putilich

In 2011, the famous venture capitalist Marc Andreessen coined the term “software is eating the world”. Since that point, software tools have become embedded into our everyday lives. However, most people don’t think about how software teams and product managers develop products, well this is where Atlassian helps.

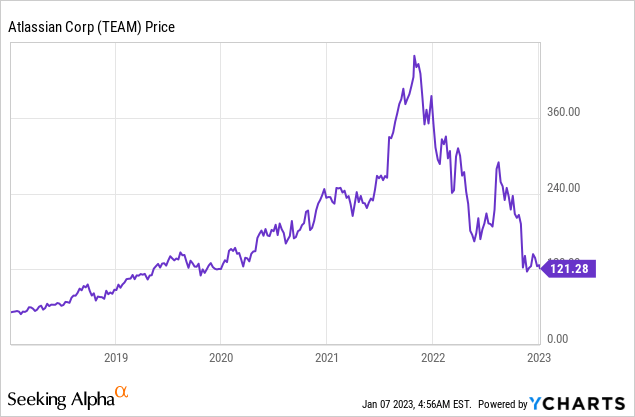

Atlassian (NASDAQ:TEAM) is an Australian-founded software company that is known for helping to enable software development teams across the world. The company is a leader in this category and is poised to benefit from the increasing development of software. The software industry is forecast to grow at a 5.72% compound annual growth rate and be worth ~$813 billion by 2027. Atlassian has produced solid financial results in the past quarter, beating both top and bottom-line growth estimates. Despite this, its stock price has fell off a cliff and is down nearly 75% from its all-time high in November 2021. In this post, I’m going to break down its business model, financials, and valuation, let’s dive in.

SaaS Business Model

Atlassian is a software-as-a-service company that pioneered the enablement of “agile” software development through its iconic “Jira” boards. To level set for everyone, “agile” is basically a modern software development methodology that focuses on “user stories” and uses rapid iteration to produce features. This is faster and more accurate than a traditional product or project development framework, which includes multiple stages in a waterfall-style method. According to a State of Agile Report from 2021, Jira was the number one software development platform recommended by agile teams. On a personal note, I’ve used the platform myself for software development, as I worked as a Product Manager for a SaaS product. According to Gartner reviews, Atlassian’s Jira is 4.4 stars out of 5, which makes it the most popular platform along with Asana. However, I do believe Asana is better suited (and more well-known) for team management personally.

Jira Board shown below (Q1 FY23)

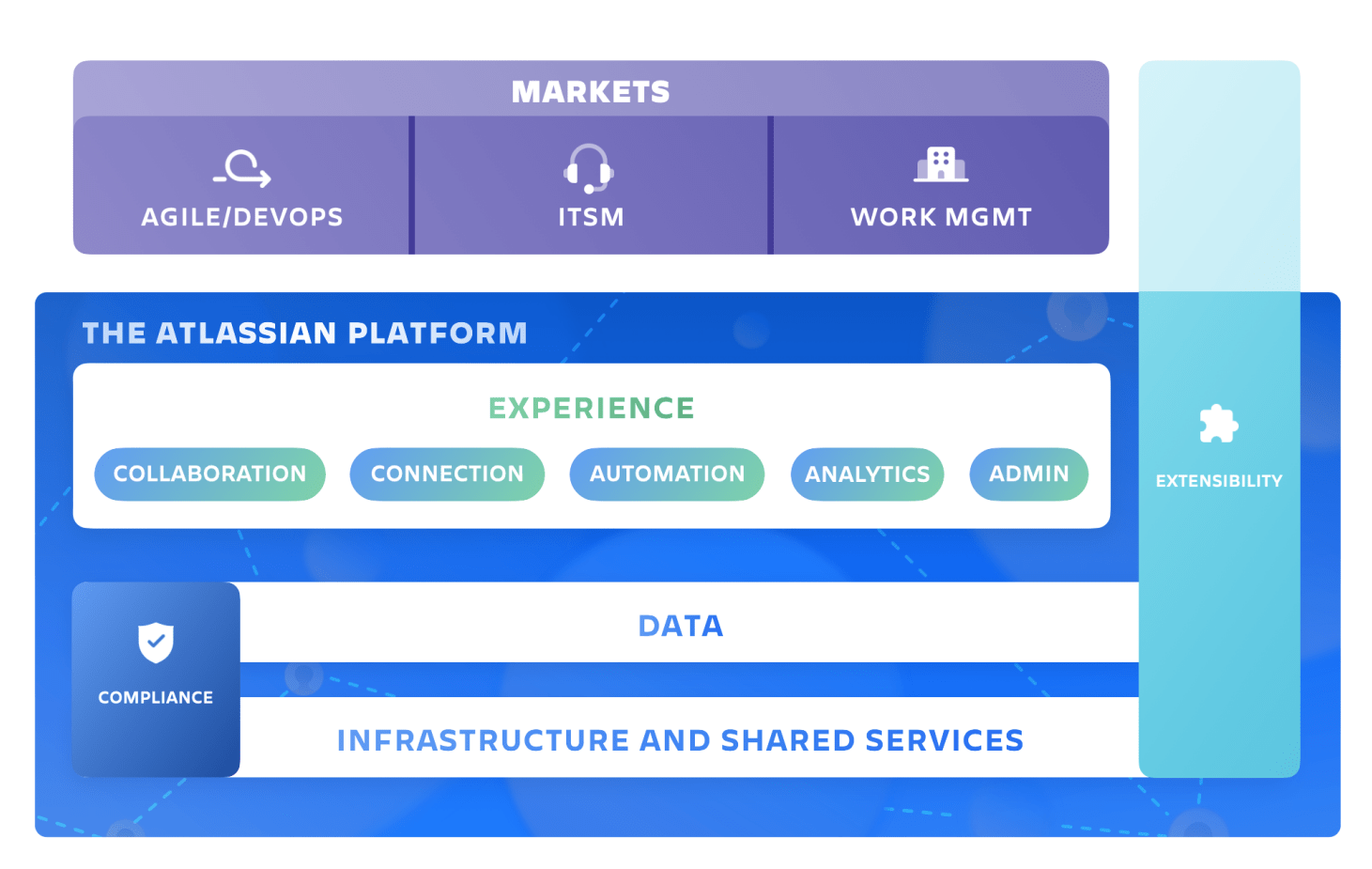

Atlassian has also expanded its platform to include service management tools, content collaboration tools [Confluence], and even Trello for visual project management. Atlassian acquired Trello in 2017, for $425 million, this signaled the company’s move to team management, not just product management. Atlassian is also rolling out an analytics product (which is currently in beta testing with customers). It is aimed to help customers break down data siloes and unlock the power of big data.

Atlassian business model (Q1 ’23)

The company’s go-to-market strategy has focused on a low-friction, “self-service” model. This means Atlassian is free to sign up for up to ten users initially. Therefore this mitigates the need for budget approval, buying committee debates, etc. The platform then scales with its customer, whether that be a startup or an enterprise. For larger organizations, the pricing is marketed in a reasonable manner. For example, its standard package is just $5.75 per month, per employee. This initially looks like a very cheap/low price. However, if a company has 10,000 employees this equates to $57,500 per month or $690,000 per year which is now a nice chunk of “change” for Atlassian.

Atlassian platform (Q1 FY23)

Growing Financials

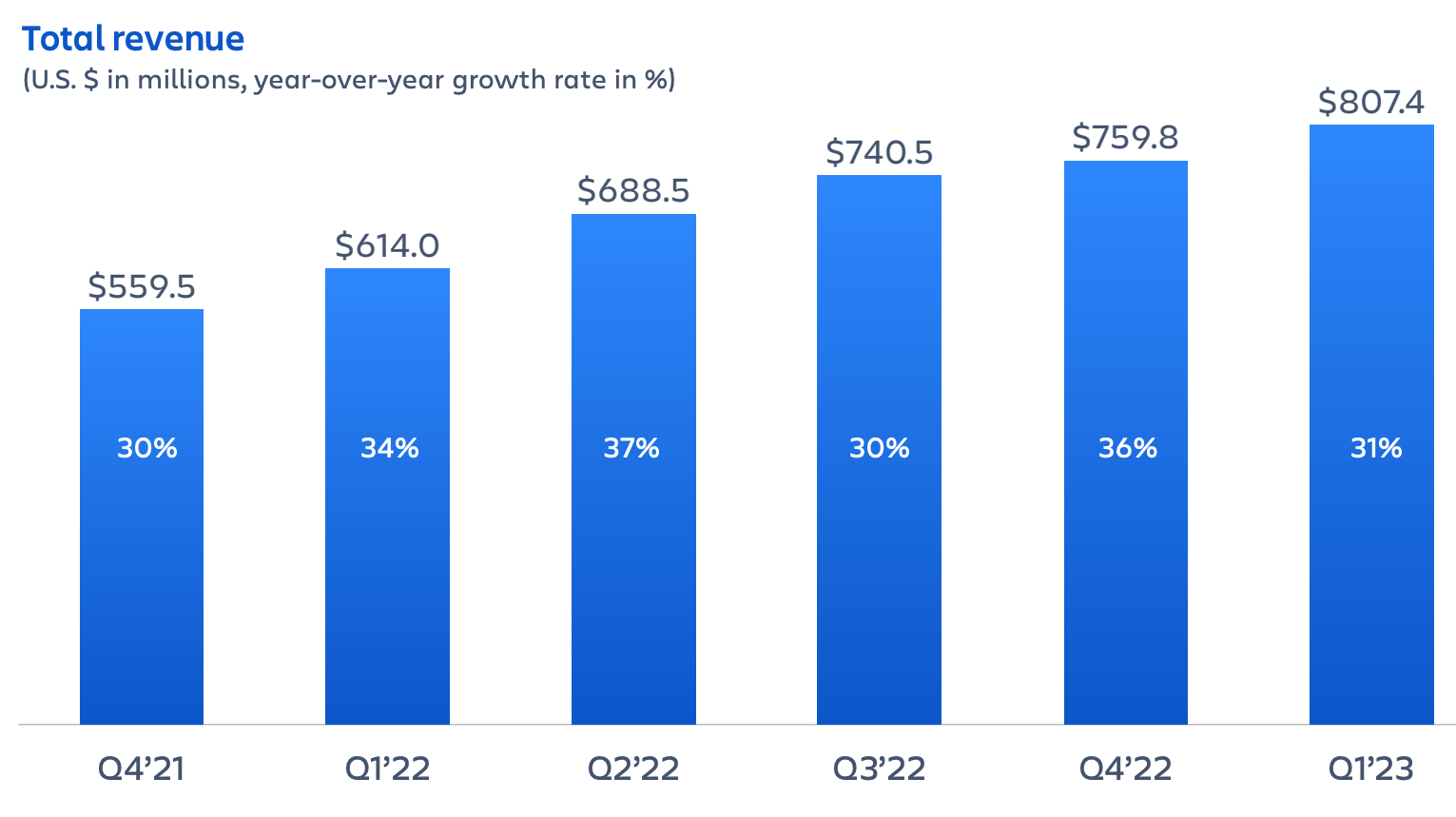

Atlassian reported solid financial results for the first quarter of the fiscal year 2023. Revenue was $807.39 million, which increased by a solid 31.49% and beat analyst estimates by $971,700. This solid top line was despite management noting a decline in the rate of free users converting to paid plans, which was expected due to the macroeconomic environment.

Revenue (Q1 FY23 report)

The top line was driven by strong subscription revenue which increased by 50% year over year to $650.98 million. Subscription revenue makes up 80% of the total revenue, which is a positive sign as subscription businesses tend to offer greater “stickiness” and lower customer acquisition costs than a single transaction-based business model. The beauty of Atlassian’s business model is once teams start uploading all their information and using the platform, inherent “switching costs” are built in.

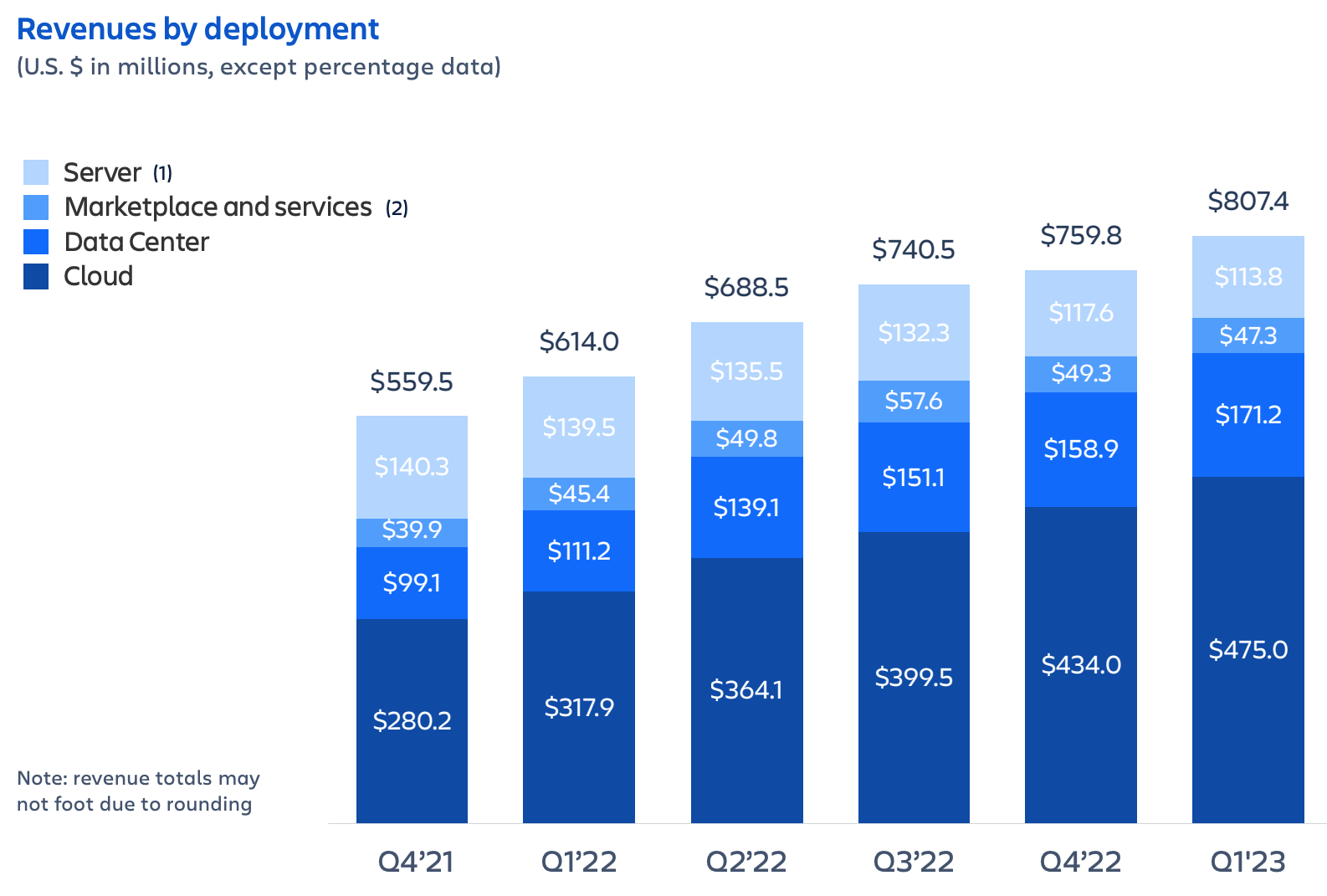

By deployment, Data Center revenue increased by 54% year over year to $171.2 million. Cloud revenue increased by 49% year over year to $475 million. It is great to see full cloud deployments make up the majority, 58.8% of revenue. This means the business can easily scale with its customers. In addition, Atlassian has positioned itself as a solid partner for companies moving software applications to the cloud. In the trailing 12 months the number of Cloud migrations and Cloud enterprise deals increased by over two times. Atlassian has also been investing in talent in this space, to further strengthen its position as effectively a cloud solutions consultant.

Revenue by Deployment (Q1 FY23)

By region, Atlassian makes 51% of its revenue from the Americas, which increased by a solid 33% year over year to $409.9 million. The company’s revenue is well-diversified and growing strongly across all regions. For example, EMEA contributes to 37.7% of total revenue and increased by 29% year over year to $304.3 million. Asia Pacific revenue contributed to 11.5% of the total and increased by 33% year over year to $93.19 million. Given Atlassian was founded in Australia (close to Asia), I believe the company has a huge opportunity to grow in the Asia Pacific market. The platform has slow performance/bugs in China, but this is mainly due to the “great firewall of China”, which effectively bans outside websites. However, I see advanced economies like Japan and South Korea, as key growth markets. But management did not allude to whether this was a focused part of their growth strategy.

Atlassian revenue by region (Q1 FY23 report)

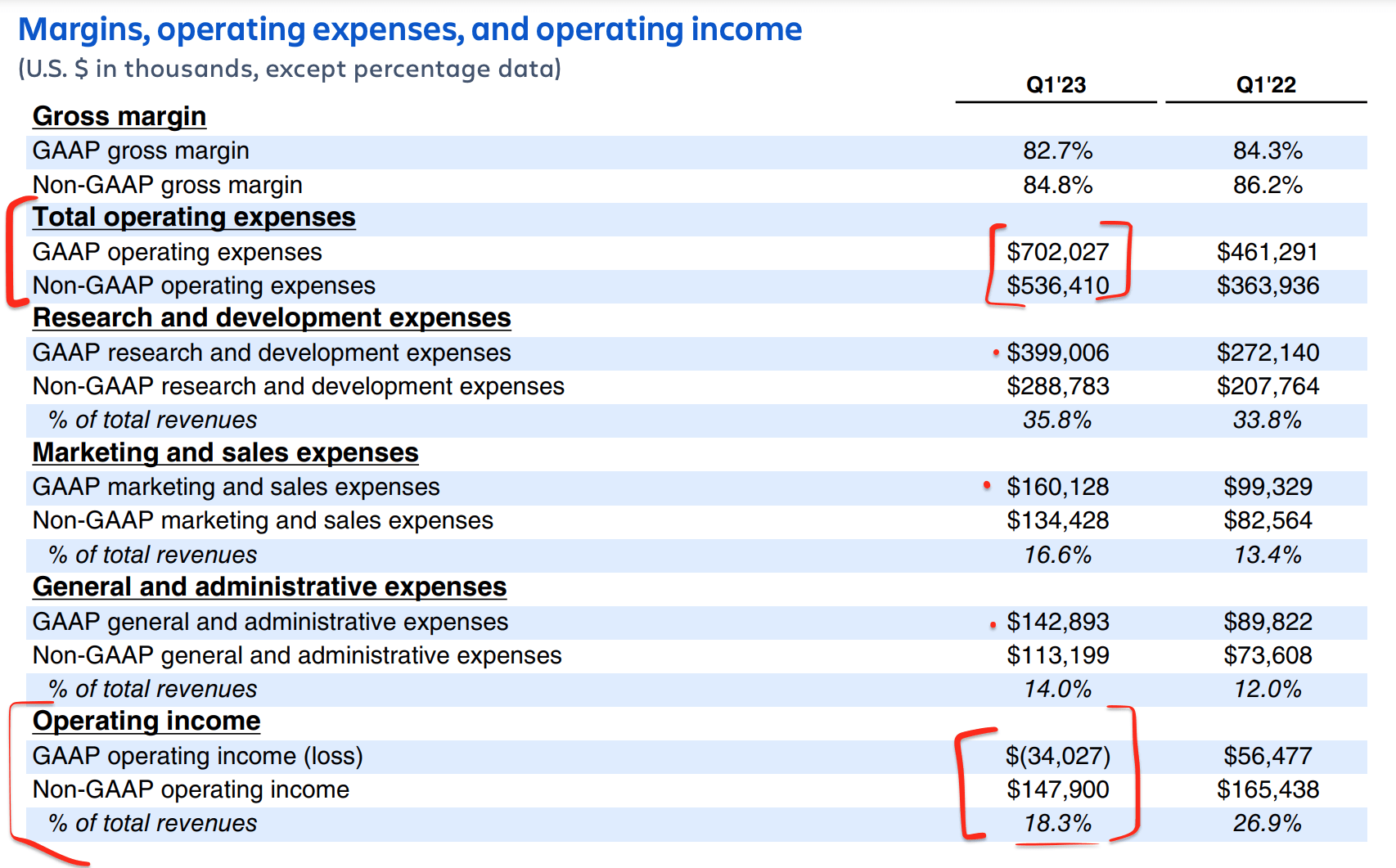

Moving onto profitability (or the lack thereof), Atlassian reported earnings per share of negative $0.05, which was better than the negative $1.63, reported in the same quarter last year. This also surprisingly beat management expectations by $0.64. However, if we take a step back the company actually produced positive operating income of $56.477 million in Q1,FY21, relative to the negative $34 million generated in Q1 FY23. The main discrepancy looks to have come from a large $425 million expense last year, which made its EPS look worse than it was. A simple way to analyze the profitability trends of the business is to analyze its expenses as a portion of revenue. In this case, R&D, S&M, and G&A have all increased by absolutely and as a portion of revenue (details on the table below). The R&D and S&M expenses don’t bother me, as the company is in a new product development and go-to-market phase, which should hopefully generate ROI long term. However, over time I would like to see G&A expenses decline as a portion of revenue (currently at 14%). Given Atlassian is a software company with high scalability, I see no reason why the company cannot accomplish this long-term.

Profitability and expenses (Q1 FY23 report)

A positive for Atlassian is its free cash flow has increased by 30.6% year over year to $75.9 million. It is 0.1% lower as a portion of total revenue. However, this is mainly driven by a huge increase in capital expenditures, which increased from $6.8 million to $16.5 million. Capital expenses in themselves aren’t a bad thing, assuming the company can generate ROI long-term.

Atlassian Free Cash Flow (Q1 FY23)

Atlassian has a solid balance sheet with $1.544 billion in cash and short-term investments. The company has total debt of ~$1.344 billion, but the vast majority of this $999.5 million is long-term debt and thus manageable.

Moving forward management believes the current macroeconomic trends of fewer free users converting to paid will continue. This will of course impact growth rates with a range of 40% to 45% expected for Cloud revenue in the full fiscal year 2023. In addition to “moderate” data center growth and “contracting” maintenance revenue for the year.

Advanced Valuation

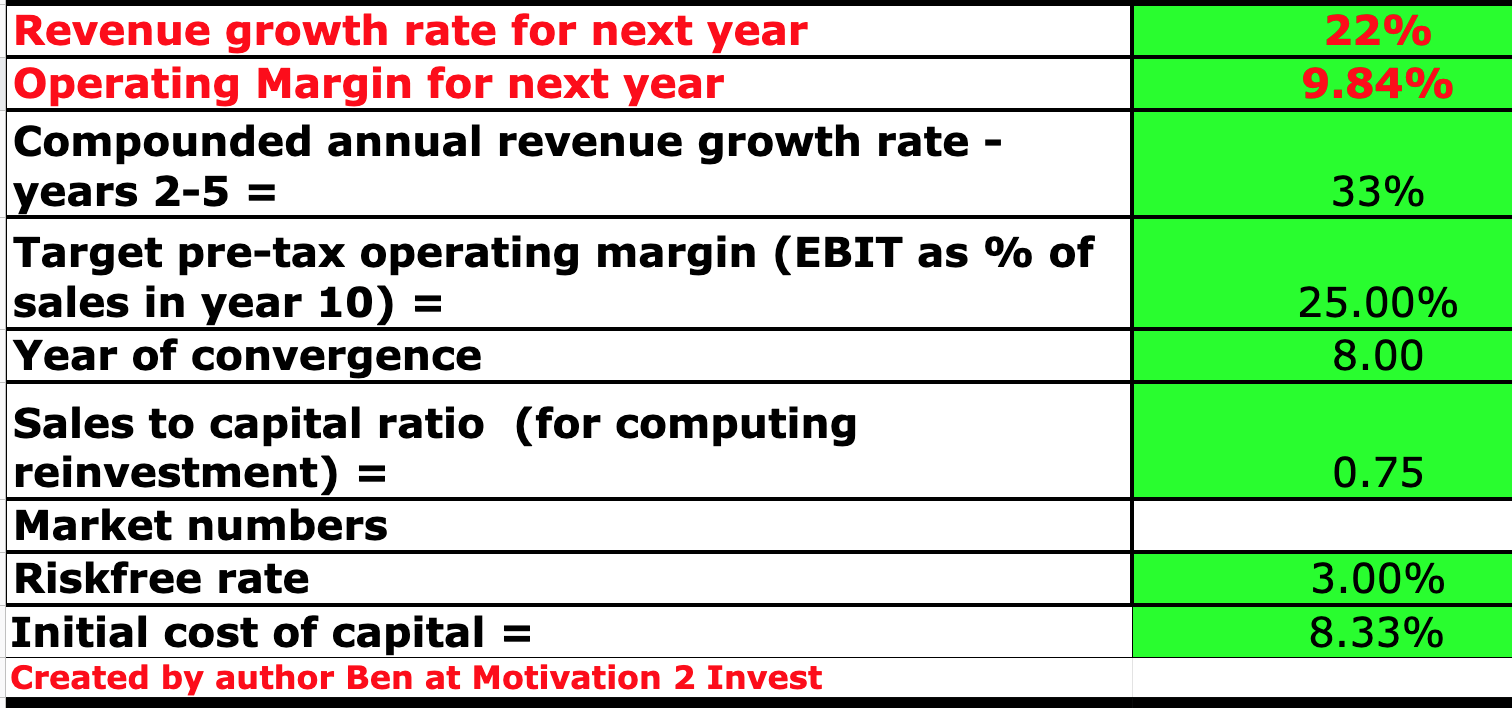

To value Atlassian, I have plugged its latest financials into my discounted cash flow model. I have forecast 22% revenue growth for next year, this is fairly conservative given the company previously grew its revenue at over a 30% rate. I expect this to be driven by the “recessionary” macroeconomic environment and fewer users converting from free to paid. However, in years 2 to 5, I have forecast 33% revenue growth per year. I forecast this driven by new product releases (Atlassian Analytics) and an improving economy.

Atlassian stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation model, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast a 25% pre-tax operating margin over the next 8 years. This is slightly higher than the 23% average operating margin for the SaaS industry. I expect this to be driven by multi-product expansion and cross-sells. For example, Atlassian has introduced an all-in-one license for enterprises.

Atlassian stock valuation 2 (created by author Ben at Motivation 2 invest)

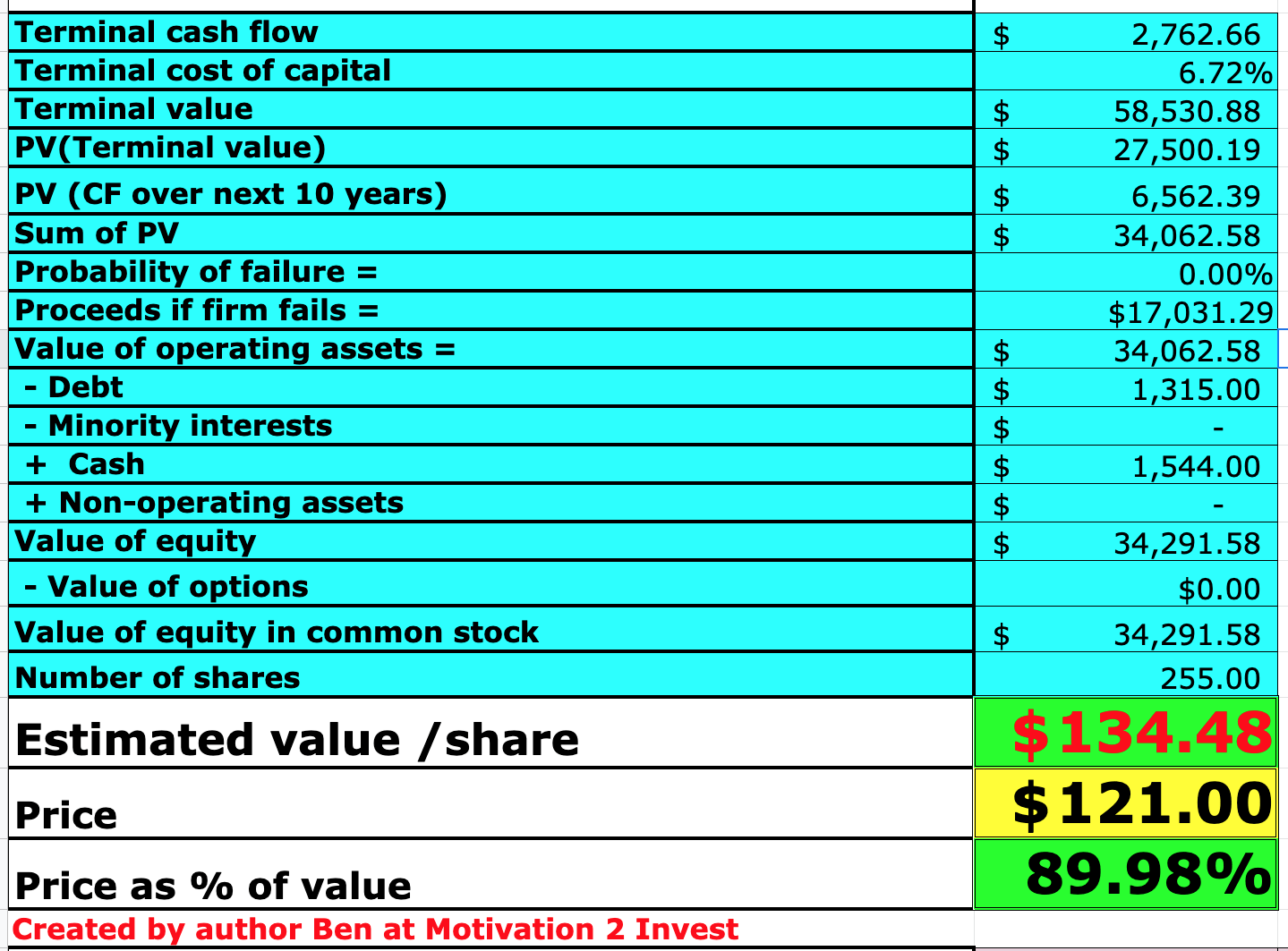

Given these factors, I get a fair value of $134.48 per share, the stock is trading at $121 per share at the time of writing and thus it is ~10% undervalued.

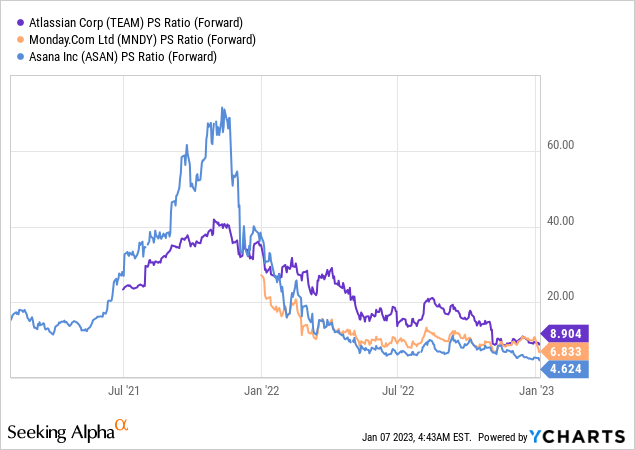

As an extra data point, Atlassian trades at a forward price-to-sales ratio = 8.9, which is substantially cheaper than its 5-year average of over 25. However, the stock is trading at a slightly more expensive valuation than Asana (ASAN) and monday.com (MNDY).

Risks

Recession/slowing growth

Many analysts have forecast a recession for 2023. Even if this doesn’t occur the psychological damage is already done. Decision makers are being more cautious with purchases and Atlassian noted a lower number of its users were converting from free to paid. Therefore I do expect slower growth for at least the next year.

Final Thoughts

Atlassian is a category leader with its software/product development platform and is poised to benefit from growth in the overall industry. The company has continued to innovate and expand its product, thus it has many opportunities for cross-sells and up-sells in the future. Its “low friction” free tier should enable more users to be collected and ready to convert to paid, as economic conditions improve. Atlassian’s stock is undervalued intrinsically and relative to historic multiples, thus it could be a great long-term investment.

Be the first to comment