Colin Anderson Productions pty ltd

As a dividend growth investor, I am always looking for fast-growing dividends. While most companies with high dividend growth also have minuscule starting yields, they can fuel income growth for years. The compounding effect of the fast growth can overtake a high-yield dividend with no growth in just a few years.

A prime example of this is Lowe’s (LOW). In 2013, Lowe’s was paying a 1.5% dividend and trading at a much higher valuation than today. An investor who bought in 2013 receives a 10.5% yield-on-cost, as the distribution has grown from $0.62 to $4.20 per share. Not to mention the significant capital gains as well. And, unlike most high-yield stocks, Lowe’s will realistically expect to see the dividend grow into the future, with additional price growth along the way.

Another fast-growing dividend has been Pool Corporation (NASDAQ:POOL). The company has traded at nose-bleed elevation for several years but is nearly 45% off its high. I decided it was time to take a closer look.

About Pool Corporation

As the name implies, POOL is in the business of installing and upgrading swimming pools, as well as selling supplies. While this is a relatively small market, it is very profitable. POOL has grown EPS by nearly 18% annually for the past 20 years.

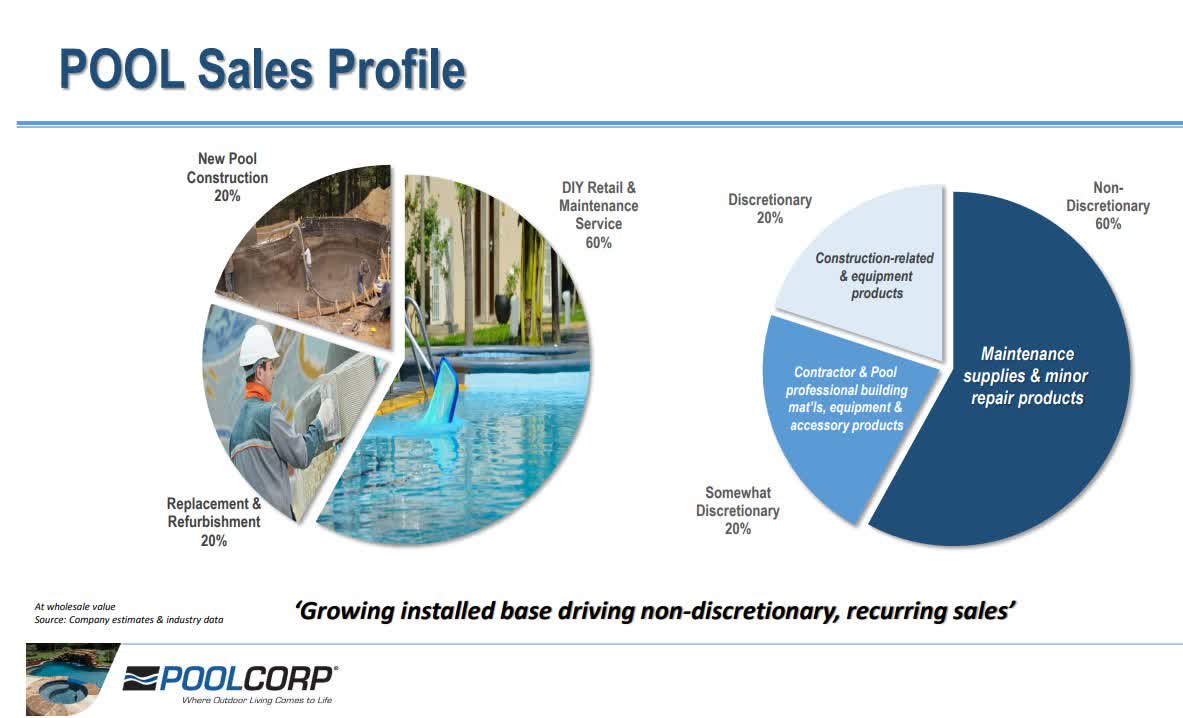

They receive approximately 20% of revenue from new installs, 20% from renovations and upgrades, and 60% from recurring sales of supplies. This is shown in the slide below from a company presentation.

POOL Corporate Website – poolcorp.com

Dividend Growth History

With a twelve-year dividend growth streak, the company is a dividend contender. The company has a 10-yr dividend growth rate of 18% and a 5-tr growth rate of 20%. The most recent increase was 25% in May of 2021. This accelerating growth rate is unusual for such a fast-growing dividend, as growth rates tend to slow with time. A 20% growth rate equates to the doubling of the dividend about every 3.6 years.

The company first established the dividend in 2004. While the distribution has never been cut, it was frozen during the Great Recession. Finding companies that made it through the 2008-2009 recession without cutting dividends is a plus. While payout ratios jumped during this time, they never reached excessive points thanks to the company maintaining a low payout ratio.

Payout Ratio

Throughout its dividend history, POOL has maintained low payout ratios, which is not easy when the dividend is quickly growing. This ability shows that the earnings and cashflows have also been quickly increasing.

In the past, the company has always maintained a steady 35% payout ratio on adjusted earnings. This has fallen sharply in recent years, thanks to the post-pandemic boom in their business, and stands at 20% today. Additionally, operating cashflow payout ratios have been steady at around 30%, while free cashflow ratios have improved over the past several years.

Everything about the payout ratios indicates the dividend is well-managed and positioned to weather an economic downturn. At the Great Recession low, the payout ratio rose to 54%. At today’s dividend rate, the earnings would need to collapse by nearly 65% to reach this point again.

Valuation on Yield

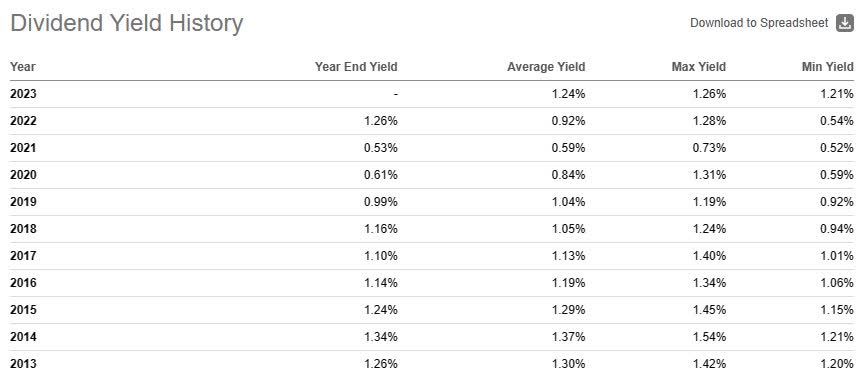

Today, POOL yields around 1.3%. While this may seem paltry, it is not unusual for a fast-growing dividend, and significantly higher than it was just a couple of years ago. However, it is nothing exceptional compared to the max yields available over the past ten years. This is shown in the yield table below.

Seeking Alpha

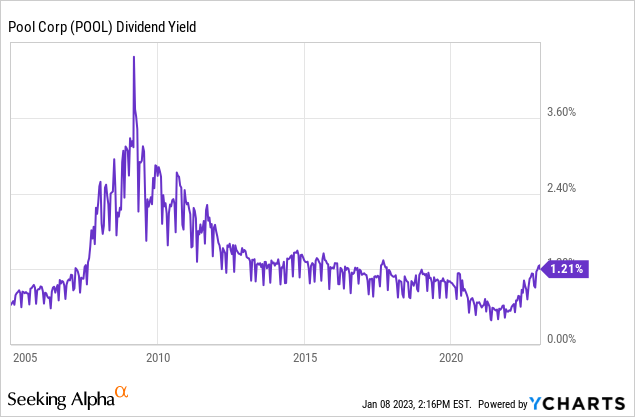

Expanding the time frame, as shown in the yield graph below, offers that during the 2008-2009 recession, the yield spiked significantly, topping 4.5%. Based on this precedent, the market will probably punish POOL in a downturn.

While the company appears fairly valued today based on historical dividend yields, significant downside exists should a recession materialize. To match its yield during the 2008-2009 time, it would need to fall to about $90, a massive drop from today. However, looking at historical PE, a different story unfolds.

