One of the things we will talk a lot about in the future is supply chain reconfiguration. We have discussed it in the past, but we haven’t covered a lot of actionable investment ideas. That is about to change. In this article, I will do two things. First, we will discuss global supply chain relocation efforts and why that benefits the United States. The pandemic proved that supply chains need to be more resilient. This includes reducing geopolitical risks.

Moreover, overseas (i.e., in Europe) economic fundamentals are weakening, making the United States and North America, in general, an excellent target for higher manufacturing investments (re-shoring). Hence, the second thing I’m going to do is provide you with three investment ideas. They all pay a dividend. Two are REITs. One is a transportation company combining all three North American nations after a pending 2023 merger.

I own one of them and will add another one in 2023.

I believe that all picks will outperform the market on a long-term basis, offering investors high-quality dividends and healthy balance sheets.

So, without further ado, let’s get to it!

Supply Chain Reconfiguration

Supply chains are extremely complex. Even since the pandemic, all eyes are on the complexity of global trade, production chains, and related.

There are two things I’m increasingly looking for. One of them is a shift toward North American nations as a result of supply chain reconfiguration. Even China is moving production to Mexico to avoid certain tariffs. The other thing I’m looking for is a move from European companies to North America. This allows them to be closer to their customers and avoid unfavorable regulations’ negative impact (i.e., the ones causing the energy crisis).

The other day, I read the Government Trends 2022 report from Deloitte.

Deloitte gave us three factors that accelerate the trend toward improved supply chain resilience.

Global supply chains have become more interdependent.

Lean supply chains are increasingly subject to external shocks.

Rising geopolitical tensions among trading partners heighten the risk.

Re-shoring supply chains is a difficult process. It is also expensive. For example, China controls 90% of rare metals (mainly due to processing capacities). Controlling commodities will mean trade partners cannot easily move production out of a country.

Also, moving production out of low-wage nations means that investments in technology and related will have to lower overall costs. I kept that in mind in my stock selection.

After all, there is a reason why companies moved to China: it was cheaper. Reconfiguring supply chains is inflationary.

Hence, so far, the focus was on supply chain adjustments. According to Deloitte:

Governments may not be able to conjure up entire domestic industries or supply chains. But they can bolster resilience by evaluating the strength of critical industries, improving supply chain awareness, and cultivating links with trusted foreign nations and suppliers. In 2021, India, Japan, and Australia partnered to enhance the resilience of Indo-Pacific supply chains. Under their Supply Chain Resilience Initiative, these nations agree to share best practices on resilience and hold investment promotion and buyer-seller matching events to encourage businesses to diversify their supply lines.

As a European who has commented a lot on these issues, I can say that European multinationals are indeed changing their plans. Volkswagen, for example, will move production to its largest markets (China & USA), Siemens and BASF are both divesting in Germany, and increasing energy price differentials continue to favor the United States.

Reuters

This is what Bloomberg wrote with regard to this terrible investment environment:

Last week, Thomas Schaefer, one of the most senior executives at Volkswagen AG, publicly said what many other business people and policy makers had only raised in private. “When it comes to the cost of electricity and gas, in particular, we are losing more and more ground,” he said, warning that unless prices fall quickly, investment in Europe will be “practically unviable.”

Not only that but there are many more reasons to be bullish on US manufacturing. In August, McKinsey & Company wrote a paper titled “Delivering the US manufacturing renaissance”.

According to the report:

For some companies that supply US markets, the evolution of factor costs has significantly eroded the comparative advantage of global production locations and supplier networks. When organizations expand their definition of value to take account of sustainability issues and supply chain risks, the gap can narrow even further.

Moreover

That shift could unlock a wave of regionalization in the world’s manufacturing networks as companies develop shorter, more resilient, and more adaptable supply chains that better serve the needs of different markets. Across key manufacturing sectors, our analysis suggests that up to $4.6 trillion in global trade could shift across regions in the next five years (Exhibit 4).

McKinsey & Company

Moreover, US manufacturing has become much more efficient. Most companies put most of their profits back into the business, creating a framework similar to the ones in Germany (to name a highly successful manufacturing nation).

Also, once the ball starts to roll, the US is in a terrific place to boost re-shoring benefits even more.

When you begin to nudge that a bit with industrial policy—as we are seeing with the Biden administration’s push around things like electric vehicles—suddenly you start to be able to connect the dots. An electric-vehicle production facility in South Carolina could perhaps connect with a textile maker in North Carolina, who then might be able to move from making clothing to making upholstery for an electric vehicle or, potentially, a cloth to cover wind turbines. I see a lot of potential there, and I think we’re only at the beginning of it being realized.

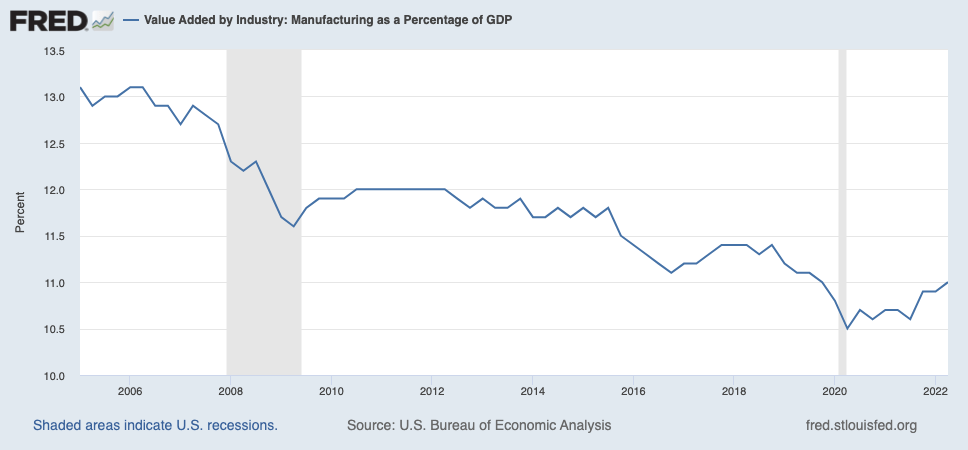

Don’t get me wrong, I don’t expect the US to “suddenly” benefit from a steep increase in manufacturing output. I believe it will be a gradual but steady process, benefiting domestic production as companies move out of China to North American nations, while European manufacturing will move closer to its customers. This, too, benefits North America tremendously, and I expect manufacturing to move back to 12% of GDP in the 5-7 years that lie ahead of us.

