Back in September 2021, I called out Tesla (NASDAQ:TSLA) for being the original meme stock and alluded to the possibility of a reverse gamma squeeze. At the time, I did not expect such a move to play out so quickly (or if at all) and rather suggested a multi-year consolidation for the stock [at ~$250 per share (split-adjusted)] to allow for Tesla’s fundamentals to catch up to its valuation. However, a perfect storm has struck Tesla, and its stock is now in free fall.

During 2022, I covered Tesla multiple times – rating it “Neutral” up until mid-October (>$250 per share):

And then turning moderately bullish on the stock (in the low $200s), with the recommendation of slow accumulation over 6-12 months:

As interest rates climbed higher in 2022, a large majority of the tech universe has undergone a vicious valuation moderation, and so has Tesla. That said, Tesla’s business fundamentals have gone from strength to strength.

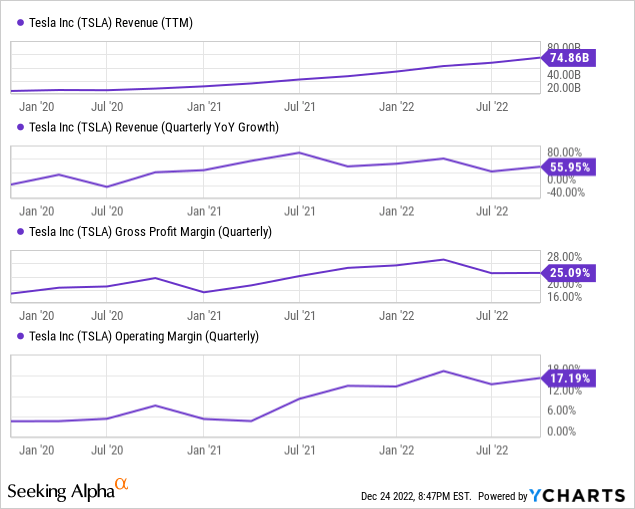

Over the last twelve months, Tesla raked in revenues of ~$75B with revenue growth of ~50%+. The transition to EVs (and sustainable energy in general) is still in the early stages, and as such, Tesla has a long growth runway ahead of itself. Currently, Tesla remains in hyper-growth mode, and its revenues are expected to grow at ~30-50% per year in the foreseeable future.

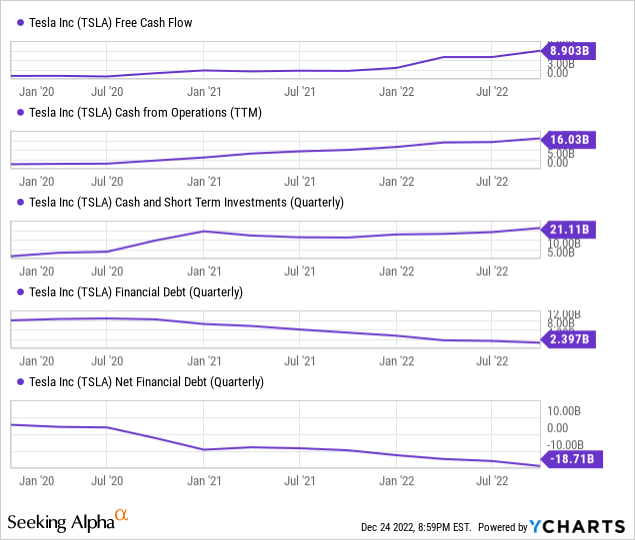

Asset prices are derived by calculating the net present values of their free cash flows, and hence, free cash flow (and growth thereof) is the most important metric for any business. Over the last twelve months, Tesla has hit record sales numbers and expanded margins. This combination resulted in free cash flow generation of ~$8.9B, which is an incredible figure for a company that was close to bankruptcy in 2018-19. As of Q3, Tesla held roughly ~$21.1B in cash & short-term investments. With little debt (~$2.4B), Tesla is now a cash-rich company (net cash position: ~$19B).

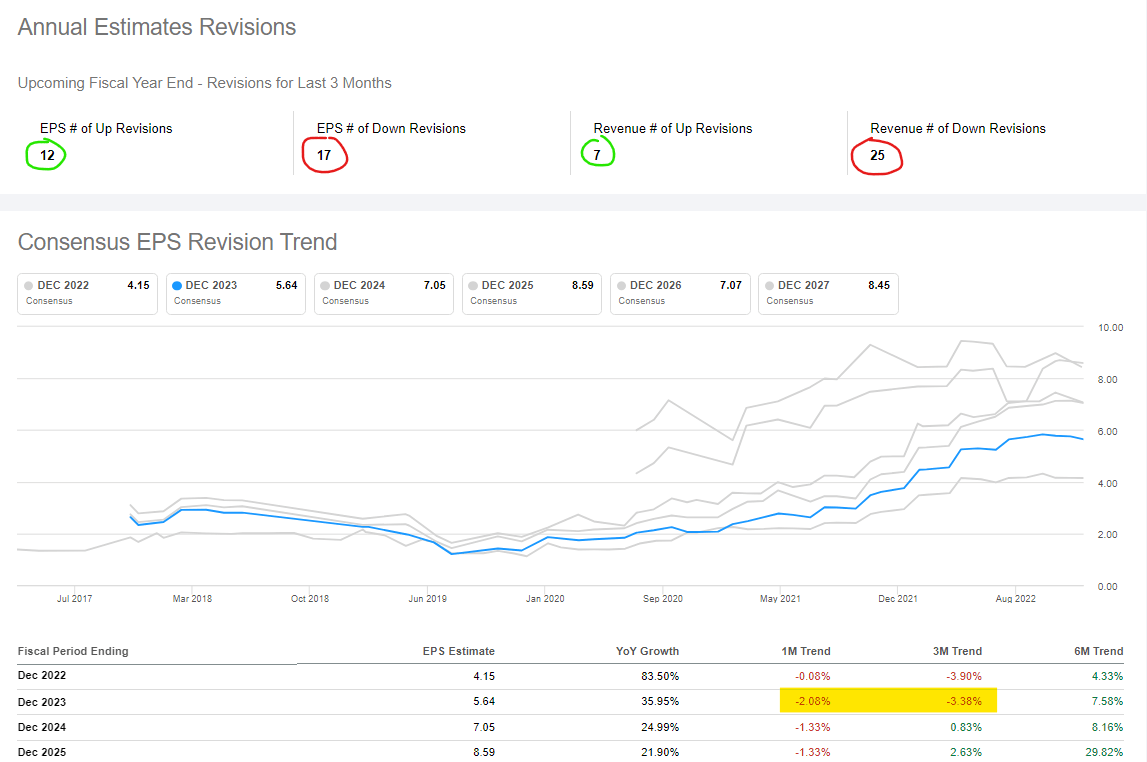

In recent quarters, Tesla has delivered record sales numbers with explosive growth in its business, and consensus analyst EPS estimates for Tesla have risen in tandem. While we are seeing a slight moderation in the estimates for 2023 in recent weeks, Tesla’s EPS estimates for next year are far higher than where they were just six months ago.

