Yijing Liu/iStock Editorial via Getty Images

Business Overview:

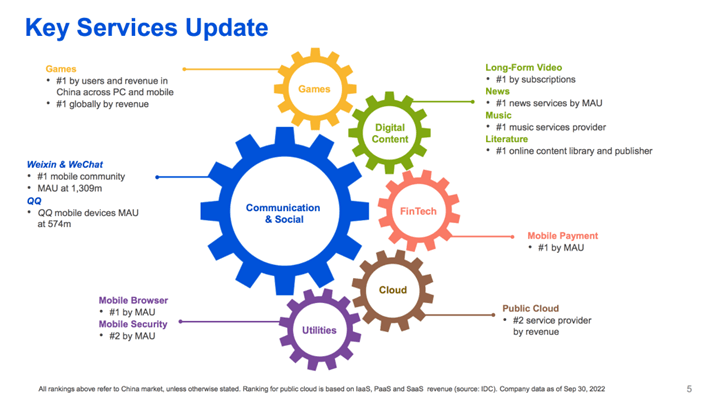

Tencent (OTCPK:TCEHY) generates revenues through a diverse portfolio of business segments, including communication and social media platforms, mobile, PC, and console gaming, fintech services, cloud computing services, and advertising. The company has several impressive accomplishments within its various business segments. These include being the top mobile community with over 1.3 billion monthly active users, the leading company in gaming revenues worldwide, and the top news service by monthly active users, among others. The below picture illustrates more of these notable achievements. The latter helps TCEHY to generate TTM revenues of $78 billion, cash flow from operations of $22 billion and free cash flow of $19 billion.

Tencent Services Highlights (Tencent Quarterly Report)

The market is currently valuing the company at $421 billion which is a steep decline since its peak at approx. $915 billion. The reasons for the decline were a combination of several factors including fines and restrictions to technology companies by Chinese regulators, a slowdown in the economy as well as in the company´s financials, etc. This significant valuation decrease has placed TCEHY in a very attractive position for a long-term investment opportunity. Based on strong fundamentals and coupled with significant growth potential in various markets I believe TCEHY presents a compelling opportunity to buy. Let´s dive into the financials.

Tencent Financial Overview:

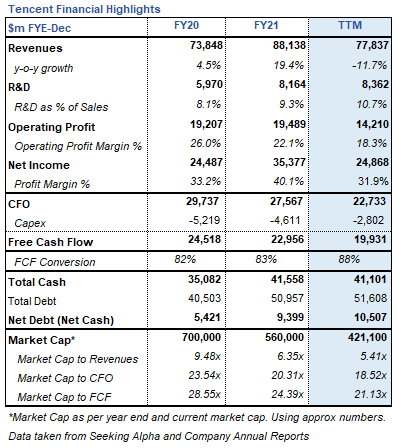

Tencent Financial Highlights (Seeking Alpha & Tencent Annual Report)

As already mentioned above TCEHY has strong fundamentals with TTM revenues of $78 billion cash flow from operations of $22 billion, and free cash flow of $19 billion. TCEHY generates 52% of total revenues through its Value-Added Services segment which consists of games and social networking. To understand the scale of this segment, we could simply take a look at the monthly active users from its famous social media platform WeChat, which surpassed the 1.3 billion mark during 2022. TCEHY also has a wide portfolio of games including League of Legends, Clash Royale, Call of Duty, etc. Among, TCEHY international mobile games, the company develops and operates 5 of the top 10 tittles measured by daily active users.

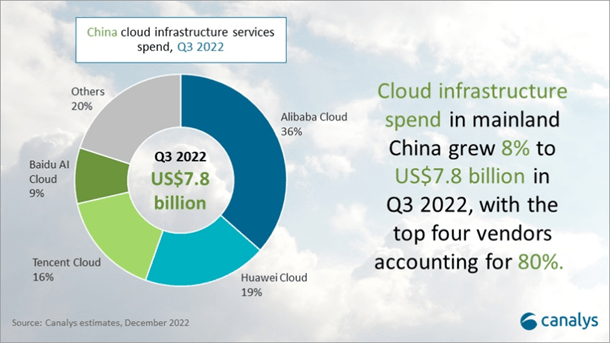

Further to this, approximately 31% of TCEHY total revenue is generated from its Fintech and Business segment, which primarily includes fintech and cloud services. It is worth noting that TCEHY holds a dominant position in China’s cloud market, ranking as the third largest generator of cloud computing revenue in the country, behind Alibaba (BABA) and Huawei. Finally, 16% of total revenues is derived from online advertising, which brings revenues through media and social advertisements.

China Cloud Market (Canalys)

The company also has a strong balance sheet with $41 billion in cash coupled with approx. $75bn in stakes of different companies. TCEHY has built a massive equity investment portfolio which covers over 750 companies in its domestic market and abroad. Popular names within its portfolio include: NIO (NIO), Pinduoduo (PDD), Spotify (SPOT), Snap (SNAP), etc. TCEHY does carry a debt position of $10.5 billion. However, this is neutralized by its extensive free cash flow generation which totaled $24.5 billion and $23 billion during the previous two years, respectively.

Shareholder Returns:

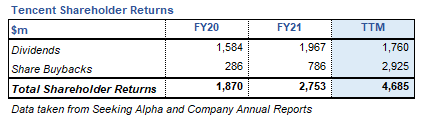

In May of 2022, TCEHY authorized a program to buy back 10% of its outstanding shares. Management has been cautious and has only started buying back shares more aggressively during the previous twelve months. Should TCEHY share price remain at current levels we could see management buying back shares more aggressively, as with $41 billion in cash it has enough fire power to redeem approx. 10% of shares from the open market.

Tencent Shareholder Returns (Seeking Alpha)

Growth Prospects:

TCEHY has a diverse range of businesses and is constantly seeking out new opportunities for growth and expansion. We can clearly see this with its investment portfolio which includes over 750 companies. The company has a strong track record of strategic acquisitions and investments, which have helped it to enter new markets and add new capabilities to its existing businesses.

Some key areas of focus for TCEHY future growth include:

- Expanding its cloud computing and artificial intelligence capabilities.

- Compete alongside tech giants like Meta Platforms (META) and ByteDance in the race to develop the metaverse.

TCEHY is clearly making a play in the cloud computing and artificial intelligence markets, with the company pledging $70 billion over the next five years for investments in these areas. Let´s begin with the cloud computing market. TCEHY is a prominent player in the cloud market in China with the third largest market share in the country behind BABA and Huawei. Meaning this is a market TCEHY is already well positioned in and which has the potential to grow in China alone to $84 billion by 2028. We can be sure that TCEHY cloud aspirations do not stop on the Chinese market as the global cloud computing market is estimated to grow to $1.2 trillion by 2027. We can expect the TCEHY to actively compete for a significant market share, both domestically and internationally.

AI & Metaverse (AI Time Journal)

The integration of AI and metaverse technology can be a synergistic opportunity for TCEHY. Through its gaming segment, TCEHY is already involved in technologies such as augmented reality, virtual reality, and artificial intelligence. TCEHY game studios continue to develop innovative and creative games for customers, positioning the company to continue to strive for better capabilities in these areas. Furthermore, Reuters reported that TCEHY has created an extended reality division to develop hardware and services for the metaverse, adding to the company’s efforts to stake a claim in this space along with other tech giants such as Meta, Microsoft (MSFT), and TikTok-developer ByteDance. TCEHY has also registered more than 20 metaverse-related trademarks for its various apps inside China.

The potential for growth in the metaverse and AI markets is substantial, with projections of $1.5 trillion and $400 billion by 2030 and 2028 respectively. This presents a favorable investment prospect for TCEHY as the company has the capability to capture a significant share of these expanding markets.

Valuation:

TCEHY experienced a significant decline in market valuation of over 70% from its peak at $915 billion on Feb. 2021 to its trough at $250 billion just a few weeks back. This decline was driven by several factors, including fines and restrictions on technology companies imposed by Chinese regulators and a slowdown in the global economy. The current market valuation of the company is $421 billion, which represents a multiple slightly above 18.5x cash flow from operations, and below 5.5x revenues. Despite this decline in value, the company’s long-term growth prospects remain robust, given its potential to capture a significant share of the rapidly growing cloud computing, artificial intelligence, and metaverse markets, which are collectively forecasted to be worth trillions of dollars in the future.

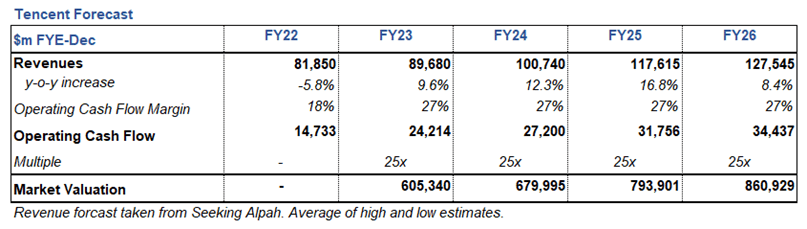

Due to accounting rules and the impact that the investment portfolio has on TCEHY bottom line, I will forecast earnings using cash flow from operations (this is actually what I prefer to use). I will utilize the market multiple method, using future forecasted cash flow from operations to a 25x multiple.

Tencent Forecast (Seeking Alpha )

I have obtained the analysts’ revenues forecast from Seeking Alpha data and have applied an operating cash flow margin of 27%, which is below the previous 2 years operating cash flow margin at 41% and 32%, respectively. Given these assumptions, I have applied a multiple of 25x, this multiple is below the company historical price to earnings ratio, which is usually above 25x. Using this method, I have arrived at a market valuation for TCEHY in 2026 of $861 billion.

Risks:

Competition: TCEHY operates in highly competitive environments, these include: i) Social networking and digital content space where TCEHY competes with Weibo (WB), Baidu (BIDU), among others. ii) Online gaming space, TCEHY competes with companies such as Activision Blizzard (ATVI), Electronic Arts (EA), etc. iii) In Fintech, TCEHY competes with BABA financial arm, Ant Financial among others. iv) In the cloud computing space, TCEHY competes with cloud service providers in China including Alibaba Cloud, Huawei, etc. As well as international players like Amazon (AMZN) Amazon Web Services and MSFT Microsoft Azure.

Semiconductor Restriction: It is well-known that advanced semiconductors play a crucial role in powering a wide range of potentially transformative technologies. The restrictions imposed on China by the USA have the potential to limit China’s firms’ abilities to build advanced data centers and deploy artificial intelligence. Advance semiconductors are also essential for improving supercomputing and artificial intelligence capabilities. The biggest impact of these restrictions will be felt by China’s technology firms as the cost of AI is expected to be very power-intensive, making it expensive to implement.

Conclusion:

In conclusion, TCEHY has a diversified portfolio of business segments with impressive accomplishments, strong financial performance, and a strong balance sheet. Additionally, the cloud computing, artificial intelligence, and metaverse markets present a favorable investment opportunity for TCEHY as it has the capability to capture a substantial share of these expanding markets. I estimate a market valuation for TCEHY in 2026 around $861 billion. Overall TCEHY strong fundamentals, diversified portfolio and growth potential makes it a promising investment opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment