urbazon/E+ via Getty Images

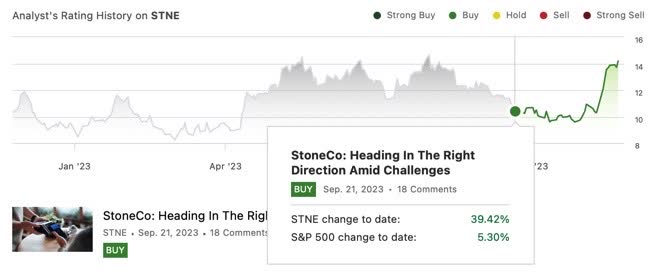

In my previous StoneCo (NASDAQ:STNE) article, I adopted an optimistic stance on the payments company, emphasizing its exceptional position among domestic peers due to rapid expansion and growth.

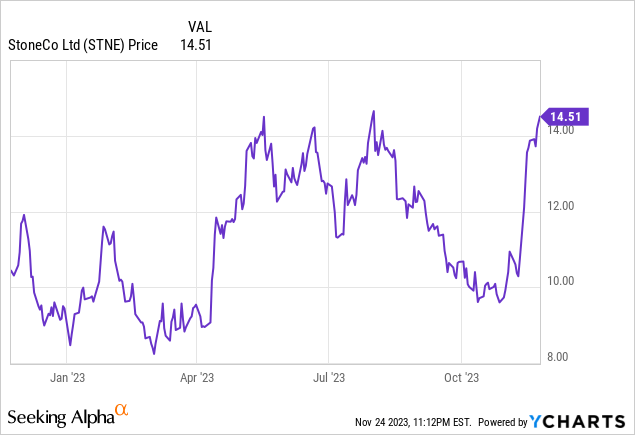

Seeking Alpha

Over the last month, the bullish thesis has proven valid, especially considering that the third-quarter results potentially marked the end of a cautious investor sentiment that had emerged during the second-quarter earnings season of Brazilian banks, driven by concerns about defaults.

Following the company’s guidance for Q3, the projected revenue growth of 22% pointed to challenges linked to a deceleration in Total Payment Volume (TPV) within the sector and the continued expansion of Earnings Before Tax (EBT). Nevertheless, the results exceeded expectations, with revenues increasing by 25% year-over-year, TPV accelerating by 11% year-over-year, and a robust EBT underscoring the company’s cost efficiency.

Furthermore, the market reacted positively to the guidance from 2024 to 2027, leading to a more than 50% rally in Stone’s shares in November alone.

Looking ahead, aiming for a robust expansion in Total Payment Volume (TPV) and a credit portfolio growing at annual double digits for the next four years, while possible, will likely face challenges in execution amid macroeconomic hurdles. This is particularly true in a scenario of ongoing credit recovery and persistently high-interest rates in Brazil despite a downward trend.

Until proven otherwise, I maintain my bullish thesis intact, believing that Stone’s progress toward fulfilling its guidance in the coming years positions it with an attractive valuation.

Stone’s 3Q23 Earnings Results

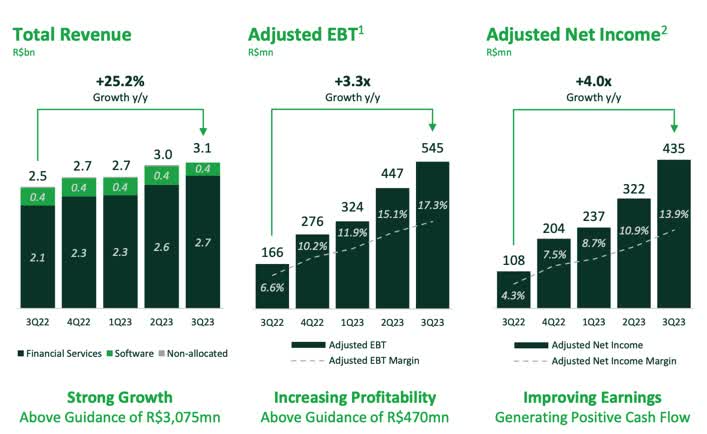

Reported on November 10, Stone concluded the third quarter of this year with an adjusted net profit of R$435 million, signifying a remarkable 302% increase compared to the previous year. Sequentially, there was an impressive increase of 35.1% from the second quarter of this year.

StoneCo’s IR

As reported by the company, the adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) for the period reached R$1.590 billion, showcasing a substantial 43.4% increase compared to the third quarter of 2022. Notably, within a single quarter, this figure rose by 6.1%.

Stone’s net revenue experienced robust year-over-year growth of 25.2%, reaching R$3.1 billion. This performance was primarily driven by the financial services sector, encompassing slot machines and banking services, which recorded net revenue of R$2.7 billion, marking a significant 29% increase in one year.

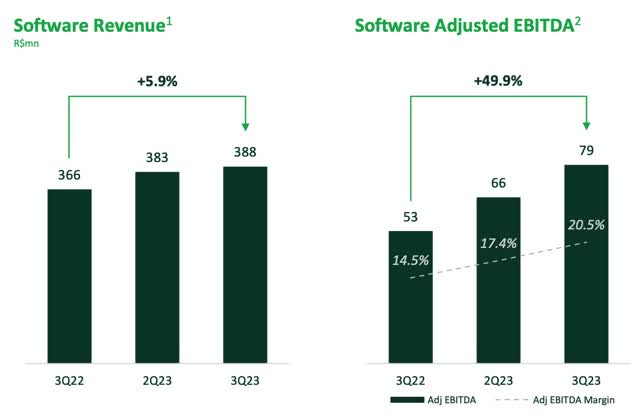

In the software segment, Stone’s net revenue demonstrated a year-on-year growth of 5.9%, reaching R$388 million in the third quarter. The company highlighted a noteworthy 6 p.p increase in the EBITDA margin of this area, totaling 20.5%, attributed to efficiency gains in process integration.

StoneCo’s IR

Regarding the software area, the company emphasized ongoing improvements in the EBITDA margin, driven by efficiency gains in back-office process integration.

The company reported that its banking platform had reached 1.9 million customers, reflecting a remarkable annual increase of 244.2%, and the quarter concluded with R$4.5 billion in deposits, a substantial 51.1% year-on-year growth.

StoneCo’s IR

The third quarter marked the end of the testing phase for the credit operation, with the portfolio standing at R$113 million. The company plans to expand the credit offer while closely and cautiously observing market conditions. The credit offer, which impacted the company’s results and shares in 2021, underwent reformulation last year, with new tests initiated this year.

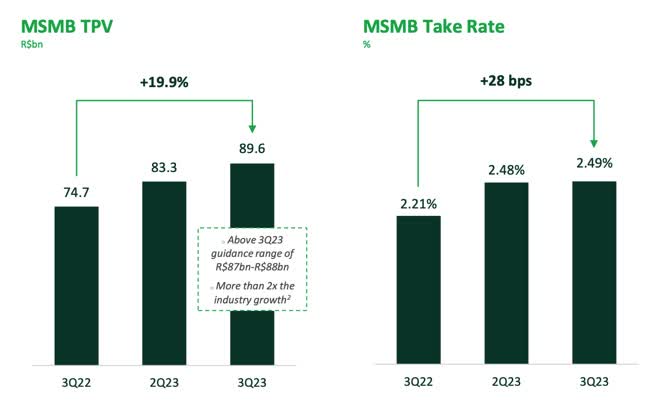

Stone processed R$103.9 billion in transactions through acquiring, indicating an 11.3% growth compared to the third quarter of 2022. In the micro, small, and medium-sized business segment, the largest segment, the volume reached R$89.6 billion, a 20% year-on-year growth. The take rate was 2.49%, up 0.28 points over the same period.

The volume of payments processed (TPV) totaled R$103.9 billion, marking an 11.3% increase over the same period last year. The TPV of micro, small, and medium-sized companies rose by 19.9% to R$89.6 billion, exceeding the company’s projections ranging from R$87 to R$88 billion.

StoneCo’s IR

The weakest aspect was the reduction in the Total Payment Volume (TPV) of critical accounts, experiencing a 22.8% annual decline despite a take rate growth of 18 percentage points over the same period.

Stone had 3.3 million payment customers at the end of September, reflecting an increase of 316,000 in one year. In banking services, the customer base expanded more than threefold, reaching 1.9 million, and the deposit base reached R$4.5 billion, a growth of 51.1%.

As a noteworthy development, Stone’s Board of Directors has approved a new share repurchase program, allowing Stone to repurchase up to R$ 1 billion in outstanding common shares. Previously, the company repurchased approximately R$300 million in outstanding shares, a process completed in November.

A Highly Ambitious Guidance Provided

On November 15, Stone unveiled its highly robust and ambitious guidance for 2024 to 2027.

The company presented a strategy based on three priority pillars: to grow in the Micro, Small, and Medium Entrepreneur (MSMB) market, to increase the engagement of its base by expanding the offer of financial services and integration with software, and to gain increasing operational efficiency to grow with low incremental investment.

The software platform will prioritize four verticals: retail, food, pharmacies, and gas stations. The aim is for Stone to consolidate itself as the “one-stop-shop” for its customers, integrating its solutions to help them sell more, manage better, and turn their businesses around.

Following the arrival of the company’s new CEO, Pedro Zinner, in April of this year, StoneCo announced a restructuring to direct the company in its market strategies by customer segment to accelerate the integration of financial services solutions with software assets.

According to the company’s current management, the time is now to use efficiency to improve Stone’s profitability, considering that it has managed to grow its business very quickly.

In general terms, Stone wants its leading performance indicators to grow at an average annual double-digit rate over the next four years. For example, the total volume of payments processed (TPV) in the micro, small, and medium-sized business (MSMB) segment should rise from R$412 billion next year to more than R$600 billion in 2027. This means an average annual growth (CAGR) of 13% over the period.

And, since part of the company’s revenue is generated by the fee it charges per transaction, there’s nothing better than raising the average take rate from 2.49% to 2.70% in the same time window.

StoneCo’s IR

Increasingly focused on banking operations, the company also plans to increase the total deposits under its responsibility from R$7 billion to R$14 billion over the same period, which implies an average annual increase of 26%.

The credit portfolio has a much more aggressive target of growing 90% per year, from R$800 million in 2024 to R$5.5 billion in 2027.

If all these results are achieved, Stone expects to crown the period with an average annual growth of 31% for adjusted net profit, which would rise from R$1.9 billion to R$4.3 billion.

Valuation

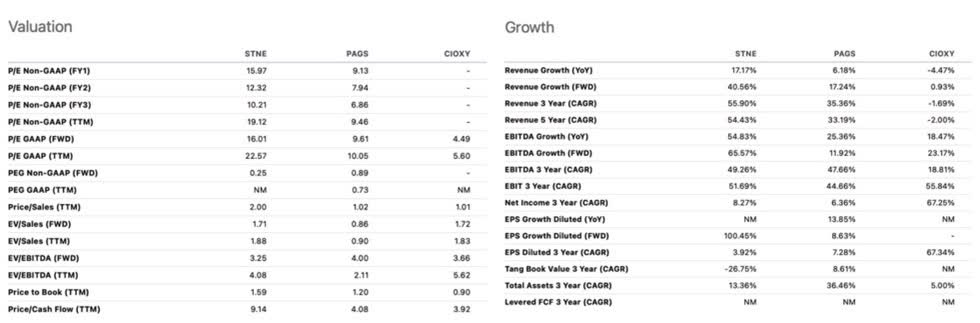

As the company with the highest growth potential among its domestic payment peers, PagSeguro (PAGS) and Cielo (OTCPK:CIOXY), and boasting positive efficiency figures along with robust growth targets over the next few years, Stone continues to trade at a valuation multiple of 71% above the average for the payments sector. However, it remains 70% below its historical average over the last few years. It’s worth noting that Stone is currently 84% below its historical peak at the beginning of 2021.

Seeking Alpha

On the other hand, a significant asymmetry is apparent when examining Stone’s forward PEG Ratio (Price/Earnings to Growth ratio), which considers the company’s earnings growth to the share price (P/E ratio) and the growth rate. Stone is trading at 0.25, compared to a sector average of 1.27.

In essence, by purchasing Stone below $15, investors would pay a quarter of the share price for each unit of expected earnings growth.

Indeed, for this to be a sound strategy, Stone must grow in line with the expectations outlined in its guidance. Achieving this will require the company to operate efficiently in the face of a challenging credit scenario in Brazil. However, with better prospects for the coming years, mainly driven by an estimated interest rate (Selic) of 9.25% at the end of 2024, 8.75% in 2025, and 8.5% in 2026, the trend suggests an improvement in economic activity and, consequently, a more favorable credit scenario from 2024 onwards.

The Bottom Line

StoneCo unveiled its third quarter, surpassing critical metrics outlined in its guidance and reinforcing a robust trajectory toward the ambitious guidance disclosed at its Investor Day following the earnings release.

The focus now shifts to how adeptly Stone can execute its outlined guidance. Within the domestic landscape, Stone has consistently outperformed its peers with solid execution and impressive indicators. The challenge lies in the company’s strategic pivot toward segment growth beyond its traditional offerings, including banking, lending, and software. While this shift makes sense, executing it successfully poses a formidable challenge.

Stone’s execution strategy must navigate through scenarios of uncertainty and potential headwinds linked to the economic conditions in Brazil and the US. This includes a credit environment still in recovery and purchasing power showing signs of strain, especially in a US economy precariously close to a recession.

On the other hand, the scenario of lower interest rates in Brazil for 2024 and beyond reinforces hopes for a more robust economic activity.

As Stone embarks on this next growth phase, its ability to overcome challenges and capitalize on opportunities will be pivotal in determining its success in the evolving landscape.

Given the company’s effective execution of its strategy, my recommendation is to buy until there is evidence suggesting otherwise. In my assessment, the current valuation seems significantly discounted compared to the potential value the company is expected to deliver in the coming years.

Be the first to comment