sturti

Main Thesis & Background

The purpose of this article is to evaluate the Nuveen AMT-Free Quality Municipal Income Fund (NYSE:NEA) as an investment option at its current market price. This is a multi-state, closed-end fund with an objective “to provide current income exempt from regular federal income tax and the alternative minimum tax applicable to individuals by investing in an actively managed portfolio of tax-exempt municipal securities.”

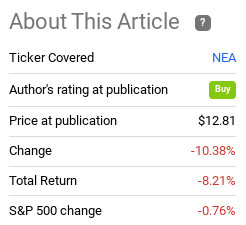

I have owned NEA for a long time and wrote about it last summer. At that point, NEA has been in a consistent downtrend and I believed a bounce may be forthcoming. Unfortunately, I missed the mark here, as NEA continued to decline and has delivered a negative return in the interim:

Fund Performance (Seeking Alpha)

This is not a comforting graphic, but I do think it signals that NEA could have plenty of room to push higher if the price action normalizes. What I mean is, the fund took a tremendous beating in 2022 and has only partially recovered. With fixed-income getting a nice boost in the short term, there could be room to run for the sector and still-beaten-down funds like NEA in particular. In this vein I see merit to maintaining a “buy” rating – and I will explain why below.

Income Cuts Weighing On Investors’ Minds

I have been a long-term holder of NEA and a bull for quite some time. I don’t want to ignore this and will be upfront in noting I got this call wrong. While the Q4 and subsequent 2023 rally in fixed-income have given some relief, the fact is I saw the weakness mid-year as a buy signal that was much too early. The Fed stayed aggressive, inflation accelerated (what happened to “transitory”), bonds remained unloved.

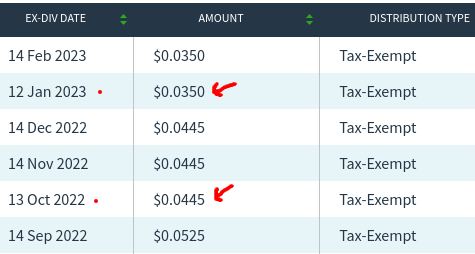

All of these factors pressured NEA as well and could continue to do so if we see an uptick in inflation figures and/or the Fed ends up being more hawkish this year than currently expected. Beyond those macro-events, NEA has also come under fire for two distributions cuts in the near term. While October’s cut was not a surprise, the fact that a second cut came soon after in January did not exactly jive with my expectations:

Recent Distribution Cuts (NEA) (Nuveen)

This is a fundamental development readers need to be aware of. NEA still has a reasonable yield in my opinion, once taxes are factored in. But these cuts have taken their toll. The overall yield is down and investor confidence is shaken. This is just one of a few headwinds that will pressure this CEF in the next few quarters and readers should evaluate this carefully before deciding if NEA is indeed a fund they want to own right now.

Fixed-Income Has Enjoyed A Relief Boost

I do want to point out that while 2022 was a year to forget for fixed-income investors, 2023 is off to a better start. This includes IG and high-yield credit, munis, treasuries, and corporate bonds. Simply put, NEA has seen a rebound since its 2022 lows, but the broader fixed-income market across the board has been posting gains:

YTD Performance (Various SPDR funds) (Google Finance)

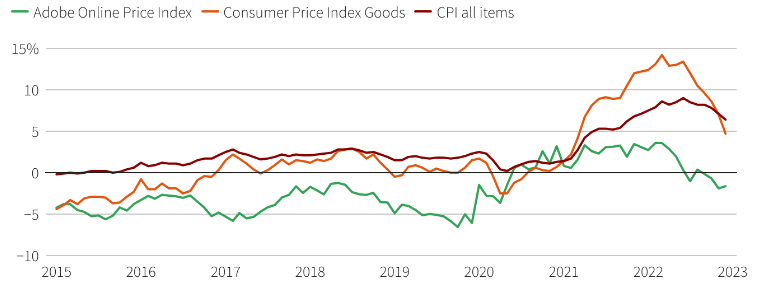

This is due to the macro-environment. The Fed has taken to smaller (.25 basis point) rate hikes that are less hawkish than what we saw in 2022. Inflation has also been falling – which is giving fixed-income investors confidence that the yields they are able to lock in today are going to be attractive longer term:

Inflation Metrics (Adobe)

As inflation has come down to more manageable levels, so too have Fed rate hike expectations for the future. This, in turn, has led to NEA recouping some of its lost ground:

1-Month Move (NEA) (Google Finance)

This is important for understanding why I like NEA. Under these circumstances, many bonds are seeing an increase in value, so deciding whether or not to buy munis really comes down to relative attractiveness. One could buy treasuries or corporate bonds using the same logic – that lower inflation and fewer interest rate hikes will boost them too.

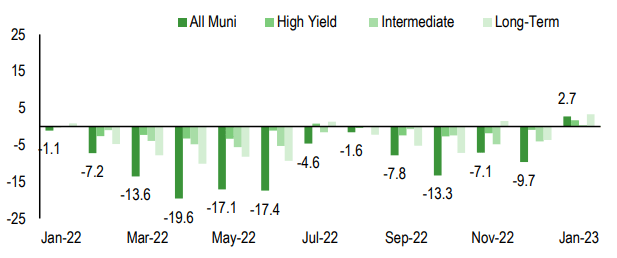

So, why like munis (and NEA by extension)? For me, it mostly comes down to tax-free income. As a working professional, shielding as much income as I can from Uncle Sam makes sense. For those in low tax brackets and/or who are retired it may not make as much sense. But to those who are drawn to munis, they may garner confidence from seeing how market sentiment has shifted. After 2022 saw consistent outflows in the sector and resulted in sustained losses, January saw a marked shift. The sector experiencing robust inflows that show why the bleeding stopped in muni CEFs for the most part:

Fund Flows (Munis) (Lipper)

Given how last year saw near-record outflows, I think there is still time to front-run continued investor interest in this space. One month does not make a trend, but it does encourage me that the worst is over. Buying in now still gives readers a reasonable entry point and time to profit off a broader, longer-term rotation back into the sector. This is critical for my “buy” thesis.

The Valuation Is Hard Not To Like

Looking at NEA specifically, one attribute that definitely piqued my interest at these levels is valuation. My long-term followers know that this always plays a key role in my buy/hold/sell decisions, and NEA is not unique in this respect.

Over time this fund tends to trade at a discount. During the boom time of 2021 that narrowed to near par – but that reality didn’t last long. Generally, NEA will trade in the 5 – 12% discount to NAV range which gives me comfort when buying in. Back in July, this discount was on the narrower end around 6%. I still viewed it favorably, but we know how that turned out. Today, by contrast, that discount is almost twice as wide at over 11% to NAV:

Fund Stats (Nuveen)

The takeaway here is straightforward. NEA is very attractively priced on the surface and by its historical trading pattern. While this doesn’t guarantee strong (or even positive) returns in the future, it does help limit downside prospects because the discount can only get so wide before value investors step in. I think we are at, or nearing, that level, and see it as supporting a buy case at the moment.

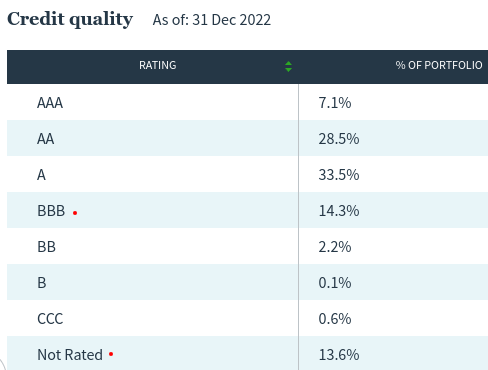

NEA Is Filled With Mostly Quality Debt

Another point of emphasis is that when I invest in credit/debt securities I tend to focus on the investment grade realm. I do own some junk debt exposure, but that is very limited in my overall portfolio. NEA fits in with this objective because the fund is heavily tilted towards the highest rungs on the credit ladder. While roughly 1/3 of its debt is below A-rated, about half of that remaining balance is still IG-rated, at BBB. Further, a substantial portion of that balance is non-rated, which can vary in quality:

NEA’s Credit Quality (Nuveen)

What I am getting at is that NEA does pump up its yield a bit with some junk and non-rated debt, but it is a reasonable amount. Some of the BBB-rated debt comes from Illinois – more on that below – but the other two-thirds of the portfolio comes with strong credit marks. This is fundamental to my personal investment strategy and a key reason for why I will look to add to this exposure in particular in what could be a challenging 2023 economically.

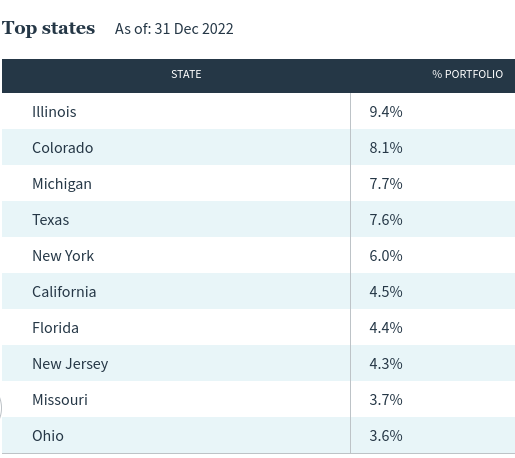

Not In Love With The Illinois Weighting

I will wrap up this review with another cautionary tale. This one concerns Illinois, which has long been a thorn in the side of the muni sector in relative terms. As mentioned, this is where some of the lowest IG rated debt within NEA’s portfolio comes from as the state happens to be the largest individual contributor to the fund. At over 9% of total holdings, it has a big impact:

NEA’s State Breakdown (Nuveen)

Quite frankly this is not something I view positively. It is balanced out by the fact that the fund is still rounded out with a plethora of different state exposure. No single state is too overweight this fund – so that helps. A drawback for me personally is the North Carolina exposure has been slimmed down a bit. A few years ago NEA absorbed a North Carolina-specific muni fund from Nuveen, and that amplified the state’s exposure in this particular fund to around 5%. As a NC resident, that piqued my interest. Unfortunately, over time this has dropped to around 3%. Coupling that with the above-average Illinois exposure and that explains why this is just one of several muni funds that I own.

This may beg the question – if I am not keen on Illinois debt, why do I still own this? Beyond the broader diversification that I just mentioned, another reason has to do with some progress Illinois has made in the short term. While this state may never be known for fiscal responsibility, the latest budget proposal has two line items that improve the backdrop for muni debt issued by the state:

Illinois’ Budget Proposal Line Items (Illinois Government)

What this is showing is state is going to pump $500 million in to a “pension stabilization fund”. This is significant for two reasons. One, it is the first time Illinois has made a contribution to a reserve fund in almost twenty years. Two, soaring pension liabilities are notoriously bad for Illinois. Only a handful of other states even come close to their predicament (think New York and New Jersey) and therefore any step in the right direction on this front provides some comfort that the state government is willing to take some much-needed action.

The next line item is a payment of $900 million to the general “rainy day” fund. This helps support the prices for GO bonds because it means there are reserves on hand to pay debt and interest in case the state runs into fiscal trouble – which it almost certainly will at some point in the future. Having this buffer gives investors some breathing room so that the state can make good on their obligations while continuing to fix structural problems.

I want to be clear that I am not a cheerleader for Illinois’ muni debt. I see these as signs of progress, but it will take more than that to truly love this state exposure. Still, with such a heavy weighting in NEA, seeing these steps allow me to feel comfortable continuing to own this fund without having to find a replacement in the immediate future.

Bottom Line

NEA was a drag on my portfolio last year but there were plenty of investments I had in that company. Looking ahead, I think the fund is long overdue for a rebound and I am looking to build on to my position on any forthcoming weakness. I was fooled on this strategy last year and as the adage goes “fool me twice, shame on me”. If I’m wrong again, I will have to dig deeper into why this seemingly quality fund is not performing. But 2022 was a down year for fixed-income broadly, and recent positive momentum for this fund suggests the worst is over. Therefore, I stand by a “buy” call on this CEF and I hope this gives readers some productive food for thought going forward.

Be the first to comment