JHVEPhoto

Introduction

Target (NYSE:TGT) has experienced a significant increase in revenue and earnings over the last 5 years. The company returned more cash to shareholders through dividend increases and share repurchases. Now that the stock has been in bear territory since mid-2021, its stock price looks favorable.

High inflation has taken its toll, with more consumers showing signs of stress and refraining from making discretionary purchases.

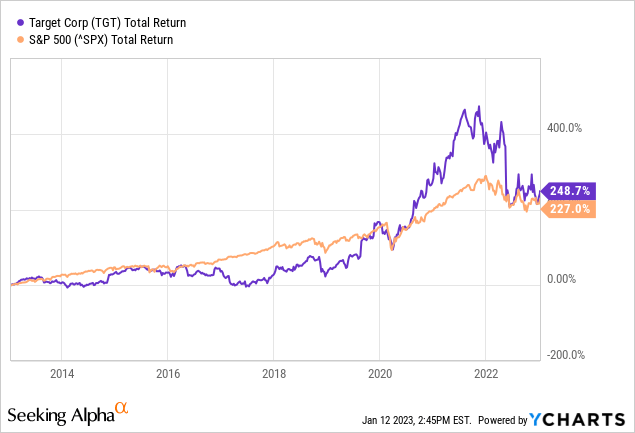

Over the last ten years, the stock has outperformed the S&P500, with an annualized return of 13.3%. The current financial headwinds have reduced earnings, causing the stock price to fall. The current stock price drop could be a fantastic buying opportunity if it persists.

Mixed Third Quarter Earnings

Comparable sales at Target were up 2.7% in the third quarter compared to the same period a year ago. Both an increase in traffic (1.4%%) and average ticket price (+1.3%) contributed to the 1.6% increase in comparable sales.

Consumers are becoming more frugal as a result of financial stress. Beauty, food and beverages, and household essentials led to category growth, which helped to offset weakness in discretionary categories. This year, many consumers were using their savings in order to make it through the week, as high inflation rates have eroded their purchasing power. Consequently, Target’s customers are showing heightened price sensitivity, responding favorably to discounts but remaining wary of paying the full price.

The 3.9% operating margin rate in the third quarter was a significant improvement from the 2.1% rate in the previous quarter, but it still significantly lagged behind projections. In addition to a growing financial headwind from inventory shortage, a notable increase in theft and organized retail crime, and a higher-than-expected mix of promotional sales as guests moved away from full-price purchases all contributed to this.

Target is preparing for the future by fine-tuning its systems to meet the demands of its expanding business. It aims to save between $2 and $3 billion over the next 3 years, which could be put toward the company’s long-term growth investments or returned to shareholders.

Shareholder Return Is High At 93%

The current dividend yield for Target stock is 2.5%, and the company pays out a dividend of $4.32 per share. With an annual growth rate of 11.6% on average, the dividend per share has increased from $1.32 in 2012 to $3.96 in 2022.

Dividend growth history (Seeking Alpha TGT ticker page)

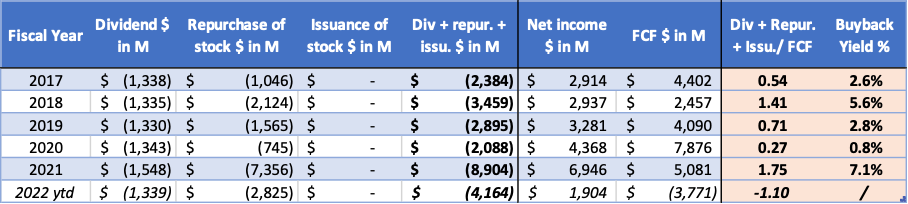

We can see from the cash flow statement that the dividend distribution hasn’t changed much over the last 5 years. The dividend distribution was increased beginning in fiscal 2021.

Free cash flow has fluctuated over the years, with 2020 being the best year with $7.9B generated. The current free cash flow is negative due to a significant increase in cost of goods sold, inventory shrinkage due to theft, and increased capital expenditures.

To increase its dividend per share, the company repurchases stock, reducing the number of outstanding shares. This will result in higher earnings and dividends per share. Furthermore, purchasing shares on the open market increases demand while decreasing supply, which may result in share price appreciation.

Total shareholder return, as measured by dividend distribution plus share repurchases, is on average 0.93 from 2017 to 2021, indicating that it is long-term sustainable.

TGT cash flow highlights (SEC and author’s own calculations)

Over the years, the company has used its free cash flow to fund share repurchases and dividends. The company’s free cash flow has now turned negative, indicating that it has been financed with cash and debt. The balance sheet is strong, with $954 million in cash (and equivalents), $16.4 billion in total debt, and $15.4 billion in net debt. In a good year, like fiscal 2021, net debt to EBITDA is 1.7. During normal economic conditions, the company could service its debt effectively.

Stock’s Valuation Is In Favorable Territory

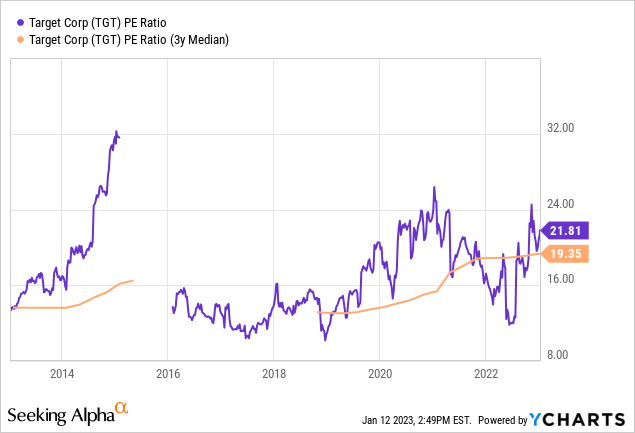

Target’s stock price has fluctuated over the last ten years, but if you bought shares in mid-2017, you would have seen a strong rally from $53 per share to $260 per share in mid-2021. With a PE ratio of 24, the stock valuation in mid-2021 was undeniably high.

Since then, the stock has dropped 38% to $160 per share today, making the stock valuation appealing. Despite the low share price level, the PE ratio has risen to 22, indicating that the shares are overvalued. However, this is not the case because the company saw an increase in organized crime rates in 2022 and wrote off $400 million in inventory. These are temporary headwinds that will pass quickly.

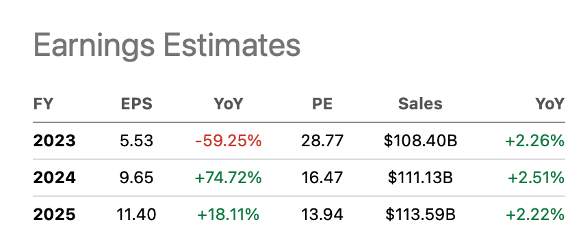

The GAAP PE ratio graph above is created by YCharts, while the non-GAAP PE ratio is calculated by Seeking Alpha. Both show currently a high valuation. However, in fiscal 2025, the non-GAAP PE ratio is expected to be only 14. This is even though 27 analysts have reduced their earnings estimates for the coming years. The stock is available at a slight discount to its 5-year average non-GAAP PE ratio of 18.

Earnings estimates (Seeking Alpha TGT ticker page)

Conclusion

Inflationary pressures have prompted consumers to reconsider making discretionary purchases. Target discovered in 2022 that consumers are more focused on and responsive to promotions, and less willing to pay full price. Comparable sales increased by 2.7% in the third quarter compared to the same quarter last year. Traffic increased by 1.4%, and average ticket prices increased by 1.3%. Growth in Beauty, Food and Beverage, and Household Essentials drove category performance, offsetting continued softness in discretionary categories.

Target is optimizing its operations to match the scale of its business and becoming leaner, which will result in a total savings of $2 billion to $3 billion over the next three years. Nonetheless, high inflation will put pressure on its revenue and earnings streams as the cost of goods rises.

The recent drop in share price is good news for the stock’s valuation. I believe the stock’s valuation is in line with the historical average. Although 27 analysts have downgraded the stock, they predict strong earnings growth in the coming years. The stocks appear to be undervalued, with a forward PE ratio of 14 for 2025. Still, I would sit on the sidelines and buy Target when inflationary pressures are lower.

Be the first to comment