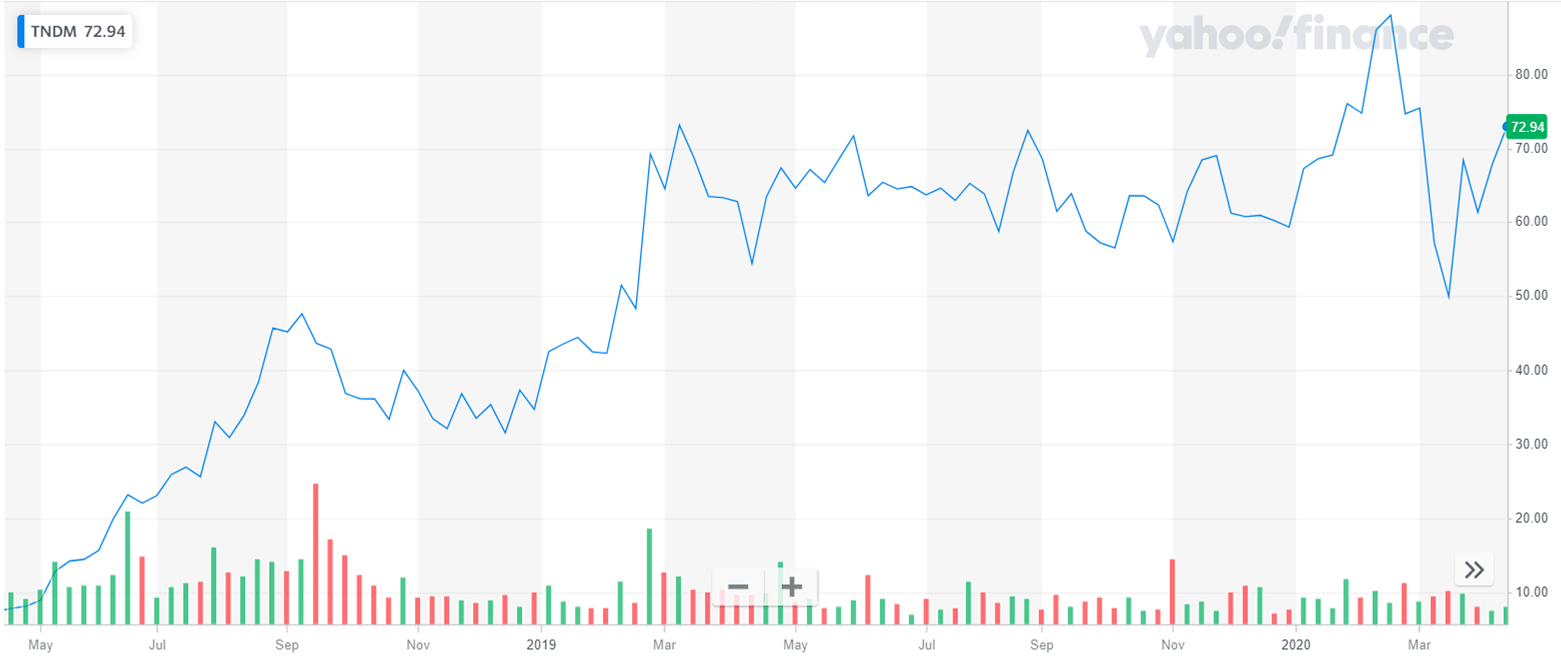

Last month, Tandem Diabetes Care (TNDM) became one of the unexpected victims of the coronavirus pandemic. The stock fell from $60.21 on January 2 to $54.54 on March 23. The stock is already up and closed at $72.94 on April 17. While the company is up by 22.36% YTD (year-to-date), there is still quite some room for growth left for the stock.

Tandem Diabetes Care is a MedTech company focused on manufacturing insulin pumps for diabetes patients. The company is focused on both type 1 and type 2 diabetes patients who require insulin pumps to control their blood sugar levels. Since the first commercial launch in 2015, the company’s signature insulin pump, t: slim X2, has been witnessing robust uptake both in the U.S. and ex-U.S. markets. In all, the company has launched 7 different insulin pumps to date. Tandem Diabetes Care has also been constantly innovating with the pump and has included additional features such as Basal-IQ and Control-IQ automated insulin delivery technology. The company currently accounts for a 20% share of around 600,000 patients in the U.S. who use insulin pumps. A leading market share coupled with a robust financial profile has pushed Tandem Diabetes Care to the limelight in April.

{kind=link}

Tandem is targeting a huge underserved market opportunity in diabetes space

According to Meticulous Research, the digital diabetes market is expected to grow at a high single-digit CAGR (compound annual growth rate) and be worth $16.33 billion by 2026. The research agency has estimated the digital diabetic device global market to grow at a mid-single CAGR, while the apps and software global market to grow at a strong double-digit CAGR from 2019 to 2026.

As seen in the diagram, around 70% of insulin-dependent diabetes patients are still on MDI (multiple-dose injection) therapy. The percentage is even higher in ex-U.S. markets. This highlights the significant growth opportunity available for Tandem Diabetes Care to further penetrate in the existing diabetes market. Besides, we also have existing pump users requiring to renew the device presenting a significant market opportunity for Tandem. The company is now looking forward to increasing its user base from 142,000 at the end of 2019 to 500,000 by 2025. While the company serves both type 1 and type 2 diabetes patients, the former account for around 90% of the customer base.

Tandem has been focused on meaningful innovations in the digital diabetes space

Launched in 2016, Tandem has positioned its flagship product, t: slim X2, as a much more user-friendly yet equally effective and safe insulin pump as compared to the older Medtronic MiniMed 670G. Patients have been impressed with t: slim X2’s features such as small size, low weight, large touchscreen, Bluetooth compatibility, and automatic software updates. The company has developed two innovative algorithms, Basal _IQ, and Control-IQ, to further improve the usability of the t: slim X2 insulin pump.

Tandem Diabetes Care’s Control-IQ algorithm has been approved for use with t: slim X2 insulin pump and DexCom’s (DXCM) G6 continuous glucose monitoring tool to form a complete AID (automated insulin dosing) system. In March 2020, the company also announced FDA clearance of its Basal-IQ technology platform as an interoperable device. This can open doors for multiple innovations and opportunities for the company to combine capabilities of its automated glycemic controller with hardware from other device manufacturers.

The company is expected to report significant improvement in financials in 2020, despite higher planned investments

In the fourth quarter, Tandem shipped 19,602 insulin pumps, a YoY increase of 21%. The company’s sales also jumped YoY by 42% to $108.4 million in the fourth quarter. However, the $18.9 million in non-cash charges related to stock-based compensation and a change in the fair value of warrants led to a 27% YoY decline in the company’s net income of $2.7 million.

In 2019, Tandem shipped 73,431 insulin pumps, a YoY increase of 113%. The company’s sales were up by 97% to $362.3 million. The company reported a loss of $24.75 million in 2019.

Tandem Diabetes Care has guided for revenues of $450 million-465 million for fiscal 2020, a YoY increase of 24-28%. This may seem low, considering that the company almost doubled revenues in 2019 on a YoY basis. However, we should remember that we are now working with a much higher revenue base. The company expects gross margin to be 54% and adjusted EBITDA margin to be 12-14% in fiscal 2020. I believe there is a slim chance of the company revising down its fiscal 2020 guidance in its first-quarter earnings call. The company is exuding confidence in its operations as well as consumer demand, which cannot be said for many companies in such uncertain times.

Investors should be aware of these risks

Tandem Diabetes Care may witness some supply disruptions in the coming months since the company has few component suppliers in China and Mexico. The company may also require to curtail its marketing and training activities as COVID-19 may force people to practice social distancing for many more months to come. The delay in the launch of t: sport device to 2021 has also disappointed investors.

Safety incidents related to the insulin pump can be a major challenge for the company. In October 2019, FDA reported a death which was then linked to malfunctioning of tandem’s insulin pump. However, after investigation, it was found that the death was prescription drug-related and unrelated to tandem’s insulin pump or supplies. Although Tandem had refuted the role of the pump in the patient’s death, the company’s shares did suffer in October 2019.

Tandem Diabetes Care is also facing tough competition from another insulin pump manufacturer, Insulet (PODD). The exit of Roche Holdings (OTCQX:RHHBY) and Johnson & Johnson (JNJ) from the insulin pump business in 2016 and 2017, respectively, came as a relief for Tandem. However, Insulet continues to be a pretty formidable foe. Insulet’s fiscal 2019 revenues grew YoY by 31% YoY to $738.2 million. Although tandem’s revenues rose 97% to $362.3 million in 2019, these are almost half of Insulet’s fiscal 2019 revenues on an absolute basis. Luckily, both companies have significant room for growth considering the sheer size of the type 1 diabetes market and the less saturated automated insulin pump market.

Although Tandem Diabetes Care has emerged as a pioneer in the development of the first-ever hybrid closed-loop insulin management system, competition is not far behind. Although Medtronic’s (MDT) MiniMed 670G insulin pump has fallen out of favor, the company is expected to launch the next-generation MiniMed 780G AID system in 2020. Similar to Control-IQ, MiniMed 780G will also be a closed-loop system adjusting insulin doses automatically based on the patients’ blood sugar level. This will also not require constant manual adjustment of the pump and maybe even more appealing as it is being designed to be connected with smartphones.

Insulet is also working to launch Omnipod Horizon, the first-ever tubeless, personal smartphone-controlled AID system. The company is integrating DexCom’s G7 CGM into Omnipod Horizon. The company has also collaborated with Abbott Laboratories (ABT) to develop an on-body AID system, next-generation Libre sensor. A European company, Diabeloop, may also consider commercializing its already EU-approved DBLG1 closed-loop insulin monitoring and pump system, in the U.S. Finally, the open-source artificial pancreas system is also a competition for Tandem’s insulin pump.

A bigger risk for Tandem is the potential launch of drugs that can effectively treat or at least slow disease progression in type 1 diabetes patients. The top candidate is Provention Bio’s (PRVB) Teplizumab, currently in Phase 3 trials. I have already explained about the drug’s potential in type 1 diabetes indication in greater detail here.

The good news, however, for Tandem is that Teplizumab is targeting patients at high risk of type 1 diabetes and not those already suffering from the disease. This implies that Teplizumab is currently not targeting the existing diabetic market. Besides, Teplizumab will enter the market earliest by 2022. Hence, while this drug can hamper the growth rate of type 1 diabetes patient population, Tandem and other insulin pump manufacturers can continue to serve the already huge existing patient population.

What price is right here?

According to finviz, the 12-month consensus target price of Tandem Diabetes Care is $88.07, 20.74% higher than the previous close. The company is currently trading at a forward PE (price-to-earnings) multiple of 248.94x, which is pretty steep. However, Tandem is essentially a growth stock. Based on the market-leading position in a huge market, continued focus on innovation, and stable financials, I believe that the target price of $88.07 is a fair representation of the company’s growth potential.

Tandem’s relative resilience to COVID-19 pandemic disruptions is also a key appealing factor for investors. In March, the company had announced that its warehouse and manufacturing facilities have been operating as normal despite the pandemic. The company is also not expecting a significant supply chain and shipment disruptions in the coming months. This announcement is a welcome change from those being put out by the majority of other companies across the world.

Analysts are mostly giving mixed opinions for the stock. On March 23, Guggenheim analyst Chris Pasquale downgraded Tandem Diabetes to Neutral from Buy. On March 4, Citi analyst Joanne Wuensch initiated coverage with a Neutral rating and an $89 price target.

On February 25, Lake Street analyst Brooks O’Neil reiterated Buy rating and a $100 target price. Craig-Hallum analyst Alexander Nowak raised his price target to $108 from $92 and reiterated Buy rating. Oppenheimer analyst Steven Lichtman raised his price target from $84 to $97 and reiterated Buy rating. Raymond James analyst Jayson Bedford raised his price target for Tandem Diabetes to $91 from $85. Cowen analyst Ryan Blicker raised his price target to $90 from $85 and reiterated Outperform rating. Piper Sandler analyst Matt O’Brien raised the target price from $70 to $90 and reiterated Outperform rating.

I believe investors should pick up Tandem at current levels, as a part of a large diversified portfolio. Chances of significant first-quarter underperformance and substantial downward revision of fiscal 2020 guidance seem low. Hence, retail investors with above-average risk appetite and investment tenure of at least one year should start considering picking up Tandem Diabetes Care in April 2020.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment