dimitris_k/iStock Editorial via Getty Images

The collapse of SVB Financial Group (NASDAQ:SIVB) late last week came as a surprise to many and investors are left wondering if any other financial institutions will fail in the coming weeks. While subtle, SVB Financial’s latest financial statements showed that there were cracks forming in the bank as early as last year and some investors had already taken note. SVB’s stock had gone from massively outperforming its peers to cratering below the S&P 500 and NASDAQ index returns in 2022.

SEC 10-K

From a regulatory standpoint, everything looked fine. The bank was well above the regulatory requirements for risk-based capital and leverage. These regulatory ratio requirements were established in the wake of the financial crisis of 2008. Of interest is the CET1 risk-based capital, which consists of common equity tier 1 capital. This is the measurement of the bank’s liquid holdings against risk.

SEC 10-K

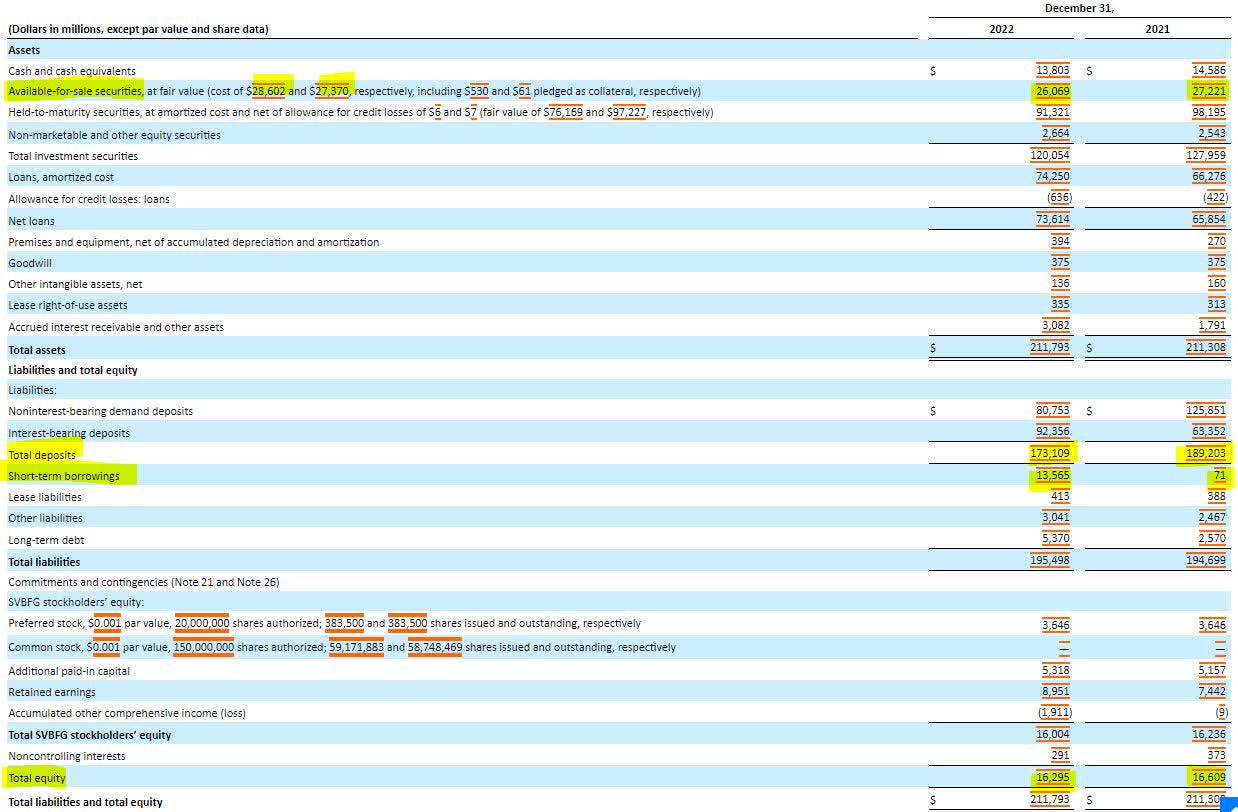