Seeking Alpha

According to my estimates, Tesla will rake in an EPS of ~$6 in 2023 (if there is no or mild recession [soft or softish landing]). For 2023, the consensus analyst EPS estimates for Tesla have started moderating in recent weeks, but this figure still stands at $5.575. Hence, Tesla is currently trading at ~20-22x forward earnings. At this multiple, a company projected to grow sales at a CAGR of 30-50% for the next five years is certainly cheap.

A combination of strong business fundamentals and significant valuation moderation turned me bullish on Tesla. And finally, after waiting for more than two years, I initiated a long position in Tesla at $155 per share on 15-16th December within TQI’s GARP portfolio. We will be building this position over the next 10-12 months in accordance with our DCA plan.

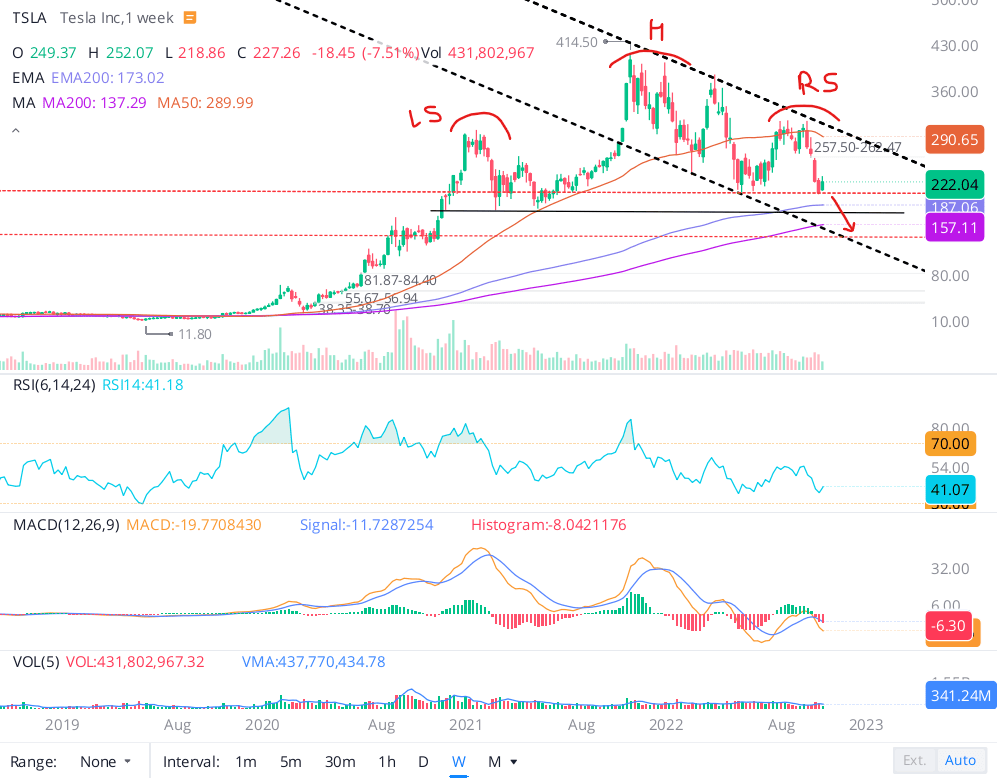

If you have followed my work on Tesla, you know that I have been harping about the need for slow accumulation in this counter. For those looking for an explanation, here’s an excerpt from one of my previous notes (before the breakdown of Tesla’s H&S pattern):

On Tesla’s chart, we are now looking at the potential breakdown of a bearish “Head and Shoulders” pattern, which could mean a quick ride down to the mid-100s (even low-100s is possible). The prospect of a reverse gamma squeeze in Tesla is real, and despite my switch to a bullish stance for Tesla’s stock after considerable valuation moderation, I urge investors to proceed with caution. For anyone looking to buy Tesla for the long term, I see slow accumulation as the right strategy. However, if you are looking for a short-term buy, just skip Tesla for good.

Tesla chart 20th October 2022 (WeBull Desktop)

After undergoing months of painful correction, Tesla’s stock is finally undervalued; however, given current market conditions, it may very well overshoot to the downside. A bearish post-ER price move indicates that Elon Musk’s positive commentary around [50% CAGR] revenue (volume) growth, [$5-$10B] stock buyback, [best-ever] product roadmap, and Tesla’s future valuation [$4.5T = Apple + Saudi Aramco] has failed to paper over the evident cracks (albeit small misses) in Tesla’s Q3 report. That said, Tesla just reported yet another record-breaking quarter and is set to create new records in Q4. As a long-term investor, I view Tesla’s Q3 miss as nothing but short-term noise.

From a long-term perspective, Tesla is one of the strongest earnings growth stories in the market. And now that Tesla is undervalued, investors shouldn’t pass up on this fantastic company. Considering the rising probability of an economic recession and Tesla’s precarious technical chart (showing a ‘Head & Shoulders’ pattern), I think slow accumulation is the way to go here. As I have said in the past, the low-200s seem like a reasonable entry point in Tesla for long-term investors. If we do see Tesla break down to the mid-100s, I think that would be a great buying opportunity.