St. Louis Federal Reserve

With that said, there’s a reason I have zero dividend exposure in Europe. It has everything to do with these developments, which are currently coming to fruition. The US is looking better politically, energy security is much better, and now supply chains are strengthening.

While a lot of investments would benefit from that, I picked three. I own one of these and I am looking to add at least one more in 2023.

Don’t worry, the other picks in this article will have decent yields!

Canadian Pacific is one of my all-time favorite dividend growth stocks. Not because of its yield (it’s below 1.0%), but because of its ability to grow.

In September, I wrote an article focused on supply chain reconfiguration, and why CP shares would benefit from that.

Seeking Alpha

With a market cap of $77 billion, CP is one of North America’s largest public railroad companies.

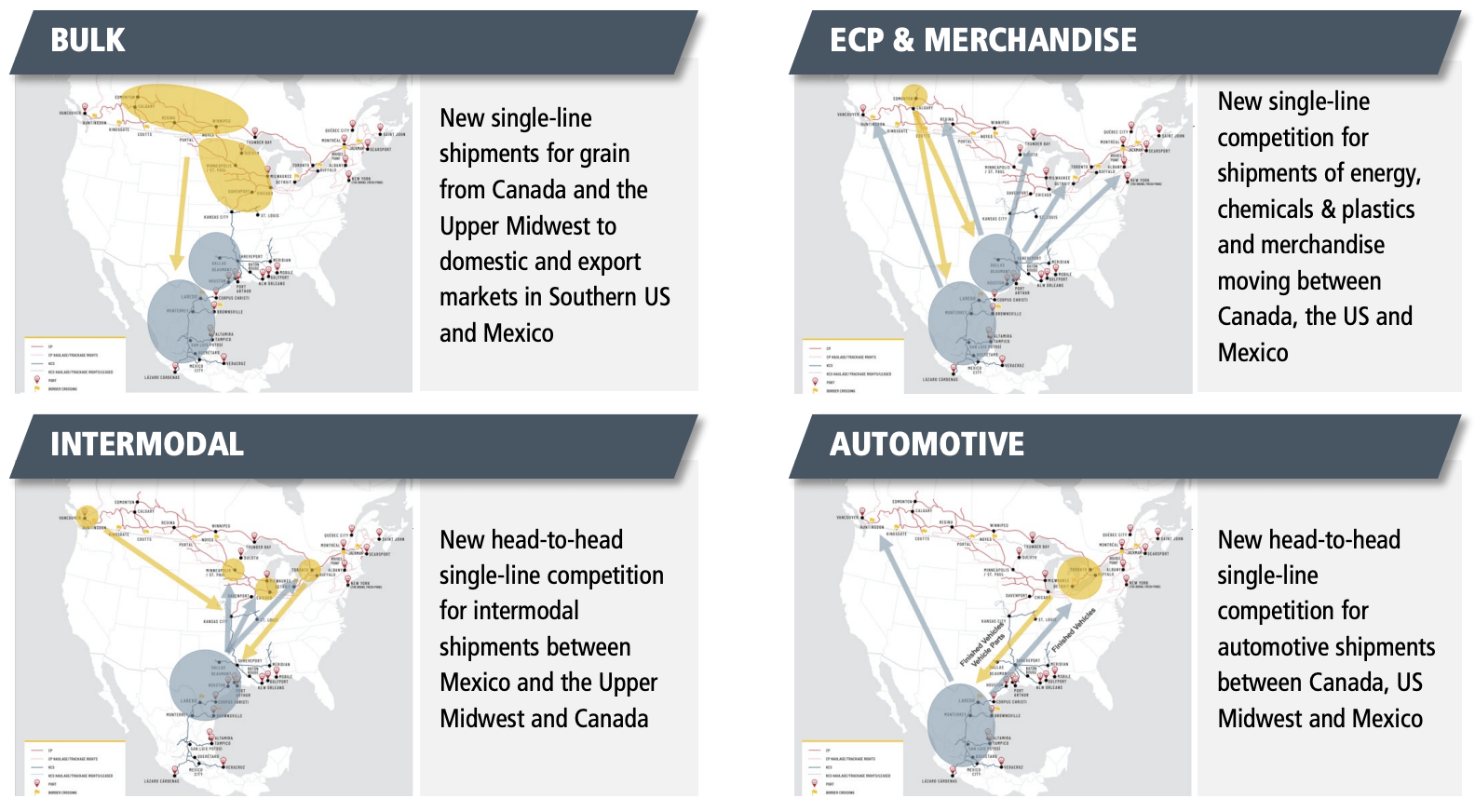

In early 2023, the company is expected to get STB approval, allowing the company to formally integrate Kansas City Southern. This deal would turn the company into the first railroad combining all three North American nations.

Canadian Pacific

While the company would not cover big parts of the United States, it would become a major player in the import, export, and domestic production of products in all major categories.

Canadian Pacific

It’s also good for the environment as it reduces the need for trucking on certain routes.

“CPKC will become the backbone connecting our customers to new markets, enhancing competition in the U.S. rail network, and driving economic growth while delivering significant environmental benefits. We are excited to reach this milestone on the path toward creating this unique truly North American railroad.”

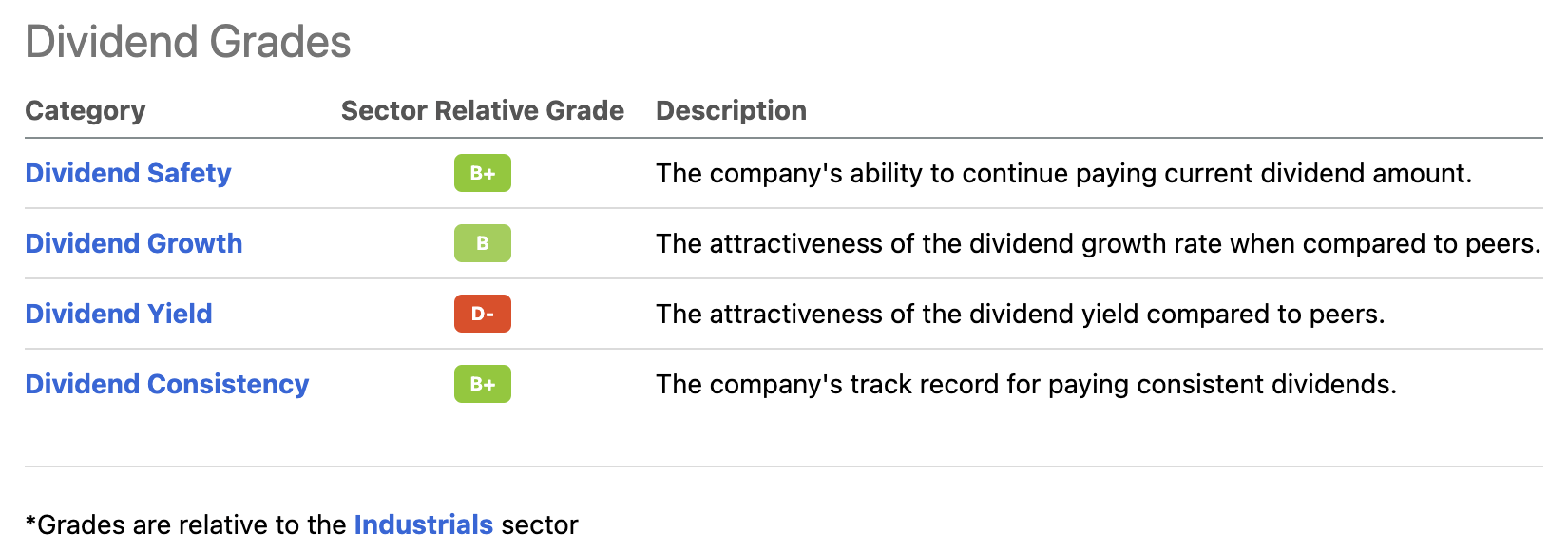

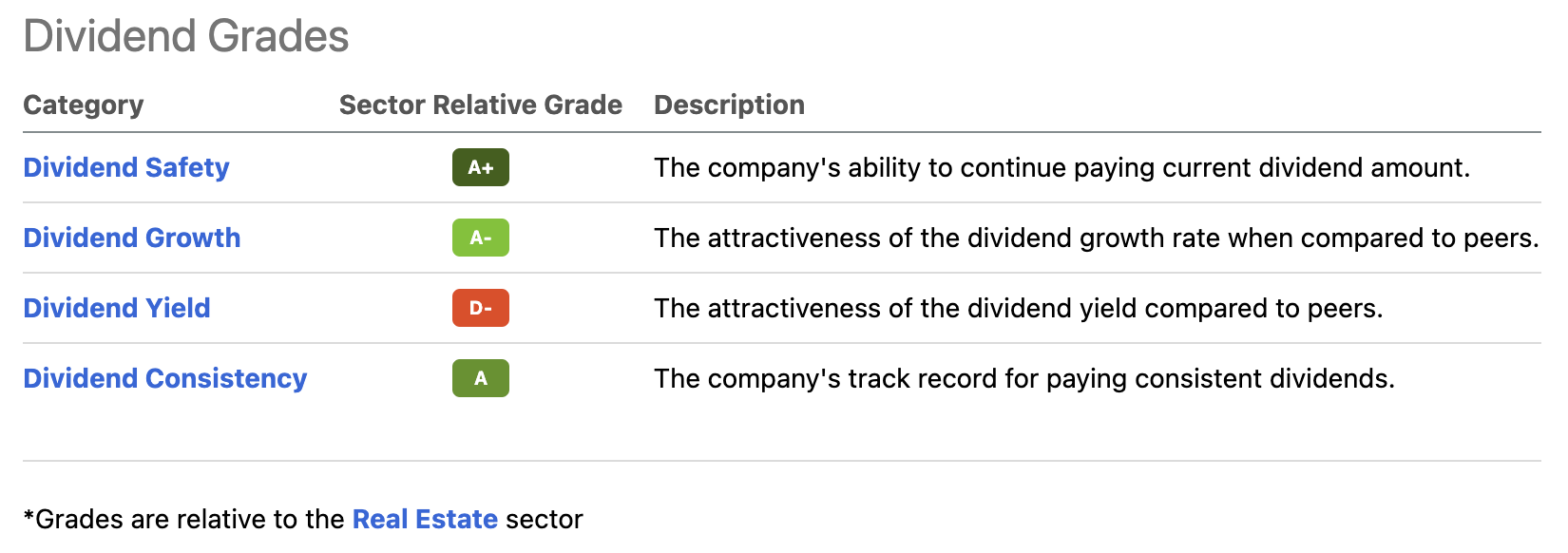

The company is not a traditional (well-known) dividend growth stock. Its low yield is one reason. However, the company scores high on safety, growth, and consistency.

Seeking Alpha

Over the past 10 years, the average annual dividend growth rate was 8.6%, which is OK, but not special.

