jejim

Synopsys (NASDAQ:SNPS) is one of the global leaders in EDA tools and solutions to bringing the age of smart technology into everyday life. It is well known for its Semiconductor and System solution designs services. The company also provides leading software tools that improve software security.

SNPS remains fundamentally stable despite today’s bearish macro environment. In fact, the company managed to lower its total debt and has a $300 million accelerated share buy catalyst. However, in terms of setting up price action expectations, I believe SNPS may print a potential lower swing high, which may offer investors and traders a better long opportunity with a wider margin of safety.

Company Overview

SNPS ended FY ’22 with a top line of $5,081.5 million, up 20.87% from its $4,204.2 million recorded in FY ’21. This growth rate remains greater than it was pre-pandemic, demonstrating resilience against today’s uncertainty. Despite the possibility of a recession next year, experts remain optimistic about the company’s rising top line.

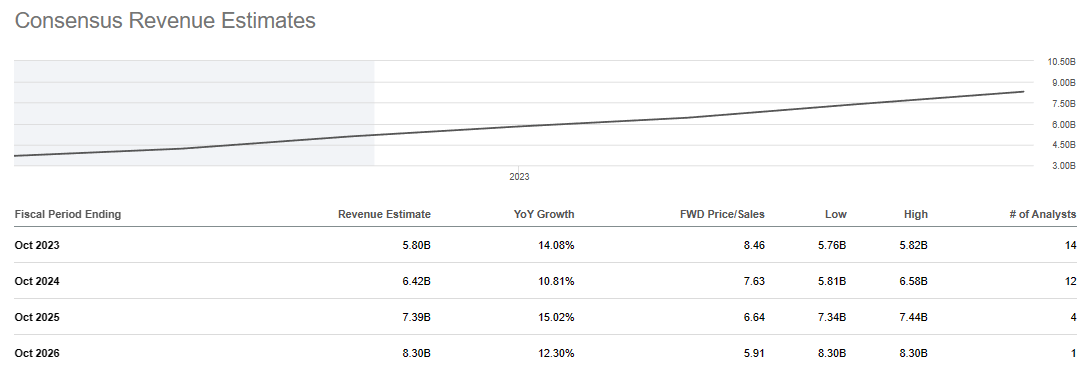

SNPS: Growing Consensus Revenue Estimate (Source: Data from SeekingAlpha)

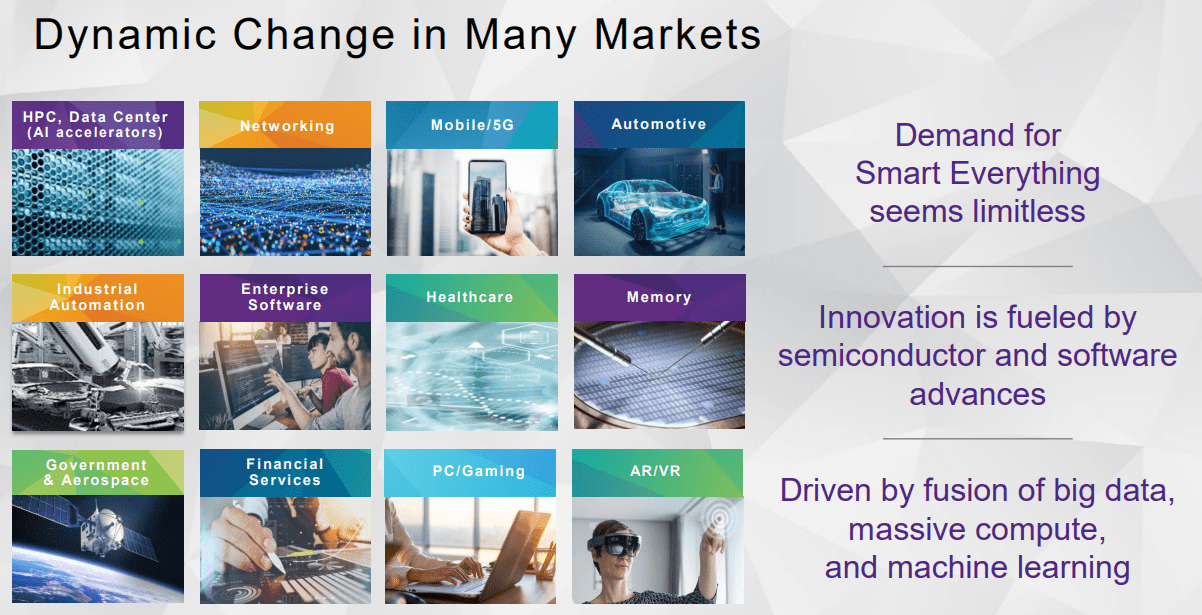

Management expects continued growth in demand as we continue to move towards digitalization. SNPS, in particular, is strategically positioned “in the Heart of Accelerating Electronics Innovation,” and as a result, it continues to benefit from its long-term tailwinds as shown in the image below.