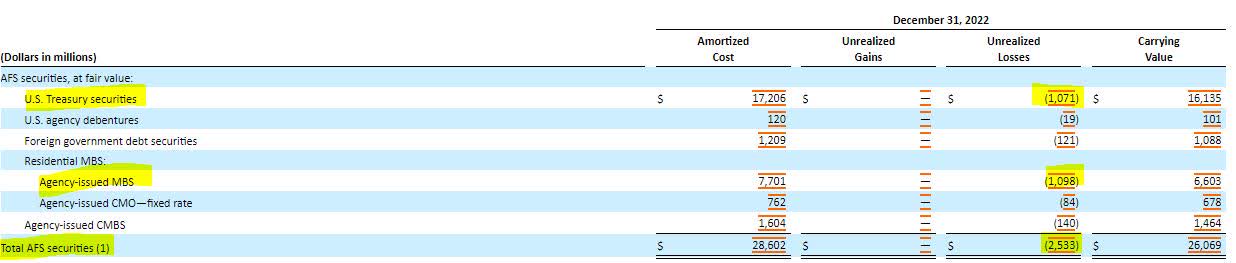

The bank’s balance sheet shows signs of the first problem. SVB Financial held $26 billion of securities listed for sale, but according to the notes, the securities cost $28.6 billion, an implication that it was underwater on these securities. The bank also saw a $16 billion decrease in total deposits which it supplemented with $13 billion of short-term borrowings. Taking on short term debt is a good way to avoid having to sell securities at a loss.

SEC 10-K

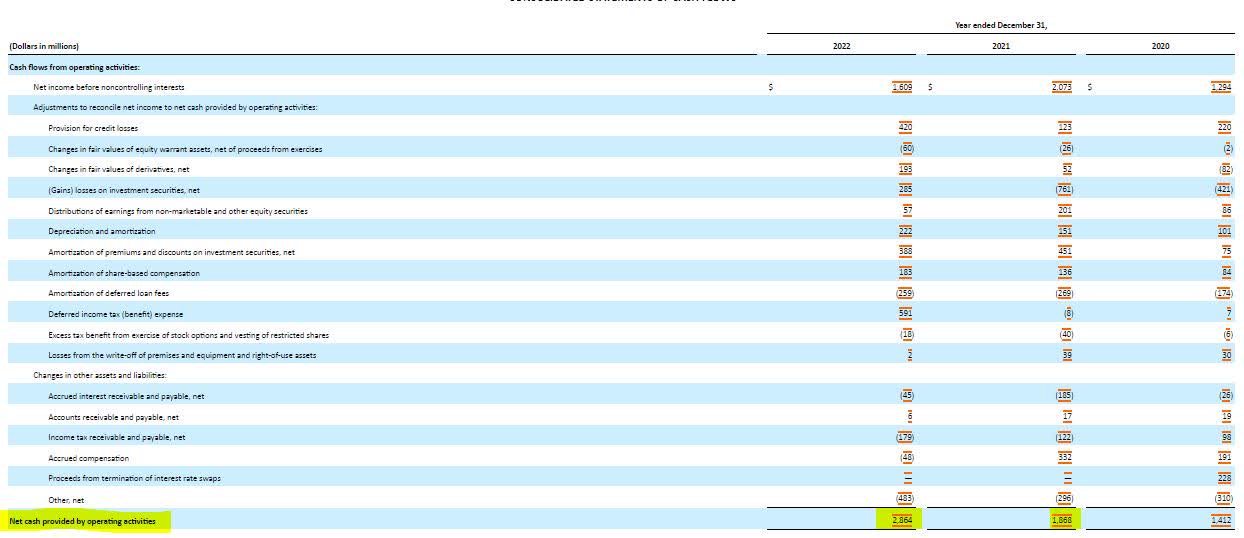

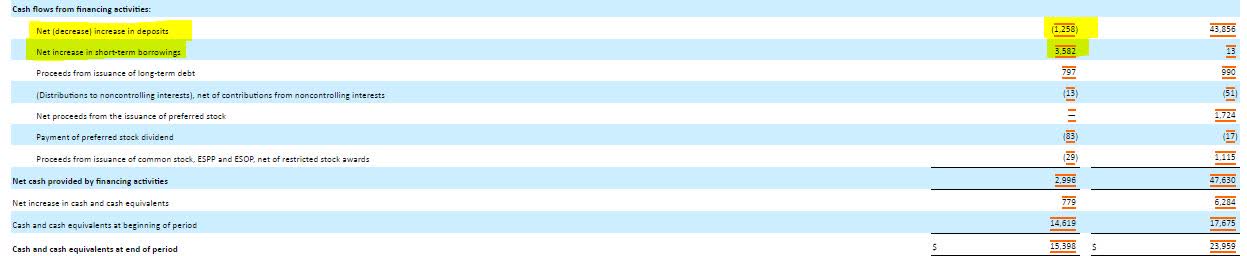

The cash flow statement shows that the company’s earnings generated a strong cash flow from operations. In the financing section of the cash flow statement, the $16 billion decrease in deposits is noted. The bank covered these funds by borrowing $13.5 billion in short-term debt and more than $2.5 billion in long term debt. Of the $16 billion in deposit outflow, $13 billion occurred during the second half of 2022.

SEC 10-K SEC 10-K Q2 2022 cash flow shows deposit outflow barely starting (SEC 10-Q)

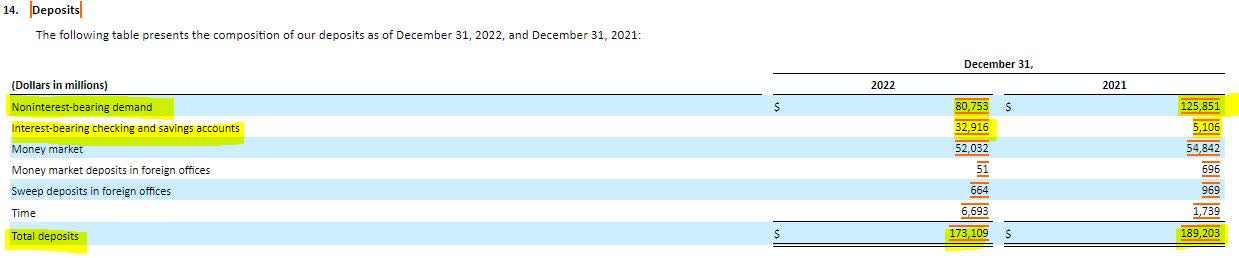

Digging further into the bank’s deposits reveals a larger shift from the bank’s customers. During 2022, the bank’s depositors shifted $45 billion out of noninterest bearing accounts. $29 billion of that money found itself in other types of accounts, mostly in interest bearing checking and savings accounts. Whether it was due to the overall liquidity of the bank’s customer base or the desire to seek higher yields, it remains to be seen why that shift occurred in 2022, but I suspect it was a little of both.

SEC 10-K

Thursday morning, the shock regarding SVB Financial hit when the bank announced it needed to raise capital and had sold all its AFS securities, taking a more than $2.5 billion realized loss. These losses existed as unrealized losses prior to the sale and were disclosed in the bank’s February 10-K filing. The bank’s investments in Treasury securities and Agency issued MBS, considered the two safest types of investments out there, had each lost over $1 billion.

SEC 10-K

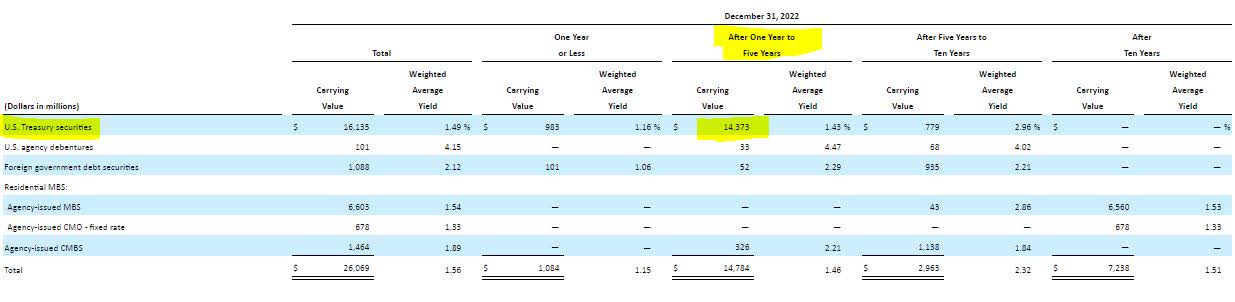

The truth of the matter is that SVB Financial had purchased these investments when interest rates were exceptionally low. While these investments are safe if held to maturity, their inherent value will decline as interest rates rise. In the case of the Treasury investments, SVB opted to buy Treasuries maturing between one and five years out.