Valuation on PE

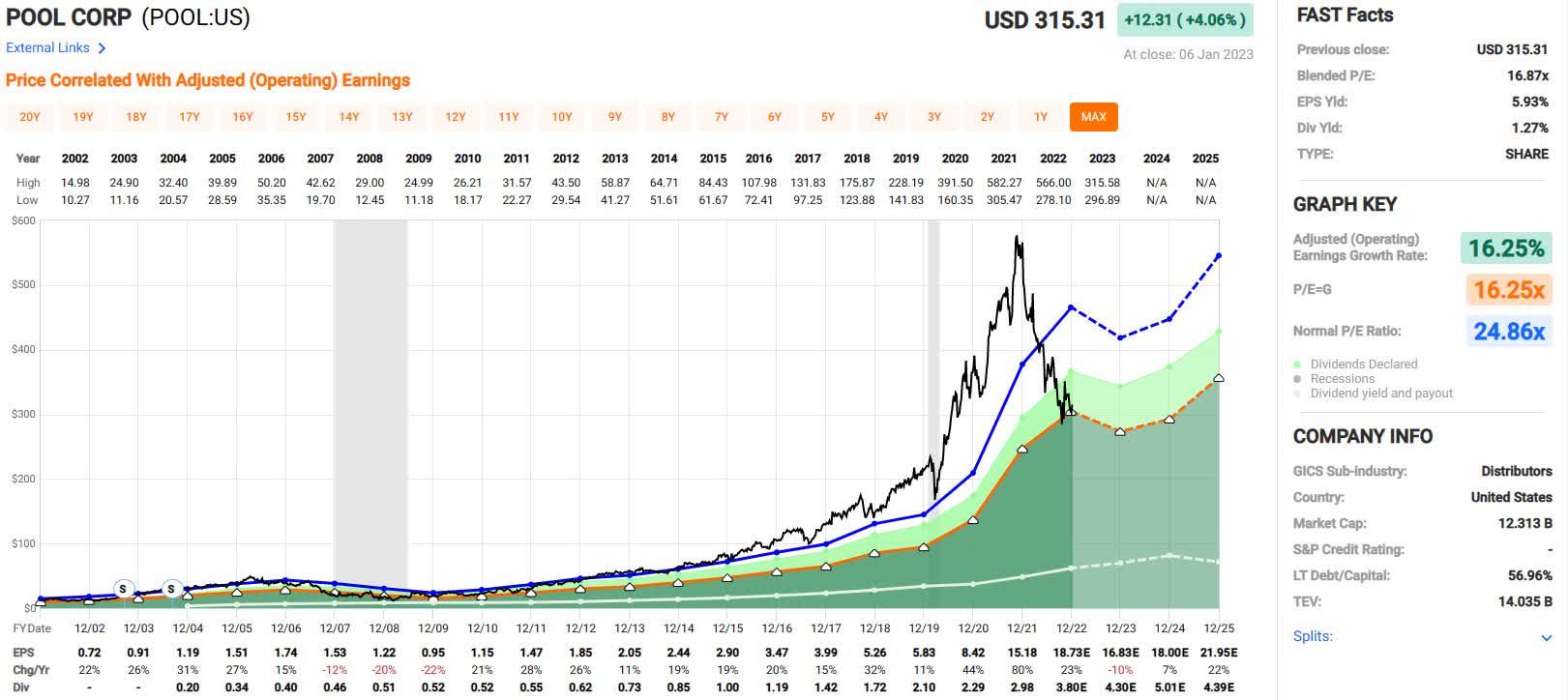

Today, POOL is trading at a PE of about 17. A much more reasonable valuation than the whopping 40 assigned to it a little over a year ago. In fact, this is better than the average PE over the past 20 years of around 25. The below-average valuation indicates the company may be a bargain right now. The Fastgraph below shows the average PE with the blue line and the price with the black line. Notice the massive overvaluation in 2021.

fastgraphs.com

Zooming in on the GFC timeframe tells a similar story to the dividend yields. The company’s stock fell over 75% from the middle of 2007 to early 2009, bringing the PE from 26 to under 10. For the company to reach a PE of 10 today, the price would need to fall to about $185, bringing the dividend yield to 2.1%. However, keep in mind that earnings are projected to be lower next year by about 10% before bouncing back in 2024.

fastgraphs.com edited by Wyo Investments

During the Great Recession period, the company’s earnings fell by a combined 45% over three years. Earnings estimates will likely fall sharply if a recession materializes.

Forward factors and risks

Clearly, swimming pools are a luxury item and would be susceptible to risk in a recession. Even with the steep fall from its highs, it doesn’t appear the market has fully accounted for a potential slowdown. Management has remained optimistic, so the next earnings will likely clarify the trends. Of course, management’s job is to be positive.

Currently, analysts expect a 10% decline in earnings for 2023. Based on the earnings declines during the Great Recession, this seems optimistic should a recession materialize. Considering the revenue mix of new construction (20%), renovation and upgrades (20%), and supplies (60%), I think a 20% decline would just be a starting point. Customers will scrap new projects, delay upgrades, and even push minor repairs and maintenance. Although, some of these can only be delayed for so long.

The company shows the average age of an install is 22 years. This indicates plenty of renovations and upgrades in the future. Additionally, each new install is a customer for ongoing maintenance supplies. The company has undoubtedly increased its recurring customer base since the last recession.

Conclusion

It is doubtful that the market is assigning significant recession risk to POOL at this time. While the company is trading at an attractive valuation versus historical, it is at risk of a steep fall in a recessionary environment.

Even though the company is better positioned than it was entering the Great Recession, it sells a product that is perceived as having a high risk of being cut from people’s budgets. I think it’s likely that market sentiment would hit the stock hard if we see a recession. Additionally, smaller cap companies tend to be punished more in downturns than larger ones, and with a market cap of around $12B, POOL falls into this category.

While POOL is a fantastic dividend growth company, the downside risk here is too much for me to enter a position. I don’t see it reaching a single-digit PE in a recession as it did in 2009, but I think it might get close. I will consider entering a position at a 2% yield, or $200. There is considerable upside potential if a recession doesn’t materialize, and this is a good entry point for a long-term investor.

Be the first to comment