MXW Stock/iStock via Getty Images

The Thesis

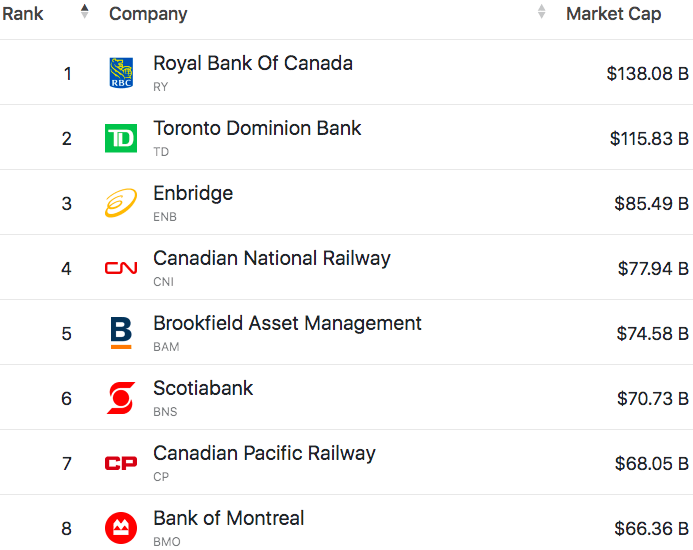

The list of Canada’s largest companies is dominated by banks:

Largest Companies In Canada By Market Cap (CompaniesMarketCap.com)

The Toronto-Dominion Bank (NYSE:TD) and Royal Bank of Canada (NYSE:RY) are raking in huge profits, with consumers in debt up to their eyeballs. The problem is, this looks all too similar to the U.S. in 2007. Let’s dig into the risks, to see why we’re bearish on Canadian banks.

The Housing Bubble

Canadians have been bidding up the prices of homes over the past few years, literally. Over the past year, many new listings, especially within urban centers, received multiple offers above the listing price. Bidding wars literally broke out. The economies of British Columbia and Ontario have been especially hot. Vancouver, the capital of British Columbia, is at the apex of the bubble. Vancouver is the 3rd least affordable city in the world. The average home in Vancouver costs 13.3x household income, and the average price of a detached single-family home is $1,870,000 CAD. Yes, nearly $2 million.

Sailing On A Sea Of Debt

If you own stock in a bank, this is not the kind of headline you’re hoping to see:

News Headline (Better Dwelling)

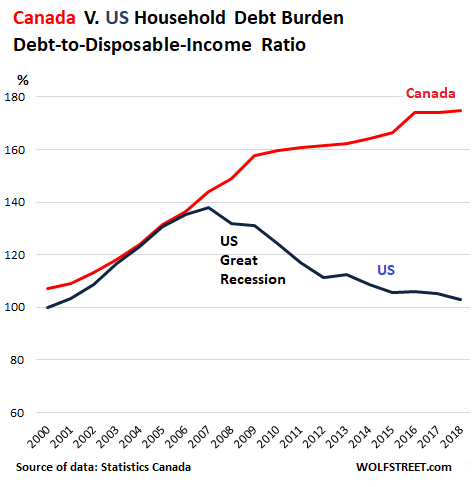

Debt has been growing faster than income in Canada for quite some time. Recently, household debt to disposable income hit a record high of 180%. For a country to get this indebted, there usually needs to be some unwise lending by the banks. Canadians are often on a 5-year fixed-rate mortgage, and will soon be forced to refinance at higher interest rates. When this happens, the debt squeeze will be severe. Notice that Canadian consumers are now in significantly worse shape than American consumers, even if you compare to The Global Financial Crisis of 2008:

Household Debt To Disposable Income: Canada vs U.S. (Wolf Street)

Canada’s corporations are also in terrible financial shape. Just have a look at the balance sheets of companies like Bell Canada (BCE), Enbridge (ENB), and Air Canada (OTCQX:ACDVF). It’s not uncommon for Canadian companies to have net debt to income ratios of 10x or more. These business compete on who can pay the highest dividend, and their competitiveness and financial positions often deteriorate as a result.

So why is all this happening? Basically, in 2009, the United States completely deleveraged, and Canada didn’t. Canadian consumers and businesses have been skating on thin ice with enormous debts and near zero interest rates for years, but with interest rates on the rise, that’s about to change.

Bankruptcy Risk

Could Canada’s biggest banks go bust? Likely not without bailouts attempts from the Bank of Canada. The latest round of bankruptcies in Canada’s banking industry occurred in the late 80’s and early 90’s. Government bailouts failed in 1985. But, had the banks been the size of TD and Royal Bank, the government probably would’ve injected a 2nd round of capital.

The Valuation

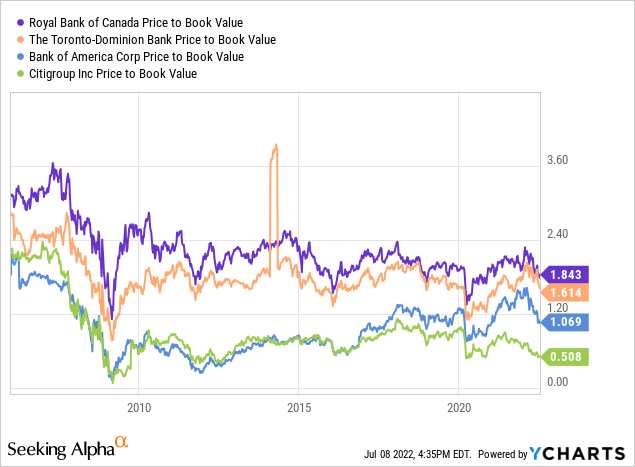

TD and Royal Bank are trading at a large premium to book value. This leaves no margin of safety should recession losses hit home. Just look what happened to Bank of America and Citigroup’s P/B ratios in 2009:

This is how the banks compare to each other, as well as their U.S. peers:

| Toronto-Dominion Bank (TD) | Royal Bank of Canada (RY) | Bank of America (BAC) | JPMorgan Chase (JPM) | |

| ROE | 16% | 18% | 12% | 16% |

| P/B | 1.6 | 1.8 | 1.1 | 1.3 |

| P/E | 10 | 11 | 9 | 8.5 |

| Balance Sheet Ratios | TD | RY | BAC | JPM |

| Equity To Assets (%) | 5.4% | 5.2% | 8.2% | 7.2% |

| Cash & Equivalents To Assets (%) | 0% | 6.1% | 8.3% | 18.3% |

Our main takeaway here is that U.S. banks are both better capitalized and cheaper than their Canadian counterparts.

Prospective Returns

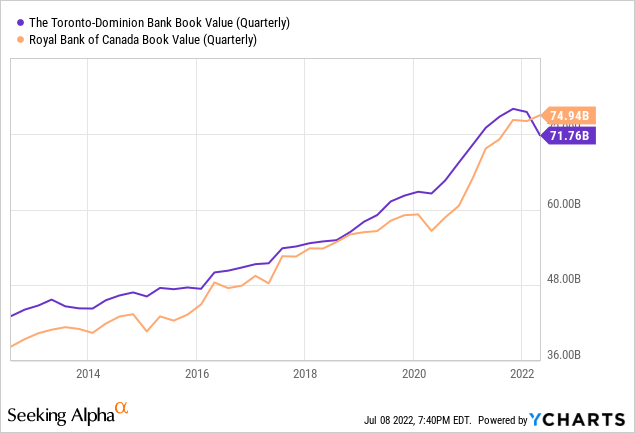

Over the past 10 years, TD Bank (TD) and Royal Bank (RY) have grown shareholders equity at 5.5% and 6.7% per annum, respectively. In the future, Canadian consumers should begin to save more, and take on less debt. As we go forward, we believe these banks will see slower growth in their book values, and estimate growth of 5% per annum. This gives us shareholders equity of $117 billion and $122 billion for TD and RY in 2032.

We expect multiple contraction following Canada’s next severe recession. Events like this tend to change sentiment and risk premiums, as well as make the banks themselves lend more conservatively and even earn less on equity. Currently, many Canadians see banks as blue chip companies, rather than cyclical investment vehicles. We’ve assigned a P/B of 1.3 for RY and 1.2 for TD in 2032. Royal Bank currently has the best brand in the industry, and is known for its customer service. TD is weaker in this regard, but this can change over time.

Altogether, our 2032 price targets are $78 and $113 per share for TD and RY, respectively. This indicates returns of 6% and 5% per annum with dividends reinvested.

Risks To The Thesis

The risk to this conclusion is that the banks manage to sail smoothly through the next recession, perhaps with preemptive support from the Canadian government. If the banks can maintain their market premiums and continue to grow as they have in the past, you could get higher returns. Banks could benefit from moderately higher interest rates 10 years out.

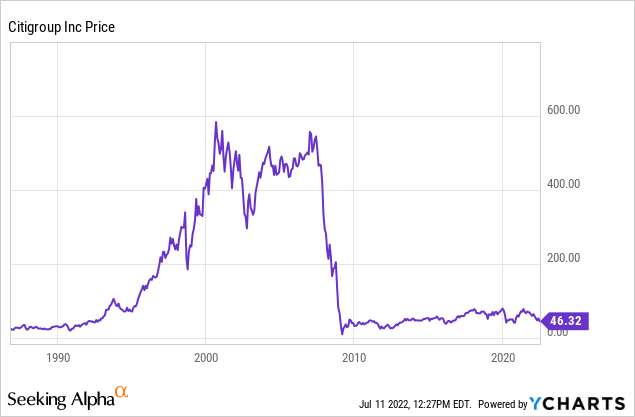

The worst-case scenario is Citigroup, which still hasn’t recovered from The Great Recession:

Conclusion

For TD and Royal Bank, we believe the risk and reward do not favor the common shareholder. We have a “sell” rating on both shares. Canadian banks are often viewed as blue chip companies, but the Global Financial Crisis is a sobering reminder of the downside. There is far too much debt and financial folly in Canada right now. There may be better buying opportunities after loan losses hit home. If investors would like to hold their positions in financials, we recommend U.S. banks, which appear to be both cheaper and better capitalized.

For more on this, check out my articles:

Be the first to comment