SEC 10-K

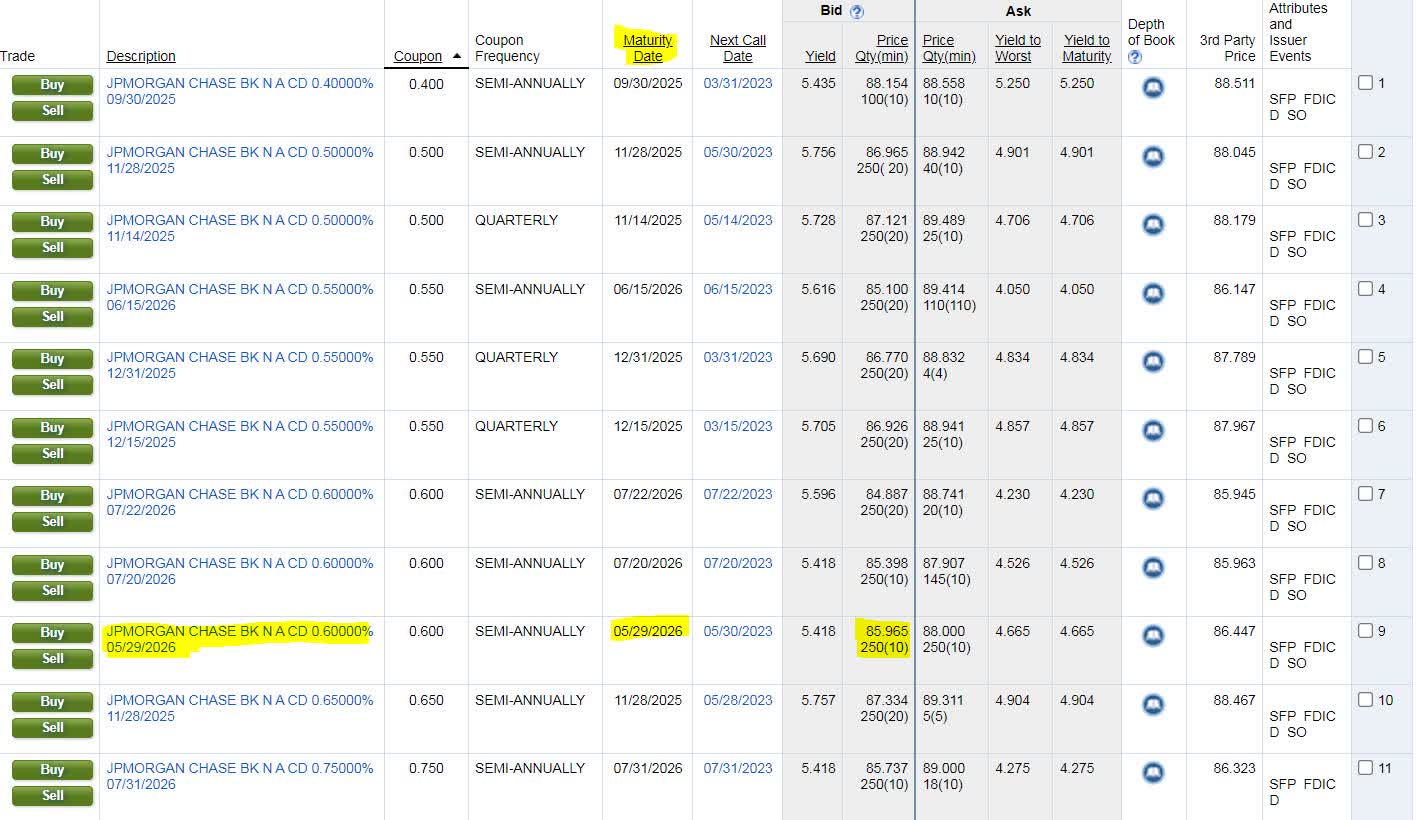

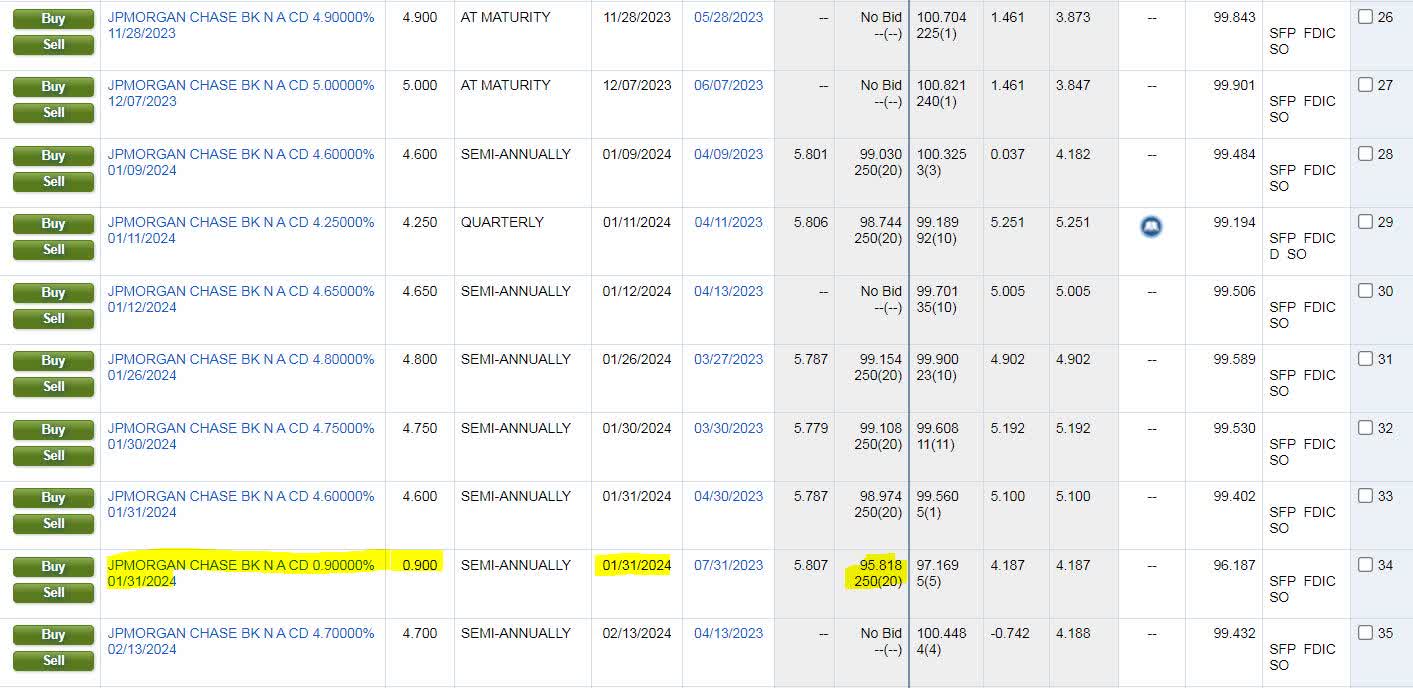

The prices of these bonds have been subjected to exceptional volatility as interest rates have risen so quickly. Had the bank opted to purchase Treasuries maturing in six months or less, they would have been subject to far greater price stability and constant liquidity from the maturity of short-term investments. An example of this can be found when looking at the prices of low coupon CD’s. Someone who purchased a JPM 0.6% coupon CD at issuance would need to take a 15% loss to sell it today versus a 5% loss for a comparable CD coming due in 10 months.

Fidelity Fidelity

