zamrznutitonovi/iStock via Getty Images

Situation Overview

Standard General struck a deal to acquire Tegna (NYSE:TGNA) back in February 2022. All the conditions have been met, except for the regulatory approvals. The sticking points are (1) retransmission rate hikes and (2) job cuts post-transaction. Standard General has publicly committed to doing neither in filings to the FCC. Standard General has waived its right to hike retransmission rates and committed to no station-level job cuts for a minimum of two years. In my opinion, the only excuse to not approve the transaction is the fact that Apollo is providing non-voting preferred equity financing and Apollo also owns Cox and the FCC would have to prove that they will collude – which sounds impossible before the fact. If you have some legal background, I’m happy to hear your thoughts.

Risk and Reward

With the stock above $20 and a takeout price of $24.20 ($24 plus a ticking fee of $0.05 per month), there is an upside of ~$4.00/share if the deal successfully closes. The downside is a little difficult to estimate as Tegna was in the M&A rumor mill for the past few years. The stock was trading around $18 before the definitive news came out, and Tegna’s comps (except for Nexstar) are all down +30%. Let’s use 15% to adjust for market beta as Tegna is higher quality and lower levered, which puts the deal-break price at $15.30 or $5.0/share of downside.

On the bond side, both the 2028s and 2029s are offered for around $94. Both bonds are not callable yet, and this transaction should be a change of control event, so the bondholders should at least see a $101 change of control bid coming. Interestingly, given how much the treasury curve has risen, it’s not much more expensive to make-whole call these bonds (roughly $102-$102.50 by my calculation). I expect Standard General to tender for these bonds between $101-$102 and most bondholders should tender. In other words, there is an upside of $7-$7.50 in the bonds if the deal closes.

If the deal breaks, the bonds should start to trade on relative spread/yield again. Nexstar 4.75% 2028s trades around 7.15% YTW, and I think 7.25% yield is fair for Tegna 2028s, which translates to a price of ~$89 or a downside of $5.

In summary, the risk/reward ratio for the bond is more attractive than the stock. The upside/downside for the stock and the bond is $4/$5 and $7/$5, respectively.

Long Bond and Short Stock

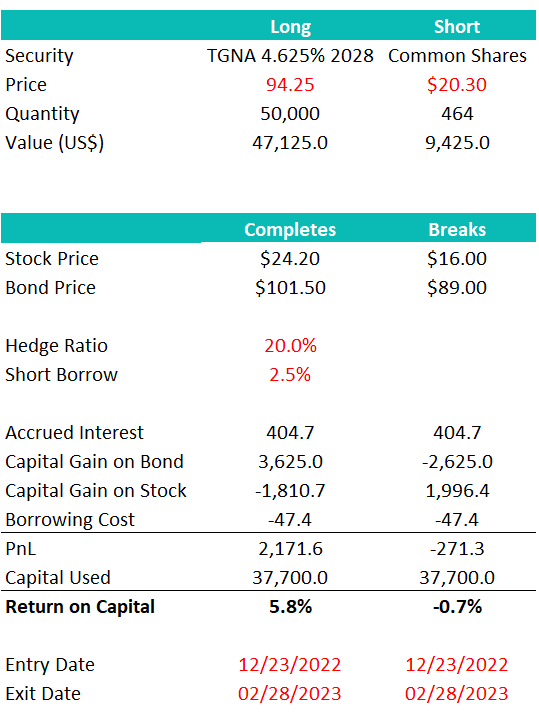

I believe a better trade is to buy the bond and partially hedge it with shorting the stock. At 20.0% hedge ratio (i.e., shorting 20% of the market value of the bonds), it’s possible to construct a trade where you earn ~6% if the deal completes and only down slightly if the deal breaks. See below for a hypothetical example. Note that the 6% is the holding period return (i.e., not annualized), which is roughly three months.

Author’s Estimate

Conclusion

Standard General is literally doing everything within its power to help ease the regulator’s concerns with this transaction. While it still feels like a coin flip, I don’t really see more excuses for the FCC to block this acquisition, especially since collusion is impossible to prove before it happens. Given the slight runup in Tegna’s stock, the risk/reward favors owning the Tegna bonds. It might not be worth the trouble but bondholders can short a small amount of the stock to hedge the downside.

Be the first to comment