AsiaVision

Thesis

Investors who are looking for exposure to emerging markets and emerging business models (entrepreneurship) might like StoneCo (NASDAQ:STNE). The company is a leading payment technology company in Brazil and out of the approximately 30 million entrepreneurial firms in Brazil, StoneCo has captured 2 million so far. Arguably, StoneCo is also trading relatively cheap, with one-year forward P/B at x1.4 and P/S at about x2.

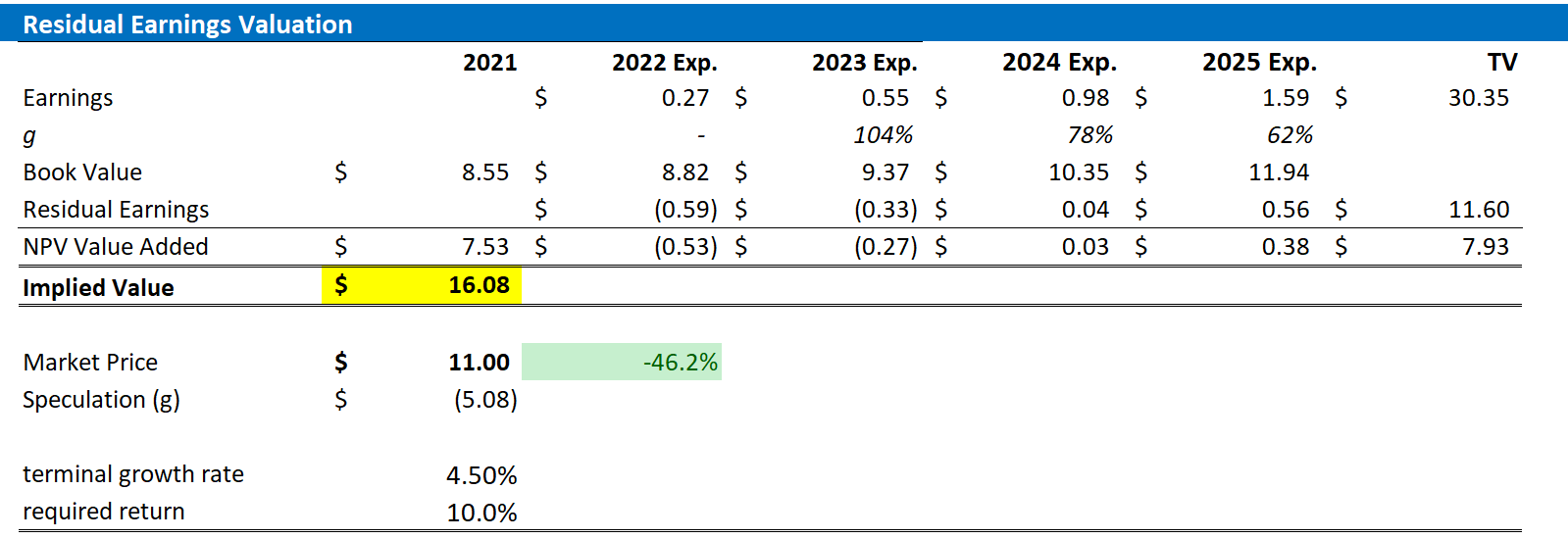

I value STNE based on a residual earnings framework and analyst consensus EPS and calculate material upside of about 46%. My target price is $16.08/share.

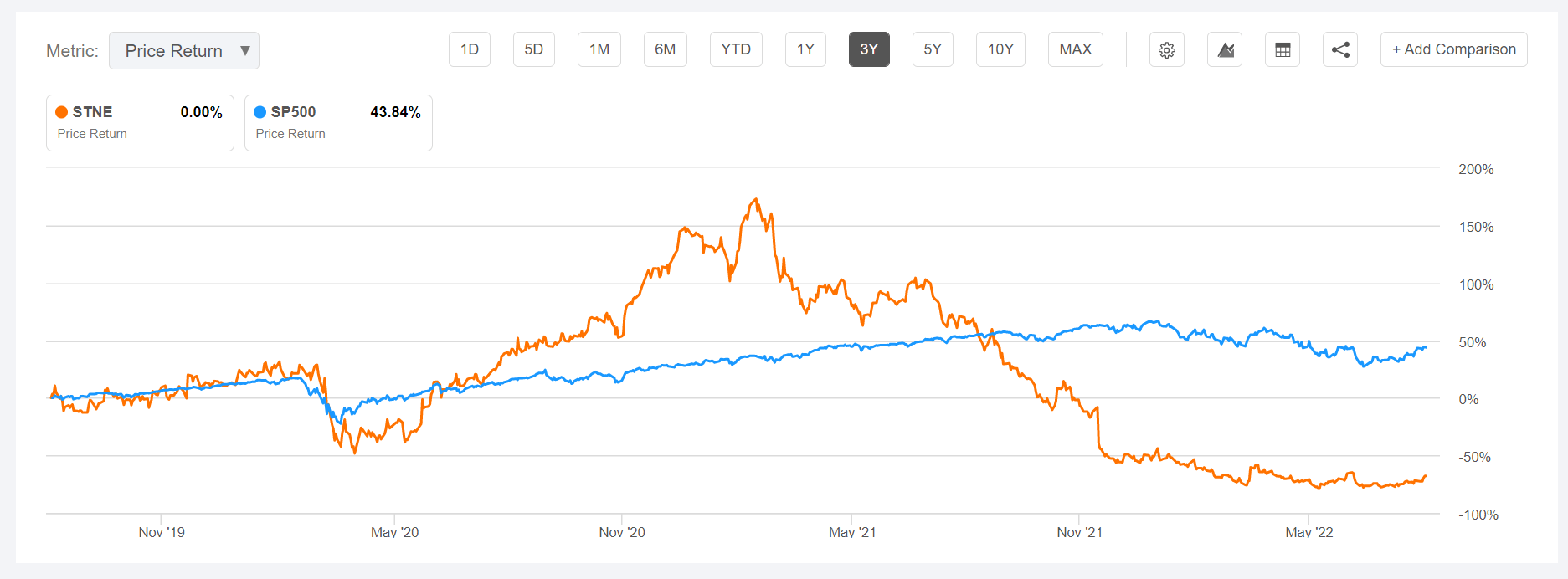

StoneCo is down about 35% YTD, versus a loss of nearly 15% for the S&P 500. Moreover, although StoneCo stock has rebounded by more than 50% since May, the stock is still 85% down from all-time-highs.

Seeking Alpha

About StoneCo

StoneCo is a fintech company based in Brazil. Founded in 2012, the company has grown to become a leading provider of financial technology solutions, which enable the BTC electronic payment infrastructure in-store, online, and mobile channels. As of June 2022, the company serves about 1.9 million active customers, of which most of them are entrepreneurial small-/mid-cap firms.

According to the company, the official mission reads as follows:

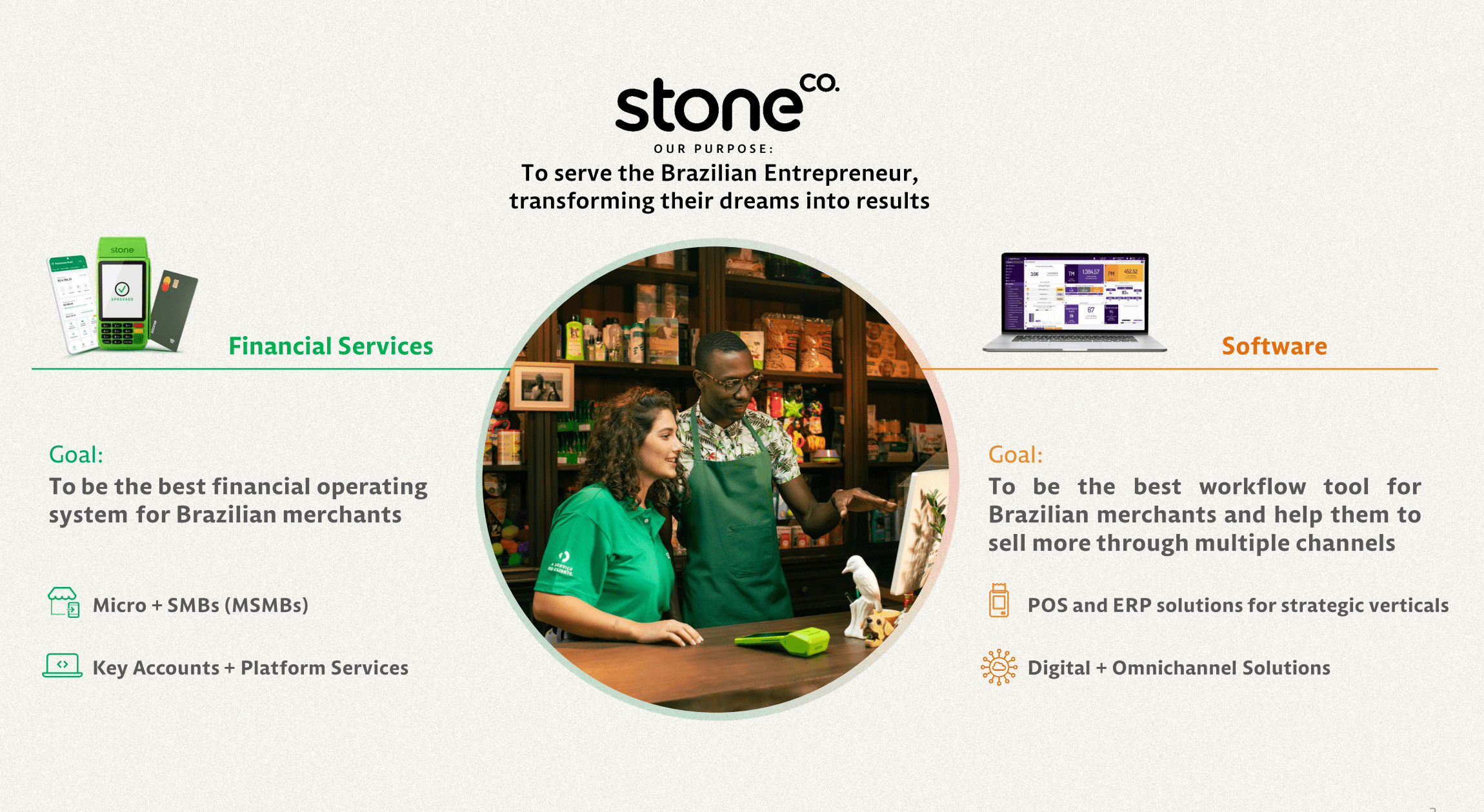

Our primary mission is to remain focused on empowering our clients to grow their businesses and help them conduct commerce and run their operations more effectively.

StoneCo Investor Presentation

StoneCo operates two core segments: Financial Services and Software. Financial Services include payment solutions, credit and digital banking and accounts for about 85% of total revenues. Software encapsulates ERP, POS and Digital Solutions that help clients capture and monitor the payment ecosystem.

Financials

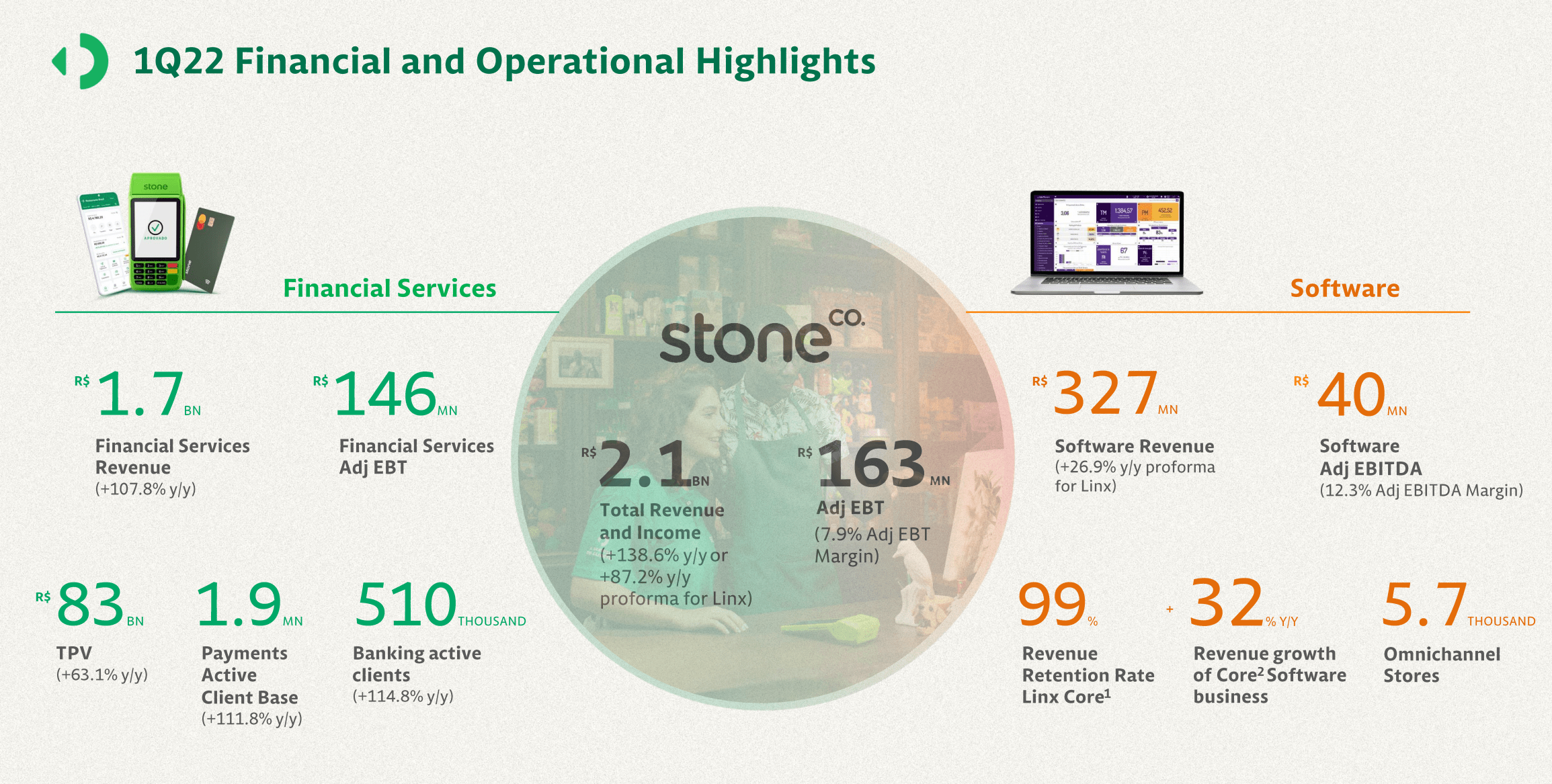

StoneCo is truly a high-growth firm. From 2016 to 2021, the firm’s revenues surged at a 5-year CAGR of 50.3%, jumping from $130 million to $1,005 million. Respectively, operating income jumped from $24.7 million in 2016 to $200 million in 2021.

As of June 2022, StoneCo has about 1.93 billion of cash and short-term investments against total debt of $1.5, making the company a net creditor of about 430 million.

StoneCo Investor Presentation Q1

Analysts expect that StoneCo could generate about $1.70 billion of revenues in 2022 and $2.02 billion in 2023. If materialized, this would indicate a 2-year of about 41% since 2021 — indicating that StoneCo’s business is still expanding rapidly. EPS for 2022 and 2023 are estimated at $0.27 and $0.55, respectively.

Residual Earnings Valuation

Let us now look at the valuation. What could be a fair per-share value for the company’s stock? To answer the question, I have constructed a Residual Earnings framework and anchor on the following assumptions:

- To forecast EPS, I anchor on consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework.