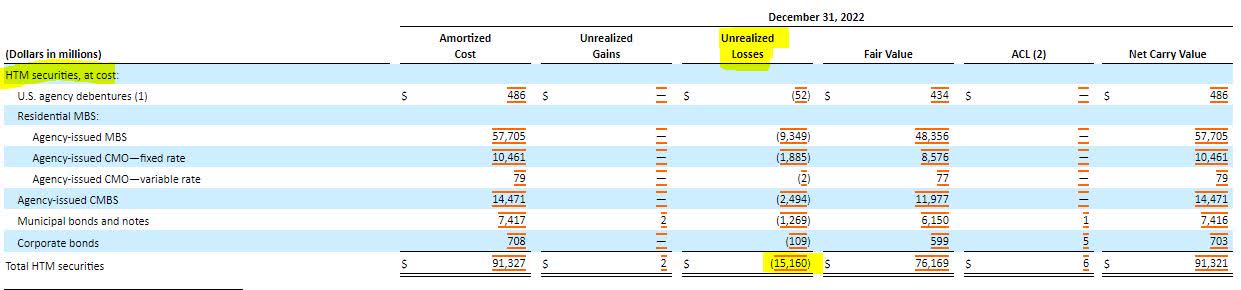

While the available for sale securities got the most attention, the unrealized losses spread further than that. There was an additional $15 billion in unrealized losses in the securities that the bank was planning to hold to maturity. The bank was out a shocking $9.3 billion or 15% in its agency issued mortgage backed securities alone.

SEC 10-K

The presence of unrealized losses is going to be a big topic next month as banks release their first quarter earnings. If banks are going to have to book massive losses (and subsequently induce panic) to convert securities into cash, the question must be asked, how much liquidity really exists?

Be the first to comment