vetkit

Investment Thesis

Teradata (NYSE:TDC) is a cloud data platform for enterprise analytics. The business had a challenging 2022 period. And investors lost interest in the stock.

However, what investors didn’t seem to fully appreciate is that, unlike other cloud warehousing companies, TDC actually produces quite a significant amount of free cash flow.

Consequently, this has allowed TDC to ramp up its capital return program. As we look ahead to 2023, TDC is committed itself to return at least 75% of its capital back to shareholders.

I believe that paying approximately 19x this year’s non-GAAP EPS is an attractive multiple.

Revenue Growth Rates Aren’t The Only Picture

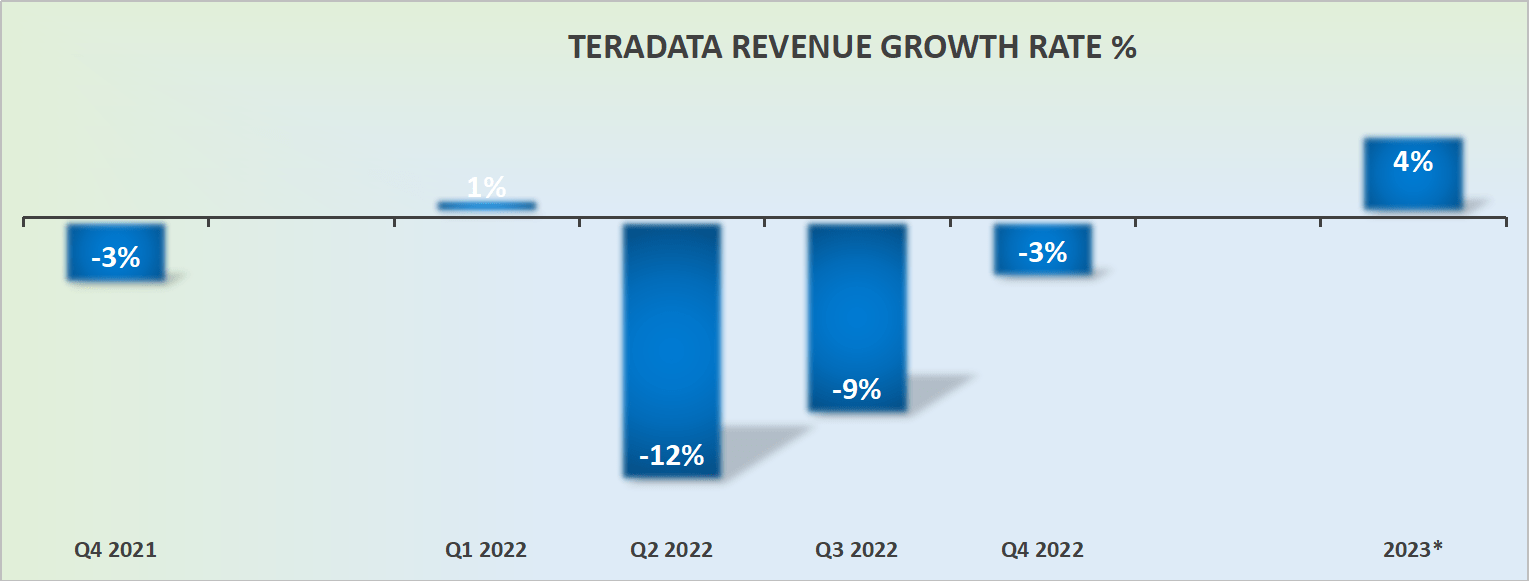

TDC revenue growth rates

The above graphic highlights how 2022 saw several quarters with negative CAGR figures.

For a business that’s supposed to be ”well positioned” for the digital transformation that is underway, the facts and narrative appear to be incongruent. However, that’s the headline story. What follows next is a more subtle interpretation.

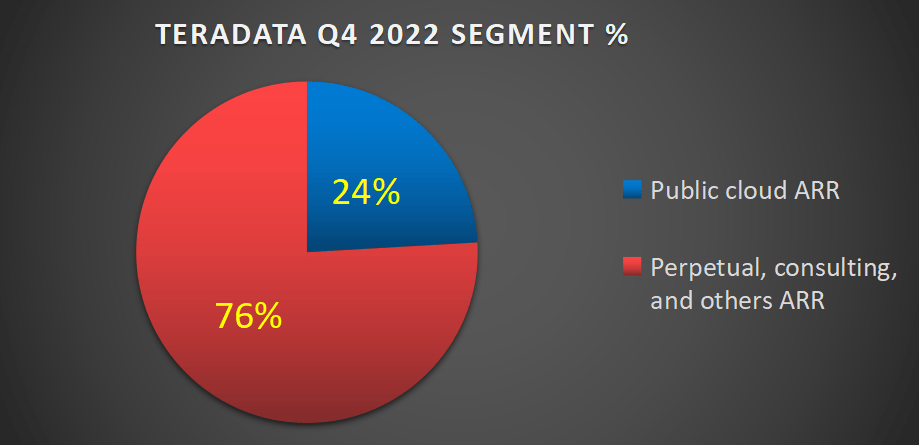

TDC author’s calculations

The above segmentation is a close approximation of the underlying business units.

The figure does not account for the different ARR and when the revenues are ultimately ”recognized”. But I believe this approximation works for our purposes.

As you can see above, roughly a quarter of the business is exposed to the public cloud. That’s TDC’s fastest-growing segment, and Q4 saw that business unit increase 81% y/y on a constant currency basis.

Now, we should state the obvious. For the most part, TDC is likely to be cannibalizing its own business. That means that even though the public cloud business appears to be growing incredibly fast, TDC is simply uprooting customers away from its perpetual license business to its public business.

So, even though the narrative here is about TDC growing its public cloud ARR, the total revenues for the year ahead are only pointing to 4% top line growth rates.

On the other hand, given what TDC’s revenues were in 2022, I am inclined to believe that investors are going to welcome some top line growth expected in 2023. Any growth really, even just 4% y/y CAGR.

After all, the business is clearly printing strong free cash flows.

Strong Cash Flows Are Being Returned to Shareholders

During TDC’s pre-prepared remarks, TDC’s CFO Claire Bramley stated,

[TDC] returned to shareholders ninety-six percent of our 2022 free cash flow. For the full year, we repurchased approximately nine point four million shares, or approximately three hundred and eighty-seven million dollars in total.

So, it’s not only that TDC returned approximately 10% of its market cap back to shareholders in 2022. But that looking ahead, there are reasons to assume that this pace of capital returns continues. Or at least something in the same ballpark.

On the one hand, TDC’s Q1 2023 will not benefit from a one-off tax refund again that it saw during last year’s Q1.

On the other hand, this time around TDC believes that it’s well positioned to increase its capital return program from 50% to ”at least 75%” of free cash flow.

TDC Stock Valuation — 19x Forward EPS

TDC is guiding for approximately $2.06 of EPS. This puts the stock at approximately 19x 2023 EPS.

I’m not going to argue that this is a particularly cheap multiple, because it’s not. But what this figure doesn’t sufficiently emphasize is management’s guidance that by 2025, TDC’s midpoint free cash flow could reach $500 million.

This puts the stock priced at approximately 8x forward free cash flow two years from now.

Put another way, looking out to this year, the stock looks cheap. But looking out 2 years, once the business transition gets further underway, the FCF could start to look more compelling.

The Bottom Line

By focusing solely on TDC’s share price, it isn’t immediately obvious that this company is actually gaining traction.

TDC investor presentation

My hope is that after reading through my analysis, the reader will view this company’s prospects in a different light. Whatever you decide, good luck.

Be the first to comment