Sundry Photography/iStock Editorial via Getty Images

The President of TDK Corporation (OTCPK:TTDKY), a producer of power electronics such as lithium-ion batteries and passive components, recently said in an interview with Bloomberg that he expects a more gradual smartphone demand recovery in “late 2023.” The stock subsequently sold off, but I view the near-term concerns as overblown. For one, TDK has already incorporated a more conservative outlook in its updated FY23 guidance.

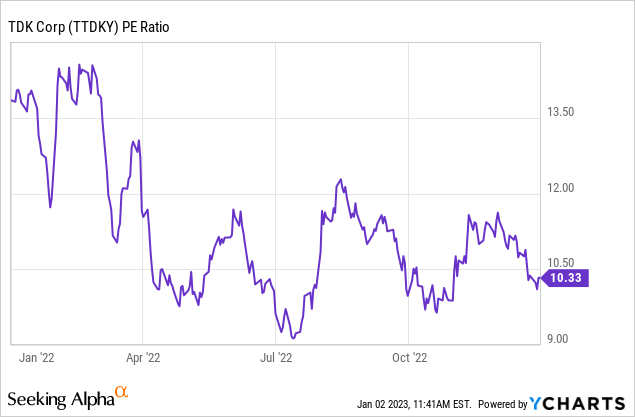

More broadly, though, TDK’s passive components business will continue to benefit from secular automobile electrification tailwinds, while an enhanced product lineup for North American customers is supporting an earnings turnaround in the sensors business. With the company’s energy application products segment also adding to the long-term growth trajectory via industrial and residential storage batteries, there is ample potential for upward revisions to the earnings trajectory in the coming years. Relative to the double-digit earnings growth potential, the ~9x fwd P/E (~10x trailing P/E) is undemanding and should re-rate over time.

A More Gradual Smartphone Recovery but No Impact on Guidance

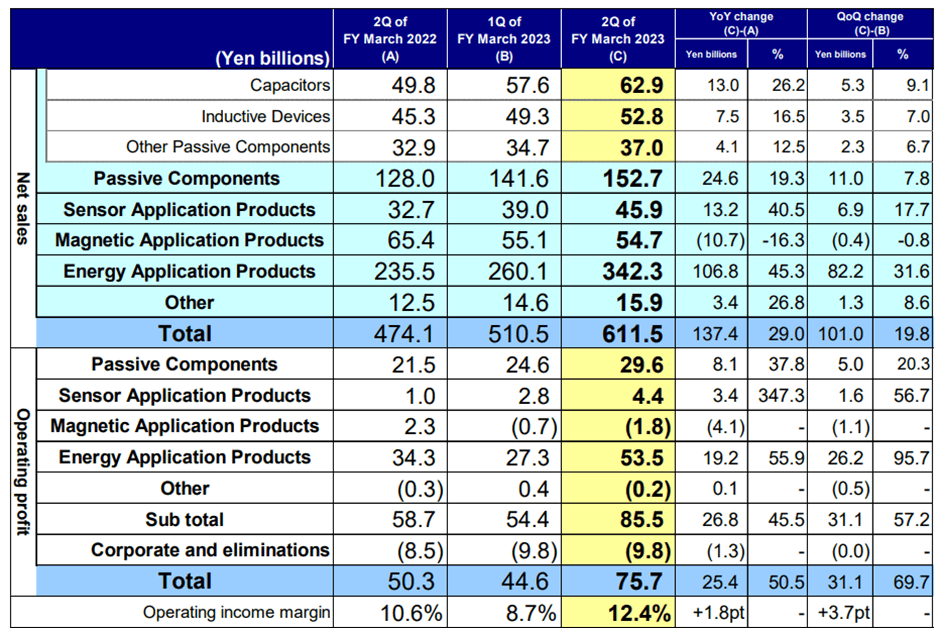

Following a strong H1 result, which saw sales up across all three key segments (passive components, sensor application products, and energy application products), it came as no surprise that TDK raised its full-year sales guidance to JPY2.2bn and its operating profit guidance to JPY200bn. Underlying this guidance raise, though, were some surprisingly conservative projections, including a decline in batteries for smartphones and other applications in the back half of the fiscal year. Management has also penciled in a lower overall profit margin, assuming a decline in selling prices and elevated input costs.

