Oselote

You can ask ChatGPT for the top 10 reasons for owning gold and get a sufficiently operational list. This list is quite familiar to anyone who follows gold:

- inflation or currency hedge

- portfolio diversification

- store of value

- safe haven against geopolitical drama or economic uncertainty

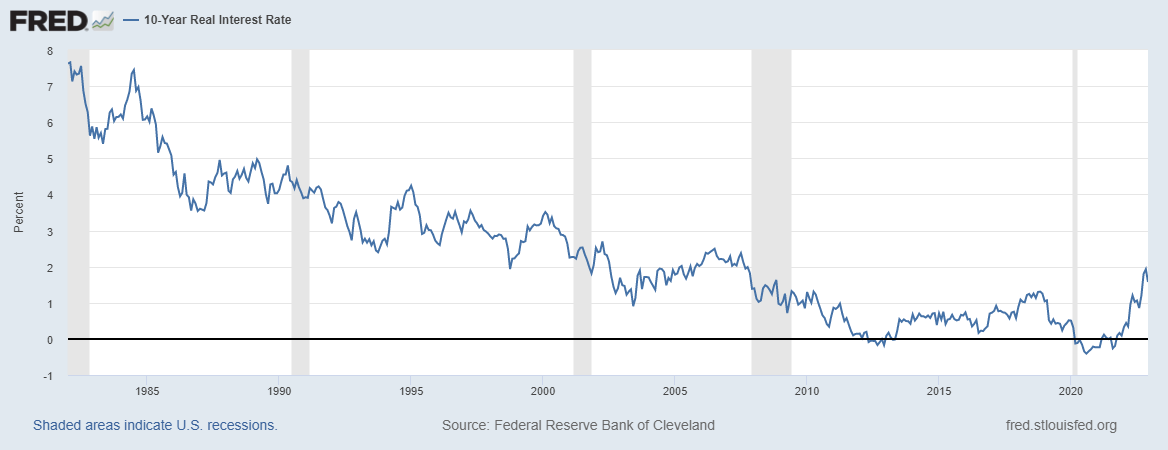

Back in 2013, I critiqued a paper called the “Golden Dilemma” by Claude B. Erb and Campbell R. Harvey (of Duke University and the National Bureau of Economic Research respectively) which presented a superset of reasons for owning gold and debunked each and every one. Erb and Harvey thus concluded that gold was overvalued even though it could still go higher driven by speculators chasing momentum. Since then, GLD is up around 30% (and rising). However, that gain is a sliver of the 127% (and falling) performance of the S&P 500 (SPY) over that time. It just so happened that my 2013 piece also coincided with the end of the secular decline in the 10-year real interest rate. The decline starting in 2007 helped ignite a tremendous run-up in GLD.

The 10-year real interest rate ended its secular decline in 2013. The recent rise is helping to hold a ceiling over gold. (Federal Reserve Bank of Cleveland, 10-Year Real Interest Rate [REAINTRATREARAT10Y], retrieved from FRED, Federal Reserve Bank of St. Louis; December 22, 2022.)

So, technically, gold has fared relatively well all things considered, especially with the U.S. dollar gaining in value: the Invesco DB US Dollar Index Bullish Fund (UUP) is up around 27% since my 2013 piece. In other words, holding gold over this time (and longer) requires a permabull mentality anchored by gold as a portfolio diversifier.

Seeking Alpha author Victor Lai recently concluded that gold has use as a portfolio diversifier after poignantly asking whether gold should be considered a low-risk safe haven. Lai observed that “based on historical data, gold does not appear to offer a meaningful hedge against risky assets like stocks. Furthermore, from a volatility perspective, gold has been as risky as stocks, and sometimes even more so.” I appreciate this risk and volatility differently. I see it as an opportunity to trade around my core GLD position. I also acknowledge that gold has different “seasons.” In my early post I claimed “it is more interesting to think of gold as moving in three distinct phases in the past 40+ years: a rapid run in response to the inflationary 1970s, a steady decline for twenty years as inflation rates came down, and finally another rapid run-up as the U.S. dollar index experienced a new secular decline.”

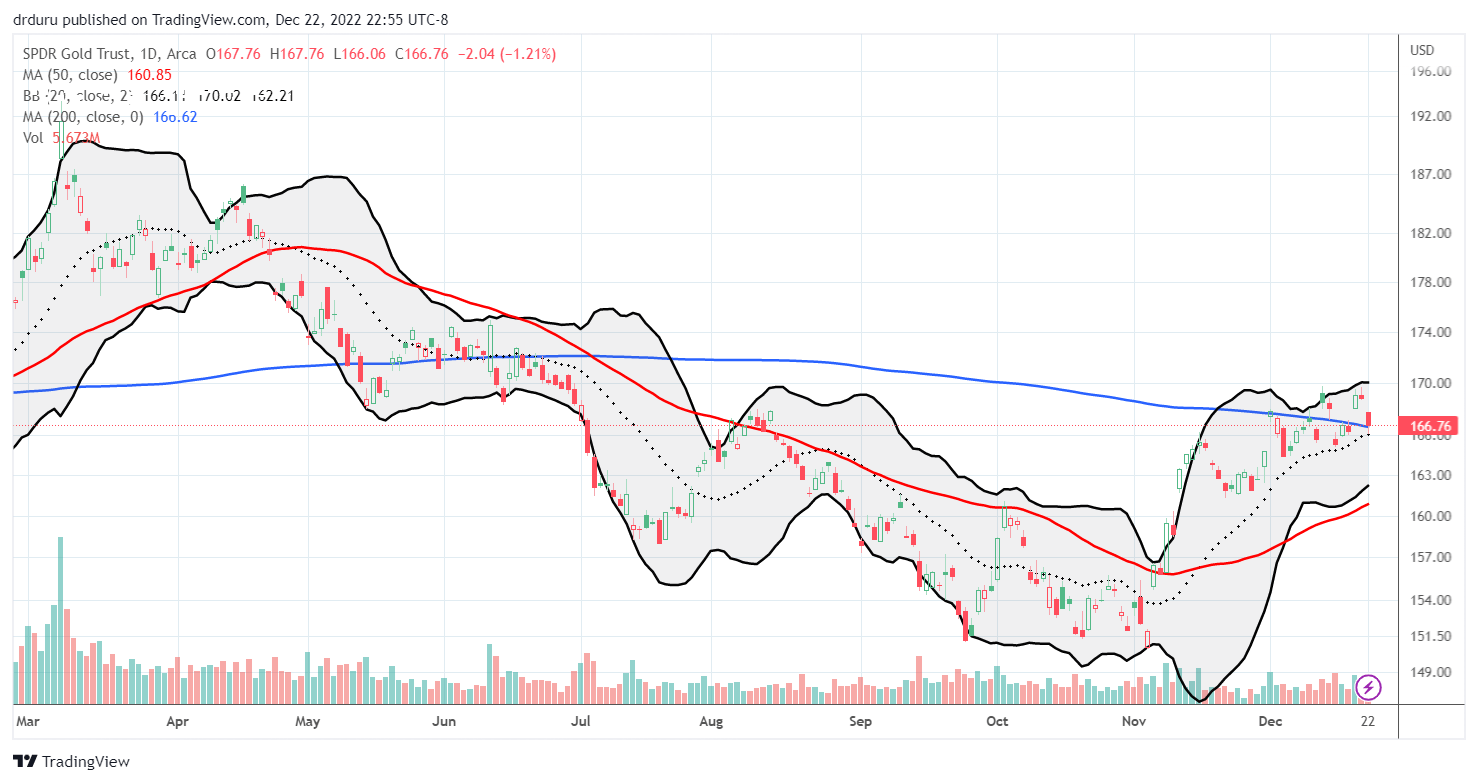

We are now in an era of the dollar’s secular increase in value. This era may finally come to an end once the Federal Reserve ends its cycle of monetary tightening in a scramble to over-correct against inflationary pressures. The market almost seems ready to look ahead to this next season for gold. Both the short-term and long-term views are suggestive. GLD is currently scraping at the edges of an important technical breakout above its 200-day moving average (DMA) (the blue line below). This 200DMA has created a “gravitational pull” on GLD since early 2021. Thus, a breakout above this important long-term trend line could lead to a sustained launch to higher levels. I am currently anticipating that prospect with rolling GLD call options.

The SPDR Gold Shares (TradingView.com)

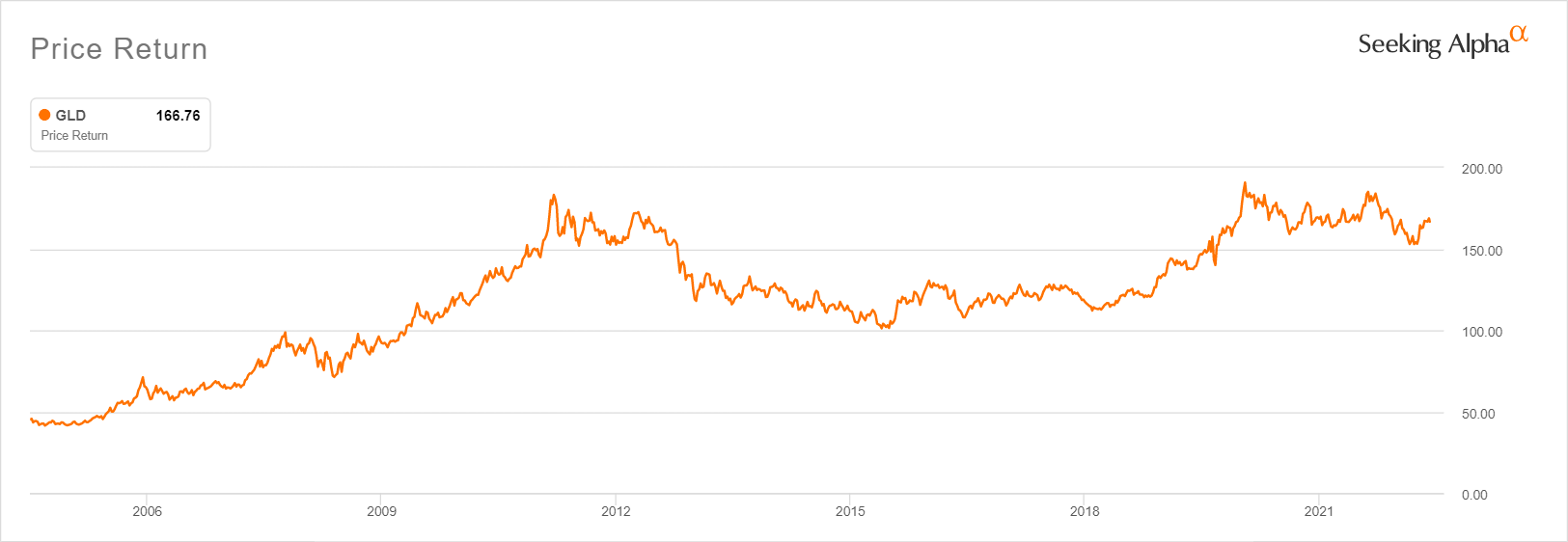

A multi-year chart makes GLD look like it is ready for a breakout. The turbo blast of stimulus in response to the pandemic helped push GLD briefly past its 2011 high. Since then, GLD has settled into a trading range above the $150 level. The longer $150 holds and GLD consolidates, the more likely a positive catalyst will send GLD above the current range.

The SPDR Gold Shares (Seeking Alpha)

The catalyst could come in the form of an acceptance of an economy with a historically higher inflation rate.

A Higher Inflationary Environment

Inflation has peaked, but the path to the Federal Reserve’s 2% target is quite unclear. Current macro-economic and policy signs point to a slow-growth, higher inflation era around the corner. Mohamed El-Erian predicts that eventually the Fed will acquiesce to a stable but higher-than-target inflation rate. While the Fed will continue to talk about the path to 2%, gold could surf higher awaiting proof that such a target is possible. This is mostly speculation on my part of course, but I think the scenario has a high enough probability to warrant trading.

A Look Back at the Google Search Trends Indicator

There was a time when I actively reported on extremes in Google search trends on the phrase “buy gold”. These extremes tend to signal changes in trading direction for GLD, so I created a simple rule of thumb. If Google searches on “buy gold” surged along with an extreme move in GLD, whether up or down, then anticipate a reversal in GLD’s price direction. I hypothesize that a spike in searches signals the final swell of interest in the current direction of GLD, especially to the upside. In other words, on the way up surges in searches on “buy gold” come from the last buyers of the trend; the short-term directional bets get exhausted. I did not find a compelling relationship on searches for “sell gold”. Accordingly, the driver of the end of a sharp plunge in GLD acts on a different dynamic: “buy gold” searches likely come from traders eager to get in early on the latest discount.

The search spikes in recent years do not compare to the spikes from the great financial crisis. Also, the spikes are clearer for U.S. searches whereas in the past I used worldwide search. Yet, the three recent spikes are still instructive.

Surges in “buy gold” searches are not as prominent as earlier years, but they are just as important. (Google Trends)

U.S. searches for “buy gold” spiked in May, 2020, July, 2020, January, 2021, and most recently March, 2022. In 3 of 4 cases, gold’s price reversed direction. The May, 2020 spike came on the heels of the rebound from the pandemic lows and preceded a parabolic run-up for gold. That parabolic run-up ended with a July, 2020 spike higher for Google search trends on “buy gold.” A subsequent and sharp recovery in GLD ended alongside the January, 2021 Google trends surge. Finally, the March, 2022 search spike marked the end of GLD’s last parabolic run-up. GLD is still trying to recover from that hyper-activity that occurred as gold bugs started to conclude that the Fed was going to move too slowly against inflation. Oh have times quickly changed! The Fed’s increasing hawkishness has unsurprisingly slammed a ceiling over GLD.

Summary

I am a gold bug who sticks by GLD as a portfolio diversifier. I do not require any specific correlation to work for GLD over decades. Instead, I am content to trade around gold’s seasons. I anticipate that the next season for GLD will take it much higher as inflation stubbornly lingers above the Fed’s 2% target, and the Fed is forced by a contracting economy to end rate hikes. I will refer to Google search trends on “buy gold” as an approximate indicator that the next run-up has likely run its course. If a significantly different scenario materializes, I will make the needed changes to my trading strategy. My core position will stay year-in, year-out.

Be careful out there!

Be the first to comment