Joe Raedle

Stanley Black & Decker (NYSE:SWK) engages in the tools & storage and industrial businesses globally. The firm’s primary products include electric power tools and equipment, pneumatic tools and fasteners, home products, garden products, hydraulic tools, and performance-driven heavy equipment attachment tools.

We have already published an article on SWK titled: “Stanley Black & Decker: Temporary Headwinds, Long-Term Opportunities” in August 2022.

Analysis history (Author)

Today, we have decided to revisit SWK, as the firm has released earlier in February its Q4 and 2022 full year results. First, we will take a look at the company from a profitability and efficiency point of view, and how these metrics have been changing over the past 5 years. At the same time, we will be commenting on their potential further development, while addressing the latest earnings results.

Our discussion will be primarily centered around the net profit margin, asset turnover and equity multiplier.

So let us dive into the topic by starting with the net profit margin.

Net profit margin

Net profit margin essentially measures how much of the revenue the firm can keep as a profit after accounting for the costs.

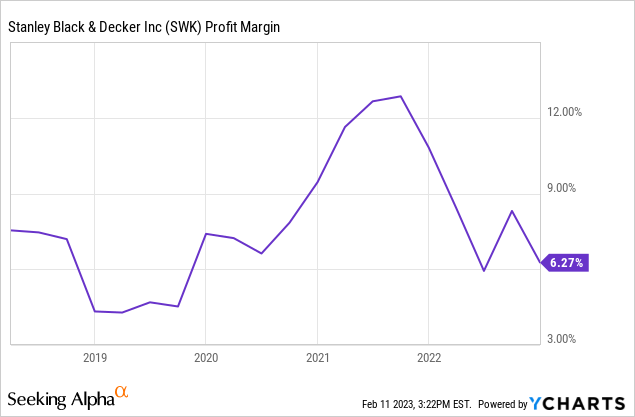

The firm’s net profit margin has been quite volatile in the recent years. Despite the sharp improvement in 2020 and 2021, the margin has contracted substantially in 2022. We believe that the macroeconomic headwinds in the prior year have been playing a major role in this development. Energy- and raw material prices, along with transportation costs have been skyrocketing. Inflation and interest rate hikes have also had significant negative impacts. As a result, consumer confidence in the United States has fallen to historic lows, resulting in lower demand for non-essential durable goods, like the ones SWK is also selling. The company has summarised the impact of these factors:

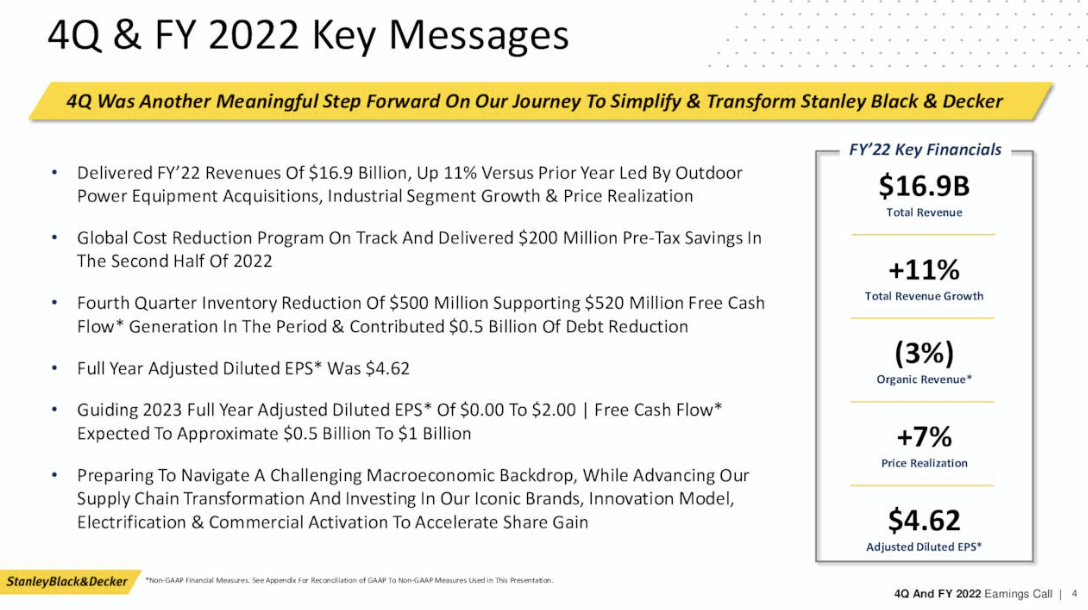

Gross margin for the quarter was 18.9%. Adjusted gross margin* was 19.5%, down 950 basis points from prior year, as price realization was more than offset by commodity inflation, lower volumes, and higher supply chain costs, including the impact of planned production curtailments. The impact from production curtailments and destocking high-cost inventory reduced gross margin by approximately 6 to 7 points.

While the sales have increased in 2022, the demand has actually fallen substantially. SWK manage to offset the lack of demand by an acquisitions and by pricing. The divestiture of the oil and gas division has also had a minor negative impacts.

Net sales for the quarter were $4.0 billion, flat versus prior year as strategic outdoor power equipment acquisitions (+7%) and price realization (+7%), were offset by lower volume (-10%), currency (-3%) and the previously announced Oil & Gas divestiture (-1%).

Q4 and FY22 results (SWK)

So what do we expect going forward?

In our opinion, the macroeconomic environment has already started normalising. Consumer confidence has bounced back significantly from its 2022 lows. While the rate of improvement may slow, we do not believe that it will retest the 2022 levels. As a result, we expect the demand for SWK’s products to improve in the coming quarters, especially towards the second half of the year. This can definitely have a positive impact on the sales.

Further, energy prices have also fallen from their highs, therefore we expect improvement in certain costs, which could have a positive impact on the margins.

As SWK is generating substantial revenue outside of the U.S., currency related headwinds have also been hurting the firm’s financial performance in the prior year. The relative strength of the USD, however, has fallen rapidly from its 2022 peak, therefore we expect the impact to be much less severe in 2023.

The company is also working towards reducing its costs and has several initiatives ongoing. They have made the following comment on the progress in the latest press release:

The Company advanced a series of initiatives designed to generate cost savings through corporate simplification and inventory reduction, with the ultimate objective of driving long-term growth, improving profitability and generating strong cash flow. These initiatives are expected to optimize the cost base and fund investments to accelerate growth in the core businesses. The execution of these initiatives remains on track and the Company expects these initiatives to generate cost savings of approximately $1 billion by the end of 2023 and grow to approximately $2 billion by 2025.

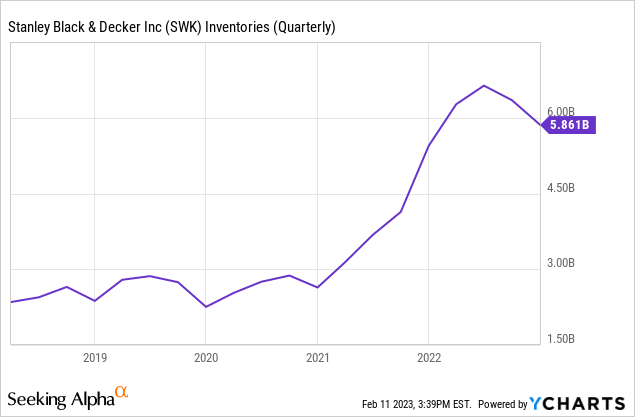

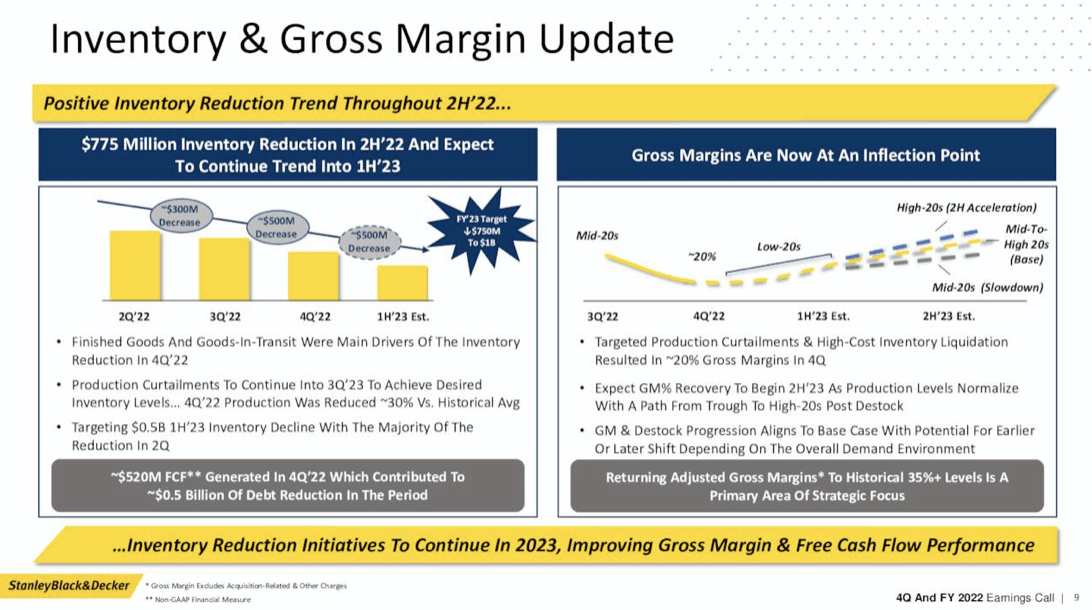

They have also indicated their intention to reduce inventory and they have managed to do it to a certain extent.

[…] the Company reduced inventory by approximately $500 million sequentially versus the prior quarter and expects further inventory and working capital reductions to support free cash flow generation in 2023.

While the initiative is good, inventory levels are still extremely high.

We would like to see it come back to pre-pandemic levels. There is one significant problem with it, however. Often, the reduction of inventory can only be achieved by high promotional activity and discounting, which could have a downward pressure on the company’s margins in the coming quarters. The firm is somewhat more optimistic, expecting gross margin expansion to start already in the first half of 2023.

Inventory and gross margin update (SWK)

All in all, we believe that from a macroeconomic point of view, the margins are likely to have a positive development in 2023, but from a company-specific perspective, further contraction may be likely. For these reasons, we remain cautious right now. Our view is neutral on this profitability measure.

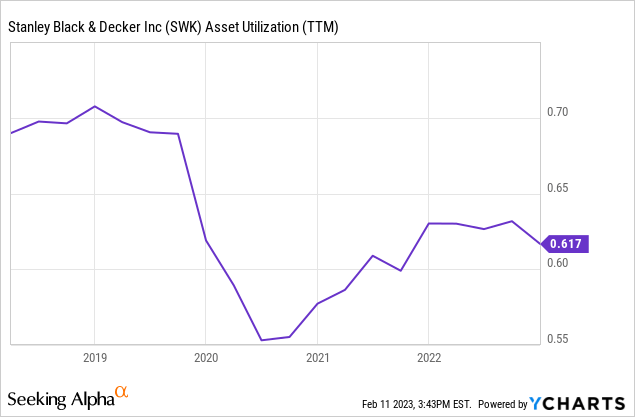

Asset turnover

Asset turnover, or sometimes called asset utilisation, is a measure of efficiency. It measures how efficiently the firm uses its assets to generate revenue.

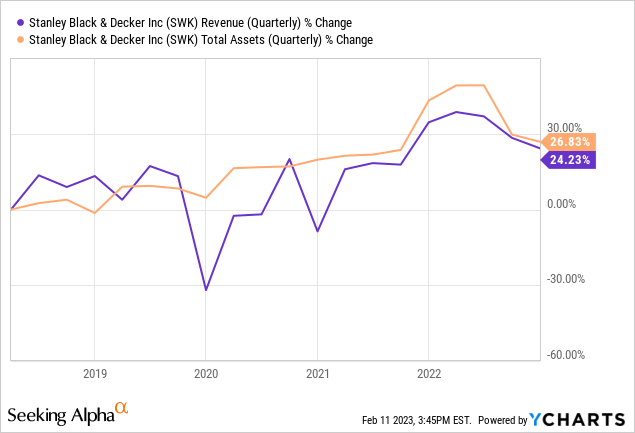

SWK’s efficiency appears to have declined materially compared to pre-pandemic levels, despite the improvement in 2021. The primary reason for this has been the sharp decline in revenue growth, which has been induced partially by the pandemic. At the same time, total assets kept growing.

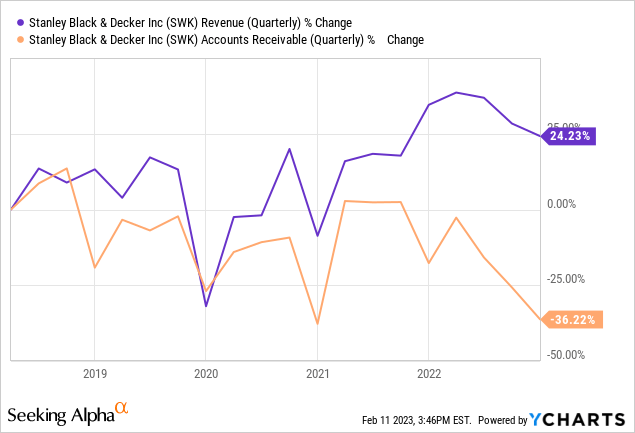

When we evaluate this measure, we usually like to compare the growth of the revenue with the growth of the accounts receivable. It can often be a warning sign if the accounts receivable grow faster than the revenue. It could potentially signal aggressive accounting practices or increased sales on credit, which could be an indication of “pulling demand forward” from future periods. Fortunately, this is not the case for SWK.

Once again, the recent improvement is a positive sign, but we would like to see the efficiency coming back to pre-pandemic levels before we would turn more bullish.

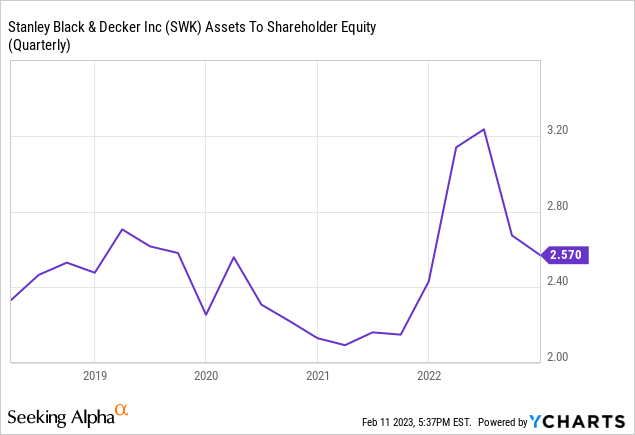

Equity multiplier

Equity multiplier is the ratio of assets to shareholder equity. It shows how much of the firm’s total assets are supported by equity.

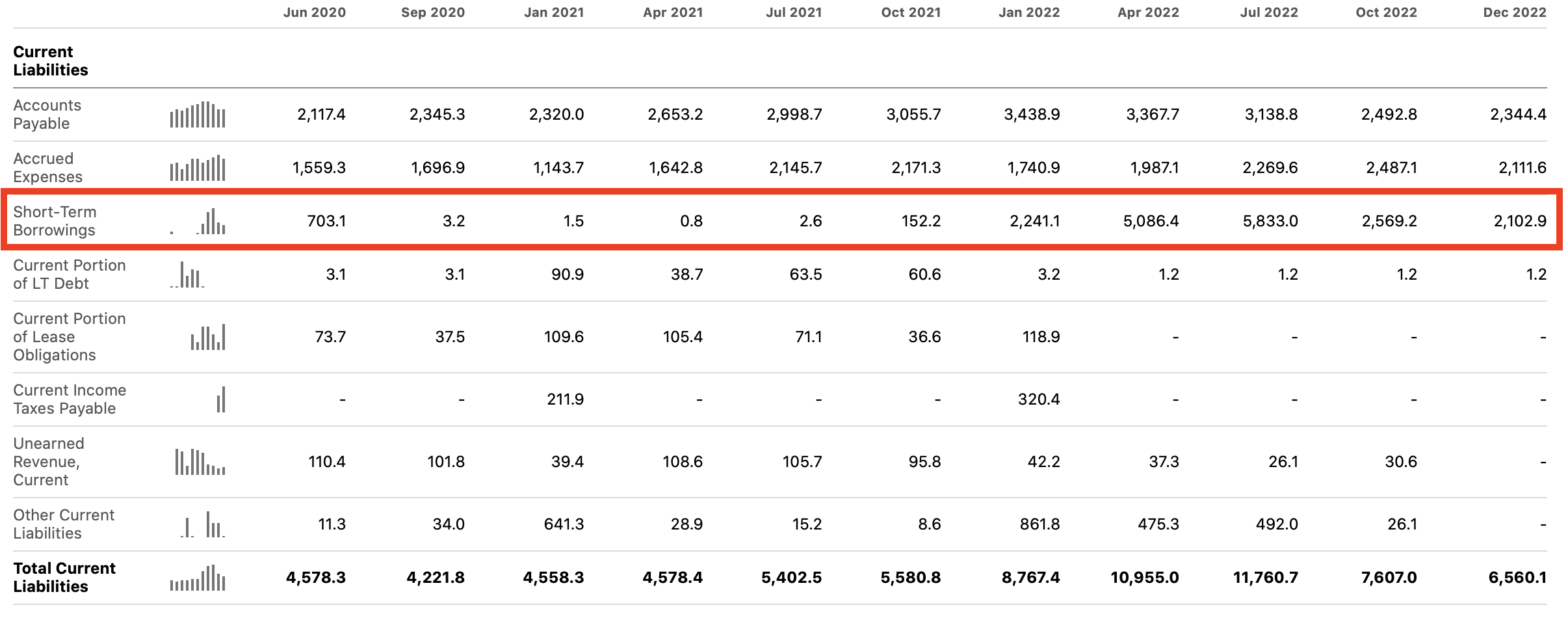

Just like the other measures, SWK’s equity multiplier has been also quite volatile in the prior years. Although it increased rapidly in the first half of 2022, it started to normalise towards the second half of the year. The explanation for this behaviour can be found when we take a closer look at SWK’s balance sheet. Short-term borrowings have gone up extremely high in the first two quarters of 2022.

Current liabilities (Seeking Alpha)

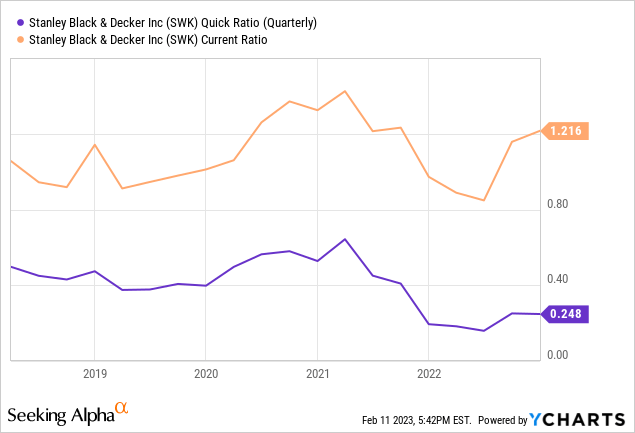

In turn, the company’s liquidity ratios have also been hurt. Two of the most popular liquidity ratios are the current- and the quick ratio. Both measure whether current assets are sufficient to cover current liabilities, however the quick ratio excludes the inventory from the calculation.

We can see that over a long time horizon, the current ratio has been actually improving, however, largely due to the inventory management problems, the quick ratio has not exhibited a similar trend.

To put this into perspective, the following table shows SWK’s industry peers and their quick ratios. SWK has the lowest among them all. We would definitely like to see this liquidity measure improve, before we consider upgrading our rating.

Comparison (Seeking Alpha)

If SWK manages to remain on track with its transformation plan, as well as with its inventory reduction plan, we may soon see an improvement in liquidity.

To sum up

SWK’s net profit margin has been declining sharply since the beginning of 2022. Macroeconomic factors, including elevated energy and raw material prices, along with low consumer confidence and an unfavourable FX environment, have been playing a role. Going forward, we expect these headwinds to diminish, which could lead to improved sales and expanding margins from the second half of 2023 onwards.

The firm’s efficiency has also declined from pre-pandemic levels, largely due to the decline in sales, while assets kept increasing.

We would like to see SWK’s liquidity improve before we would consider upgrading to “buy”. The inventory reduction plan may contribute to this improvement in the near future.

For these reasons, we maintain our overall neutral view.

Be the first to comment