TDK Corporation

So, while TDK President Noboru Saito called for a delayed recovery in smartphone demand in his recent Bloomberg interview, with full-year demand also set to come in lower, much of the bearishness has already been factored into the last guidance update. Beyond smartphones, expect significant inventory adjustments in the Hard Disk Drive (HDD) market to drive further weakness in the magnetic application products segment. This should be more than offset, though, by an above-par profit contribution from energy application products in H2; thus, I see a clear path to a >JPY200bn operating profit result this fiscal year.

Automotive Tailwinds Support the Growth Outlook

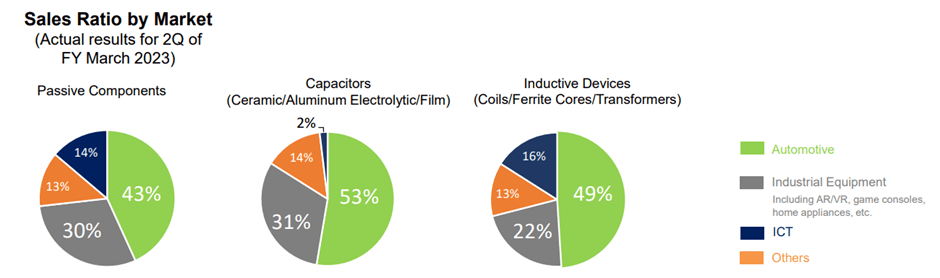

Elsewhere, the strength of TDK’s automotive applications end market remains underappreciated, in my view. Recall that autos (>40% of segment sales) were the key driver of the passive components segment outperformance in Q2, with sales up double-digits % YoY. The focus here is capitalizing on the secular auto 2.0 transition, in particular, electric vehicles (EV), where TDK has focused its product development efforts and built up an expansive automotive client base. These efforts have already begun to pay off as electric vehicle growth continues to outpace the broader auto market, helped by increasing subsidies from governments around the world (e.g., the EV tax credits in the US’ recent ‘Inflation Reduction Act’).

TDK Corporation

TDK is exposed to more than just the EV shift, though. Through its sensor application product segment, which derives >30% of segment sales from auto applications, TDK is also exposed to the secular growth in vehicle connectivity and autonomy. For instance, the increased adoption of TMR sensors used in everything from cameras and compasses to measuring EV battery flow has driven much of the growth thus far. Additional growth engines include motion sensor solutions for navigation. Continued product development here will be key in TDK benefiting from the pending shift toward autonomous vehicles.

Long Runway for the Batteries Business

Things are also looking up for TDK’s energy application products segment. The combination of a higher rate environment and COVID-driven supply chain disruptions has led to many smaller producers withdrawing from the industry. So, while costs have risen, TDK’s increased competitiveness has allowed it to raise prices to protect margins. With volumes also moving higher in Q2 despite the price hikes, the energy application products (mainly batteries) operating margin was sequentially higher in Q2. In addition to the continued price pass-through, higher contributions from North American smartphones and growth in industrial batteries also helped.

TDK Corporation

In the near-term, management’s guidance for the battery price pass-through to taper off means the Q2 margin outperformance is unlikely to be repeated anytime soon. That said, the industry is consolidating around major players like TDK, supporting the long-term growth runway. Similarly, the industrial batteries business likely won’t sustain the earnings contribution in Q2 for another few quarters following the shift to a JV structure with CATL. Yet, the mid to long-term growth potential in industrial batteries remains intact, with residential storage batteries emerging as a key focus area in light of higher energy prices globally. With consensus estimates factoring in minimal contribution for now, good execution here could yield significant earnings upside sooner rather than later.

Fade the Near-Term Bearishness

TDK stock sold off recently following a Bloomberg interview with its President calling for a more gradual recovery in smartphone demand in H2 2023. TDK has already incorporated a weaker smartphone outlook (among other conservative assumptions) into its guidance, though, so the bar is low heading into the full-year earnings announcement.

Plus, the long-term case remains intact on electrification tailwinds in its passive components and energy application segments. A recent turnaround in the sensors business also bodes well for the outlook, supported by an expanded lineup of products for its North American customer base. Thus, I expect a stable earnings trajectory through FY23/FY24, with a further re-rating likely from the current ~9x fwd P/E (~10x trailing P/E) as TDK outperforms its P&L targets.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment