MAXSHOT

Sunrun (NASDAQ:RUN) is a company operating in the US with designing, selling and maintaining solar modules. But with a large amount of debt on the balance sheet and high risk for share dilution, any investment right now would be at risk. This is why I have a sell recommendation until I see a turnaround happening.

The Company Outlook

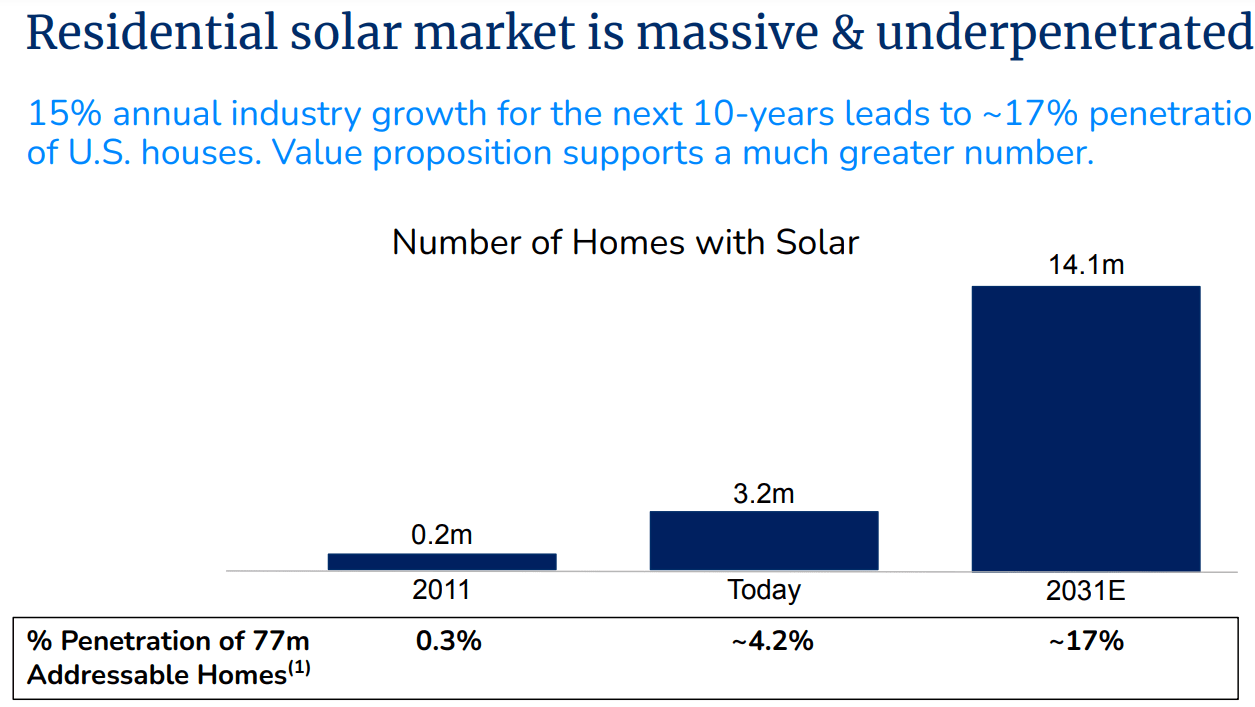

Before diving in and looking at the last earnings report the company provided I want to take a moment and see what Sunrun themselves think about their future. One of the most promising claims Sunrun has in their investor presentation is that the residential solar market is incredibly underpenetrated.

Sunrun Potential Market (Sunrun Investors Presentation)

Even if the market for it would grow around 15% CAGR for the next 10 years, that would still just serve around 17% of the total possible market. Leaving companies like Sunrun or other residentially focused solar companies having an easier time getting their products sold.

The company also holds around 18% of the total market share for residential solar panels right now. I think that they have almost plateaued and it will be difficult getting more market share from the other players in the space. It’s still a new sector with a lot of local companies. That makes it incredibly difficult for larger companies getting a foothold in new markets. It’s not a product that gets changed year after year. Solar panels are things you buy for the long-term.

The way that Sunrun believes they could still capitalize is becoming more of a network and providing neighborhoods with solar panels. Larger contracts that could potentially drive down the operating expenses as they can streamline their installations more and more then.

The future is bright for the solar sector, with plenty of tailwinds for all the companies competing for their own market share in this exciting green energy wave.

Q3 Earnings Report

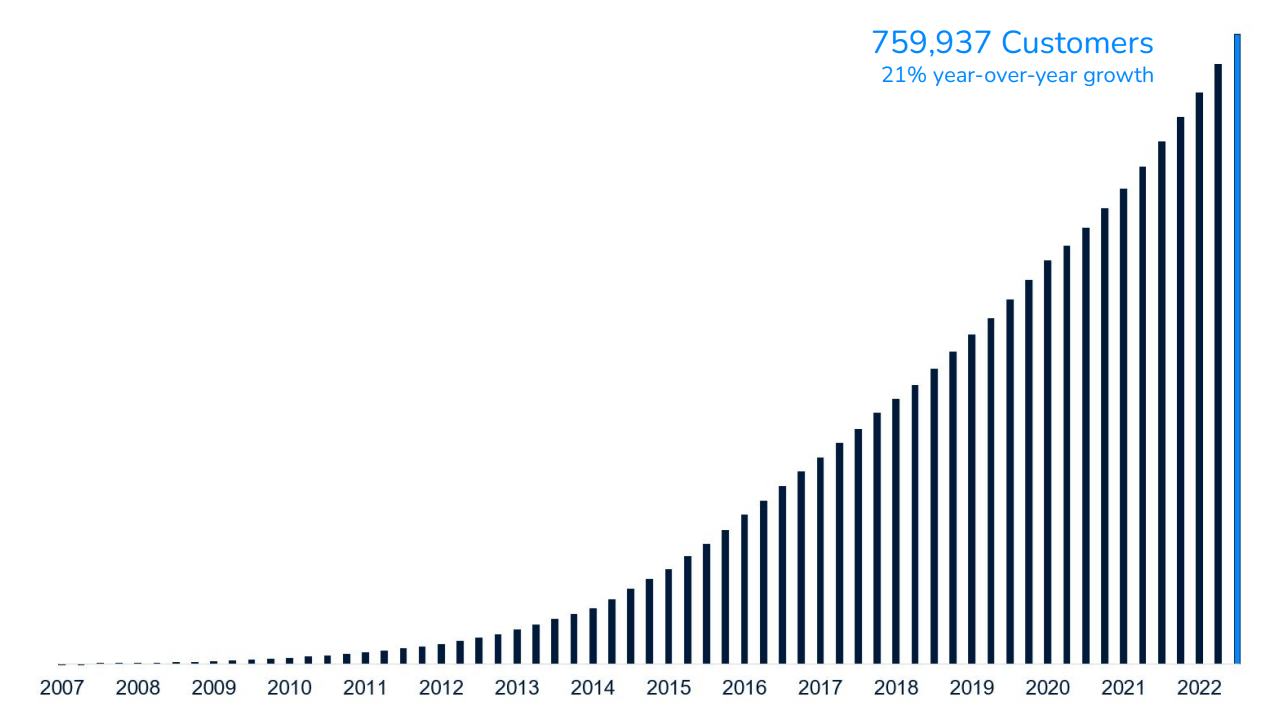

On November 2. 2022 Sunrun provided investors with their Q3 earnings report. For me one of the biggest highlights was the increased margins and in turn the bottom line making a big jump up from last year’s performance.

The company noted that they have a 21% YoY increase in new customers. With the outlook the company provides of a residential solar market still underpenetrated the management seems confident they will be able to continue having high growth such as this. I believe it’s not out of the picture that they can continue like that, but I also think the next few years will be more capital intensive, so I expect the bottom line might start taking some hits again.

The Customer Growth Of Sunrun (Sunrun Investors Presentation)

With this earnings report the company also expects to be able to increase sales by around 25% for the full year. But with higher interest rates and in turn a more challenging economic environment to maneuver in, Sunrun mentioned a few things on that. They have managed to increase the price of their product without a large drop in new customers or canceled projects/orders. This gives some comfort to investors as it seems the demand is still there for the products.

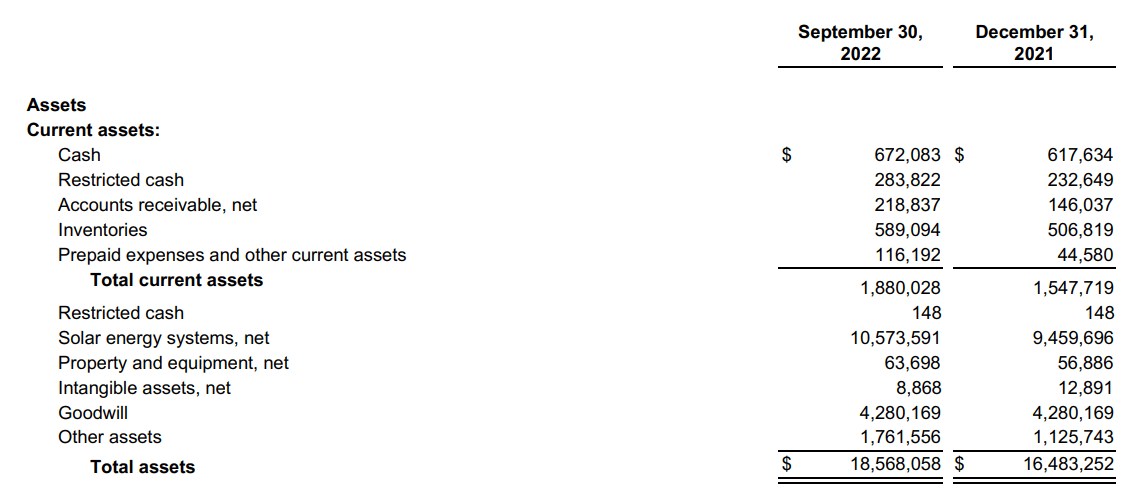

Sunrun’s Balance Sheet

For me, knowing how a company is doing currently financially is incredibly important to properly value a company and spot any possible red flags. In the case of Sunrun I have some pretty serious concerns.

Sunrun Balance Sheet (Sunrun Q3 Earnings Report)

The first would be the amount of cash that they hold in relation to the amount of debt they have on their books. With just under $700 million in cash that doesn’t come close to paying off nearly $6 billion in long term debt. In the short term they will have to pay off around $185 million in debt, so any share dilution shouldn’t be necessary for that. Which leads me to my second concern, the outstanding shares. As an investor you don’t want your share of the pie getting diluted year after year as the company is not able to keep up financially with their operations.

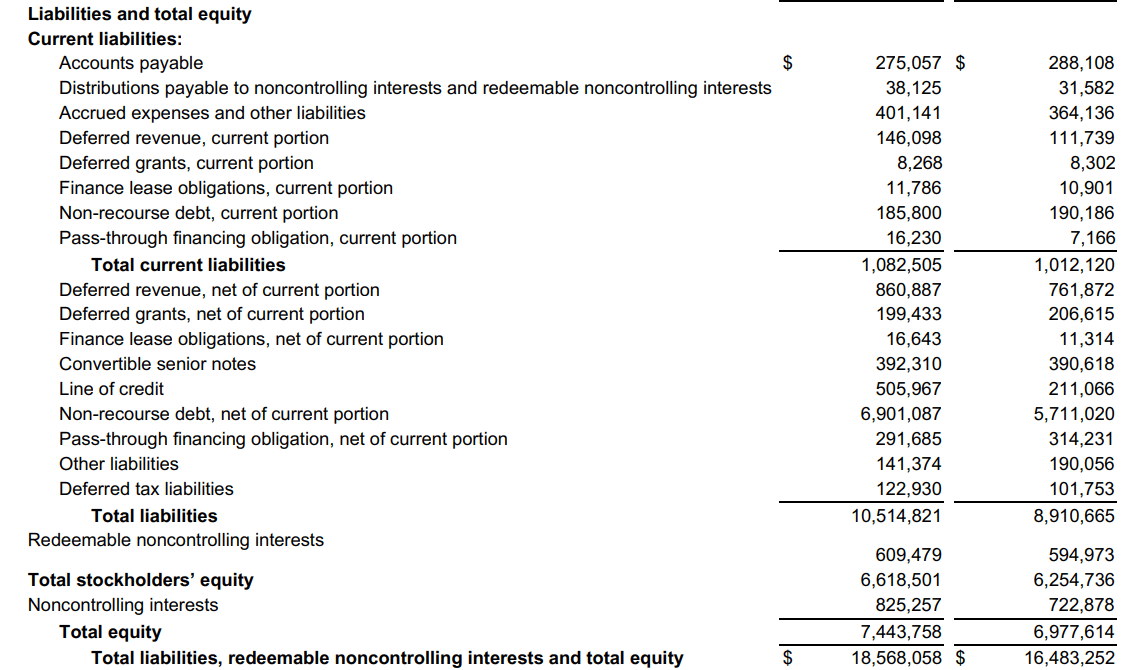

Sunrun Current Liabilities (Sunrun Q3 Earnings Report)

In the case of Sunrun they have nearly doubled the outstanding shares from 5 years ago. Going from 108 million to 215 million outstanding. If I were a long term investor and bought the company back then I would be furious. The company has returned around 300% to shareholders buying back then, but Sunrun is trading at incredibly rich valuations so that number feels inflated and could be brought down.

Outstanding Shares Of Sunrun (SeekingAlpha)

Apart from the concerns I have regarding the debt and shares being diluted, I don’t see the company having made enough efforts to build up their cash position. I have covered solar energy companies previously and a trend I spotted was an increase in cash and less debt taken on. Sunrun has increased their cash by almost 9% compared to last year, but that feels slim compared to some of the other competitors in the sector. Especially when they had such a successful quarter raising the bottom line as much as they did.

Expansion Challenges

Some of the challenges that Sunrun could face comes in penetrating and getting a foothold in new markets. Sunrun is the largest solar panel supplier for residential homes in the US. But I believe that there could be future challenges coming from Sunrun trying to establish themselves in smaller regions.

Here there is often a bigger trend to go with something local. Word spreads quickly and if Sunrun would perhaps stumble a little too much it could isolate them from smaller pieces of the market. In the broader picture however I don’t think Sunrun should face significant headwinds in getting their products sold.

With the inflation reduction act focusing on bringing energy supplies home to the US, Sunrun has their path paved for them to get more and more modules sold and installed.

Valuing The Competitors

I really like reading and learning more about the solar sector. It helps me be a better investor and hopefully make better investment decisions. In the case of the solar sector, it’s very capital intense and will require companies to move quickly and adapt to new challenges all the time.

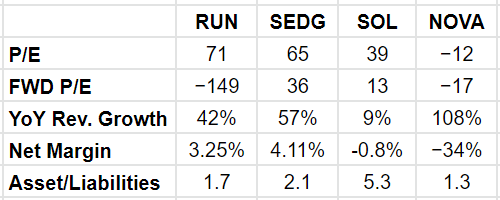

Valuation Of Competitors (Author´s Own Calculations)

Some things that are important to look at are the amount of cash companies keep in relation to the amount of debt they have. It’s a good indication for knowing whether they will bust or not eventually. The valuation of the company is also a good indication about what investors think about the future and outlook.

In the chart I have made, I have chosen some of the companies that Sunrun themselves have set out as competitors, SolarEdge Technologies (SEDG), ReneSola Ltd (SOL) and Sunnova Energy International (NOVA). In all honesty I think SolarEdge Technologies seems like the best choice out of these with large increase in revenues and a good net margin too.

I can see a red line among a lot of solar companies in that they like to hold a lot of assets in comparison with the amount of liabilities they have. It usually comes down to the companies owning large factories or other properties that props up the value of the assets. Large revenue growths are also a common trend as the sector is new and there is a lot of money flowing into it. But I also think that the recent higher pressure coming from the public to find greener energy sources helps these companies find more potential customers.

Valuing Sunrun

Sunrun is the largest company in its specific sector that it operates in. Holding almost 18% of the market share and in my opinion a product where they can pass on expenses to their costumes quite efficiently too.

But having a realistic valuation of the company gives me more relief in putting money into it. Because of their surprise to the upside that is just a bonus for me as an investor. But I also tend to mitigate risks by having conservative price targets and assumptions about the future of the company.

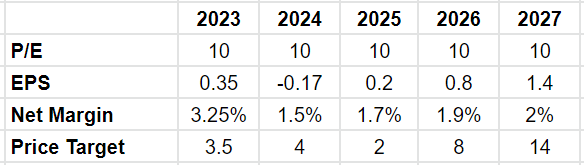

Future Potential Valuation Of Sunrun (Author´s Own Calculations)

I would argue that a conservative terminal p/e of 10 is right as the company has some red flags like high debt and inconsistent bottom line growth. I think that in the coming years, the operating expenses will increase as the company tries to cope with expanding, this gives a negative EPS for 2024. Share dilution will also bring the EPS down. But I think net income growth will catch up and outpace the share dilution until 2027.

With Sunrun having a negative return on capital in the last 12 months, I see that as a reason for the share price being supressed and having a low p/e. Once the company starts to focus on increasing net margins and having positive cash flows, that could be catalysts for a higher p/e and in turn share price. But until I see that change I think the estimates will stay this conservative.

I don’t think buying Sunrun right now is a very good idea. I will not put money anywhere close to them anytime soon. I believe they will have some incredible challenges in the next few years trying to cope with the large amount of debt that they hold. This will force them to dilute more and more shares, which they have proven they have no problem doing. With shares almost doubling in the last 5 years, this is a big red flag to me.

If Sunrun can manage to maneuver efficiently and land more and more projects and contracts then I could see them staying relevant in the solar sector. But with almost 10x more debt than cash I wouldn’t be able to sleep at night having money invested here. That comes also with Sunrun having negative cash flow of $2 billion.

Sunrun has an incredibly rich valuation, which unfortunately seems to be a trend with a lot of solar companies right now. It will take many years of growth until these current prices could ever be justified.

Conclusion

Sunrun has a bright future ahead of them if you ignore the financial issues with small amounts of cash and large company debts. They have managed to steadily increase their customer base by 21% CAGR since their inception.

Looking at the balance sheet Sunrun has issues they need to deal with. For investors they need to address the share dilution they need to do in order to raise capital and pay down their debt. But getting some comments on the negative cash flow would also be appreciated.

In the last earnings report however, Sunrun continued to perform and increase revenues at a good pace and also managed to raise their bottom line by an impressive amount.

But with valuations being important, I can’t see Sunrun being a buy anytime soon. I would recommend investors to look at other companies in the sector if they want exposure to the green energy wave. Right now investors would be better off selling any position in the company, as the downside risks start to amount.

Be the first to comment