Olga Tsareva

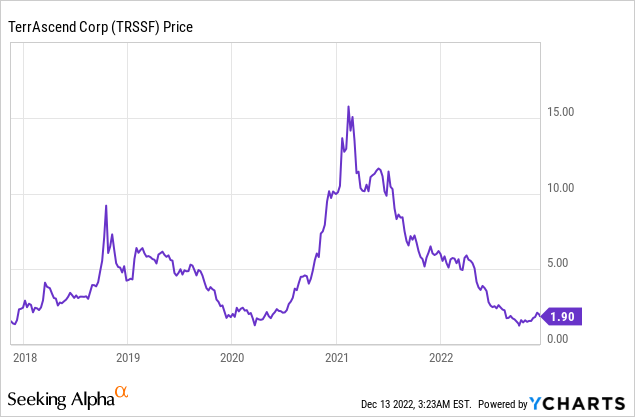

It might seem dramatic to state that October 17, 2018, is a date which will live in relative infamy. This day saw recreational cannabis sales begin in Canada, ushering in tens of billions of dollars in investment to spawn dozens of enterprises and thousands of jobs. But returns for investors in the space have either been abysmal or catastrophic. Large numbers of retail shareholders have lost their shirts, with the year-to-date capital returns for most cannabis stocks being negative. Indeed, the YTD returns of most stocks are negative, but the cannabis industry’s pre and post-2018 history have been characterized by a directionless meandering between periods of extreme volatility.

The performance of Mississauga, Ontario-based TerrAscend Corp. (OTCQX:TRSSF) perhaps most perfectly illustrates this.

The company went public the year before Canada’s legalization date and the trading in its common stock has forever been beyond the influence of its financials. This is despite revenues growing from $5.3 million in fiscal 2018 to $210.4 million in fiscal 2021, a staggering 241% compound annual growth rate. While bears would be right to flag that profits remained elusive for most of this period, the revenue growth has been met with common shares essentially trading in line with their 2017 figure. Positive returns came in just two periods over the last five years; the pre-legalization euphoria and the pandemic-era retail trading bubble. In both these periods, performance was driven by outside factors.

The Next Five Years

TerrAscend is a vertically integrated cannabis company that operates cultivation, processing, and manufacturing facilities in several U.S. states and Canada. The company also owns and operates a chain of dispensaries and retail stores under The Apothecarium, Gage, and Cookies brands. Its operations focus on producing cannabis products for both the medical and recreational markets. The company has been expanding rapidly in the U.S., recently closing the $28.5 million acquisition of a Michigan-based dispensary chain operator and expanding The Apothecarium and Cookies into new locations in New Jersey and Pennsylvania.

TerrAscend’s ability to acquire U.S.-based companies and become a multi-state operator despite its Canadian roots is due to its commons not being listed on the NASDAQ or NYSE. Whilst the U.S. market is materially larger, Canada’s incredibly onerous recreational cannabis regulations have made it difficult for operators to survive. There has been a long string of bankruptcies this year with shareholders blaming high taxes, a centralized government-controlled distribution system, and marketing bans for a market that has so far failed to fully replace the black market or deliver positive returns. In comparison, the US system broadly provides a freer and more direct market environment. This saw its larger Canadian peer Canopy Growth Corporation (CGC) dramatically quit cannabis retailing in its home country and restructure itself to gain access to a U.S. cannabis market still pending federal legalization.

The new Canopy USA converted a C$125 million loan into 24.6 million exchangeable TerrAscend shares, a transaction that ups Canopy’s stake to 18.2% from 12%. This could increase further to 23.4% if Canopy exercises its warrants. Fundamentally, Canopy’s exit from Canada materially increases the likelihood of TerrAscend being fully acquired in the future. However, the likelihood of this being completed in the near term will be limited due to NASDAQ’s objection to the restructuring.

A Future It Controls

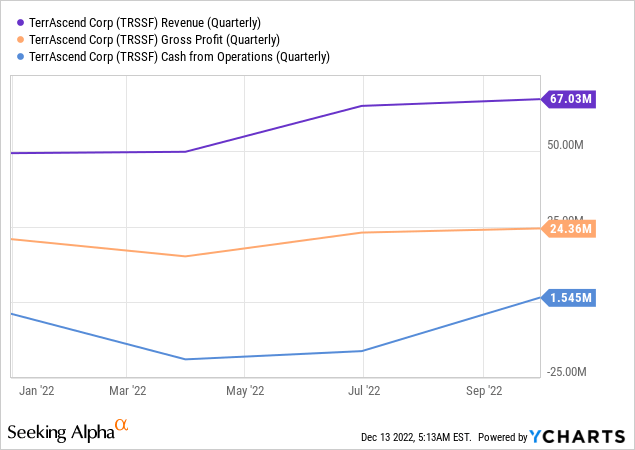

Reporting in USD, TerrAscend’s last reported earnings were for its fiscal 2022 third quarter. This saw revenue come in at $67 million, an increase of 36.4% over the year-ago comp and a 3.4% sequential increase. This formed a new quarterly revenue record and was of course driven by recent acquisitions and the continued rollout of its retail footprint.

A gross profit margin of 36.3% was an 80 basis point increase from 35.5% in the prior second quarter but was down from 43.7% in the year-ago comp. This saw gross profit come in at $24.36 million during the quarter, a 9.25% increase from the year-ago period. However, the company recorded a GAAP net loss of $311 million due to a $331 million one-time non-cash impairment charge. Removing this would have seen net income come in positive at around $20 million. Indeed, the company was able to record positive cash from operations of around $1.55 million, up from a cash burn of $18 million in the year-ago quarter.

Whilst the company’s deal with Canopy Growth helped reduce its annual interest expense by $10 million, net debt remains high at nearly $260 million. If the move into positive cash flow territory is sustained, then TerrAscend will be able to progressively pay down and refinance its debts.

Hence, what type of investor should be buying TerrAscend? Someone looking at an alternative way to play potential U.S. federal legalization and to gain exposure to Canopy Growth. The common shares currently trade on a 1.87x price to trailing 12 months multiple, lower than its sector median of 4.13x. This provides a seemingly de-risked entry point.

I don’t believe TerrAscend Corp. shares will begin to track growing financials anytime soon, and the near-term macro outlook is forecasted to be quite torrid. This is a hold, with broader market elements set to continue to dictate TerrAscend Corp. stock performance.

Be the first to comment