- To estimate the cost of capital, I use the WACC framework. I model a three-year regression against the S&P 500 to find the stock’s beta. For the risk-free rate, I used the U.S. 10-year treasury yield as of August 2, 2022. My calculation indicates a fair required return of about 10%.

- To derive StoneCo’s tax rate, I extrapolate the 3-year average effective tax-rate from 2019, 2020 and 2021.

- For the terminal growth rate, I apply 4.5% percentage points. This is approximately the global nominal GDP growth plus one percentage point to reflect StoneCo’s strong and above-average growth outlook.

Based on the above assumptions, my calculation returns a base-case target price for STNE of $16.08/share, implying material upside of almost 50%.

Analyst Consensus Estimates; Author’s Calculation

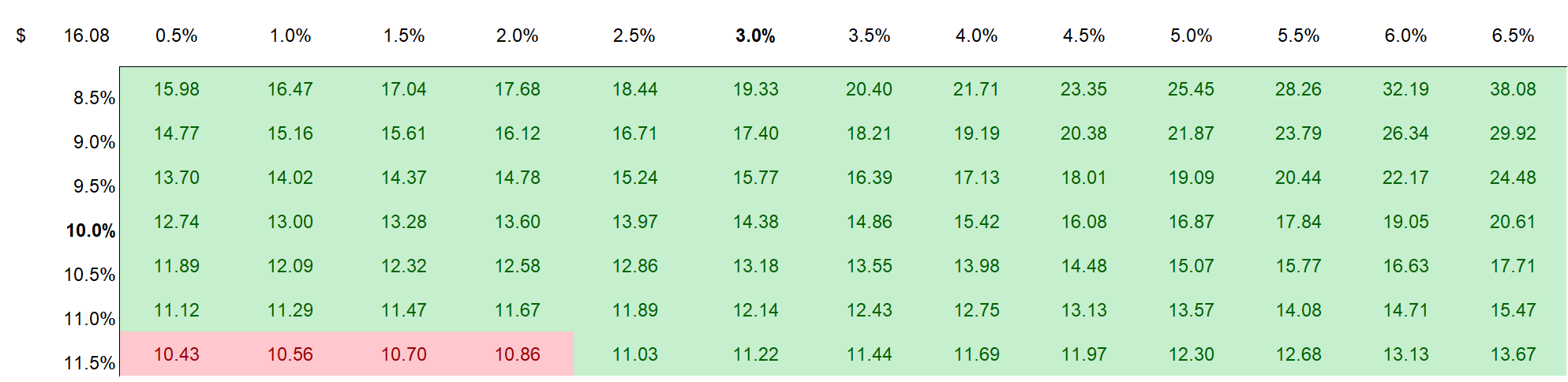

I understand that investors might have different assumptions with regards to STNE’s required return and terminal business growth. Thus, I also enclose a sensitivity table to test varying assumptions. For reference, red-cells imply an overvaluation as compared to the current market price, and green-cells imply an undervaluation.

Analyst Consensus Estimates; Author’s Calculation

Risks

I would like to highlight a few notable risks that could cause STNE stock to materially differ from my target price:

First, arguably most of STNE’s current share price volatility – especially to the downside – is driven by investor sentiment towards risk assets, especially growth companies such as StoneCo. Thus, it’s likely that STNE stock experiences significant volatility even though the company’s business outlook remains unchanged.

Second, all of StoneCo’s sales are generated in Brazil. Investors in the company are thus fully exposed to Brazil’s idiosyncratic risks.

Third, StoneCo’s fundamentals are correlated to the success of small- and mid-cap businesses in Brazil. And given globally slowing consumer confidence, wage and price inflation, rising interest rates and increasing unemployment, StoneCo’s business outlook might be pressured by macro-headwinds.

Conclusion

I like the risk reward set-up for StoneCo: The company is down about 85% from-all-time-highs and trades at a P/B of x1.4 and P/S of about x2. Moreover, StoneCo is growing topline revenues at a >40% CAGR and the company does not appear to have any structural profitability issues — as many other high-growth peers.

I believe investors could enjoy close to 50% upside, as I calculate a $16.08/share target price, based on a residual earnings valuation framework.

Be the first to comment