marchmeena29/iStock via Getty Images

Uncover the secrets of Stifel Financial Corp.’s (NYSE:SF) success and find out why it’s a top pick for savvy investors looking to capitalize on the thriving financial services industry.

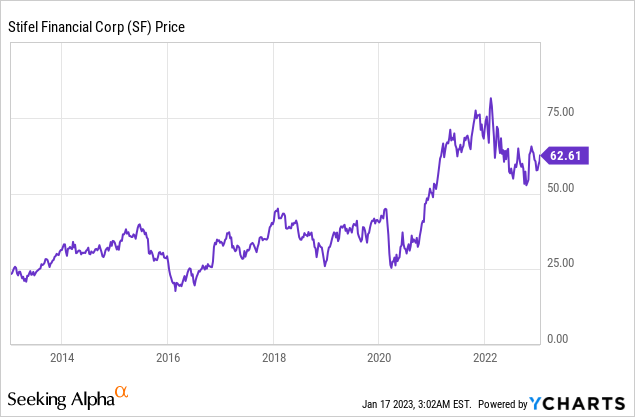

Stifel’s stock market returns were decent over the past decade. The companies’ continuous growth in revenues, earnings, and cash flows was rewarded by a decent share price return. There is more upside as its growth was faster than the graph shows.

About Stifel Financial

Stifel Financial Corp. is a financial services holding company founded in 1890 and headquartered in St. Louis, Missouri. The company operates through several subsidiaries, including Stifel Nicolaus & Company, Inc, a retail and institutional brokerage firm, and Keefe, Bruyette & Woods, Inc, a leading investment banking firm that specializes in the financial services industry.

Throughout its long history, Stifel has established a reputation for providing high-quality financial services and advice to its clients. The company’s success can be attributed in part to its focus on strong relationships, a commitment to integrity and excellence, and a deep understanding of the industries and markets in which it operates.

Looking ahead, Stifel’s strong financial position and diversified revenue streams position the company well for continued growth and success. The company’s solid capital base, coupled with a pipeline of potential deals, bodes well for its future profitability and performance. Furthermore, the company has been doing well over the last years with growing revenue and expanding presence across the US and some other countries as well.

Upcoming Earnings

Stifel’s Q4 earnings are expected on January 25. There was positive news from its AuM as it rose in November by 4.7% after it also increased by 5% in October. December should be flattish as the markets declined slightly which could be offset by inflows. Global Wealth Management probably gains importance as M&A activity remained slow during Q4. A drop in earnings in comparison to Q4 2021 is expected.

Its 2023 guidance could surprise the market positively. Markets had a good start in 2023 and M&A activity is expected to increase by market participants according to Deloitte.

Growth

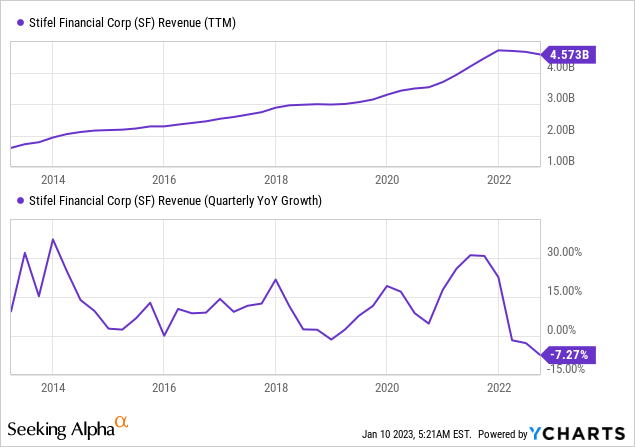

Stifel grows through regular acquisitions and organically. Its focus led to an impressive increasing revenue of 11% CAGR over the past decade.

Recent revenue growth stalled due to the dropping financial markets. Overall, its assets under management only dropped ~5% up until November 30. Pretty good in comparison to the S&P 500 (SP500) drop of 17.5% in the same period. This is due to net inflows of assets under management.

Forward Growth

Stifel needs a revival of the M&A market to get back on a substantial growth track. I find it hard to predict such factors in the near-term (1-2 years) as it depends on a lot of macroeconomic factors that experts get wrong all the time.

It just acquired another specialized M&A house, Torreya Partners. The addition grows its presence in the advisory to the life science industry. A sector with plenty of M&A activity.

Global Wealth Management could recover quickly as markets get back up. It has the same unpredictable near-term as the M&A market. Over the long run, a 7% to 10% growth rate is reasonable.

In the long run, such markets always recovered and it’s plausible that Stifel gets back to high single-digit or low double-digit revenue growth rates.

Strong Profitability And Free Cash Flow

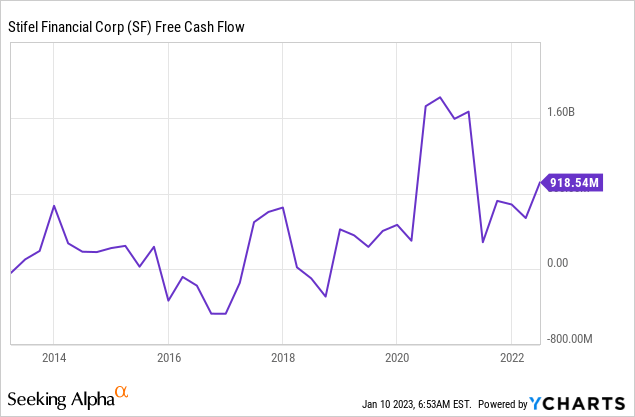

Free cash flow is vital as this is what a company could use for shareholder returns. Potential buybacks or dividends are only possible if the company produces enough cash.

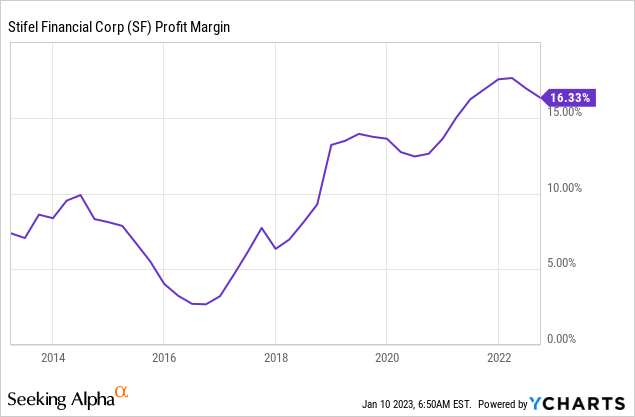

Stifel improved margins drastically by increasing its scale and focusing on undercovered areas of the stock market. Its model of acquisitions and organic growth worked well. These margins hold up through 2022 as well despite slower closings in its M&A business. Dropping revenue in investment banking is partially compensated by lower variable costs. The increase in net interest income also helped offset the lower income from other divisions.

Strong margins and growing revenues also lead to an increasing free cash flow for Stifel:

Free cash flow is a bit lumpy but is in line with its earnings in the long run. It generates plenty of cash keeping open options for organic growth by growing loans, acquisitions, and shareholder returns.

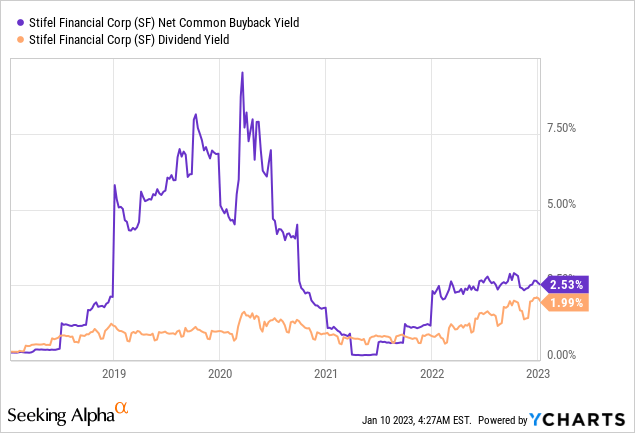

Shareholder Returns

So given our high level of profitability, the fact that our capital ratios are well above our target levels and the fact that we will slow our balance sheet growth, it is likely that our capital deployment will focus more on dividend increases and share repurchases and, if appropriate, acquisitions.

CEO Ron Kruszewski – Q3 Earnings Call

A shift in capital deployment favors shareholder returns over growth in the near future.

Stifel introduced a dividend in 2017 and has committed to strong dividend growth. The dividend even doubled in 2022 while keeping a low payout ratio of ~20%.

Share repurchases stopped in the most recent quarter. The company has an open buyback program for 10.3 Million shares out of 106.2M shares outstanding. Opportunistic buybacks during fallbacks on the stock market should support the share price.

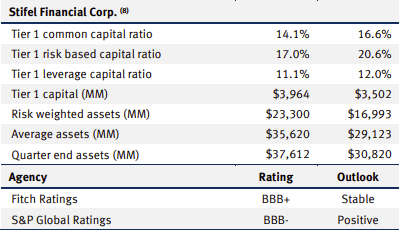

Balance Sheet

Stifel works with a strong balance sheet and keeps a lot of excess capital above its minimum requirements. Its Tier 1 ratios are more than adequate and it gets investment grade ratings from Fitch and S&P Global.

Stifel Investor Presentation Q3 (Seeking Alpha)

The Tier 1 leverage capital ratio minimum is 5%.

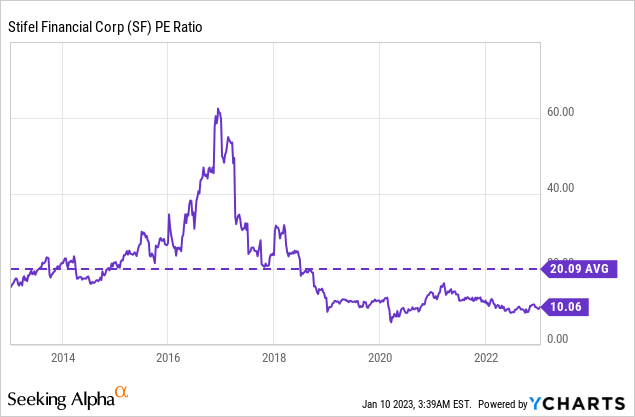

Valuation

Stifel looks undervalued. It has the highest dividend yield since it started paying one as shown in the shareholder returns section above.

The PE ratio is far below the 10-year average and only got lower during the pandemic lows. Keep in mind the company has grown revenue by 10% annually and EPS by 28% since 2015. The current valuation leaves a lot of share price upside while you get paid a nice dividend to wait.

Risks

I believe near-term growth will slow a bit in favor of shareholder returns. Slower growth could mean it needs to look for a new investor base. The current environment of rising interest rates provides new opportunities and risks for investment firms.

Stifel’s asset management could get threatened by passive investment possibilities like ETFs provided by competitors like BlackRock (BLK). Their low costs and decent returns pose a continuous threat. So far, Stifel managed to grow pretty well despite this competition.

Conclusion

Stifel has a lot going for it in the long run. It diversified its business towards more asset management and profited from strong M&A activity in the past. Near-term headwinds made the share price stall. The valuation remains rather low for a company with strong growth in revenue and shareholder returns. It has the attributes of a cashflow compounder.

Be the first to comment