SNPS: Dynamic Change in Many Markets (Source: Investor Presentation 2022 )

In fact, SNPS boasts a growing Time-Based Products Revenue growing 14% YoY on a comparable basis, better than 11% YoY recorded in FY ’21 and better than 8% in FY ’20. Additionally, total deferred revenue of the company remains growing, as shown in the image below, making SNPS fundamentally stable despite the pandemic and today’s challenging operating environment.

SNPS: Growing Deferred Revenue (Source: Data from SeekingAlpha. Prepared by the Author)

According to management, they have a large non-cancellable backlog and a positive demand environment for FY ’23, as quoted below.

In addition, our time-based business model, with $7.1 billion of non-cancelable backlog and a diversified customer base, all provide stability, resilience and forward momentum. While fully mindful of the macro dynamics around us, including the most recent US government export restrictions, Synopsys is poised for strong results in fiscal 2023. Source: Q4 2022 Earnings Call Transcript

Continued Growth Expansion

Management also sees continued growth in their Software Integrity segment. In fact, this segment contributes $465.8 million only this FY ’22 and estimated by the management to continue growing as quoted below.

Notably, we saw good progress with the go-to-market and product initiatives introduced last year. Our indirect channel partner business, for example, continues to ramp well by expanding our reach into customer groups and geographies that we haven’t connected with in the past. We are building momentum with the goal of another significant increase in indirect sales in FY 2023.

On the product side, we expanded our offerings by launching two new SaaS services for static analysis and open-source analysis integrated into our Polaris platform. We expect these SaaS capabilities to accelerate adoption and consumption of our solutions as they are particularly well-suited to growth in the mid-market. Source: Q4 2022 Earnings Call Transcript

Remains Fundamentally Stable

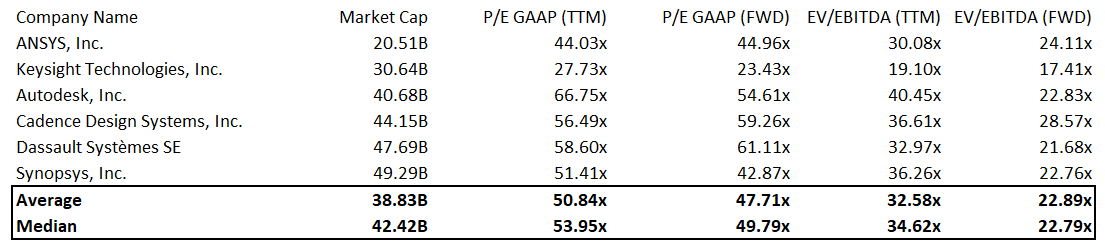

SNPS: Relative Valuation (Source: Data from SeekingAlpha. Prepared by the Author)

ANSYS, Inc. (NASDAQ:ANSS), Keysight Technologies, Inc.(NYSE:KEYS), Autodesk, Inc. (NASDAQ:ADSK), Cadence Design Systems, Inc. (NASDAQ:CDNS), Dassault Systèmes (OTCPK:DASTY).

SNPS is trading at a trailing P/E of 51.41x, which is lower than its selected peers’ median of 53.95x as shown in the image above, and trading below its P/E 5-year average of 76.77x. However, looking at its trailing EV/EBITDA of 36.26x, shows some premium compared to its peers’ median of 34.62x and fairly trades to its EV/EBITDA 5-year average of 36.50x. In these comparisons, we can plainly see that SNPS’s value is better than that of its peer CDNS, but this, in my opinion, will not result in a significant discount.

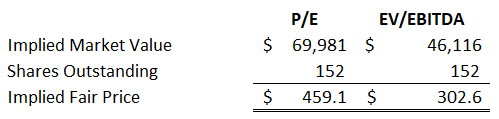

SNPS: Relative Valuation (Source: Prepared by the Author)

Putting these into consideration, generously, at an implied P/E of 49.79x and EV/EBITDA of 22.89x and using analyst’s EPS estimate of $10.33 and EBITDA $2,127 million in FY ’23 and applying a 10% discount, we can arrive at an average fair price of $380 or 19% upside potential as of this writing. I believe a price below $295 will provide a better margin of safety to consider.

Keep an Eye on This Consolidation

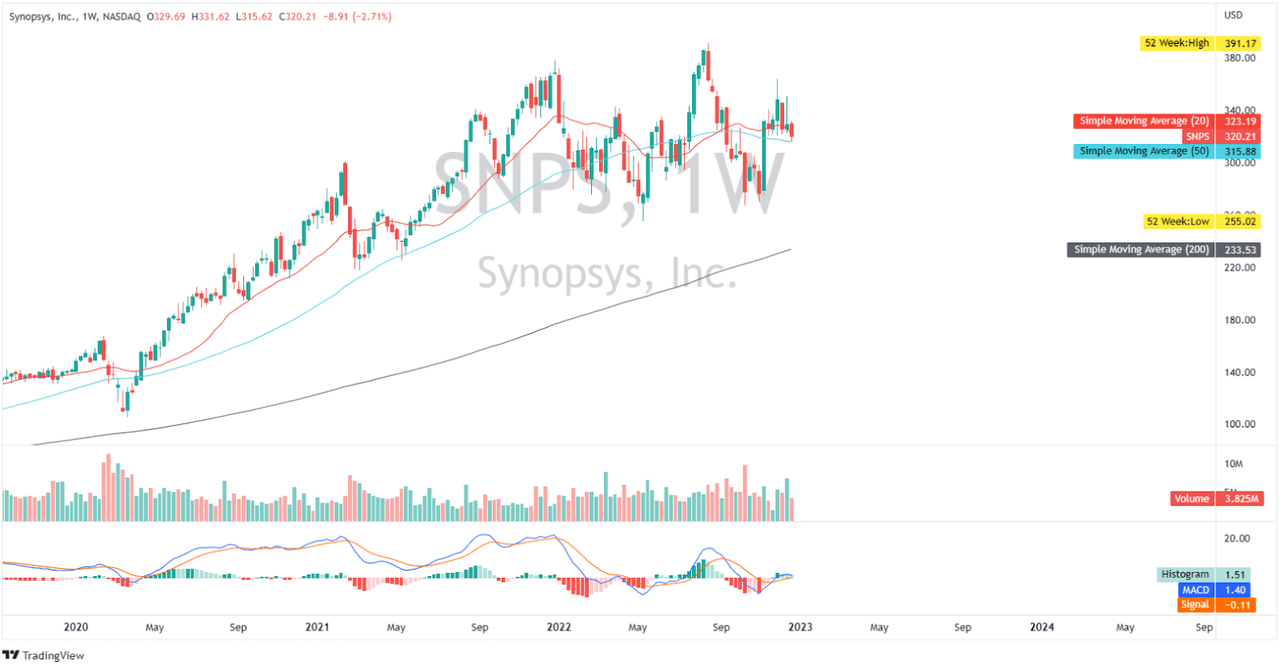

SNPS: Weekly Chart (Source: Author’s TradingView account)

Currently, SNPS is consolidating between $308 and $368. It has had difficulty breaking out of its $368 zone and has the potential of printing a lower swing high this December. Investigating its MACD indicator, we can see its Signal line in negative territory implying some bearish price. In fact, potential bearish crossover from its MACD and Signal line will add bearish confluence and should be monitored. If this occurs, it will give a safer entry point than the current price action.

Undisrupted Operating Margin

Another factor that is helping is that SNPS has kept its growing margin despite the economic crisis we have been going through, as can be seen in the image below.

SNPS: Growing Margin Trend (Source: Data from SeekingAlpha. Prepared by the Author)

This additional efficiency comes from the company’s effective partner model and as mentioned earlier, management sees positive momentum with their indirect channel partners contributing positively on SNPS’s overall operating margin. Finally, the management provided a reassuring FY ’23 outlook, as quoted below.

For fiscal year 2023, the full year targets are; revenue of $5.775 million to $5.825 billion; total GAAP costs and expenses between $4.49 and $4.537 billion; total non-GAAP costs and expenses between $3.81 billion and $3.84 billion, resulting in a non-GAAP operating margin improvement of more than 100 basis points; non-GAAP tax rate of 18%; GAAP earnings of $10.28 to $10.35 per share, cash flow from operations of approximately $1.7 billion. Source: Q4 2022 Earnings Call Transcript

However, we can witness a decline in its cash flow from operations of $1.7 billion (versus $1.739 billion in FY ’21), despite a higher expected stock-based compensation expenditure of $582 million to $594 million on average in FY ’23. This represents a negative sentiment on its forward Price/ Cash flow ratio of 28.42x, which is much higher than its five-year average of 30.97x.

Final Key Takeaway

The management posted a reassuring outlook for its FY ’23 and it seems achievable thanks to its huge backlogs. However, considering today’s macro uncertainties, I would not be aggressive to enter today’s level, especially with the potential recession which might affect SNPS’s customer spending behavior. Overall, SNPS is fundamentally stable and any fear-driven dip will present a chance to purchase this stock at a lower cost.

Thank you for reading and happy holidays everyone!

Be the first to comment