Sundry Photography

Nutanix, Inc. (NASDAQ:NTNX) is one of the leading companies that simplifies digital transformation. It provides single software platform for all hybrid and multi-cloud applications and simplifies database management. An interesting catalyst that this company has is its growing customer base and how it has maintained a net promoter score of 90. In fact, according to management, their end customer (for 18 months or above) on average increases spending by 7.1x from their initial investment. These snowballed to its improving profitability outlook for FY ‘23. However, further dilution will remain a key risk for the company and considering its current valuation, I believe NTNX remains unattractive.

Company Overview

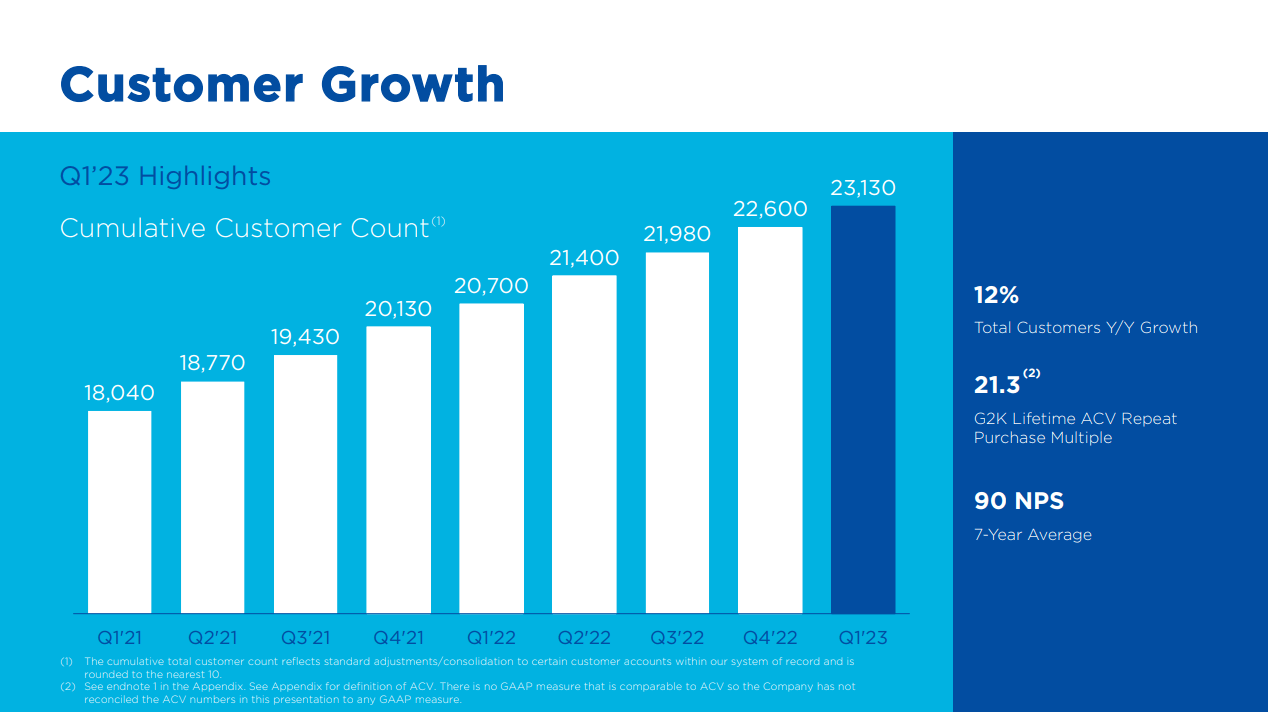

NTNX ended its Q1 ‘23 with a revenue amounting $433.6 million, up from $378.5 million recorded in Q1 ‘22. This is thanks to its sticky product and growing customer base, as shown in the image below.

NTNX: Customer Growth (Source: Q1 ‘23 Earnings Presentation)

In fact, according to management, their Global 2000 end customers spend 21.3x more than their initial investment, up from 20.9x in Q4 ’22. One of Nutanix’s highlights is its successful Azure partnership with its NC2, which will further improve customer experience, as mentioned below.

On the product and partnership front, we achieved an important milestone in realizing our hybrid multi-cloud vision with the general availability of NC2 on Microsoft Azure. Now with support of AWS, Azure and service provider cloud environment, we continue to deliver on our hybrid multi-cloud vision. Our customers have the ability to rapidly and seamlessly shift their workloads between their private clouds and the largest public cloud providers, with a consistent management, governance and data services provided by the Nutanix Cloud Platform, all without the time and expense of refactoring their workloads. Source: Q1 ‘23 Earnings Call Transcript

NTNX is gaining some momentum on its effort to upgrade its Nutanix cloud platform to accelerate the adoption of Kubernetes-based application in the enterprise, as quoted below.

In keeping with our philosophy of offering customers choice throughout the stack, we added Amazon’s Kubernetes service to an already long list of supported Kubernetes container platforms, including Red Hat, OpenShift, SUSE Rancher, Google Anthos, Azure Arc and our native Nutanix Kubernetes Engine. We also added built-in infrastructure as core capabilities and advanced cloud-native data services for modern applications, both of which will enhance the Nutanix cloud platform’s ability to efficiently run Kubernetes applications at scale. Source: Q1 ‘23 Earnings Call Transcript

Furthermore, management sees continued progress in their efforts to make the transition towards a more subscription-based software company with improving ACV billings and ARR.

ACV billings in Q1 was $232 million, higher than our guidance of $210 million to $215 million and representing a year-over-year growth of 27%.

…

ARR at the end of Q1 was $1.281 billion, a year-over-year growth of 34%. New logo additions were about 530 in Q1. Source: Q1 ‘23 Earnings Call Transcript

Finally, NTNX has $1.48 billion in total deferred revenue, demonstrating that the demand environment remains healthy and businesses continue to invest in digitalization.

Improving Profitability

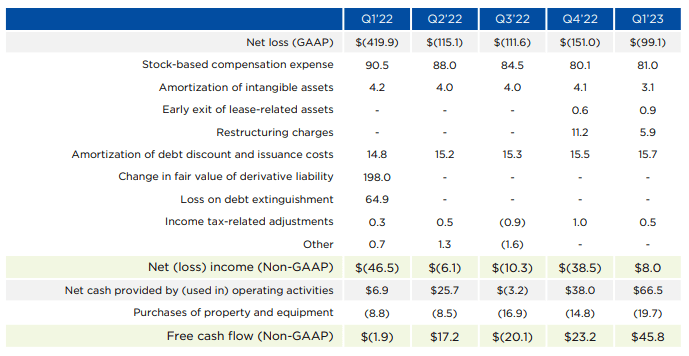

NTNX: Improving Profitability (Source: Q1 ‘23 Earnings Presentation. All Amounts in Millions)

Another value-adding catalyst is NTNX finally recognized its first positive bottom line (Non-GAAP) of $8 million and EPS of $0.03. It also reduced its stock-based compensation expenditure, as indicated in the image above; despite this, it generated $66.5 million in cash flow from operations, leaving the company with a positive FCF of $45.8 million.

Trading Below 200-day SMA

NTNX: Weekly Chart (Source: Author’s TradingView Account)

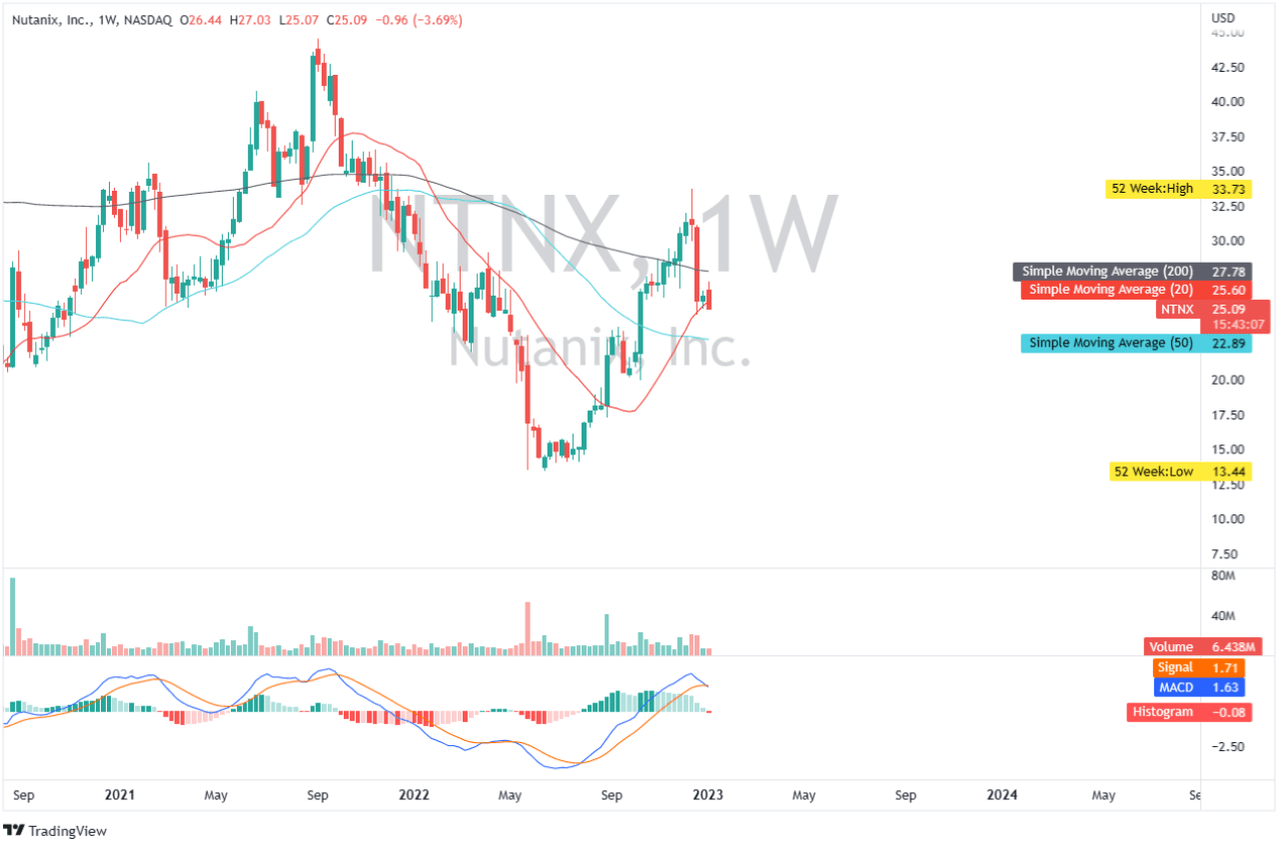

NTNX just broke its support from its 20-day simple moving average, as indicated on the weekly chart above. This indicates a negative price action sentiment which coincides with its price placement below its 200-day simple moving average. The immediate psychological support to monitor is around $23. If this level is not maintained, the price may retest its 52-week low of $13.44. When looking at its MACD indicator, we can see that it is now indicating some price action weakness and a potential bearish crossover might draw bear momentum.

A Bit Expensive

NTNX: Relative Valuation (Source: Data from Seeking Alpha. Prepared by the Author)

Informatica Inc. (INFA), PTC Inc. (PTC), VMware, Inc. (VMW)

NTNX is starting to improve its profitability and is expected to have a favorable forward EV/EBITDA ratio of 41.59x. However, when compared to its peers’ projected EV/EBITDA multiples, as indicated in the image above, it remains pricey. On the other hand, it is trading at a trailing EV/Sales of 3.57x, which is much cheaper than its peers and has a forward EV/Sales of 3.28x, well below its peers’ average of 4.74x.

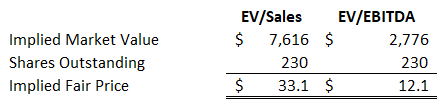

NTNX: Relative Valuation (Source: Prepared by the Author)

We can arrive at a conservative average fair price of $22 based on an implied EV/Sales of 4.74x and EV/EBITDA of 22.06x, analyst revenue estimate of $1.78 billion, expected EBITDA of $141.2 million in FY ’23, and a 10% discount. As of this writing, this makes the stock unattractive, and as a result, I believe waiting for a purchasing opportunity below $22 will give a better and safer entry point.

Risk

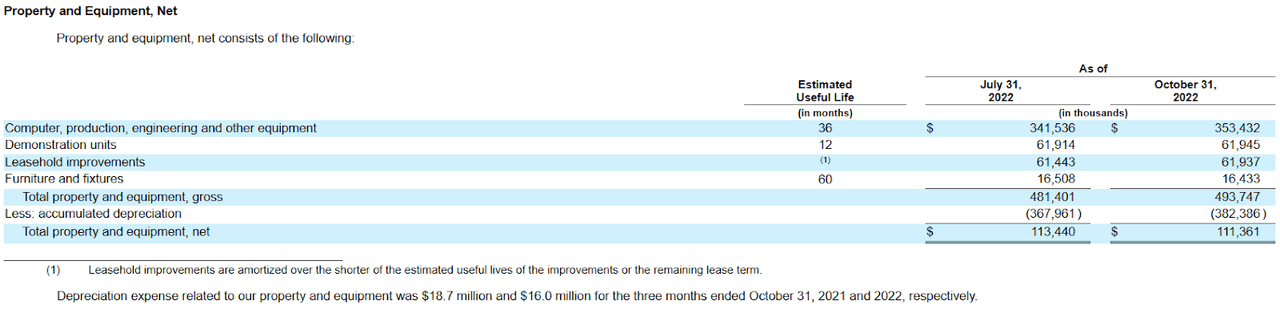

NTNX: Aging PPE (Source: Q1 ‘23 Report)

However, upon further investigation, NTNX’s PPE, which is mostly made up of computer-related assets, is actually aging, as seen by its dropping Net PPE value. Furthermore, as part of the company’s cost-cutting strategy, management announced that they will be reducing their labor force. As a result, this might have a detrimental impact on NTNX’s future growth. On top of this dilution remains a problem for the company, as the management provided a higher Weighted Average Shares Outstanding (Non-GAAP) amounting to 279 million in Q2 ‘23.

Final Key Takeaway

NTNX showed improving profitability, which might be sustainable considering its growing customer base. However, further growth seems uncertain, especially considering the mentioned risks and without the M&A with Hewlett Packard Enterprise (HPE). Furthermore, it is alarming to see that its total debt has increased to $1,449.8 million, putting pressure on the company’s overall profitability through higher interest expense obligations. To conclude, I believe NTNX is an unappealing investment at the time of writing, although it is worth monitoring.

Thank you for reading and good luck!

Be the first to comment