Frank Rossoto Stocktrek/DigitalVision via Getty Images

When one thinks of defense contractors, top names like Lockheed Martin (LMT) and Raytheon Technologies (RTX) may first come to mind. However, what often gets ignored is the moat-worthy shipbuilder, Huntington Ingalls (NYSE:HII), which is sometimes referred to as the “Lockheed of the Seas”.

It’s been a while since my last bullish take on the stock back in the middle of 2021, and it’s fared better than the S&P 500 (SPY), giving investors downside protection. This is reflected by its 6% total return over this time frame, which is ahead of the 4% decline in the S&P 500.

Recently, HII’s stock price has taken a dip since reaching a near term high of $240 back in December, and in this article, I highlight why the stock is a buy for potentially strong total returns, so let’s get started.

HII Stock (Seeking Alpha)

Why HII?

Huntington Ingalls has been around for over a century and came to its current form when it was spun off from Northrop Grumman (NOC) in 2011. Its shipbuilding divisions in Virginia and Mississippi have built more ships in more classes than any other shipbuilder for the U.S. Navy and Coast Guard.

HII also gets recurring revenue from its Technical Solutions division, which supports national security missions around the globe with unmanned systems, defense and federal solutions, and nuclear and environmental services. The steady nature of HII’s revenue stream combined with healthy margins, and capital returns to investors has resulted in outsized shareholder returns. As shown below, HII has produced a 468% total return over the past decade, far surpassing the 222% return of the S&P 500.

HII Total Return (Seeking Alpha)

Meanwhile, HII continues to demonstrate strong growth despite general economic uncertainty and high inflation. This is reflected by revenue rising by a robust 12% YoY to $2.6 billion during the third quarter. This was driven by its acquisition of Alion Science and Technology in the second half of 2021 as well as revenue growth at Newport news Shipbuilding. Importantly, HII’s operating margin has held steady despite inflation, standing flat compared to the prior year period at 5.0%.

Potential headwinds to HII include the need to recruit the next generation of skilled workers at its shipbuilding facilities. Management is addressing this concern through ramping its development pipeline and apprenticeship programs, as highlighted during the last conference call:

To address our shipbuilding labor challenges, we have aggressively enhanced our skilled workforce development pipeline. To this end, while we broadened our recruiting efforts to bring in more shipbuilders, we are also expanding our very successful apprenticeship programs, including revised curricula, reduction in completion time lines, a focus on pre-apprenticeships and use apprenticeships and expansion to underserved populations and women in the industry.

Looking forward, HII is well positioned for growth as it’s invested $1 billion in recent years in the infrastructure, facility and toolsets at Ingalls Shipbuilding to enable process efficiency and enhanced product quality. HII also maintains a strong growth runway as management sees critical needs from the U.S. Navy for the construction, maintenance, and modernization of naval destroyers, amphibious vehicles, submarines and aircraft carriers, and management expects significant contract awards to drive its backlog stability. This includes a recent $70 million win from the U.S. Air Force and a $10.5 million win this month from the U.S. Navy for the modernization planning of Zumwalt-class guided missile destroyers.

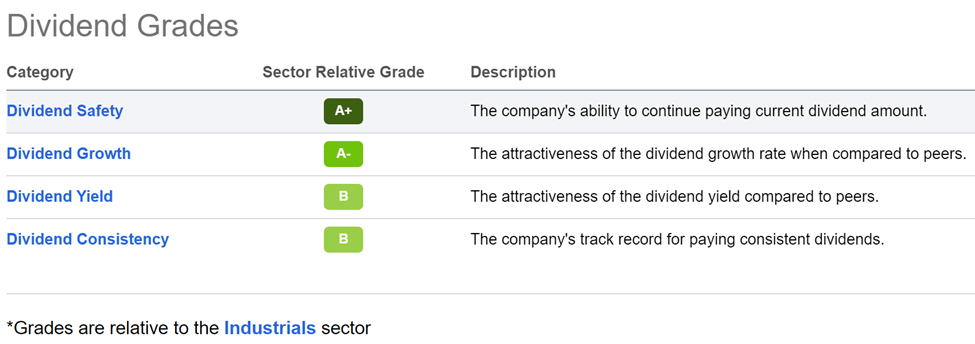

Meanwhile, HII maintains a BBB- investment grade rated balance sheet. While its 2.3% dividend yield isn’t high, it’s well protected by a 33% payout ratio, and comes with a 5-year 13.7% CAGR and 9 years of consecutive growth. As shown below, HII scores A and B dividend grades for safety, growth, yield, and consistency.

HII Dividend Grades (Seeking Alpha)

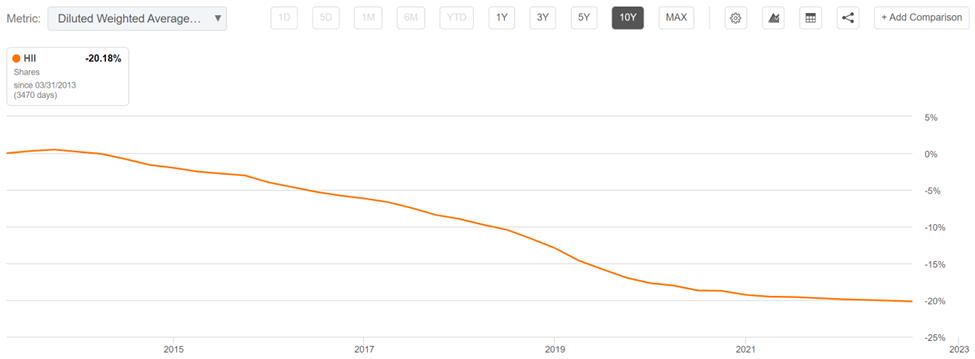

Moreover, HII should also be thought of as a total return store, as it’s reduced its share count by a meaningful 20% over the past decade, as shown below.

HII Shares Outstanding (Seeking Alpha)

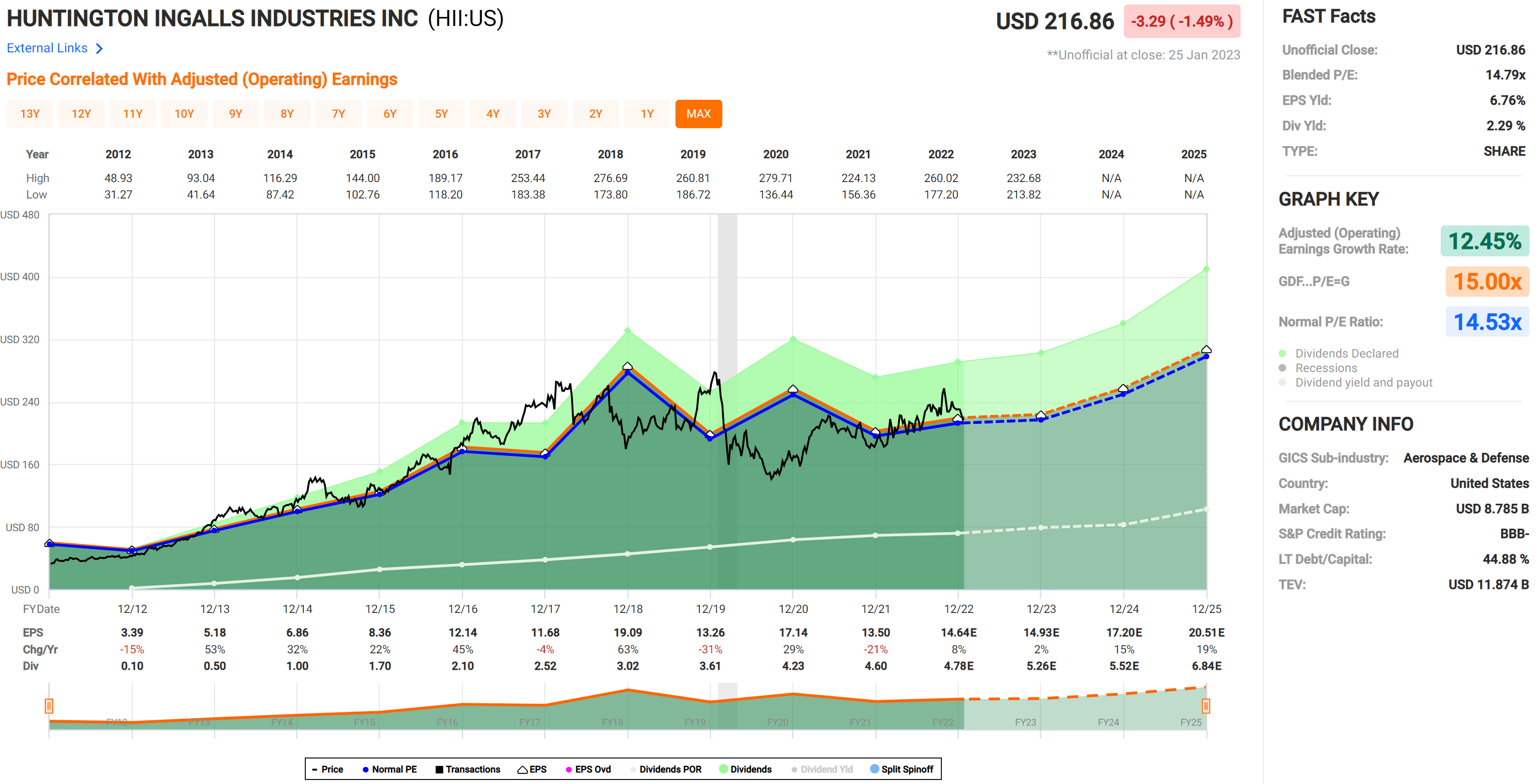

Lastly, I see value in HII after its recent dip to $216.86 with a forward PE of 14.7, sitting just slightly above its long-term normal PE of 14.5. Analysts estimate just 3% EPS growth this year, but expect growth to ramp up next year with 17% EPS growth. Analysts also have an average price target of $252, implying a potential one-year total return in the high teens.

HII Valuation (FAST Graphs)

Investor Takeaway

Huntington Ingalls is a moat-worthy shipbuilder that’s produced market beating returns for shareholders over the past decade. It continues its strong growth trajectory and has a robust line of sight as the U.S. Navy seeks to ramp up and modernize its fleet. Meanwhile, HII has rewarded shareholders with high dividend growth and meaningful share buybacks. While HII is not a bargain, the recent dip in share price does present long-term investors with a solid entry point for potentially strong returns.

Be the first to comment