MarsBars

Asset-light companies such as those in financial services are a great way to diversify one’s portfolio while also earning some additional income on the side. While names like T. Rowe Price (TROW) and Franklin Resources (BEN) may be familiar among retail investors, there are other durable names that are well-known amongst institutional investors and can provide lasting long-term value.

This brings me to State Street Corporation (NYSE:STT), which is demonstrating strong results with economic resilience. In this article, I highlight what makes STT an ideal choice for those seeking long-term growth and income growth potential to boot, so let’s get started.

Why STT?

State Street Corporation is a leading financial services company that provides investment servicing, management and research and trading in more than 100 markets globally. It’s also one of the world’s largest custody banks with $36.7 trillion in assets under custody and/or administration, and $3.5 trillion in assets under management.

STT is demonstrating resilience against macroeconomic uncertainty, with revenue growing by 1.8% YoY despite weaker equity and fixed income markets throughout much of 2022. This performance was driven by higher interest rates, with net interest income rising by 34% for the full year 2022, due to higher rates and effective deposit and balance sheet management.

Moreover, STT saw positive 12% spreads from FX trading services and front office software and data revenue grew by an impressive 14% for the full year. Notably, STT is seeing positive operating leverage, as expense growth was flat, thereby translating the aforementioned 1.8% revenue growth to benefit the operating margin.

Importantly, STT is being conservative with financial management given near term macroeconomic uncertainties. This includes winding down expenses related to its Brown Brothers Investor Services acquisition transaction, which it is no longer pursuing. In addition, STT is rightsizing its ranks by eliminating 200 middle and senior management positions, which would help with expense management and operating leverage in 2023.

Looking ahead, STT is well-positioned to continue reaping the benefits from high interest rates, while fee revenue could see a rebound, as the equity market has staged a bounce back so far this year. This is reflected by the S&P 500 (SPY) being up by 7% so far this year, which bodes well for STT’s assets under management. Morningstar sees potential for STT to generate solid returns on equity, as noted in its recent analyst report:

We expected continued growth in 2023 as there are still some easy comparisons from the first half of 2022. After that we expect net interest income growth to slow in 2024 and then stall thereafter. Fee revenue is sensitive to many factors such as equity market movements and volatility. The market downturn will weigh on 2023 asset based fees. After 2023, we expect low-single-digit growth as the firm continues to face pricing headwinds from a consolidating asset management industry. We expect State Street’s tangible returns on equity to be in the mid-teens during the forecast period.

Meanwhile, STT maintains a strong A rated balance sheet and carries a common equity tier 1 capital ratio of 13.6%, sitting well ahead of the 6% minimum requirement for large U.S. financial institutions.

STT also pays a respectable 2.7% dividend yield that’s well-protected by a 32% payout ratio. It also comes with an 8.5% 5-year dividend CAGR and 12 years of consecutive growth.

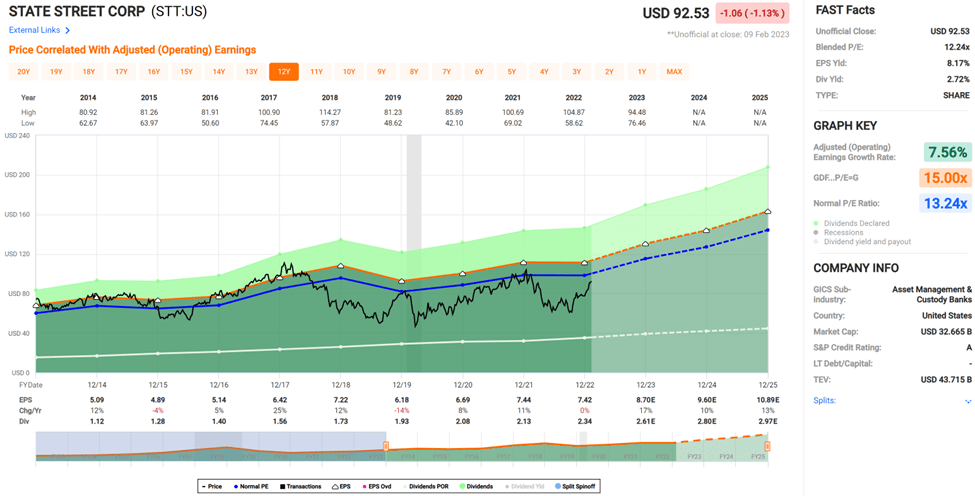

Lastly, I see value in STT at the current price of $92.53 with a forward PE of 10.8, sitting well below its normal PE of 14.3. This appears to be attractive, especially considering that analysts expect 10-11% annual EPS growth over the next 2 years. With a multi-lever revenue base and a solid dividend yield, STT can potentially deliver long-term total returns in the low-teens from the current price. Analysts also have a consensus Buy rating on the stock with a conservative price target of $95.

FAST Graphs

Investor Takeaway

State Street is a well-established financial service firm with a strong balance sheet and solidly protected dividend yield. STT is showing signs of operating leverage and resilient revenue growth in the face of macroeconomic headwinds. This bodes well for future profitability, especially considering the current high interest rate environment and equity market performance so far this year. STT has also taken steps to manage expenses, and at the current valuation, could potentially deliver strong long-term total returns.

Be the first to comment