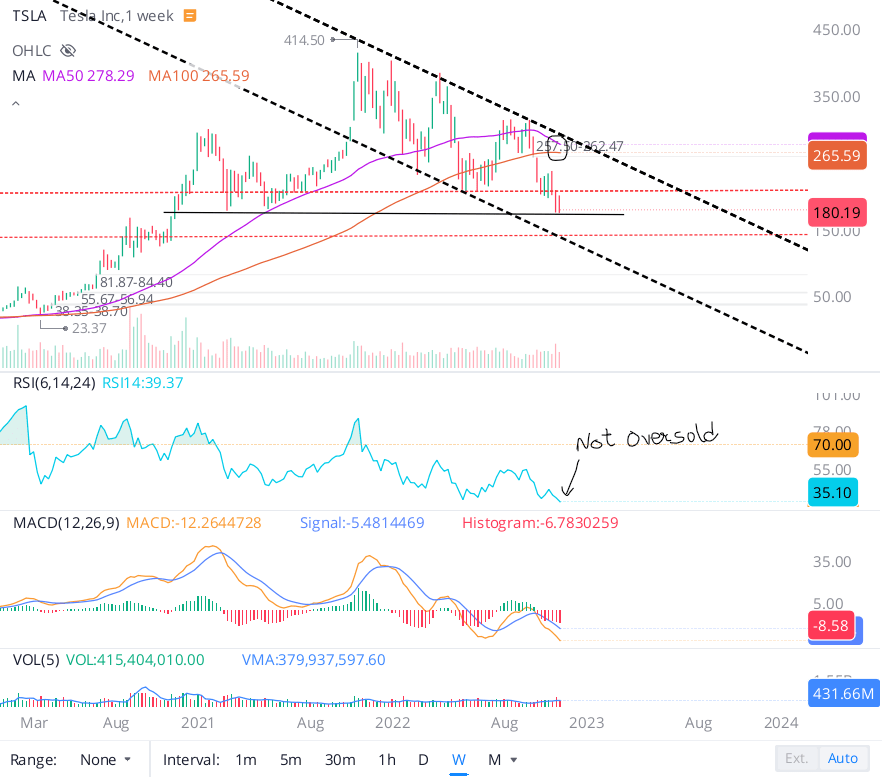

And here’s what I said after the breakdown of Tesla’s H&S pattern:

Tesla has one of the worst technical charts in the equity market right now, with a confirmed breakdown of the bearish head and shoulders (H&S) pattern pointing to even more downside from here.

Tesla Chart 21st November 2022 (WeBull Desktop)

The next big support is located on the lower trendline of the falling wedge pattern Tesla has been trading in for months, and that level is ~$140. If a reverse gamma squeeze were to materialize, I think even the low $100s are on the table for Tesla. With this precarious technical setup, buying Tesla as a near-term trade (<12 months) is simply out of the question. And any long-term investor buying here should be prepared for high volatility in this counter.

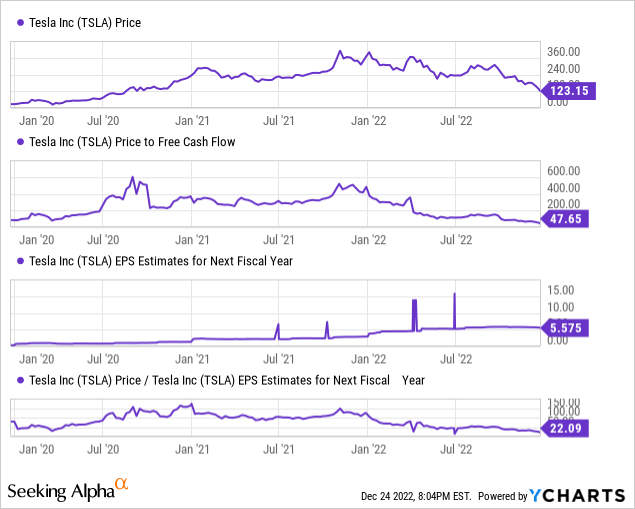

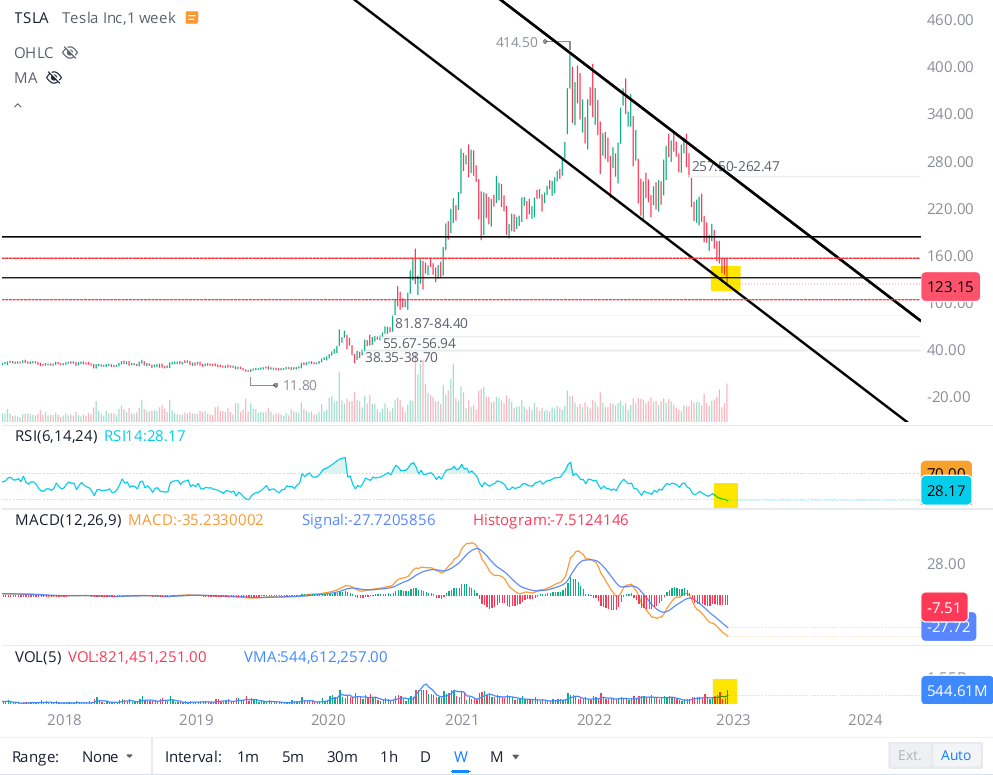

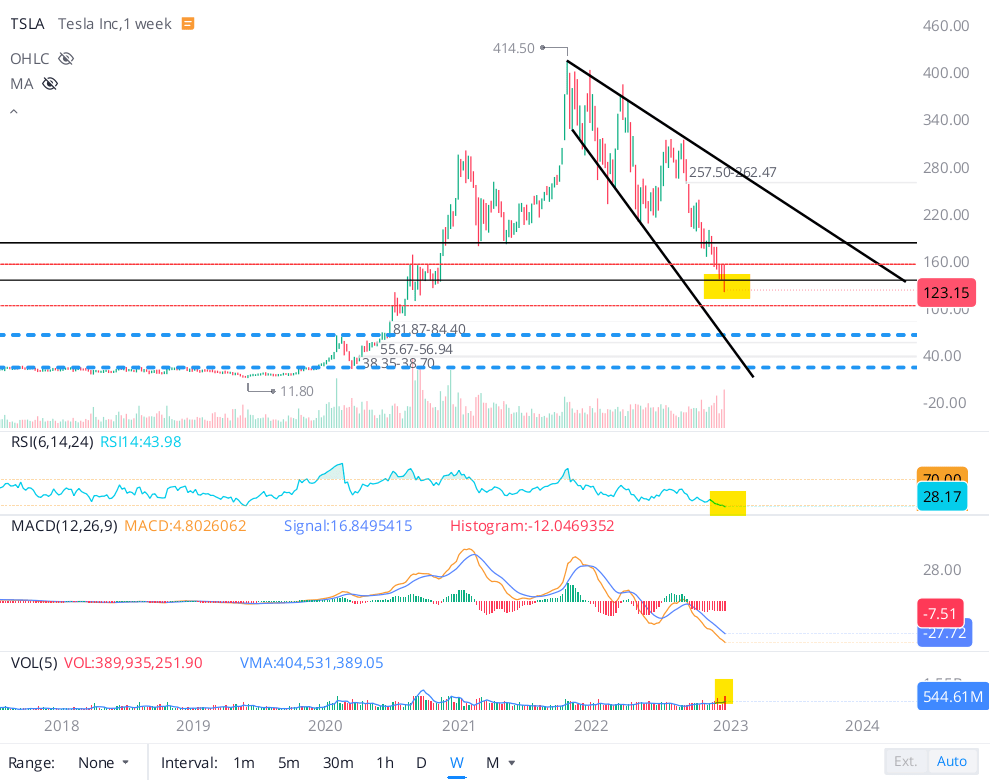

As of the close on 23rd December 2022, Tesla’s stock was trading at $123.15 per share, down ~20% for the week with heavy volumes. The rapid deterioration in Tesla’s market capitalization reeks of capitulation amid a flurry of margin calls. In this note, we will discuss the ongoing reverse gamma squeeze in Tesla and the factors that could continue to drive this move to the downside.

A Perfect Storm Rocks Tesla’s Bubbly Stock

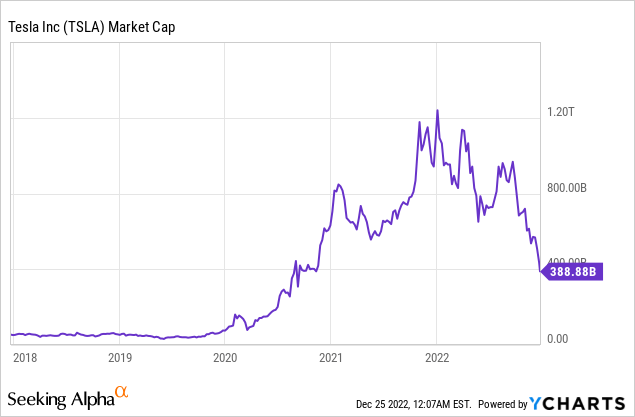

At its peak, Tesla’s market cap reached $1.23T in Nov-2021. Since then, Tesla has lost nearly 70% of its value, and in all fairness, this move is akin to the popping of a bubble. So what pricked the bubble in Tesla’s stock? While there’s been a lot of noise around Elon Musk, Twitter & China, if I had to pinpoint something, I would go with Fed’s pivot to quantitative tightening in the back end of 2021.

With the Fed raising interest rates and reducing its balance sheet (pulling liquidity out of the economy) to fight against inflation, trading multiples have been normalizing across the technology universe in 2022 and Tesla is the poster child of this move.

In mid-2021, I said that Tesla was the original meme stock, and a gamma squeeze is what propelled Tesla to an astronomical valuation of $1T+:

Even before the meme stock craze became a thing in late 2020, Tesla’s stock was trading in a similar vein to the likes of GameStop (GME), AMC Entertainment Holdings (AMC), and other such “meme” stocks. Tesla has been a retail favorite for years, and Tesla’s fanboys have hit the jackpot with their investments in the company. In just a short space of twenty-four months, Tesla’s stock has rallied by nearly +1500% (or 16x). Tesla’s rise hasn’t been as rapid as what we have witnessed with GameStop or AMC; however, it certainly resembles a typical squeeze, and the move up could have taken longer due to Tesla’s scale.

Tesla’s business fundamentals have been improving consistently over the years; however, I believe that the primary driver of Tesla’s stock is an absurd trading multiple expansion from ~2x P/S to ~20x P/S based on irrational market exuberance spurred on by a combination of factors such as short unwinding (Tesla’s Short Interest has gone down from 218M shares [30% of float] to 27.5M shares [3% of float] after peaking in May 2019), gamma squeezes (retail investors [fanboys] buying OTM calls), addition to SP500 (forced index buying of more than $100B), etc.

Tesla now commands the valuation of a high-margin SaaS business (which it clearly isn’t). In all fairness, Tesla is a capital-intensive, low-margin automotive business, which has the potential to become a SaaS-like company someday. In recent times, several analysts have lauded Tesla’s move to offer FSD as a monthly subscription service (at $99 a month for Enhance Autopilot customers and $199 a month for others); however, they fail to mention that Tesla’s subscription offering comes at the cost of a $10,000 upfront payment. To be fair, I do expect the subscription service to be a success; however, it is unlikely to be a game-changer for Tesla (unless full autonomy is achieved).