The most recent hike was back in the September quarter of 2020 when management announced a 14.5% hike. In 2017, the company hiked by 12.5%. In 2016, the hike was 42.9%.

That’s not very consistent, but it follows the company’s progress. For now, the dividend is flat as the company is absorbing the KSU merger. I expect faster dividend growth after 2023.

Yet, CP is everything but a poor performer. To quote my own article:

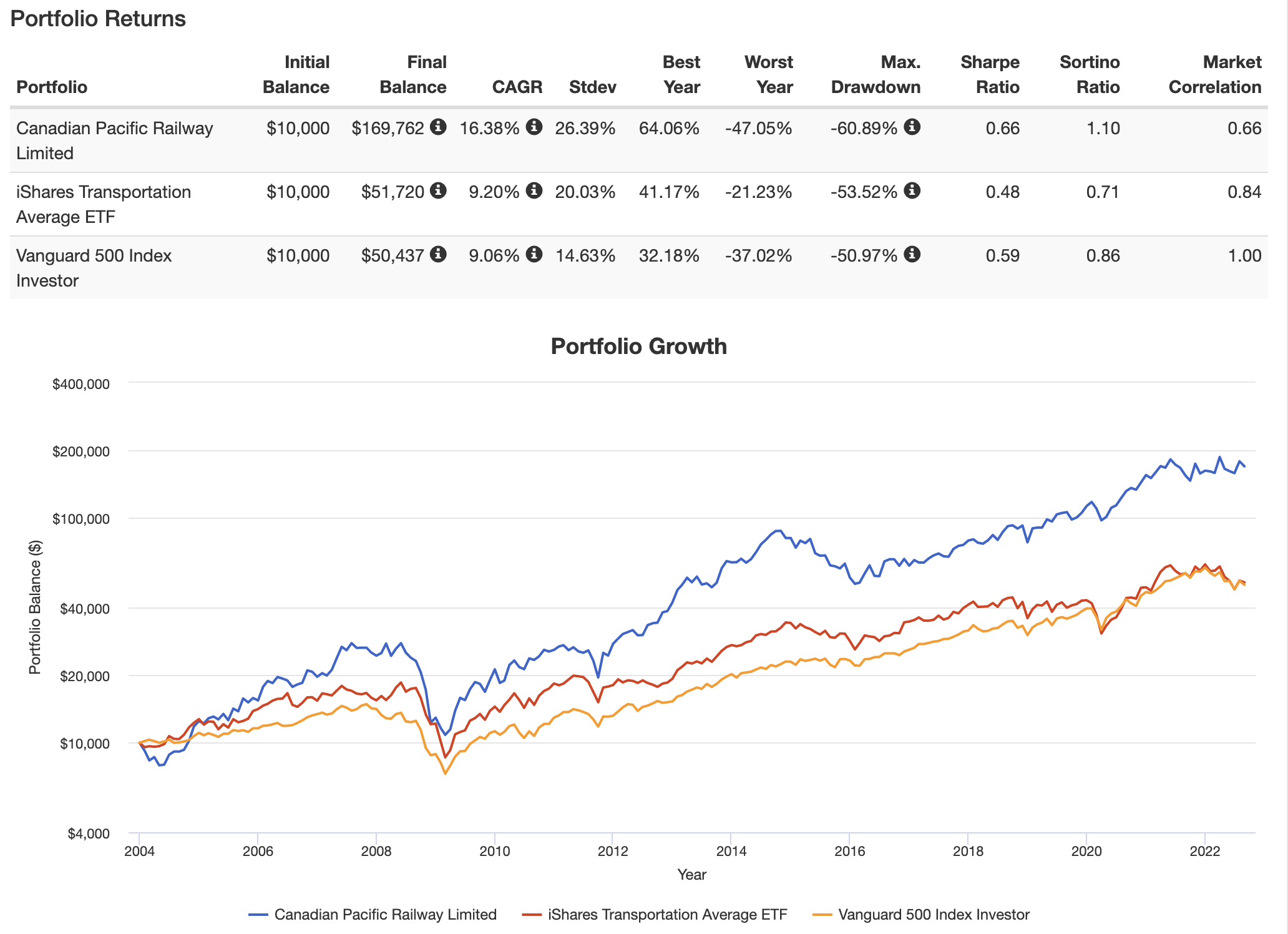

Since 2004 (and prior to that), the company has outperformed its transportation peers and the market. In this case, I’m using New York-listed CP shares that have returned 16.4% per year since 2004. This beats the market and the iShares Transportation ETF (IYT) by a wide margin. The standard deviation is (obviously) higher as we’re dealing with a cyclical company and a comparison with two baskets of stocks. Yet, even on a volatility-adjusted basis, CP shares have outperformed (Sharpe/Sortino ratios).

Portfolio Visualizer

In other words, CP may not be the best stock for income, but I sure believe it is a terrific dividend (growth) stock for investors looking to buy strategic assets, which I believe everyone should be doing.

This monthly dividend payer is an industrial REIT, as the name already partially gives away. According to the company, STAG…

[…] is a real estate investment trust focused on the acquisition and operation of industrial properties throughout the United States. By targeting this type of property, STAG has developed an investment strategy that helps investors find a powerful balance of income plus growth.

The company owns 563 properties in the United States (covering 41 states), totaling more than 111 million square feet. The occupancy rate of these assets is a stunning 98.2%, which I did not expect, to be honest. After all, the national vacancy rate is 4.0%, which means that STAG has an above-average occupancy rate.

Moreover, the company owns just 0.7% of its target asset “universe”, which it estimates to be close to $1 trillion. The company aims to outgrow its peers with an investment strategy that enhances the ability of industrial firms to create value. That sounds simple, but it’s tricky, and it needs to incorporate ongoing tends to be successful. So far, STAG has done a tremendous job supporting US manufacturers.

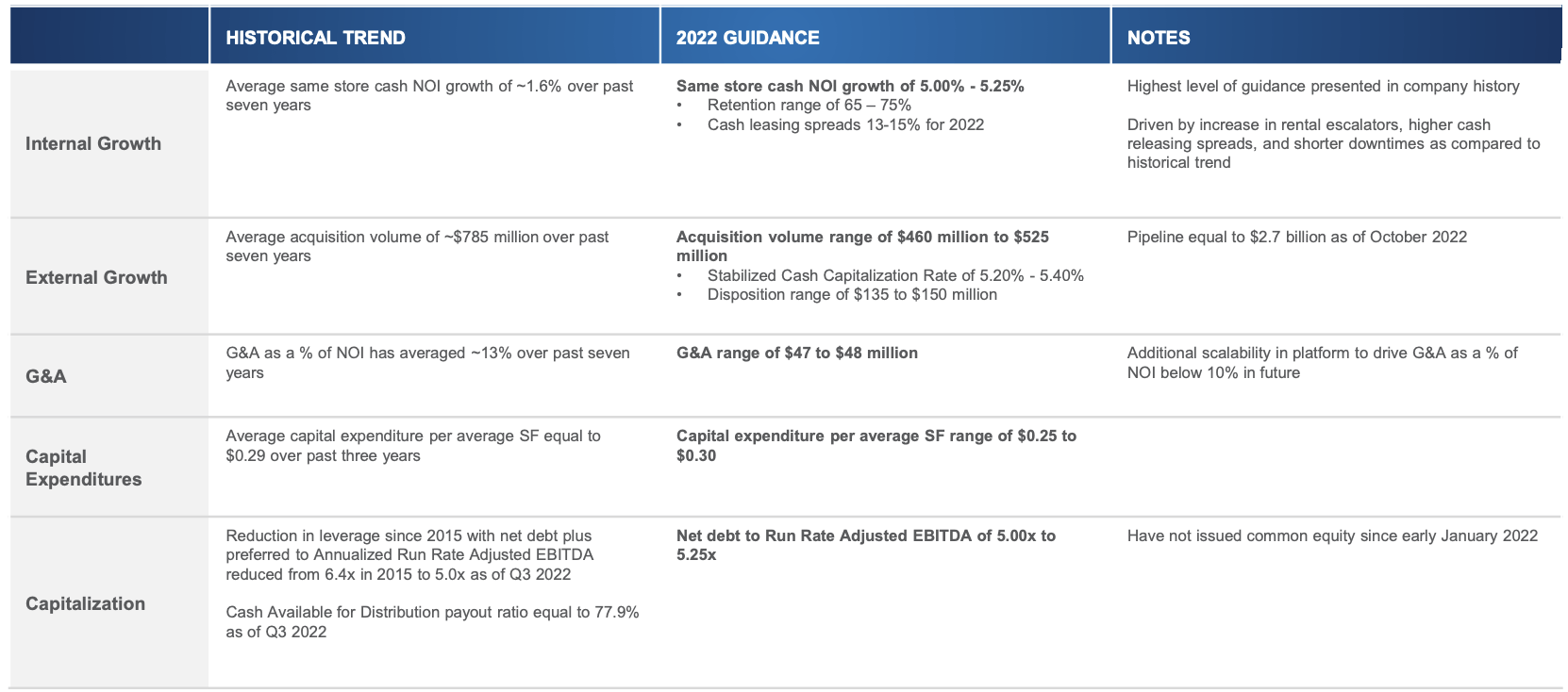

STAG is in a much better spot than at any point since its 2011 IPO thanks to strong industrial trends. The company witnesses accelerating re-shoring and near-shoring trends, driving domestic warehouse space demand. Moreover, the need for flexible inventory and reverse logistics is driving incremental demand. 40% of STAG’s portfolio handles e-commerce, which is a major beneficiary of these trends. This year, STAG is expecting between 5.00% and 5.25% in same-store cash net operating income growth, with a retention rate exceeding 65%.

59% of its tenants have revenue of more than $1 billion. 83% generate more than $100 million in annual sales. 53% of tenants are publicly traded. No tenant accounts for more than 3% of total sales. In the case of STAG, Amazon (AMZN) accounts for 3.0% of total exposure.

STAG Industrial

The good news is that despite the new supply, experts expect that demand growth will remain strong. The reason is re-shoring.

According to Yardi Matrix (which highlighted semiconductor re-shoring):

We expect that demand for industrial space will remain strong in coming years, although it is unlikely that the torrid pace at which the sector grew during the pandemic will be seen again. While the rapid growth of e-commerce and logistics may taper off, the slack could be picked up by re-shored manufacturing. Numerous semiconductor plants were underway when 2022 began, and the passage of the CHIPS and Science Act, which includes billions in incentives for chip manufacturing, will stimulate further investment in semiconductors.

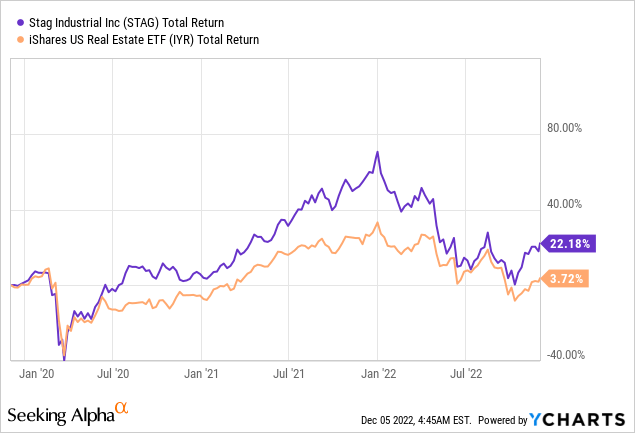

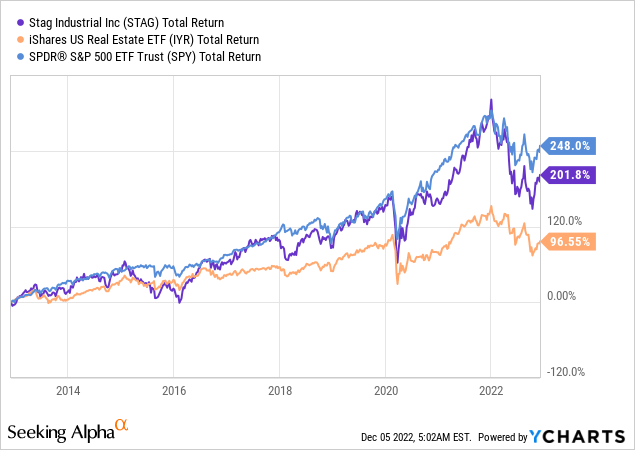

Year-to-date, STAG shares are down roughly 31%, which is 7 points worse than the iShares US Real Estate ETF (IYR). This underperformance is likely caused by its phenomenal performance during the past three years. Including dividends, STAG shares are up 22% compared to pre-pandemic levels. This beats the REIT average by a wide margin.

Moreover, like (almost) all REITs, STAG’s share price is suffering a bit from high rates. Investors have ignored REITs, buying stocks that do well in a high-inflationary environment.

However, it needs to be said that STAG has a stellar balance sheet.

The company has a net leverage ratio of just 5.0x. That’s unchanged since 2021, despite a high acquisition volume. The fixed charge coverage ratio is 5.9x. Moreover, 94.5% of total debt is fixed-rate debt with no major maturities prior to 2025. This buys the company a lot of time while it benefits from a weighted average interest rate below 3.5%.

Moreover, despite operating in a high-growth environment, the company is trading at 14.4x FFO (funds from operations). the peer average is 24.0x, according to the company.

That is a fair valuation in my view.

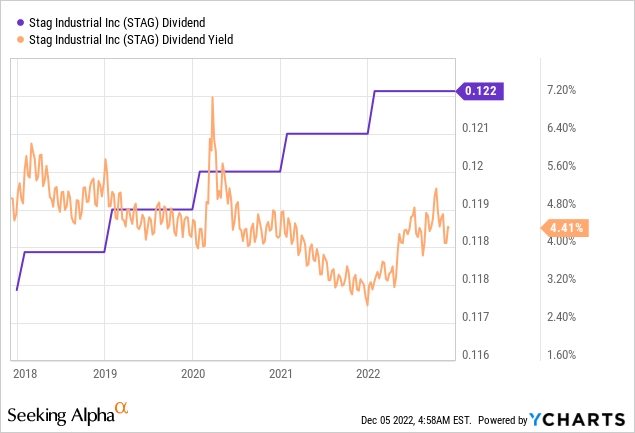

With regard to the dividend, the stock has a very decent yield. The monthly dividend is $0.1217 per share. That’s $1.4604 per share per year. This implies a 4.4% dividend yield. This yield is roughly equal to the longer-term median.

The bad news is that STAG’s dividend is not fast-growing. STAG is mainly focused on growing its business, not necessarily its dividend.

Over the past 10 years, the average annual dividend growth rate was 3.3%. That beats the Fed’s inflation target, but it’s not something to get overly excited about.

The most recent hike was announced on January 10, when management hiked the dividend by 0.7%.

Yet, that’s the only problem. The decent yield and stellar business have caused STAG to consistently outperform the REIT industry. The stock also used to outperform the S&P 500 until higher rates made that arguably impossible this year.

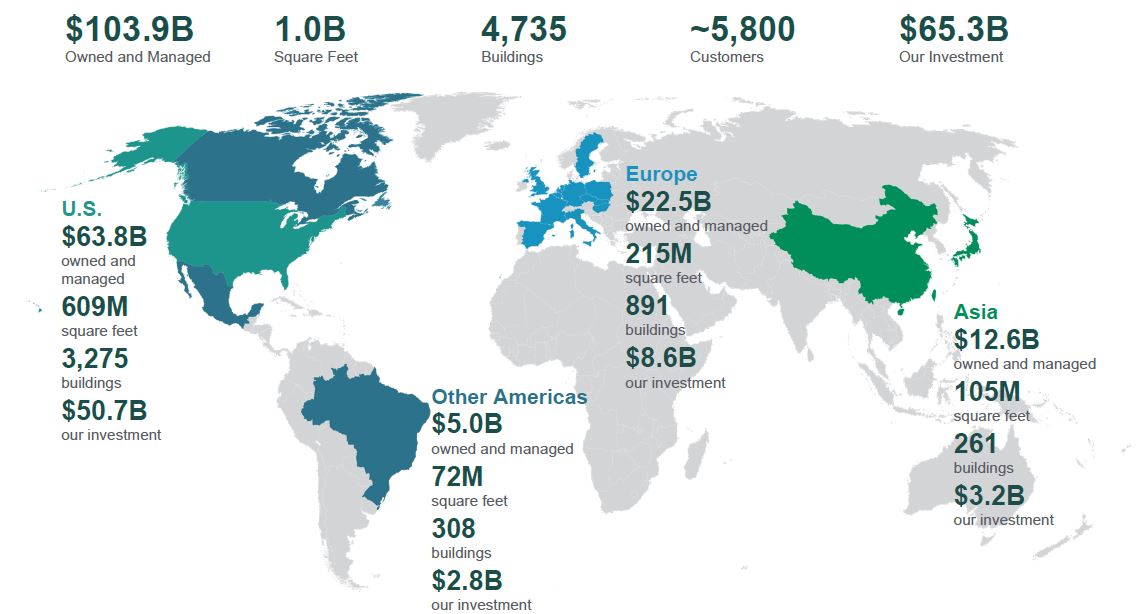

We are the global leader in logistics real estate with a focus on high-barrier, high growth markets. We own, manage and develop well-located, high-quality logistics facilities in 19 countries across four continents. Our portfolio focuses on the world’s most vibrant centers of commerce and our scale across these locations allows us to respond to our customers’ diverse logistics requirements. Our teams actively manage our portfolio to provide comprehensive real estate services, including leasing, property management, development, acquisitions and dispositions.

Prologis

With a market cap of $108 billion, PLD is by far the largest player in this area, owning global assets with a focus on the United States and Europe.

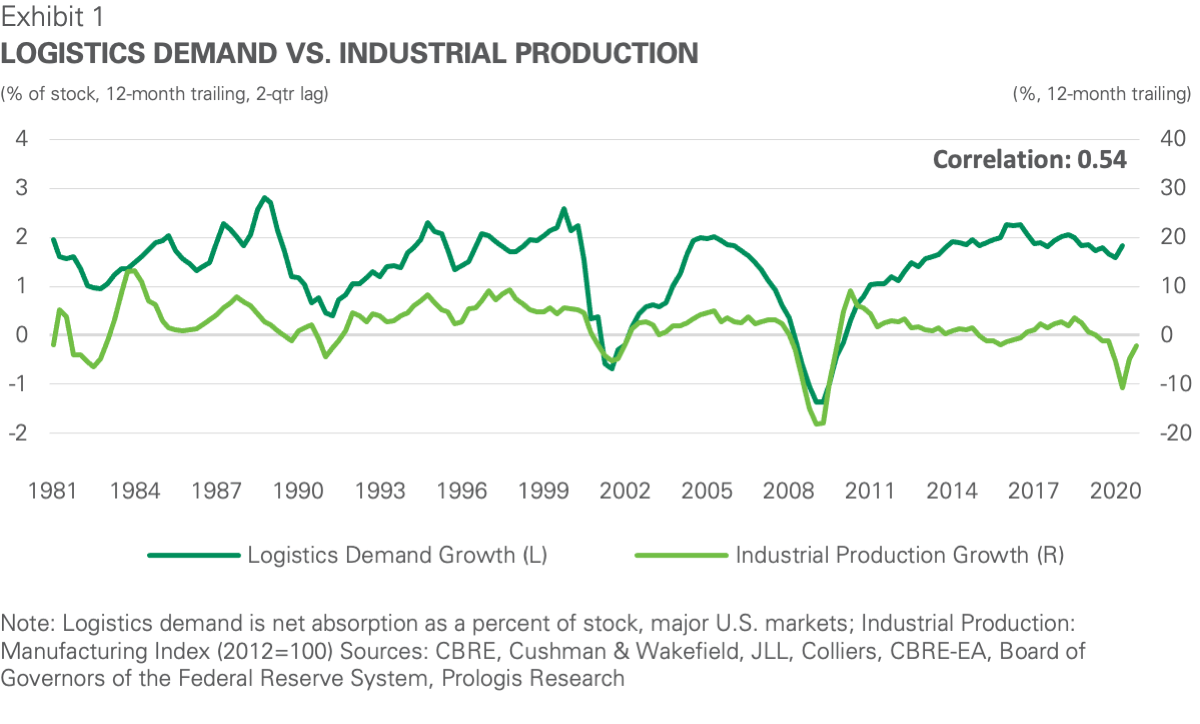

The focus on logistics is based on a few reasons, one of them is the fact that logistics are playing an increasingly important part in the industrial process. This is due to consumption being a bigger driver of industrial production, increasing the need for logistics.

The chart below shows that this spread has widened in the past 10 years.

Prologis

By offering smart logistics (Prologis goes well beyond just offering empty buildings), it plays a major role in making re-shoring (or near-shoring) possible.

The emphasis on domestic manufacturing and the rapid pace of technological advances offers the opportunity for domestic manufacturers to invest in PPE that not only increases productivity but does so at lower costs — thereby increasing the value proposition of reshoring in some industries.

Prologis

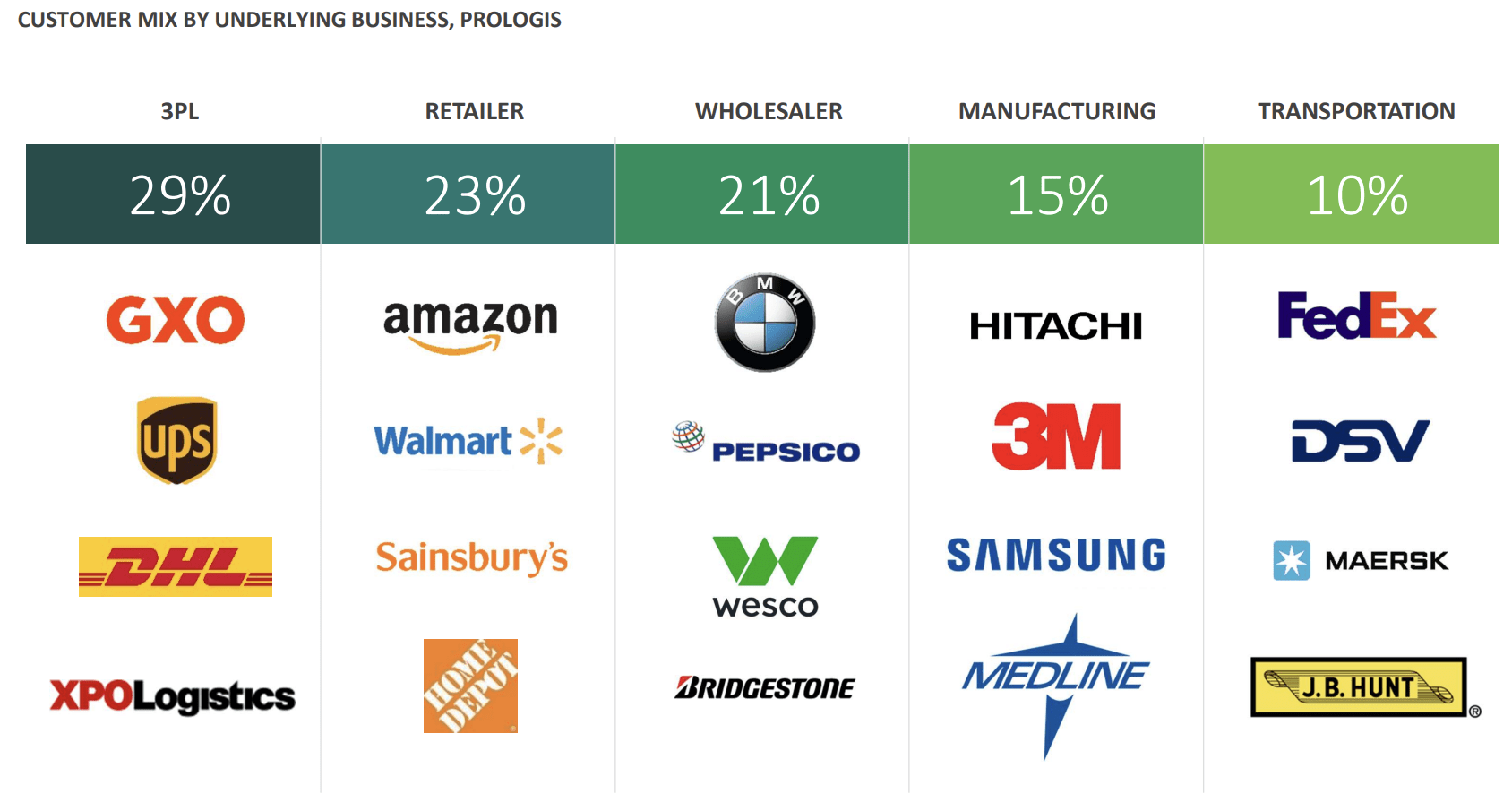

The company’s customer mix shows a focus on advanced logistics, advanced retailers, and well-known brands delivering stability to its income.

Prologis

Roughly 28% of total demand is driven by secular demand trends like e-commerce, general retailing, transportation, and health care. 37% of total demand is basic daily needs, like fast-moving consumer goods, food, and apparel. 29% is cyclical spending.

The company’s average occupancy is 97.7%. This number bottomed in 3Q20 (pandemic) at 95.3%.

The company’s balance sheet is healthy. The net debt ratio is just 3.7x. The fixed charge coverage ratio is 13.9x. It has more than $5 billion in liquidity and an investment capacity of $12.7 billion. Its balance sheet is A3/A-rated with less than 15% of total debt being exposed to a floating rate. The weighted average interest rate is just 1.9%!

I believe this is the healthiest REIT balance sheet I’ve seen all year.

The dividend yield is somewhere between CP and STAG. Based on a $0.79 quarterly dividend, investors are currently receiving a 2.7% yield.

The dividend yield is the biggest issue. Other than that, the company scores high on safety, growth, and consistency.

Seeking Alpha

The average annual dividend growth rate is 10.4%. That really adds up, especially because a 2.7% yield isn’t low. *If* the company were to maintain this dividend growth, a 2.7% yield would turn into a 7.0% yield on cost in ten years.

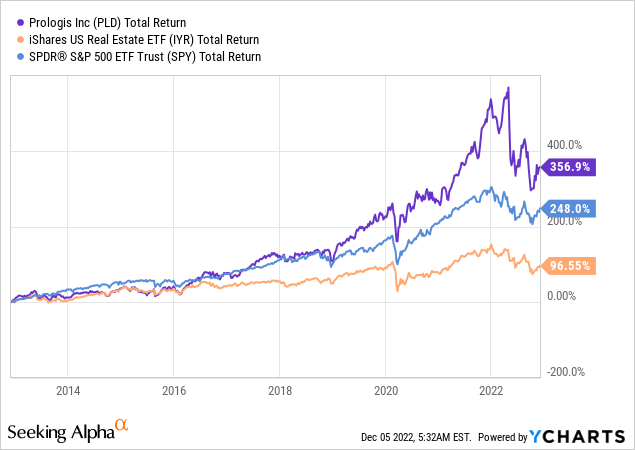

Moreover, PLD is an even stronger outperformer than STAG, beating the IYR ETF by roughly 260 points over the past 10 years. This REIT also beat the S&P 500.

In this article, we discussed one of the most important long-term business trends. Re-shoring started to accelerate after the pandemic as companies wanted to de-risk their supply chains. Add trade wars to this and challenging headwinds in Europe, and we get a great scenario of higher manufacturing production in North America. This excludes government initiatives like the Inflation Reduction Act, which accelerates these trends.

In this article, I presented three dividend stocks that I believe offer tremendous value on a long-term basis. CP has a very low yield, yet it has the power to outperform the transportation industry due to the pending KSU merger and its dominant position in rail transportation connecting all major commodity groups.

STAG and PLD are both industrial REITs. Both are US-focused. Yet, PLD has international exposure. STAG offers a high yield and slower dividend growth. PLD has a lower yield but high dividend growth and a bigger focus on technologies that support supply chain re-shoring.

I believe that all stocks in this article will outperform the S&P 500 on a long-term basis. All stocks have healthy balance sheets, and all stocks will continue to benefit from secular re-shoring tailwinds.

I own CP, and I will add either STAG or PLD in 2023.

With regard to the timing, I like all stocks, yet it is hard to make the case for a stock market bottom – in light of ongoing macroeconomic challenges. So, please do your own due diligence and see what works for your portfolio.

Also, we’ll discuss re-shoring a lot more in the future.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment