bunhill

General Overview

If risk capital vintage 2022 was worth forgetting, nothing currently indicates 2023 will be any better. With US yield curve inversions across multiple maturities, current term structures scream outright recession. The only game in town remains guessing whether this will culminate in a soft landing or one which is plausibly more painful.

In any case, holding long equities right now appears premature, at least until the Federal Reserve breaks something and reverses rate hikes initially aimed at staving off inflation.

Koyfin

The short end of the yield curve has peaked as the Federal Reserve has taken actions to quell inflation. For several months now, the 3-month yield has been higher than the 10-year yield, drawing capital funds to money market accounts.

A softer landing is likely to come about should the Federal Reserve, satisfied with its efforts to quell inflation, lowers the front end of the yield curve. In this instance, the inversion corrects itself returning the yield curve to an upward sloping one, characteristic of late-stage economic expansions.

A hard landing is typified by a recession, destroying aggregate demand and forcing the Federal Reserve to cut policy rates. In this scenario, a lower front end of the yield curve is stimulative for equities returning once again the yield curve to its upwards sloping configuration.

But right now, a meaningful inversion of the yield curve exists, making it a difficult predicament, namely for retail money managers or funds whose investment policy statements dictate a continued presence in US equities regardless of risk sentiment.

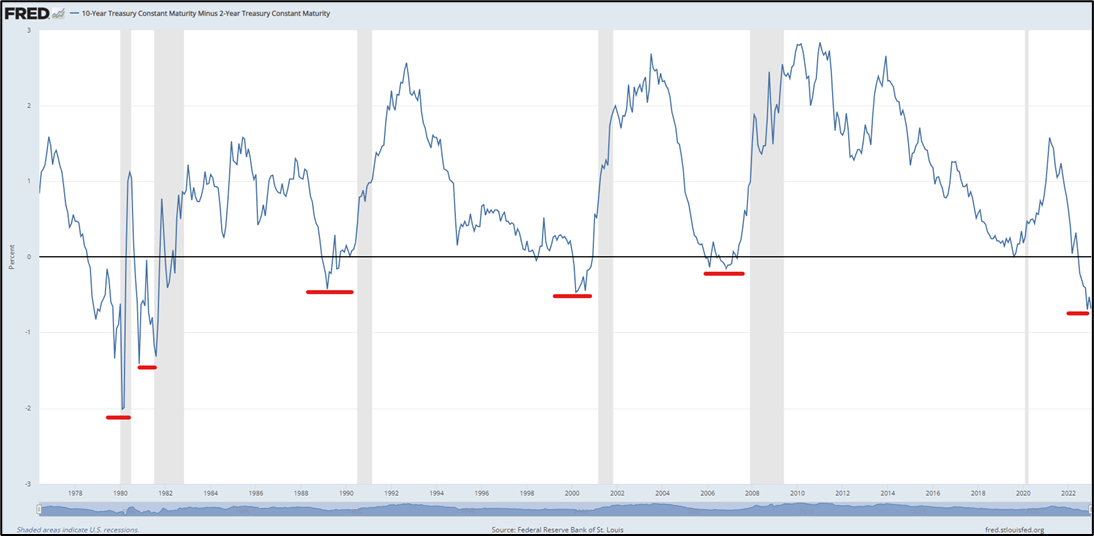

Federal Reserve Bank of St. Louis

10-year treasury constant maturity minus 2-year treasury constant maturity. Note that yield curve inversions have always preceded recessions (shading in grey). Data courtesy of Federal Reserve Bank of St. Louis.

Certain tactical trading tools do exist, like ProShares Ultra Short Russell 2000 ETF (NYSEARCA:SRTY) , aimed at allowing money managers to punctually hedge out risk exposure to a given index. Its imperfect at best but provides an additional tool in the ETF space worth discovering. Let’s find out more.

Product Overview

The ProShares Ultra Short Russell 2000 ETF provides investors an aggressive one-day directional bet on Russell’s celebrated index of 2000 small-cap US firms.

It tracks 3x inversely correlated returns on the Russell 2000, signifying that 1% gain in the Russell 2000 equates to a -3% daily return for a holding of the SRTY. Its imperfect like all other leveraged ETFs, as daily resets and compounding impact returns on holdings greater than a day.

Accordingly, its best suited to tactical trading or hedging off long risk exposure to the Russell 2000 (IWM).

Leveraged ETFs often are comprised of synthetic underpinnings (often treasury bill futures contracts, index swaps or currency futures) making expense ratios more costly (0.95%) and structural risks intrinsic to fund make-up more important. This ETF is no different, and forms part of a group of exotic leveraged ETFs that are considerably different from the plain vanilla ETF variants we are all familiar with.

Funds destined to tactical trading also generally have higher fund turnover, often complimented by an options market used to customize risk exposure. In this instance, SRTY which has been marketed for over a decade, holds around $176M in assets under management.

To put this into perspective, the famed Russell 2000 Index ETF posts around $52B in assets under management, highlighting how marginal leveraged ETFs often are.

Understanding the Russell 2000 holdings provides traders a good idea of when to use products like SRTY to hedge out risk. The index of 2000 small US equities has a relatively even spread of sectors, with health care (+16.61%), financials (+16.10%) and industrials (+15.47%) dominating.

Smaller cap equities are also generally more prone to volatility, implying outperformance in bullish market environments and underperformance in bearish ones. The present market environment, particularly given tell-tale signs of a pending recession, is not well suited to positioning in the Russell 2000.

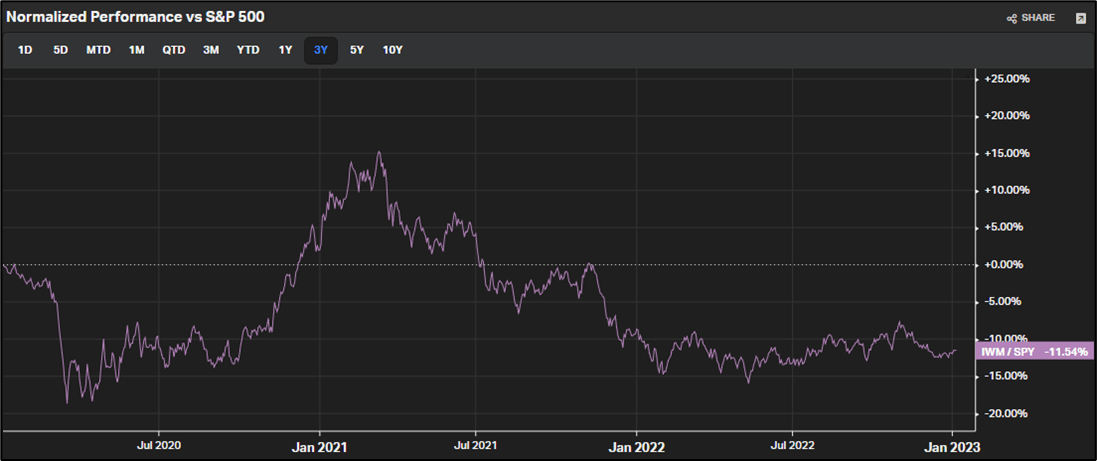

Koyfin

Over the past 3 years, the Russell 2000 has generally tended to underperform the S&P 500. As a rule of thumb, the ETF outperforms in resoundingly bullish environments but tends to underperform in bearish ones.

Product Structure

As mentioned earlier, holdings in SRTY are synthetic and made up of predominantly of over-the-counter derivatives. This implies counterparty risk between financial intermediaries used to trade the derivatives making up the fund. While not an absolute showstopper per se for recourse in using the ETF, it is worth noting the importance of derivatives used to artificially provide required leverage.

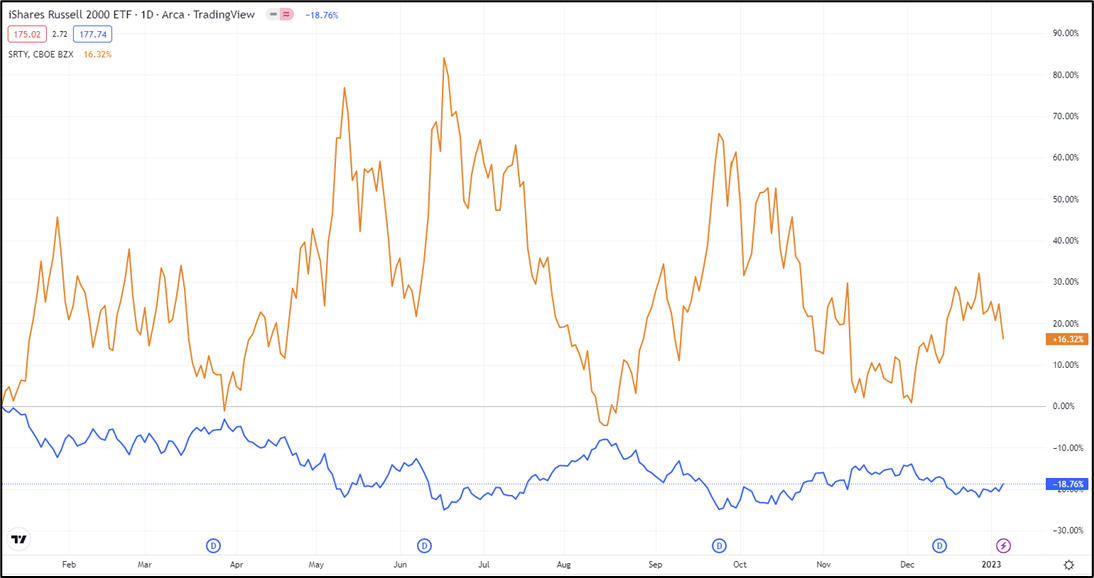

Tradingview

A one-year total returns comparison between IWM and SRTY shows just how volatile SRTY is. Over longer holding periods, the fund does not match -3x returns on IWM. In 2022, the fund delivered +16.32% against IWM which lost -18.76%.

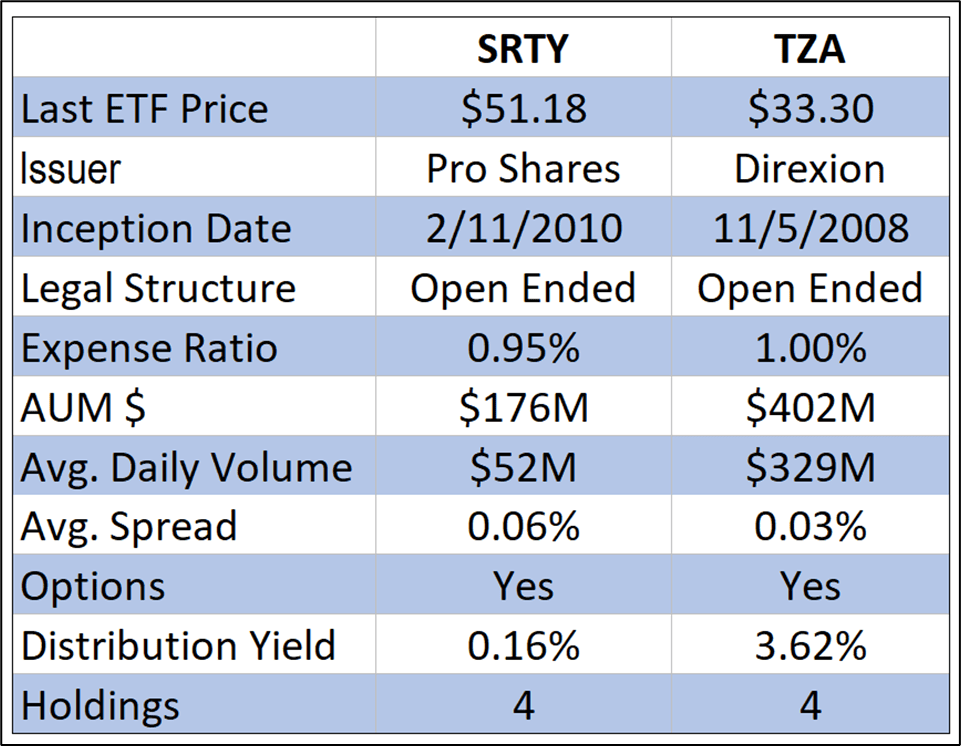

Spreadsheet developed by author

Comparative analysis SRTY v TZA

Risks

Key risks linked to holding leveraged ETFs can be summarized in product structure. OTC derivatives are the main ingredient allowing the structure to deliver the required leverage and with this comes counterparty risk.

For traders holding the ETF for anything longer than one day, daily resets and compounding will distort returns and provide only an imperfect -3x hedge on returns of the Russell 2000. The US small cap index tends to outperform in highly bullish environments and underperform in bearish ones making price movements perhaps more volatile than larger indices.

Key Takeaways

SRTY is Pro Shares take on a -3x leveraged tactical trading ETF used to speculate on movements in the Russell 2000 or hedge out a long holding that you perhaps do not wish to close. Like all exotic leveraged ETFs, it comes with a range of pitfalls – OTC derivative contracts are required to provide the fund its characteristic leverage and with that comes risk. Daily resets and compounding are among them, making this product only useful over a short time horizon.

The fund is an alternative to the more popular TZA (Direxion Daily Small Cap Bear 3x shares) but appears to have garnered less interest. In any case, this here remains a marginal tactical trading tool best used over shorter periods rather than a buy-and-hold bearish bet on the Russell 2000.

Be the first to comment