shaunl/E+ via Getty Images

A Business Lagging Behind

Star Bulk Carriers Corp. (NASDAQ:SBLK) is a mid-cap Greek dry bulk shipping company that has been a well-known and established name in the industry for over a decade. The company operates a fleet of 128 vessels, including Newcastlemax and Supramax ships, with a total deadweight tonnage capacity of 128.

Like many other dry bulk companies, Star Bulk Carriers faced a challenging H2 2022, with its stock price dropping from around $34 in June to $16.9 by September due to the declining dry bulk commodity market and declining freight rates. Investors are hoping for a rebound in demand as China re-opens and demand picks up.

However, the decline in demand has also impacted SBLK’s profits, putting its attractive dividend yield of close to 30% into question as to whether it is sustainable. After several years of high dividend payments, it may not be the best investment for investors seeking dividends. With slowing growth, the possibility of a global economic downturn, and SBLK’s weaker performance compared to its competitors, we recommend selling SBLK stock. It’s always important to carefully evaluate risks and opportunities before making any investment decisions and to diversify your portfolio.

Star Bulk: From Humble Beginnings

Star Bulk has been a well-known name in the dry bulk industry for almost two decades. Since its establishment in 2006, the Athens-based company has experienced significant growth and established itself as a major player in the global dry bulk industry. Its services span across the globe, providing investors with exposure to multiple continents, which can be highly attractive in a bull market. Each year, SBLK ships more than 60 million tons of dry bulk commodities and prides itself on its relatively modern fleet, with an average age of around 10 years.

SBLK owns and operates all 128 of its vessels through its subsidiaries, which gives it a strategic advantage in reducing operating costs and corporate overhead, while also maintaining business synergies. They pride themselves for being able to maintain a healthy balance sheet through all times in the economic cycle, which is true, as they sit on a debt to asset ratio of about 0.4.

Market outlook and risks

The global dry bulk market is anticipated to experience a decline in 2023 and potentially into 2024, according to a recent market report from Maritime Strategies International (MSI).

The decreased earnings are largely attributed to the unwinding of port delays, which had supported the market during 2020-2021, as port operations return to normalcy. MSI predicts improvements in fleet efficiency, though acknowledges that this process may be impacted by the ongoing COVID-19 pandemic and various geopolitical and trade factors. Despite its bearish outlook for market balances and earnings, MSI sees the potential for China to drive growth in the industry, driven by a possible steel-intensive stimulus from the government. According to MSI a tightening of market balances is not expected until 2025, with potential for growth in earnings from 2026. According to MSI

For Star Bulk Carriers Corporation, the company is expected to see a decline in revenues in 2023, with a return to its 2021 revenue levels not expected until 2025. These projections, however, are predicated on China’s reopening and the impact this may have on the dry bulk shipping industry. A fully reopened China is expected to drive increased demand, potentially improving SBLK’s outlook for 2023.

Furthermore, the freight rates in the industry are not expected to experience the same level of bottlenecks as seen in 2021, resulting in a relatively normal market cycle compared to recent years. As measured by the Baltic Dry Index (BDI), which tracks the cost of transporting raw materials, the BDI currently hovers around levels seen during the 2008 financial crisis with room for further decline. The direction of the BDI will be largely influenced by China in the coming months.

Stock Info with TradingView

Fortunately, SBLK sits on a relatively high amount of cash, and their solvency measures also look decent. At the moment of writing, they have a D/E ratio of 0.56, a quick ratio of 1.1 and a current ratio of 2.07. SBLK is therefore not in danger of going bankrupt, even with the risks that presents themselves in the current macro environment, however, at this moment in time, better investment opportunities might exist.

Star Bulk Carriers: A Solid Business but Better Alternatives.

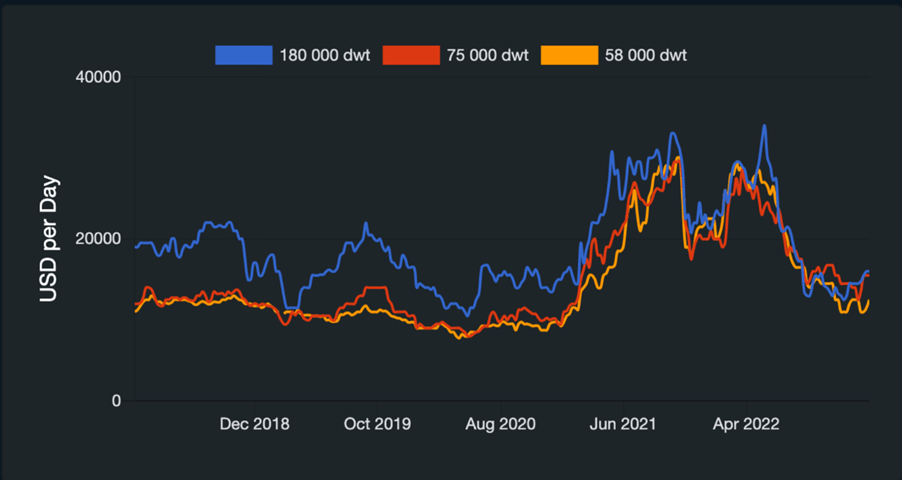

The price of SBLK’s stock has dropped 33% over the past six months as a result of declining time charter equivalent (TCE) rates, which tracks the period-to-period change in revenues per day of a voyage, as is illustrated in the graph below:

TCE rates 2017-2023. (fearnpulse.com)

The decrease in global demand for materials has affected the dry bulk market and making the outlook less favorable. A comparative company analysis indicates that SBLK’s stock price may be slightly high and could potentially decrease more compared to its competitors.

However, it’s worth noting that China is the largest importer of dry bulk commodities and recent efforts by Chinese fiscal and monetary authorities to invest in infrastructure could drive demand for dry bulk vessels.

Furthermore, the opening of China’s economy will inevitably lead to increased demand but ignoring the less-than-ideal development of demand in the west can prove to be a trap. Despite the market outlook, SBLK can still maintain a healthy capital structure through optimization, however other companies might present themselves as better options. The conclusion is that the stock is a sell.

Annual Report SBLK

When it comes to SBLK’s TCE and OPEX per vessel, we can see that SBLK is earning less per day on their voyages, while the costs of operating the vessels on the voyages have increased as well. The table below shows the changes in TCE and daily operation costs for SBLK between Q3 2021 and Q3 2022.

|

Q3 2021 |

Q3 2022 |

YoY |

|

|

TCE per day |

$ 30,626 |

$ 24,365 |

-20.4% |

|

Daily OPEX per vessel |

$ 4,596 |

$ 5,107 |

11.1% |

Not only do they earn 20% less than they did a year ago, the operational cost of the voyages has increased by more than 11%. Falling earnings as well as rising costs are something you don’t like to see as an investor. Furthermore there is a high possibility that this trend could continue in their Q4 2022 earnings report.

These changes have left its mark in their latest earnings report and when we take a look at SBLK’s Q3 2022 report and compare the results with its Q3 2021, we clearly start to see the impacts of the worsening dry bulk market on the earnings. In the table below, you can see that their revenue, operating cash flow, as well as EBITDA, has decreased significantly in just a year. If this trend continues further, it can get quite ugly.

|

Q3 2021 |

Q3 2022 |

YoY |

|

|

Revenues |

$416M |

$364M |

-12.5% |

|

Operating cash flow |

$251M |

$184M |

-26.7% |

|

EBITDA |

$273M |

$164M |

-39.9% |

Although Q3 2022 has been a difficult quarter for most dry bulk shippers, a 12.5% decline YoY in revenues is not necessarily bad considering Q3 2021 was one of the most profitable quarters ever for most dry bulk shipping companies.

However, when looking at the decline in operating cash flow and EBITDA, the picture worsens. With operating cash flow and EBITDA falling by 26.7% and 39.9% respectively YoY. In addition to revenues declining by 12.5%, it should signal to the investor that the business is truly experiencing the headwinds caused by China’s shutdown.

Furthermore, we expect that their Q4 earnings report will be in line with the trend we have seen in their Q3 earnings. It would not be surprising if SBLK decides to hold onto its equity throughout the downturn of a global dry bulk demand. As a result, investors who are looking for attractive dividend yield opportunities in the dry bulk market might be better off looking elsewhere.

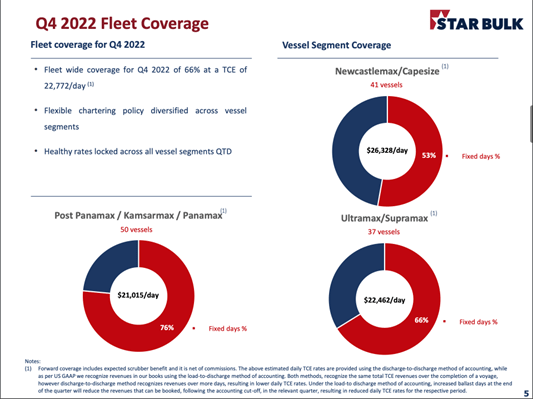

SBLK will present its Q4 earnings on February 16th, and our expectations are that the YoY growth will continue to fall. In addition, it remains a big question as to when TCEs and freight rates will start to pick back up again. The CEO stated that during Q4, the company was able to cover about 66% of its available days with a TCE (Time Charter Equivalent) of $22,772 per vessel per day. This can also be seen in the following slide from their third quarter presentation below.

SBLK fleet coverage going into Q4 (Q3 Earnings Report SBLK)

Despite global economic uncertainties, their CEO remains optimistic about the long-term prospects of the dry bulk market. The current outlook for SBLK is bleak, as the company’s return on invested capital, equity, and earnings are significantly lagging its competitors in the industry. These troubling trends are likely to persist in the face of a challenging market environment, making it a less attractive investment option.

In terms of financial performance, SBLK had an estimated TTM revenue of $866.05M in 2022, with 102.69M shares outstanding. This results in an estimated FCF per share of $8.43, giving an impressive FCF yield of 37%. However, the sustainability of this yield is uncertain, as it is dependent on global demand and supply factors affecting SBLK. To evaluate the potential impact of demand changes, three scenarios were considered: a base case, a bear case, and a bull case. In the base case, we assume that EPS will be equal to what is currently forecasted by the market in 2023, 2024, and 2025 for SBLK. In the bear case, where Chinese demand does not recover as expected, SBLK’s earnings are projected to decrease by 20%. In contrast, in a bull case scenario, where Chinese demand picks up faster than anticipated, SBLK’s revenues could potentially increase by 20%. The expected EPS for each scenario is presented in the table below.

|

EPS |

Base Case |

Bear Case |

Bull Case |

|

2023 |

3.72 |

2.98 |

4.46 |

|

2024 |

4.59 |

3.67 |

5.51 |

|

2025 |

7.00 |

5.60 |

8.40 |

Similarly, SBLK’s dividend yield of 29.31% is also at risk, particularly in a bear case scenario where earnings are expected to decline. This would make SBLK even less attractive to investors, as it loses one of its most attractive traits. With a potential decline in earnings in 2023, resulting in a lower bottom line compared to 2021 and 2022, it is likely that SBLK will adopt a more conservative dividend policy in 2023 to address the situation.

SBLK also starts to look mediocre when compared to its peers, such as Golden Ocean Group (GOGL), Eagle Bulk Shipping (EGLE) and Navios Maritime Partners (NMM), when comparing FCF pr. share, EPS, ROIC, and ROE:

|

FCF pr. share |

EPS |

ROIC |

ROE |

|

|

SBLK |

8.43 |

7.65 |

23.83 |

39.29 |

|

GOGL |

2.89 |

2.98 |

18.79 |

31.3 |

|

EGLE |

23.97 |

24.1 |

29.51 |

43.76 |

|

NMM |

12.1 |

18.93 |

16.08 |

29.76 |

While their return on equity and return on invested capital are relatively impressive compared to their competition, their EPS and FCF pr. share are less than adequate. It appears to us that SBLK may be slightly overvalued compared to its peers and if you are looking to bolster your portfolio by adding dry bulk shipping stocks, there might be better alternatives than SBLK.

Technical analysis

Looking at the technicals behind SBLK, the conclusions appear to remain the same. The RSI is sitting at around 60, while also having previously bounced off resistance levels from back in the summer of 2022. Therefore, it is more than likely that SBLK will see a short-term decline in price and will fall to a price of around $17. We believe this level is important to keep an eye on, as macroeconomic conditions will be the primary driver behind the direction this stock will move afterward.

Stock Info with TradingView

This reaffirms the recommendation that SBLK at this point in time is a sell, as the short-term headwinds are too strong to ignore. However, if you are a long-term investor, it might be worth adding this stock once we are near the next major level of support.

Conclusion

Star Bulk Carriers is a well-established business, but its financial resilience in the face of upcoming challenges may be weaker than that of some of its competitors. Although SBLK is not facing an imminent liquidity crisis, investors seeking attractive dividend stocks may want to consider other options.

The current dividend yield of SBLK is expected to start declining as the company may prioritize preserving cash over paying out high dividends to its shareholders. Given these factors, we believe that this stock is currently a sell. Additionally, the current market conditions may be favorable for selling SBLK shares, with the technical indicators pointing towards a good time to offload the stock. If you hold SBLK shares, it may be wise to sell them now and wait for more favorable market conditions to re-enter the market.

Be the first to comment