Tesla has a massive growth runway in front of itself with clear product and technology lead expected to result in rapid growth over the next decade. However, the price investors are being asked to pay for Tesla (Price to FCF ratio of ~330x) is completely out of whack with reality. As you may know, rapidly growing, high-margin businesses tend to trade at premium valuations; however, I have never come across any situation quite like this one. I would like to reiterate, Tesla is not a high-margin SaaS company, and even if it can be one, the current multiple being asked for it is not in touch with reality. The high-growth universe has many better alternatives for capital allocation, and buying Tesla at this valuation makes little sense for investors seeking alpha.

The forces that propelled Tesla’s stock higher are now acting against it, and by forces, I am primarily referring to the trillions of dollars of monetary and fiscal stimulus that global central banks and governments pumped into the economy during 2020-21. With the Fed tightening aggressively into a deeply inverted yield curve, a richly valued equity market faces the double whammy of a multiple contraction and an earnings recession in 2023. While a recession is never a certainty, it is getting likelier with each passing day as the impact of tighter monetary policies from central banks is felt across the global economy.

Blaming the Fed for Tesla’s stock price decline is easy, and this is exactly what Elon Musk has been doing on Twitter recently. And while he is not entirely wrong, I think a confluence of factors is affecting Tesla’s stock right now. And these factors include – Elon Musk’s Twitter antics & his use of Tesla shares to finance Twitter, a potential demand problem, and Musk’s scary recession strategy.

Before we talk about the factors driving the ongoing capitulation in Tesla’s stock, let’s check its technical chart:

After a rapid decline in its stock price over the last month, Tesla is now trading at the lower trendline of the falling channel pattern we have observed over the last several months. With an RSI of 28, Tesla’s stock is oversold and ripe for a bounce in the near term.

WeBull Desktop

As the sell-off intensifies, trading volumes are picking up, with the ongoing move in Tesla’s stock reeking of capitulation. Tesla is a big retail stock, and its price action is indicative of a flurry of margin calls. On the chart, I also see a megaphone pattern, and a breakdown of the lower trendline of the falling channel would make me re-draw the lines. If Tesla’s stock were to hit the lower trendline of the megaphone pattern, we could be headed down to mid-double digits.

WeBull Desktop

Looking at the rapid decline in Tesla’s stock price, I think a reverse gamma squeeze is playing out, with traders piling into out-of-the-money put options to bet against Tesla. While a test of the low $100s seems like a foregone conclusion at this point, a breakdown of these levels could send the stock plunging lower to pre-pandemic levels in the $60-65 range (and even lower) in 2023. Despite Tesla’s strong financial performance, its stock is nosediving lower as if there’s no tomorrow. So, what’s driving this price action?

Let’s look at three major factors affecting Tesla right now:

1. Musk’s Twitter Antics & Insider Selling

Tesla’s history is filled with drama; however, ever since Elon Musk decided to buy Twitter, the noise around Tesla has escalated to another level. With Musk being distracted by Twitter, the perception of him sleeping at the wheel for Tesla is growing among his investor base. Even long-term supporters are worried about Musk’s obnoxious behavior on Twitter, with his political commentary damaging Tesla’s brand and alienating its customer base.

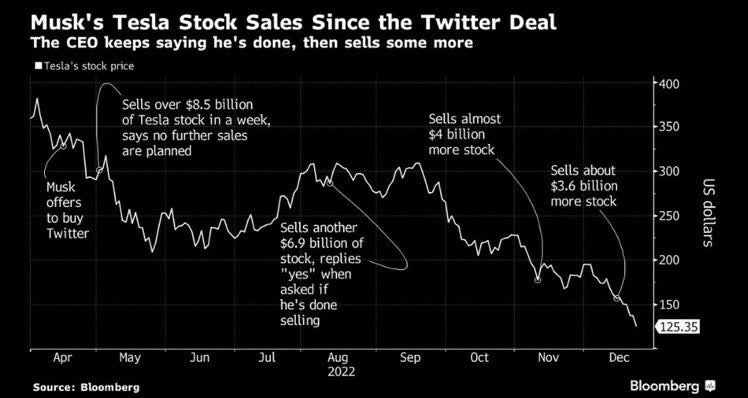

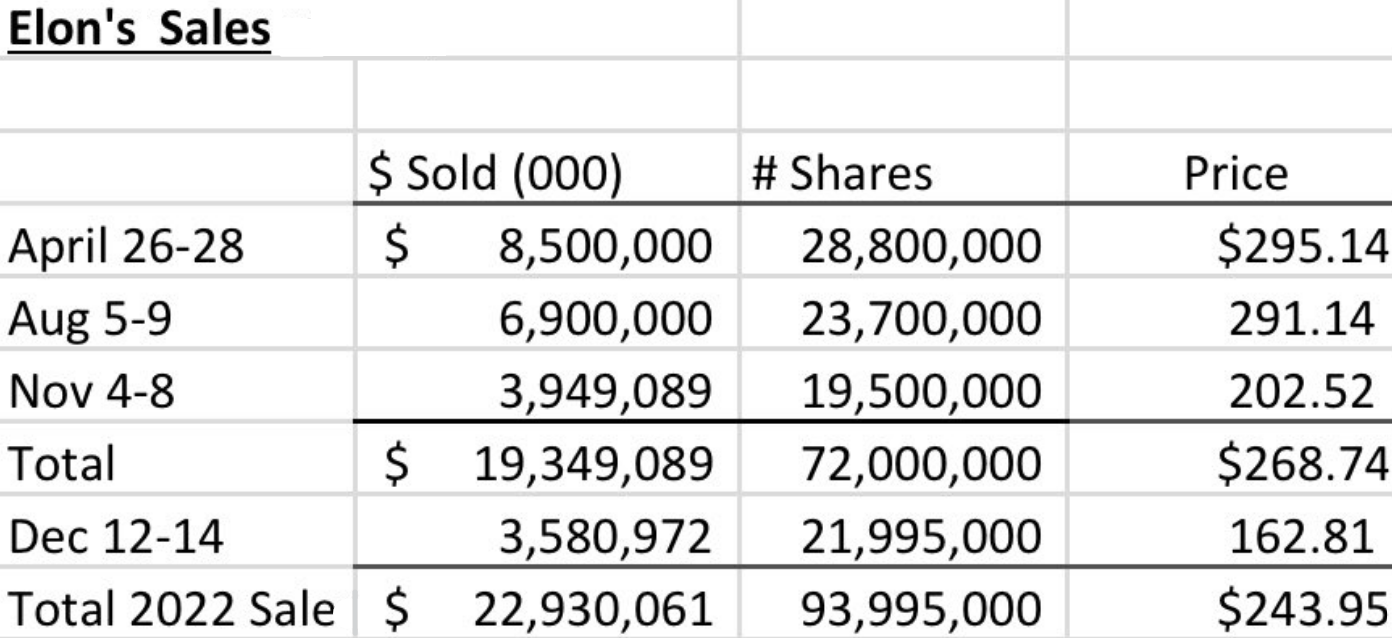

In the past, we have talked about Tesla being a religion to many of its uber-bullish investors. However, faith is being tested now that the leader has sold nearly $40B worth of Tesla shares over the last couple of years.

