Introduction

Back in January, I was positive about SSR Mining’s (SSRM) performance, as the company was combining a strong gold output with the strengthening gold price. Its shares nosedived in the first few weeks of the COVID-19 scare, but have since regained all of the lost ground thanks to the gold price, currently trading at around $1700/oz. However, two of the three producing operations are now (temporarily) closed due to the COVID-19 pandemic.

A quick look at the 2019 financial performance

While the novel coronavirus has a big impact on the 2020 guidance which had to be withdrawn after two mines were shut down, it does make sense to have a look back at the FY 2019 results, as these provide a good overview of SSR Mining’s potential in normalized circumstances.

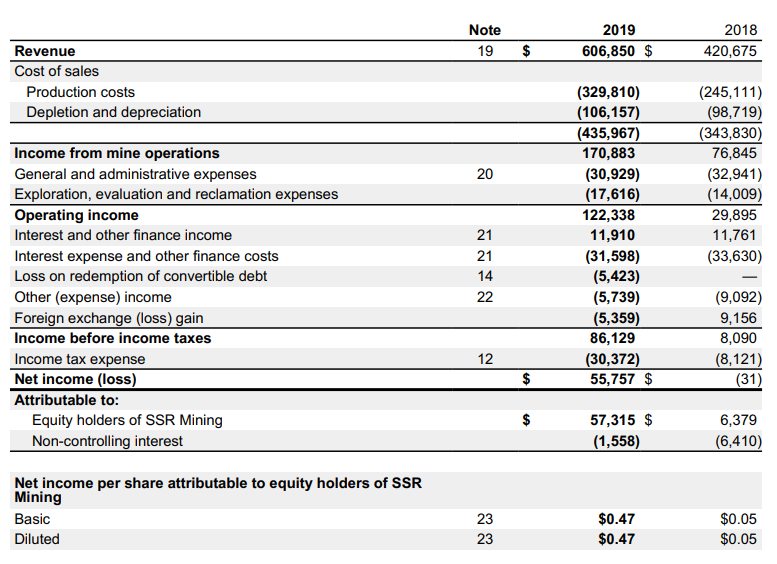

Selling a total of 421,828 ounces gold-equivalent resulted in a total revenue of $607 million and an income from mine operations of approximately $171 million, which is more than twice as much as the mining income in 2018. Additionally, SSR Mining was able to reduce its G&A expenses but spent a little bit more money on expenses exploration, and this resulted in a fourfold increase of the operating income to $122.3 million.

(Source: Financial Statements)

With a pre-tax income of $86.1 million and a net income of $55.8 million, SSR Mining clearly performed much better in 2019 compared to 2018. From this year on, the finance expenses should decrease as SSR Mining repaid its 2.875% convertible notes in full, thereby saving approximately $3 million per year.

Cash flow-wise, 2019 also was a good year for the company. It generated an operating cash flow of $134 million, but this includes a $61 million investment in the working capital and excluded a $1 million lease payment. So, on an adjusted basis, the operating cash flow was approximately $194 million (based on an average received gold price of just $1394/oz), and $204 million if you include the interest received on the sizeable cash balance of in excess of half a billion dollars.

(Source: Financial Statements)

The total capex in FY 219 was just below $136 million, so SSR Mining generated a free cash flow of approximately $68 million, approximately $0.55/share. Using a gold price of $1700/oz, the free cash flow (on an after-tax basis) would have almost doubled to $1.10/share, indicating the company’s cash flows should react very well to a higher gold price.

2020 remains uncertain, as two producing mines have shut down

Originally, SSR Mining anticipated to produce approximately 425,000 gold-equivalent ounces, of which roughly 80% was expected to be gold (with the rest of the gold-equivalent output consisting of silver and base metals from the Puna Operations in Argentina).

In the previous article, I also mentioned the sustaining capex was estimated to come in at $134 million (consisting of $90 million in capex and $44 million in capitalized stripping costs), and based on the strong production results and relatively low sustaining capex (just over $300/oz), I expected SSR Mining to generate a strong cash flow this year.

But then COVID-19 hit, and the mining sector wasn’t exactly immune. On March 19th, the government of Argentina forced mining companies to shut down, so SSR Mining’s Puna Operations had to wind down. SSR Mining also shut down its Seabee operation in Canada just one week later, which means the Nevada-based Marigold mine is now the only operating mine, and the cash flow coming from Marigold now needs to support the entire company.

(Source: Company Presentation)

The Q1 production results were still decent (as the Puna Operations and Seabee operations only shut down towards the end of the quarter) with a gold-equivalent output of 107,000 ounces, thanks to good performance at Seabee (29,500 ounces recovered from high-grade mill feed) and Marigold (almost 58,500 ounces of gold). But as you can imagine, the company had to withdraw its full-year guidance until it has a better idea of when the mines can reopen and how production will ramp up.

Investment thesis

SSR Mining will definitely benefit from a higher gold price, and the Marigold mine will very likely generate an outsized amount of free cash flow. Shutting down the Puna Operations doesn’t appear to have a very negative impact given the weak silver and base metal prices, but it is a pity that the Seabee mine was also shut down, as this reduces the company’s exposure to “pure” gold.

SSR Mining is a well-managed company that will surely get through this situation (it had a net cash position of around a quarter of a billion and has since used $115 million of its $503 million in cash to repay a convertible debenture), but 2020 won’t be its best year. Trading at $17/share, SSR may be a little bit ahead of itself until we know when all mines will be fully operational again.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

NEW at ESCI: A dedicated EUROPEAN REIT PORTFOLIO!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment