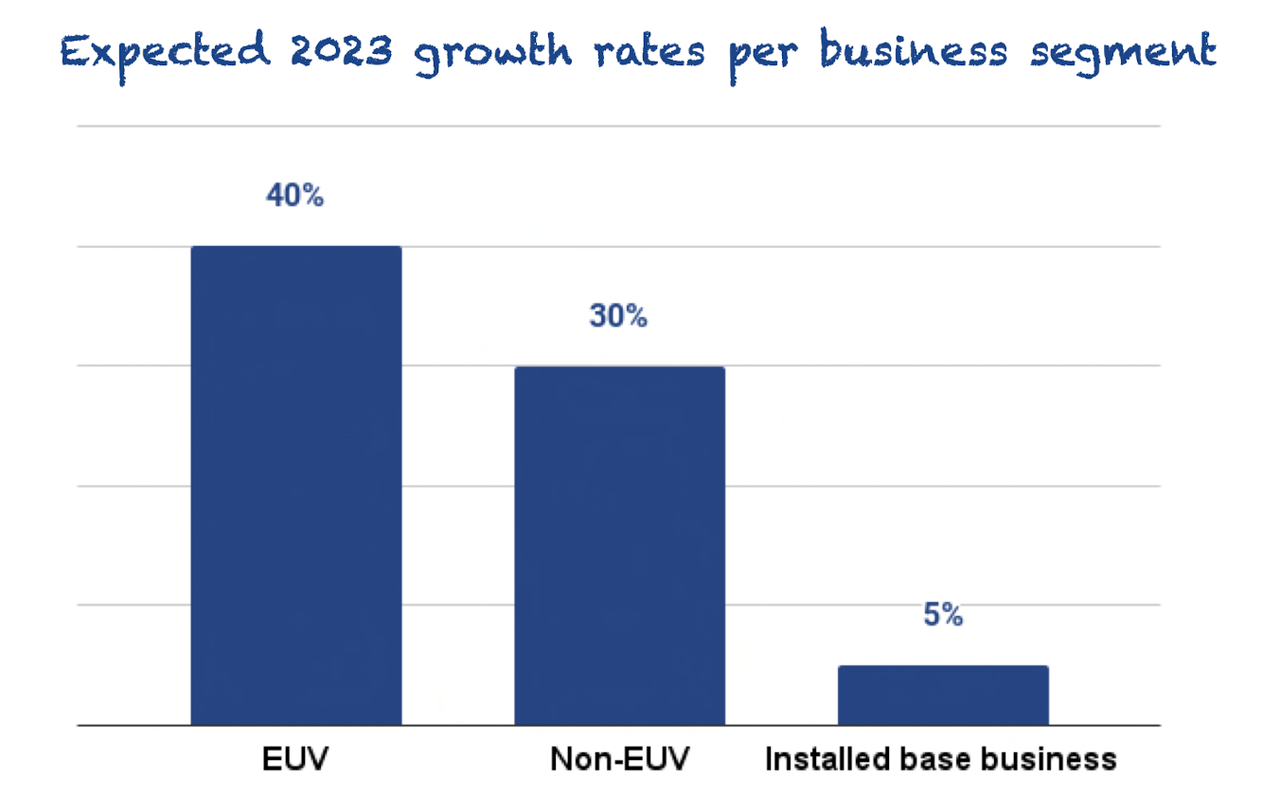

Guidance – Expecting a strong 2023

2023 guidance was very strong. Despite the existing semiconductor downturn, management expects sales to grow by over 25% this year. This growth will be divided as follows across the revenue sources:

Made by Best Anchor Stocks

The fact that EUV sales will continue to grow faster than non-EUV sales is excellent for two reasons. First, it reduces the dependency on sales from China because exports of EUV to that geography have always been banned. Secondly, it strengthens ASML’s moat as it’s the sole supplier of EUV. The world is shifting to leading-edge chips, and ASML will benefit meaningfully from this.

Note that this 25% sales growth assumes that around €3 billion in revenue will be deferred to 2024 due to fast shipments. If, as we discussed before, the company changes its revenue recognition policy this year and matches revenue with shipments, the company could grow its sales up to 39%!

This said, it’s unclear if all customers will adhere to the new policy. It’s also true that this will be a “one-time” benefit for the growth rate because it would be compared to a year that “suffered” fast shipments. However, once there are no fast shipments in any of the comparable periods, growth rates should normalize.

On the margin front, management expects a slight improvement in gross margins in 2023 and reiterated the long-term margin guidance given out during Capital Markets Day.

Conclusion

ASML had yet another great quarter. There are evident signs that demand is correcting slightly, but we believe the buffer is significant to absorb this, and orders will go back on their growth path once the semiconductor downturn is over. The company is indeed richly valued, but there are few companies with ASML’s revenue and earnings visibility and this surely deserves a premium in the market.

In the meantime, keep growing!

Be the first to comment