Twitter

Since making a $44B leveraged buyout offer for Twitter in April, Musk has dumped nearly $23B worth of Tesla shares, and his sales are creating downward pressure on Tesla’s stock price. After each round of selling, he has said that there will be no further sales, but so far, that’s been a lie each time.

Twitter

Twitter

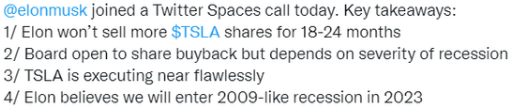

Last week, Musk joined in on a Twitter Spaces session and delivered quite a show. He not only committed to no further stock sales from him for the next 18-24 months, but he also predicted a 2009-like recession in 2023.

Twitter

Unfortunately, I can’t trust Elon Musk on his “no further sales” comment after him making such promises all year only to sell more shares.

Recently, Musk has been very vocal about an impending recession and shared some wise words on the All-In podcast:

I would really advise people not to have margin debt in a volatile stock market and you know, from a cash standpoint, keep powder dry. You can get some pretty extreme things happening in a down market.

Ironically, Elon Musk is a highly-levered, cash-poor billionaire who has pledged millions of Tesla shares as collateral for margin loans. Fortunately, Musk’s recent sales are meant to provide him with dry powder if things get rough. But will $3.6B be enough? I don’t know.

As of Dec-2020, Musk had 92 million Tesla shares pledged as collateral, according to an SEC filing in April 2022. The real-time count for Musk’s pledged shares may be far greater since he used borrowed funds to get Twitter. The one major fear in my mind is his personal leverage causing forced selling. As Tesla’s stock price sinks lower, Musk could get margin-called on his loans, and all those pledged shares could flood the market when buyers are out of liquidity (during a recession).

From Tesla’s risk factors:

Tesla Q3 2022 10-Q filing

Such an event could lead to a massive capitulatory bottom in 2023. How low could Tesla go in such a scenario? I don’t know, but we could probably revisit the pre-pandemic levels. Such a capitulation would mark the completion of an epic reverse gamma squeeze.

While I don’t think such a move will necessarily materialize due to Tesla’s robust business fundamentals and immense growth potential, the market could do extreme things in a panic situation. The EV transition will be a strong secular growth trend for years to come, and Tesla is the undisputed leader. From a long-term perspective, Tesla looks attractive at current levels; however, the near-term picture is quite uncertain, with a potential recession on the horizon. And Musk selling shares after Tesla’s stock was down ~60-65% speaks volumes. Is there something Tesla’s CEO sees in the internal company data that we aren’t privy to?

2. Demand Concerns Are Mounting

While Musk’s Twitter antics and obnoxious stock sales are playing their part, the biggest driver of the ongoing capitulatory sell-off, in my mind, is the worsening macroeconomic environment. With the Fed raising terminal rate expectations to 5.1% and re-iterating intentions to hold rates higher for longer, consumer demand is likely to slow down. And with Gigafactory Texas, Berlin, and Shanghai scaling up production; Tesla could face a demand crunch in the event of a recession next year. Looking at the discounting activity (in China and here in the US), Tesla could already have a demand problem.

According to news reports, Tesla has cut prices in China five times in recent weeks due to weaker-than-expected sales and just last week halted Model Y production at Gigafactory Shanghai earlier than planned. We know that Tesla’s Q3 deliveries fell short of expectations, and analysts have been cutting their forecast for Q4 too.

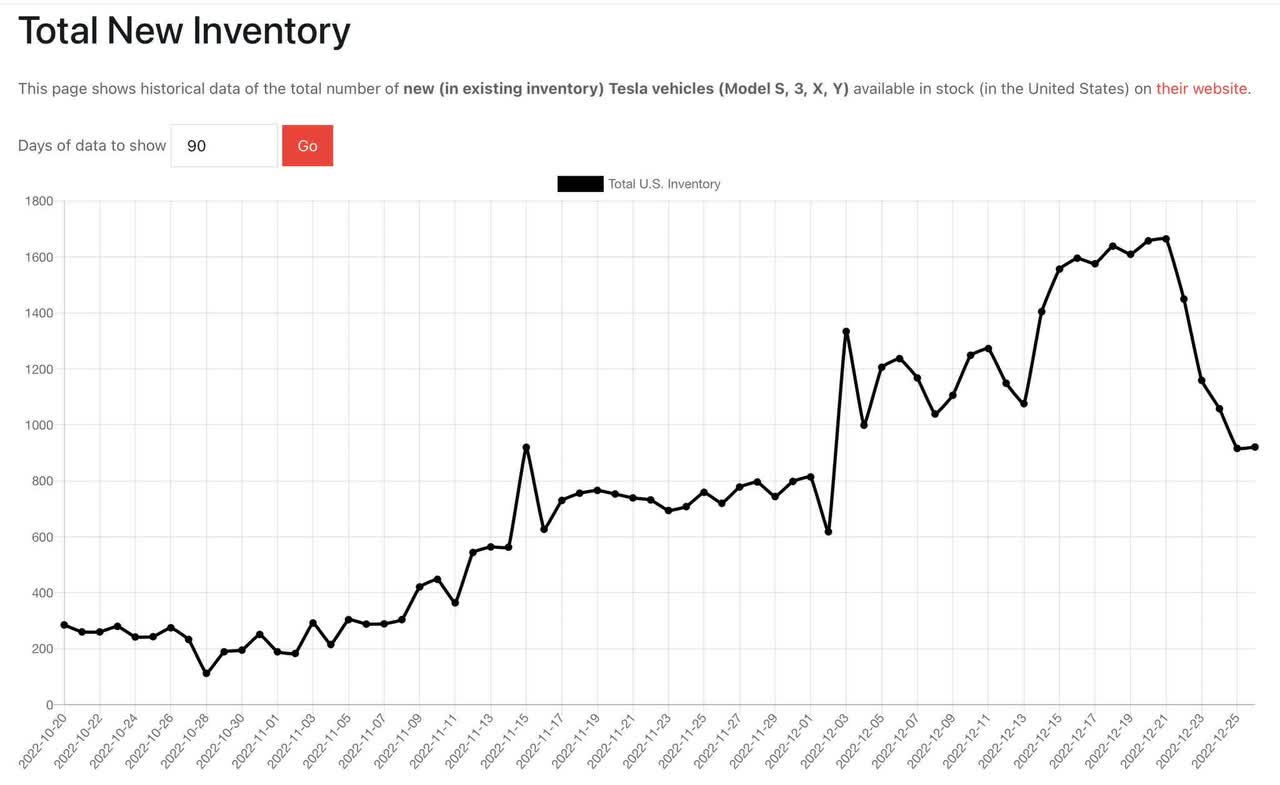

In the US, Tesla’s inventories had been rising as customers were waiting to take deliveries due to the EV tax credit (up to $7,500) not going into effect until the new year. Again, Tesla cut prices (first by $3,750, then raising the discount to $7,500) to boost demand.

Twitter

For now, price cuts seem to be working as Tesla’s inventory levels in the US are normalizing rapidly. However, such price cuts will hurt Tesla’s margins. With the macroeconomic environment set to get worse, Tesla’s demand could decline drastically. Historically, the auto industry has been cyclical, and Tesla has virtually no experience in navigating a recession.

Taking a longer-term (3-5+ year) view, I am bullish on Tesla’s business prospects. Here’s why:

Tesla is a disruptive company that’s leading the world’s transition to sustainable energy. The EV transition is still in its early innings, with only ~5% of all auto sales in the US in 2022 being EVs [long runway for growth].

One of the big bear thesis for Tesla is that massive competition (from new entrants and traditional automakers) is coming in the next couple of years and that if a recession strikes, Tesla will suffer a demand crunch. In the event of a recession (mild or severe), heavily-indebted traditional automakers are going to be hurt far more than Tesla, and I think they will need to moderate their EV ambitions, letting Tesla extend its technology lead even further.

With governments pushing for a transition to sustainable energy, EV adoption is going to increase over the next decade, regardless of a recession in 2023. And hence, even if Tesla loses market share to competition (EVs from new entrants and traditional automakers), I can see Tesla growing revenues at 30-50% per year for the next five years. With new products like Semi and CyberTruck entering production next year along with scale-up at Texas and Berlin Gigafactory, Tesla should be able to meet its production goals of ~2.1M vehicles (based on a 50% y/y growth target) for 2023. Yes, the demand concerns are warranted due to a challenging macroeconomic environment, but since the EV transition is still in its early innings, Tesla should be able to grow through this recession.

While bears may disagree, Tesla is not just a car company. I think Tesla is a battery, energy storage, robotics, and software company that happens to make cars. The long-term outlook for Tesla’s business is as bright as ever, and the company has ample firepower to get through a recession.

3. Musk’s Recession Playbook Spells Bad News For Tesla’s Shareholders

On the Twitter Spaces shared above, Elon Musk also shared Tesla’s plan for navigating the upcoming recession. As per Musk, Tesla will sell cars at cost price to boost unit sales if demand evaporates in a severe downturn. The idea is to potentially make money from upselling FSD (autonomous driving) software to its customers when the technology becomes available.

Twitter

Most of the speakers in this Spaces session seemed excited about this strategy; however, I am convinced that if this playbook is implemented, Tesla’s earnings will collapse next year due to aggressive pricing actions. And consequently, the stock will decline too. Why am I so sure?

Well, because I have seen this playbook wreak havoc in multiple stocks this year. One such stock I own is Roku (ROKU). In the post-pandemic world, Roku chose to drive new account acquisition by selling its hardware below cost. The idea was to make up these small losses through advertising profits. While user growth and engagement numbers have held up quite well, Roku’s margins have come under pressure. With the macro environment having an adverse impact on Advertising spending, Roku is hurting right now.

And the result of this strategy is clear and obvious:

WeBull Desktop

Roku’s stock is now trading well below its COVID-lows. The long-term opportunity for Roku still exists, and this is a company that will continue to grow at a healthy pace for years to come. However, Mr. Market has no patience for companies not making money right here, right now.

I am not saying Tesla’s cars are like Roku TVs (or streaming sticks), but in a poor macro environment, consumers are unlikely to pay up an additional $10-15K for FSD (before autonomous driving is actually available). And Tesla has still not achieved full autonomy (the ink is not ready). If Tesla were to start losing money on its cars again, the stock could be in for a de-rating lower, and any valuation-based floor will simply disappear. And this is something Tesla bears like Danny Moses (big short fame) are celebrating.

Twitter

In a nutshell, Tesla’s near-term demand outlook is highly uncertain, and Elon’s plan for navigating a recession is scary. If Tesla’s earnings collapse in 2023, the ongoing reverse gamma squeeze in Tesla could continue in the upcoming weeks and months. My long-term view on this business is unchanged, and here’s how I value Tesla today.

Tesla’s Fair Value And Expected Returns

At this point, I think we will end up in some kind of a recession in 2023; however, the depth and duration of this recession would depend on how much pain global central banks are willing to unleash upon us. If we only experience an economic slowdown (no recession) or a short and shallow recession, Tesla should be able to ride it out with relative comfort (many of its rivals won’t). The following model is built with a long-term view of Tesla (and doesn’t account for a severe recession [or depression]):

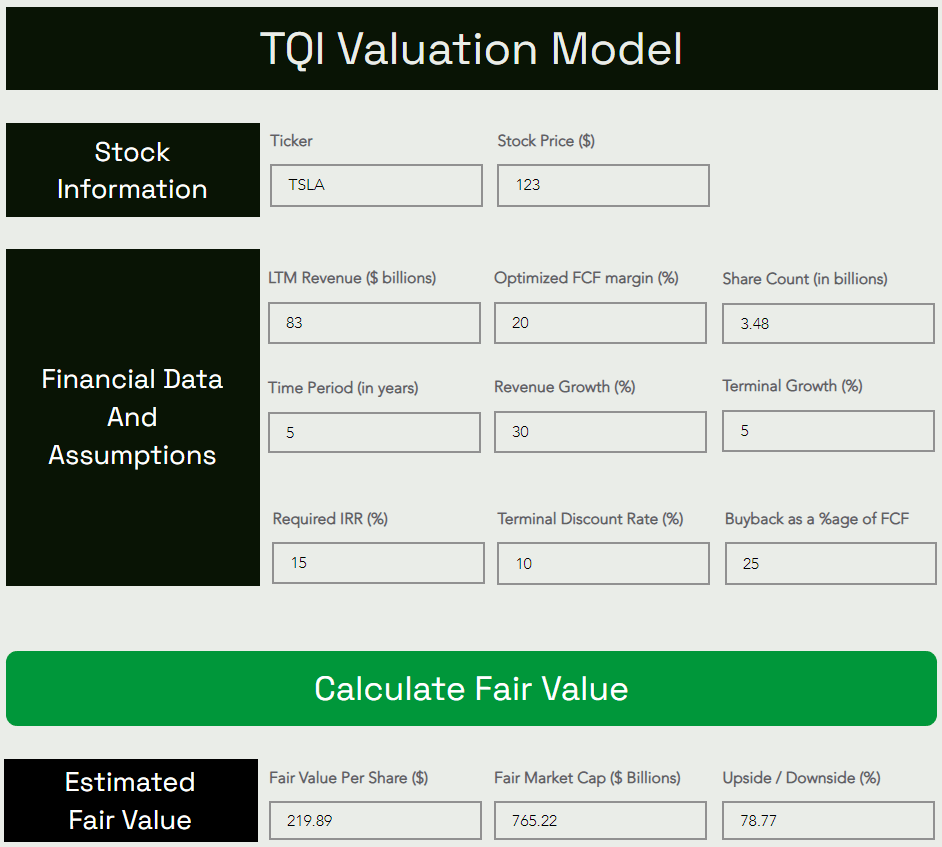

TQI Valuation Model (TQIG.org)

According to my analysis, Tesla’s intrinsic value is ~$220 per share. This means Tesla is now undervalued by ~44%. As we discussed in the past, Tesla is overshooting to the downside (and there could be more room to fall)!

Now, let’s look at expected CAGR returns for the next five years.

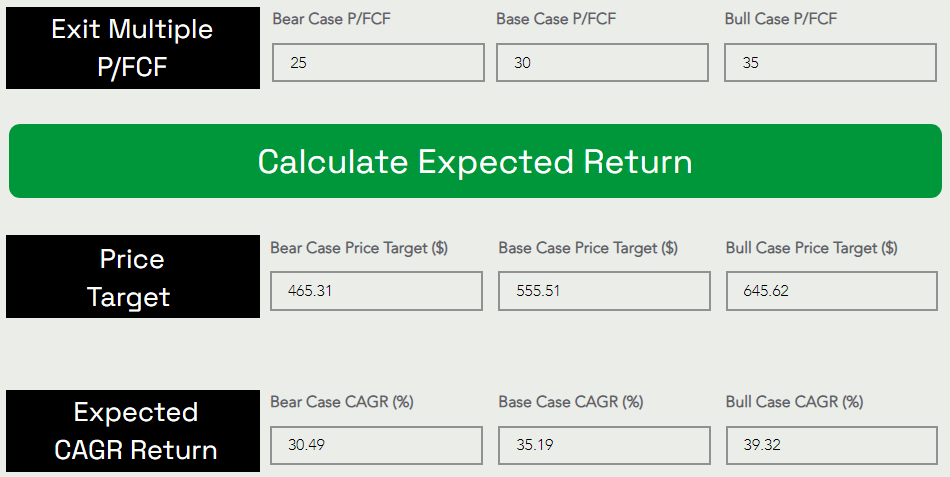

TQI Valuation Model (TQIG.org)

Assuming a base case exit P/FCF multiple of 30x for Tesla, I see the stock hitting $555.51 per share by 2027. As can be seen above, Tesla is projected to deliver CAGR returns of 35.19% for the next five years, which beats my required IRR of 15%. Hence, I view Tesla as a solid long-term buy at $123.

Final Thoughts

Tesla’s valuation has moderated significantly over the last twelve months, so much so that one could argue reasonably that Tesla is a value stock at this point. From a long-term standpoint, strong business fundamentals and reasonable valuation make Tesla a lucrative investment idea at current levels.

That said, Tesla’s near-term outlook remains uncertain. With the Fed pulling liquidity out of this economy, demand destruction is a natural outcome, and Tesla is already showing signs of demand cracking up. While Tesla is heading into its first recession, Elon Musk seems distracted with Twitter and using Tesla as his piggy bank to finance Twitter is hurting investor confidence.

In the event of a severe recession, Tesla’s numbers are likely to disappoint, and if earnings were to collapse (or go negative) in 2023, the bottom could really fall out next year. If the reverse gamma squeeze continues, Tesla could be headed all the way down to pre-pandemic lows at ~$60-65 (or even lower).

Technology giants like Meta (META) and Amazon (AMZN) are sitting at COVID-lows, and Tesla could join them in the event of a deep recession. With Tesla sitting at a key support zone (~$120-140 range), I expect to see a bounce in the near term. However, accumulating shares slowly remains the right strategy as volatility cuts both ways, and this is what we are doing within TQI’s GARP and Moonshot Growth portfolios. Within our Managed Risk portfolio, we have implemented a long position in Tesla with a zero-cost, options-based hedge guarding downside up to $65 per share.

Despite near-term downside risk, Tesla is a high-quality business that I want to own for the long haul. And I will continue to accumulate more shares slowly in the upcoming weeks and months.

Key Takeaway: I rate Tesla a “Strong Buy” in the low $100s, with a strong preference for staggered accumulation over 6-12 months.

Thank you for reading, and happy investing. If you have any questions, thoughts, and/or concerns, please share them in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment